Shopify is Quickly Climbing the Ranks of the Largest Small Business Funders

February 12, 2019Shopify originated $277 million in merchant cash advances in 2018, according to their quarterly earnings reports. That figure already places them among the largest small business funding providers nationwide.

Below is a look of how they stack up thus far:

| Company Name | 2018 Originations | 2017 | 2016 | 2015 | 2014 | |

| OnDeck | $2,484,000,000 | $2,114,663,000 | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 | |

| Kabbage | $2,000,000,000 | $1,500,000,000 | $1,220,000,000 | $900,000,000 | $350,000,000 | |

| Square Capital | $1,600,000,000 | $1,177,000,000 | $798,000,000 | $400,000,000 | $100,000,000 | |

| Funding Circle (USA only) | $500,000,000 | |||||

| BlueVine | $500,000,000* | $200,000,000* | ||||

| National Funding | $427,000,000 | $350,000,000 | $293,000,000 | |||

| Kapitus | $393,000,000 | $375,000,000 | $375,000,000 | $280,000,000 | ||

| BFS Capital | $300,000,000 | $300,000,000 | ||||

| RapidFinance | $260,000,000 | $280,000,000 | $195,000,000 | |||

| Credibly | $180,000,000 | $150,000,000 | $95,000,000 | $55,000,000 | ||

| Shopify | $277,100,000 | $140,000,000 | ||||

| Forward Financing | $125,000,000 | |||||

| IOU Financial | $91,300,000 | $107,600,000 | $146,400,000 | $100,000,000 | ||

| Yalber | $65,000,000 |

*Asterisks signify that the figure is the editor’s estimate

Small Business Funding is Blasting Off

January 18, 2019Despite the pall of the record long partial government shutdown which has hurt brokers and funders of SBA loans, many companies and individuals in the online small business funding space are off to a very fruitful 2019. Below are some that we found.

After 15 years in the screen printing and embroidering business, Edward DeAngelis spent about four years learning the online funding business before creating Amerifi, a small business funding brokerage. Amerifi and DeAngelis, its CEO and founder, have had a very strong 2019 so far. Since January 1, DeAngelis said that Amerifi has facilitated $7,420,667 in funding. This is compared to $1,284,890 for the entire month of January 2018.

DeAngelis attributes this in part to his increasingly diversified product offering. Amerifi, located in Broomall, PA, offers term loans, asset backed loans, lines of credit and merchant cash advances, among other products. He said that he’s trying to develop a brand known for funding every deal, large and small. He also said that developing a solid team, which now includes eight salespeople, is very important.

“I’m not one for high turnover,” DeAngelis said. “I invest in my team. I spend plenty to provide good leads to all my guys and I treat my team well.”

DeAngelis said he provides his whole team with health insurance. Founded in March of 2017, Amerifi has so far brought nearly $49 million of funding to American small businesses.

Co-founder and CEO of Idea Financial, Justin Leto, said they have seen an uptick in volume starting in December of last year and carrying over into 2019.

“In the first week or so of December the volume wasn’t as high as we thought,” Leto said. “But then all of a sudden as we got to the end of the year, even up until New Year’s Eve when we thought there would be nothing going on at all, the volume was tremendous. And it wasn’t volume that we were just declining. It was really good paper coming in. And it has continued through January. The paper has been solid. The quality of the deals are very good.”

Idea financial, based in Miami, FL, provides a line of credit product, with 12 and 18 month repayment periods.

“We have a 650 minimum FICO, so we have to get the higher credit quality merchants,” Leto said. “And they’ve been coming. What I’ve seen is we have an approval for $100,000-$150,000 and it’s rare that anybody takes the full amount…If people are taking a percentage of the line and using it over time and continuing to draw over time for different projects, I think that’s a sign of a responsible borrower…I don’t see a recession coming.”

CEO of Accord Business Funding, Adam Beebe, told AltFinanceDaily that it was doing about double the amount in funding this month compared to last January. Completely ISO driven, Beebe said that submissions over the past month or so have been up 30 to 40 percent but couldn’t attribute it to any one specific thing.

Founded in 2013, Accord funds MCA deals exclusively and employs over 20 people in its Houston-based office. Last year, it made a key hire to expand its marketing efforts.

“I’ve had more deals in the last two weeks than during any other two week period last year,” said Jarret Ortmann, Senior Lending Officer at Ironwood Finance in Corpus Christi, Texas.

