Brokers: It’s Okay To Be A Piker

November 5, 2015The Financial Services Industry is famous for coming up with different connotations that are outside of the comprehension level of the general public. Such connotation listings include terms such as: Derivatives, EPS, Diluted EPS, SPO, EBITA, Par Value, among others.

But there’s one word that I wanted to discuss in particular that comes off as a form of “slang” within the Industry, and that’s the word Piker. To be called a piker by someone in our industry, is to be called a person that thinks small, reaches for small goals and doesn’t dream big.

MASS NEW BROKER ENTRANTS HAVE BIG DREAMS

MASS NEW BROKER ENTRANTS HAVE BIG DREAMS

The Merchant Cash Advance Industry is in a major bubble right now, with a large quantity of new broker entrants into the market all with big dreams inspired by the myriad of industry recruiting ads, highlighting that with little-to-no experience, you can jump in and make $20k a month. The “rah rah” sales motivational speeches soon follow with examples on how one guy is making $25k per month, how another guy just sold his MCA firm and cashed out for $5 million, how another guy made $1 million last year alone, and how YOU can do all of this too if you just come on in and start dialing!

So the big dreamers begin to dream……

- “This year I’m what Dave Ramsey calls a Whopper Flopper. I hate working in this crappy Burger King drive-thru, it’s time to start making my dreams come true.”

- “Next year, I will be making $20,000 a month and driving around in a Mercedes-Benz S-Class.”

The guy joins the new rolls of rookie/new broker entrants on web based predictive dialers calling merchants about a “UCC” they filed 3- 12 months ago. He will start out with about 150 merchants to call on Monday about this UCC filing, and by the time he calls those merchants on Monday, they would have already been called by 15 – 30 other companies over the previous two weeks alone.

In other words, they will all slam the telephone down in his face after he literally mentions the fact that he’s calling from any “capital or funding” company, without him even being able to get a word in.

DREAM KILLED (REALITY SETS IN)

DREAM KILLED (REALITY SETS IN)

The reality is that success in our industry is mainly due to leveraged resources, rather than actual superior “selling” capabilities. What happens is that 20% of the brokers in the market remain profitable and sustain a good career/operations going forward, where as 80% of brokers don’t last more than 3 – 6 months, mainly because the 20% has access to resources that the other 80% don’t have access to, that provides them a significant market competitive advantage. These resources include:

- Having Strategic Partnerships with Banks, Credit Unions, Processors and Other Associations

- Having Access To Financing (Debt and Equity) Allowing For A Much Higher Marketing Budget

- Having Access To Better Base Pricing

- Having Access To Better Quality Data

- Having Access To Better SEO Positioning

- Having Access To Better Marketing Channels

Mr. New Broker, you were hired to be a part of what I call The Mom and Pop Network, which is just a group of random brokers who will resell for free (you pay for all of your expenses). So they might maintain a Mom and Pop Network of 2,000 brokers that bring in on average of 10 applications a year (20,000 apps) with 35% getting approved (7,000) and 30% closing (2,100) with an average funding per client of $30,000. This is $63 million in annual funding volume for the firm from this source alone.

A DIFFERENT APPROACH: THE PIKER APPROACH

So Mr. New Broker, how about instead of following the “rah rah” sales crowd, how about you join me over here on the Piker side and we set some goals on being solidly in the middle class instead?

- Going based on individual income, you are considered middle class in the US for the most part if from staying in an low/average cost of living area, you make over $40k a year (lower middle class), $50k – $60k a year (the middle of the middle class) or $70k – $85k (higher middle class).

- $50k – $60k a year in a low cost of living area will still allow you to live in a great quality Suburb, if you strategically manage your expenses with efficient budgeting and tax reduction strategies.

- You also want to be putting away let’s say $7,500 a year into your retirement/investment accounts. If you do this for 40 years from 25 – 65, with just a conservative 5% per year return, you will have over $1 million at age 65. At 65 you could put that $1 million principal into a long term CD paying let’s say 3% per year, opt to receive the interest every month, and get $30,000 a year. Then when you add in your Social Security payments of let’s say $20,000 a year, this now gives you $50,000 a year in spending power without even touching the $1 million principal.

IMPLEMENTING THE PIKER APPROACH

The first thing you want to do is make sure you stay in a low cost of living area, so if you are in a high cost of living area like NYC or LA, I would move immediately. Secondly, you would setup your virtual office (in the cloud) to include your telephone line, fax line, website, etc. Thirdly, you want to focus on doing market research on various market niche challenges where you can come in and creatively solve outstanding problems, for example, you might do some of the following:

- Find new solutions for niche industries that don’t qualify for most MCAs, but would like an MCA.