He also said that he’s been seeing more deals coming in from his brokers. Ironwood provides working capital, equipment financing and collateral lending.

Why Strategic Funding Rebranded as Kapitus

January 15, 2019 Today, Strategic Funding announced the launch of a new brand identity, including a name change. Strategic Funding will now be called Kapitus.

Today, Strategic Funding announced the launch of a new brand identity, including a name change. Strategic Funding will now be called Kapitus.

“We had a name that was very well respected,” said Kapitus founder and CEO Andy Reiser. “Everybody loved our name, quite frankly. They loved it so much, they all copied it. You can’t trademark ‘Strategic Funding.’ It’s too generic.”

Kapitus, spelled this way, is not a word in any language, which makes it easier to trademark.

“We wanted to separate ourselves in a way that is clearly identifiable,” Reiser said. “It’s an easy one-word name [that] symbolizes stability and strength. It’s ‘capital from us,’ if you want to break it down.”

Reiser said that the company has been relatively quiet over the last three years, but they have been advancing all along, and they are particularly proud of their brand new ISO portal. According to Reiser, the new portal helps ISOs better understand their book at Kapitus and allows brokers to generate a contract quickly without having to call them. The company has an in-house marketing team, but well over 50% of its business comes from the ISO channel.

Kapitus provides a variety of financial products, including equipment financing (they have an in house equipment leasing division) and factoring (they have a small internal factoring group). They also offer business loans, lines of credit and MCA deals. But the company’s largest portion of its business – more than 15% – comes from its Helix Healthcare Financing product, which finances healthcare practitioners like doctors, dentists and veterinarians.

Unlike other funders of healthcare practitioners that may offer financing terms up to 18 months, Kapitus offers terms of up to 10 years as long as the merchant satisfies its requirements. The company also funds a considerable number of healthcare-related businesses, like medical equipment providers. Otherwise, Reiser said that Kapitus has a diversified mix of merchants, from restaurants to manufacturers.

Reiser said that about 15% of Kapitus’s business consists of deals above $150,000 for which they have a seperate team. They do deals as high as $750,000.

When operating under the Strategic Funding name, there was a payment servicing division of the company, called Colonial Servicing. That entity will remain, but will be woven into the new Kapitus name.

Founded in 2006, Kapitus employs 240 people divided among three offices. The headquarters is in New York and there is an office with about 30 people in Arlington, VA, and a Dallas-area office with about 35 people working in collections and customer service.

Kabbage Finances US Small Business Customers of Alibaba

January 14, 2019 Kabbage announced today that it has partnered with Chinese e-commerce giant, Alibaba, to provide financing to small businesses that purchase materials on the platform. The financing program, offered by Alibaba and powered by Kabbage, is called Pay Later.

Kabbage announced today that it has partnered with Chinese e-commerce giant, Alibaba, to provide financing to small businesses that purchase materials on the platform. The financing program, offered by Alibaba and powered by Kabbage, is called Pay Later.

“Financing at the point of sale requires a fully automated solution that can handle the immense volume of daily transactions that occur on Alibaba.com,” said Kabbage CEO Rob Frohwein. “We are incredibly impressed with the service and value that Alibaba.com delivers to American businesses and want to do all we can to support their important mission.”

According to the Kabbage announcement, Kabbage had a beta launch of Pay Later in June 2018 and it has so far delivered millions of dollars in financing to American small business. The business to business (B2B) financing product provides lines of credit up to $150,000, and according to Kabbage, each purchase financed via Pay Later creates a six-month term loan for the merchant with rates as low as 1.25% per month. Kabbage also said that there are no fees to maintain the line of credit, no order transaction fees and no early repayment fees.

This partnership is not the first of its kind. In February 2015, Lending Club announced a similar arrangement with Alibaba that offered funding to U.S. small business owners for point-of-sale transactions on the platform. Lending Club offered loans up to $300,000 and had an exclusive relationship with Alibaba for point-of-sale business financing. Kabbage told AltFinanceDaily that their arrangement with Alibaba is not exclusive. Lending Club did not respond in time to explain their current relationship with Alibaba.

Is Small Business Lending Stuck in the Friend Zone?

October 23, 2018 Small-business owners have lots of places to go for capital, and the alternative small-business funding industry doesn’t exactly top the list, recent research shows. In fact, entrepreneurs claim they’re more than four times as likely to receive funding from a friend or family member than from an online or non-bank source.

Small-business owners have lots of places to go for capital, and the alternative small-business funding industry doesn’t exactly top the list, recent research shows. In fact, entrepreneurs claim they’re more than four times as likely to receive funding from a friend or family member than from an online or non-bank source.

That bit of intelligence comes from the National Small Business Association‘s 2017 Year End Economic Report, the most recent from the Washington-based trade group. Thirteen percent of the entrepreneurs who responded to the survey received loans from family or friends in the preceding 12 months, while 3 percent obtained funding from online or non-bank lenders, the report says.

But some variables come into play. Shopkeepers and restaurateurs are more likely to rely on friends and family for financing during their first five years in business, says Molly Brogan Day, the NSBA’s vice president of public affairs and a 15-year veteran of the survey. The association’s members, who account for many – but not all – of the respondents tend to have been in business longer than non-members so the actual percentage of all owners receiving funds from family or friends could well be higher than the survey indicates, she notes.

In fact, the average NSBA member started his or her business 11 years ago – a fairly long time for the sector, Day says. The association attracts well-established merchants partly because the trade group concentrates on advocacy and lobbying in the nation’s capital, Day notes. “There’s not a lot of networking, there’s not a ton of resources or educational offerings,” she says of the association. In other words, the organization’s emphasis tends to attract prospective members who have been in business long enough to see the results of laws and regulation instead of newcomers still struggling daily to establish themselves, she observes.

Anyway, it’s also worth noting that small-business owners appear nearly as likely to approach family or friends for cash as to petition large banks for funding, Day says, noting that 13 percent turn to friends and family, while 15 percent manage to obtain loans from large banks. To her, that indicates that banks just aren’t lending to small businesses as frequently as they should – a notion that should sound familiar to anyone in the alternative small-business funding industry.

Unsurprisingly, the association’s research indicates bank lending declined as the Great Recession made itself felt in 2007 and 2008. Before that, nearly 50 percent of merchants responding to the survey reported they had recently qualified for loans from big banks, small banks or credit unions, the research shows. “Now it’s pretty consistently a percentage in the low 30’s,” Day says. “People really need these loans.”

Lending by banks hit another snag in 2012 when new regulation and legislation, including the Dodd-Frank Wall Street Reform and Consumer Protection Act, made itself felt. “There was such a massive overcorrection in the banking industry that it’s still really difficult for small businesses to get loans,” Day says.

Moreover, banks were granting fewer “character-based” loans even before the double whammy or recession and regulation, Day observes. Instead of employing the older practice of assessing the intangible virtues of a business owner well-known in the community, bankers began applying a more formulaic approach to evaluating loan applications based on credit scores and other quantifiable variables, she says.

That switch to numbers-oriented decisions proved detrimental for many entrepreneurs. “A lot of small business owners don’t look great on paper,” Day admits. Even a great business plan might not convince bankers to loosen their purse strings these days, she notes.

That’s where the alternative small-business funding industry comes into the picture. NSBA researchers began including the category of online and non-bank lenders in their surveys in 2013 and have seen the percentage of respondents using them grow each year to its current level of 3 percent.

“It’s not huge growth, but it’s notable,” Day says. Notable enough to achieve importance, she continues. “It’s an important opportunity for your readers to fill that void,” she says of the shortfall of adequate small business funding. “They’ve been doing a pretty good job of doing it.”

In fact, the NSBA research indicates that alternative funding and other sources have tended to take up the slack created by the banking industry’s decision to exercise extreme caution when evaluating small business loans. Some 73 percent of small business owners are obtaining enough financing these days, according to the survey.

Yet hiccups have occurred, like the decline to only 59 percent finding adequate funding in 2010, Day points out. And the fact that two-thirds to three fourths are generally securing adequate funding means that a fourth to a third aren’t, she notes, adding that she urges focusing on the latter group. “It’s concerning,” she says.

Inadequate funding can prove especially challenging for newer businesses that don’t have a track record, haven’t stockpiled proceeds from past operations, don’t own stock to leverage and aren’t savvy enough to finesse placement of debt, Day maintains. More-established businesses have greater access to those resources or have honed those skills, she notes.