- Find new solutions for start-up companies seeking working capital.

- Analyze big data sources to find merchants in particular situations that you could address.

Map out a complete strategic business plan with sales forecast estimates, ROI estimates, and partner with companies that have the infrastructure to help deliver the solutions you laid out. Keep your credit clean and use No Interest Credit Card Promo Deals to creatively finance your marketing efforts.

FINAL WORD – AM I DREAMING TOO SMALL?

Am I dreaming too small? Shouldn’t I be up all night focused on how to be the next CAN Capital?

My issue with the “rah rah” sales speech is that they preach from the TOP of the ladder in terms of the extravagant income estimates ( $250k – $1 million per year), without providing any information to New Brokers on actual strategies, competencies, networks, and resources needed to ACTUALLY amass such levels of annual income. It doesn’t make any sense.

So my advice for all New Brokers is to be a PIKER, which is to establish yourself solidly in the middle class first, then once that’s done, you can look at ways to expand on your competencies, resources and networks to grow into the six figure income range.

Letter From the Editor – November/December 2015

November 1, 2015 Somehow 2015 is already over. It started off as the year of the broker but it ended up as a culmination of many things. It was the year of capital raising and rebrands, the year of regulatory interest and RFIs, the year of unicorns and leaderboards. 2015 solidified alternative lending’s place across multiple continents. Bankers started talking like technologists and technologists like bankers.

Somehow 2015 is already over. It started off as the year of the broker but it ended up as a culmination of many things. It was the year of capital raising and rebrands, the year of regulatory interest and RFIs, the year of unicorns and leaderboards. 2015 solidified alternative lending’s place across multiple continents. Bankers started talking like technologists and technologists like bankers.

In 2015, we introduced William Ramos who went from working at a Lowes Home Improvement store to driving a Maserati after he landed a temporary job as a financial cold caller. We also showed you Jared Weitz, who went from working as a plumber to running a financial company that’s now on pace to originate $100 million in small business funding a year.

As we close out 2015 here, we’ll introduce you to the man whose company is producing billions (that’s billions with a ‘b’) of small business funding. Daniel DeMeo is the CEO of CAN Capital, a company who has weathered both the dot-com bust and the financial crisis and still manages to be one of the industry’s top players. DeMeo shared what he’s all about and the story of CAN you haven’t read anywhere else.

That’s the good stuff, but there’s some bad stuff too. While critics have broadcast some of the not so flattering stories in alternative lending’s rise, there’s a darker side that no one has dared write about, bad borrowers. Perhaps a byproduct of rapid technological change, merchant fraud has become an all too common occurrence. These predatory merchants are causing chaos, damaging margins, exploiting underwriting weaknesses and potentially driving up the cost for the good guys. In this issue, we explore the reality of bad guys and their tactics.

And that’s not all we have of course. In 2015, we compiled the first report on merchant cash advance and small business lending in collaboration with Bryant Park Capital. We measured the industry’s growth, learned of its diversity, and got a numerical sense of the confidence for the future. A sample of that report is included within.

That was 2015 summed up, the year that Marty McFly met us all in the future. 2016 will undoubtedly mean robots, laser beams and interplanetary colonization. Sprinkled in between all that will be online loans, merchant cash advances, bitcoins, and financial disruption. In 2016, the world may become AltFinanceDaily once and for all.

–Sean Murray

The Quiet Innovator: Meet Dean Landis

November 1, 2015 Have you ever wondered who helped evolve our industry from the boutique “credit card factoring” of yesteryear, to today’s multi-billion dollar Alternative Lending industry? Credit Cash LLC may not be the best known MCA company out there. However, over its ten-year history, its innovations have become industry mainstays. Founded by, Dean Landis, an established asset based lender in 2005, Credit Cash has always focused on larger deals to better credits; but is also largely responsible for many of the important changes that have improved our industry over the years.

Have you ever wondered who helped evolve our industry from the boutique “credit card factoring” of yesteryear, to today’s multi-billion dollar Alternative Lending industry? Credit Cash LLC may not be the best known MCA company out there. However, over its ten-year history, its innovations have become industry mainstays. Founded by, Dean Landis, an established asset based lender in 2005, Credit Cash has always focused on larger deals to better credits; but is also largely responsible for many of the important changes that have improved our industry over the years.

Its first, and only slogan, “Our rates are so low, they’re actually loans,” was telling from the start. Well before On Deck and others made loans an alternative to advances, Credit Cash had determined that to attract larger and better credits, rates had to be far lower. With lower rates, a loan structure was more practical in lieu of the then existing true sale structure (innovation #1).