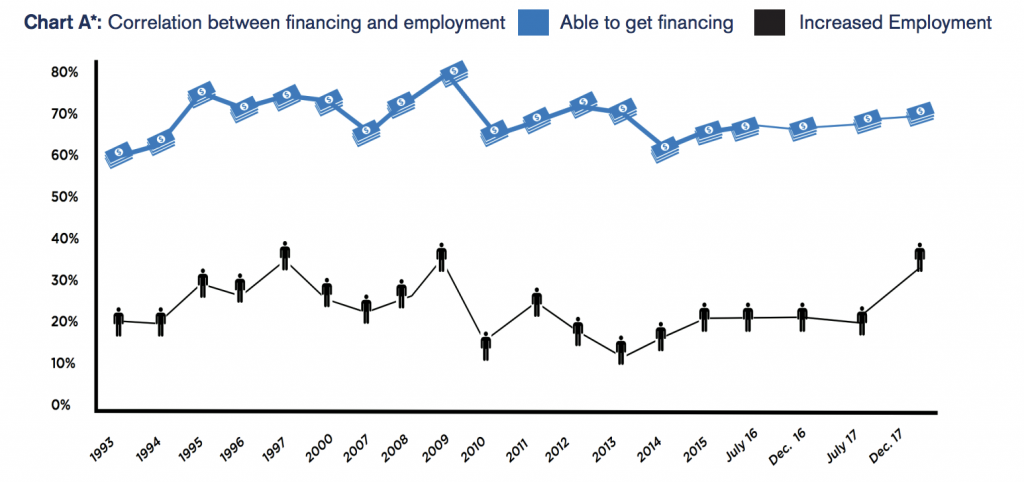

And much is at stake. Lack of funds not only hurts that significant portion of small-business owner but also prevents hiring workers, stymies economic growth and hinders community development, Day maintains. She points to research that shows the nearly direct correlation between availability of capital and increases in hiring. (See Chart A.)

And much is at stake. Lack of funds not only hurts that significant portion of small-business owner but also prevents hiring workers, stymies economic growth and hinders community development, Day maintains. She points to research that shows the nearly direct correlation between availability of capital and increases in hiring. (See Chart A.)

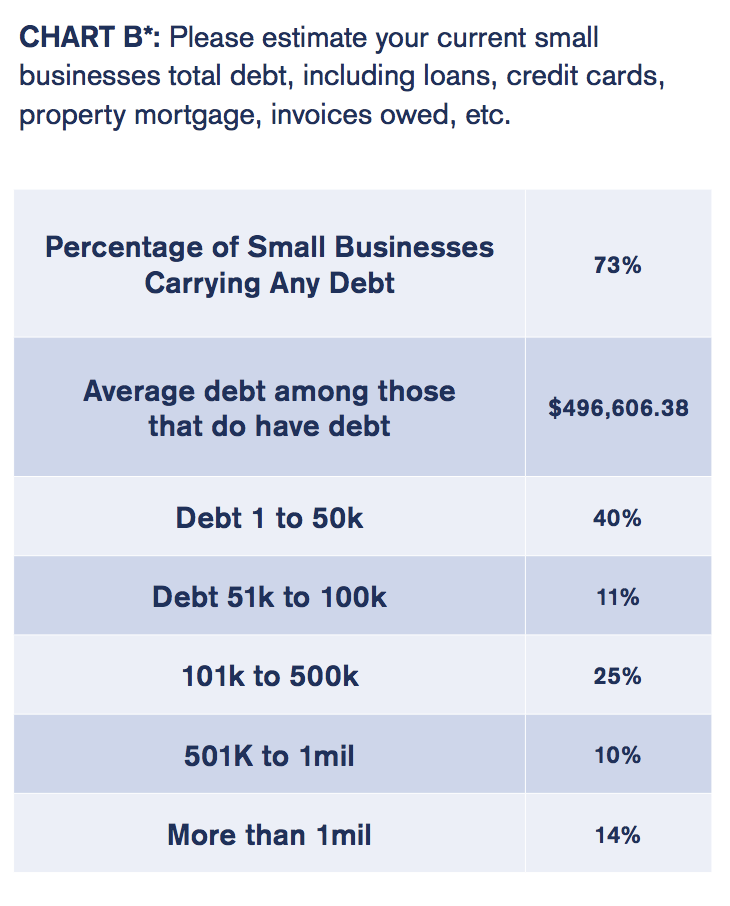

Other NSBA findings include the fact that in July of 2017 merchants reported having debt that averaged $496,000. Some 73 percent of those reported had at least some debt. Some 40 percent of survey respondents, the largest category have debt of $50,000 or less. (See Chart B.)

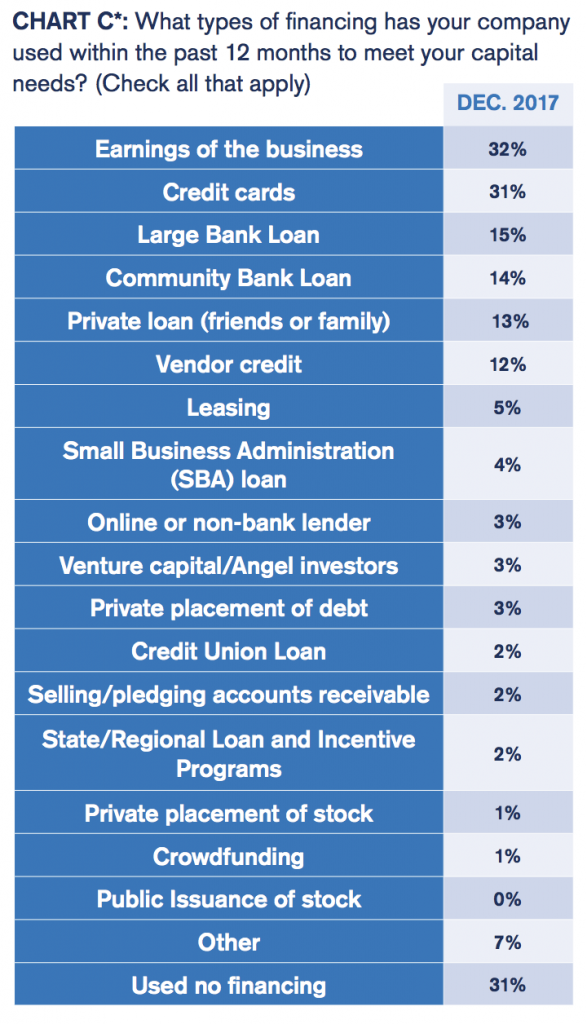

Financing most often comes from funds the business has earned, the trade group says. Some 32 percent of merchants cite that source. Yet simply pulling out a credit card remains a common way to make ends meet, with 31 percent saying they did that to meet capital needs in the last 12 months. (See Chart C.)

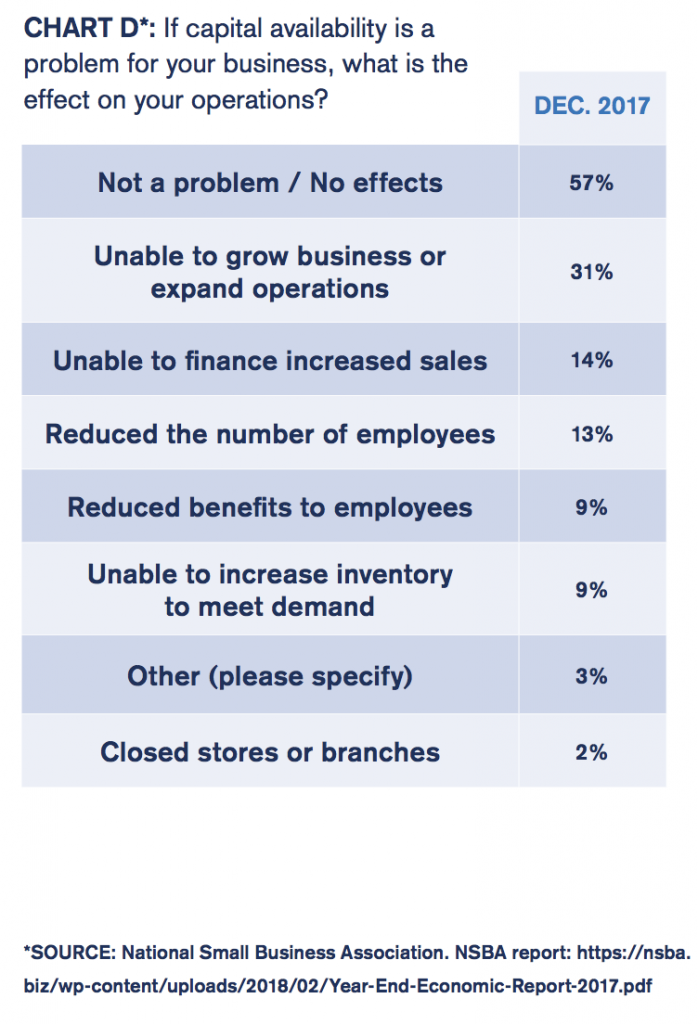

While most (57 percent) say that lack of capital hasn’t hurt their enterprises recently, 31 percent say a dearth of capital prevented them from expanding their operations, 14 percent report they weren’t able to expand their sales because they lacked funding, and 13 percent admit they laid off employees because it was difficult to find the cash to meet the payroll. (See Chart. D)

While most (57 percent) say that lack of capital hasn’t hurt their enterprises recently, 31 percent say a dearth of capital prevented them from expanding their operations, 14 percent report they weren’t able to expand their sales because they lacked funding, and 13 percent admit they laid off employees because it was difficult to find the cash to meet the payroll. (See Chart. D)

The availability of credit hadn’t changed much in the year leading up to the survey, the association says. About 77 percent reported no change in their lines of credit or credit cards, while 18 percent saw their perceived creditworthiness increase and 5 percent saw it decline.

Those results come with a bit of history. The NSBA has been surveying small-business owners since 1993. At first, the trade group hired polling companies to perform the task and cooperated on the report with the Arthur Andersen accounting firm. Computerization enabled the association to take the project in house beginning in 2007. It works on the survey with ZipRecruiter, an online employment marketplace.

Some 1,633 small-business owners participated in the research for the 2017 Year End Economic Report by answering 42 questions online in December 2017 and January 2018. Many of the survey questions have remained the same over the years to facilitate comparisons and tracking.

Some 1,633 small-business owners participated in the research for the 2017 Year End Economic Report by answering 42 questions online in December 2017 and January 2018. Many of the survey questions have remained the same over the years to facilitate comparisons and tracking.

Small businesses on the list of members and the list of non-members receive two email messages alerting them to the survey and providing an online link to the questions. The surveys take place twice a year.

As mentioned earlier, some survey respondents belong to the association and some don’t, but Day was unable to pinpoint the percentages. In response to a question from AltFinanceDaily, she said she may begin tallying how many respondents are members and non-members because non-members tend to have been in business for a shorter time than members. Non-members also tend to differ from members because political engagement often brings the former to the association’s attention.

Participating merchants come from every industry and every state, Day says. Manufacturing and professional services are very slightly overrepresented, while mining is the only category that’s scarcely represented, she admits. Not many small businesses operate in the mining sector, she adds.

National Funding Promotes Justin Thompson

October 3, 2018 National Funding announced today that Justin Thompson, formerly Executive Vice President of Sales, has been promoted to Chief Revenue Officer of National Funding. The new position is an expanded role that will include Thompson’s previous management of a 100-person sales division that includes Direct Sales, Renewal Sales, Broker Sales, Equipment Financing and the responsibilities of developing the company’s new Strategic Partnership vertical.

National Funding announced today that Justin Thompson, formerly Executive Vice President of Sales, has been promoted to Chief Revenue Officer of National Funding. The new position is an expanded role that will include Thompson’s previous management of a 100-person sales division that includes Direct Sales, Renewal Sales, Broker Sales, Equipment Financing and the responsibilities of developing the company’s new Strategic Partnership vertical.

“On the heels of our acquisition of QuickBridge, and the explosive profitable growth of National Funding, this is a great time to expand our offerings to clients with new products and solutions,” said Dave Gilbert, National Funding founder and CEO. “Justin has led sales through the biggest growth period in our 20-year history and I am thrilled for him to continue building on this strong record.”

Thompson started working as Director of Sales for National Funding in 2002, according to his LinkedIn profile, and he has remained with the company until now, with the exception of a two year stint at Reliant Services Group working as Director of Sales & Operations.

“I have never been more excited about the future of National Funding as I am now,” said Thompson. “With the acquisition of QuickBridge, expansion of our strategic partnership channel, and the ever-improving performance of National Funding, we have a lot to offer our customers and brokers – making us an important resource for small and medium-sized businesses nationwide.”

National Funding has also made two additions to support the growth of Strategic Partnerships. Jason Osiecki, previously Head of Sales for QuickBridge, has been named Vice President, Strategic Partnership for National Funding. He will be tasked with driving growth opportunities in the merchant processing, leasing, B2C, Lender Decline and other markets. And Kevin Kane has been appointed as Director of Business Alliances. He will manage day-to-day relationships with brokers across the country.

National Funding Acquires QuickBridge

October 2, 2018

National Funding announced today that it has purchased QuickBridge. The two companies will combine back-end resources, including advanced technology, innovation and product development, but they will continue to operate independently, as separate brands. Ben Gold, QuickBridge’s founding President, will remain in his current post and will work closely with National Funding founder and CEO Dave Gilbert.

“QuickBridge has an unbelievable front end system that knows how to underwrite small businesses extremely efficiently,” Gilbert told AltFinanceDaily.

Gilbert also said he was particularly interested in QuickBridge’s 10 year loan product.

National Funding was a minority interest owner in QuickBridge since the company’s founding in 2011, so this acquisition was essentially a buyout of five other partners.

In addition to the technology, Gilbert said QuickBridge’s people and its headquarters in Irvine, California were elements that made it very appealing.

“There’s a lot of great talent in Orange county and there are a lot of finance companies out there, so it’s going to be a great recruiting hub,” Gilbert said.

Given the high quality pool of talent, Gilbert said he believes he can scale QuickBridge quickly. Together, National Funding and QuickBridge have provided more than $3 billion in financing to small and mid-sized businesses and their combined overall financing volume will exceed $600 million this year, according to National Funding. QuickBridge has been recognized in recent years for its rapid rise, including year-over-year double or triple digit percentage growth.

The way that both companies get business is slightly different. Gilbert said that QuickBridge derives 75 percent of its business from ISOs and 25 percent from direct marketing, whereas National Funding’s ratio is the inverse, with a sizable direct sales team.

In addition to QuickBridge’s headquarters in Irvine, it also has a small satellite office in New York, which will remain. Of the company’s roughly 100 employees, Gilbert said that virtually all of them will stay on. Founded by Gilbert in 1999, National Funding is based in San Diego and employs roughly 230 people.

Funding Circle Stays Global; Goes Public in London

September 29, 2018 Funding Circle became a public company yesterday on the London Stock Exchange, listed as FCH. Founded in 2010, the peer-to-peer lending platform for small and medium-sized businesses, was initially priced at 440 pence (£4.40), which was on the low end of the 420-530 pence per share price range. But it opened at 460 pence, placing the value of the tech company at roughly £1.5 billion, or $2 billion, according to a Reuters report. In conjunction with the company’s IPO, it raised approximately £300.

Funding Circle became a public company yesterday on the London Stock Exchange, listed as FCH. Founded in 2010, the peer-to-peer lending platform for small and medium-sized businesses, was initially priced at 440 pence (£4.40), which was on the low end of the 420-530 pence per share price range. But it opened at 460 pence, placing the value of the tech company at roughly £1.5 billion, or $2 billion, according to a Reuters report. In conjunction with the company’s IPO, it raised approximately £300.

The stock price dropped below the initial 440 pence per share on Friday to 435 pence, but went back up by the end of the day. The company was founded by Samir Desai, James Meekings and Andrew Mullinger, who all met at a pub in Oxford, England, according to a University of Oxford publication. Desai and Meekings were both studying Economics and Management at the university.

Among the company’s investors are Union Square Ventures, Blackrock and Index Ventures, in addition to a £150 million investment from Danish billionaire Anders Holch Povlsen.

According to the company’s September 2018 prospectus, Funding Circle’s total revenue has steadily increased over the past few years with $32 million in revenue in 2015 and $50.9 million and $94.5 million in 2016 and 2017, respectively. The company has facilitated £5 billion in loans its inception in 2010.

In August, Funding Circle rebranded with a new logo, and in June, the company expanded its partnership with Kansas-based INTRUST Bank, strengthening it presence in the U.S. market. Funding Circle offers small business financing from $25,000 to $500,000 with repayment options up to 5 years. While headquartered in the UK, the company also services customers the U.S., Germany and the Netherlands. Its headquarters is in London and it also has an office in San Francisco.