When Dean, Credit Cash’s founder, came up with his concept, he posed it to some of the existing industry leaders. While all were supportive, none thought that the product worked well with the low rates Landis was proposing. Back then, with underwriting a bit more primitive, default rates were typically higher than they are today. A competitor urged Credit Cash to license its underwriting and split funding operation.

What the others didn’t appreciate is that Credit Cash was going to use its decades of asset based lending experience to create a whole new method for providing working capital to SMEs. Dean represents the third generation of his family to own and manage a specialty finance company. His asset based lending firm, Entrepreneur Growth Capital, is one of the best known and highly regarded national commercial finance companies serving small and lower middle market borrowers. First, these would not be purchases of future revenue or credit card receipts. Landis didn’t believe that was actually a tangible object that could be bought and sold. Thus, he chose the loan structure and with it, fixed daily payments (innovation #2).

Next, while most of the MCAs at the time were solely using split funding, Credit Cash required the setup of a lockbox (innovation #3). This allowed each client to keep its on processor (innovation #4), but also gave Credit Cash more control over cash flow as all credit card receipts went through the lockbox, not just a percentage.

Next, while most of the MCAs at the time were solely using split funding, Credit Cash required the setup of a lockbox (innovation #3). This allowed each client to keep its on processor (innovation #4), but also gave Credit Cash more control over cash flow as all credit card receipts went through the lockbox, not just a percentage.

At this time in the industry’s evolution, all advances were based on credit card revenue, so clients were typically in food service, hospitality or retail. Early on, Credit Cash got a request from a Burger King franchisee. It was a good prospect, but there wasn’t enough credit card revenue to meet the fixed daily payments. That is when the idea of using an ACH to debit clients’ banks accounts was born (innovation #5). From there, it wasn’t long until both Credit Cash and others realized that this type of lending deserved a far larger audience than the existing marketplace. In fact, whereas restaurants used to be over 50% of Credit Cash’s business, it is now less than 25%.

One other change was in how Credit Cash treated renewals. At the time, clients were required to essentially buy back their existing advances in order to get more funding, thus increasing their costs. Credit Cash not only avoided this practice, but began offering early termination discounts (innovation #6).

Landis claims he is as surprised as anyone at the industry’s growth. While entering its 11th year, Credit Cash has intentionally not grown nearly as much as the other industry veterans. Credit Cash has always been a quality over quantity shop. In fact, they still do all of their underwriting by hand. As their average loan is over $500,000, Landis is hesitant to rely on computers and algorithms. Dean is interested in continuing to build a strong portfolio of borrowers who require additional capital with a creative approach. “Our borrowers appreciate that we are able to think outside of the box and take a hands on approach to underwriting and servicing their loans.”

As for growth, Landis jokingly admits that Credit Cash is often ISOs’ last choice. “Because our rates are so low, so is our commission structure. An ISO may make more money by funding a prospect elsewhere. Although because of the Credit Cash’s ability to fund much larger loans, it is not unheard of for an ISO to earn $100,000 or more from a closed, single transaction.” However, with larger loans, come stronger credits and more savvy borrowers. Landis continues to smile when stating that “a typical Credit Cash borrower would rarely take an MCA at the market rates.” However, ISOs continue to send Credit Cash deals as a funded deal, is better than no deal at all.

Blurring Small Business: A Troubling Narrative is Gaining Steam

October 30, 2015Almost 18 months ago at LendIt’s 2014 conference, Brendan Carroll, a partner and co-founder of Victory Park Capital said that in regards to business lending, “the government doesn’t have the same scrutiny on this sector as it does in the consumer space.”

This double standard is the crux of American capitalism. In business you can win or lose, be smart or foolish, risk it all or play it safe. Government regulations don’t let the average consumer be subjected to the same stakes. They are viewed to be at a natural disadvantage against businesses and thus there are laws to protect them, and perhaps rightly so.

Since entrepreneurship is a choice, businesses and the people that own businesses are held to a higher standard of acceptable risk taking. In the free market, the pursuit of profit holds the system together.

This economic worldview is part of the reason why entrepreneurial TV shows such as Shark Tank are so popular. In the Tank, contestants can just as easily walk away with a terrible deal as they can a good one. And when bad deals get made, and they do, I’ve yet to see regulators descend on the set to fine or arrest Daymond John, Kevin O’Leary, or Barbara Corcoran.

But Shark Tank features entrepreneurs on a remote stage detached from their daily environment, giving it the look and feel of a game show. If you want to see cold hard dealmaking with mom-and-pop shops on an up close and personal level, just watch CNBC’s The Profit. On the show, small business expert Marcus Lemonis does not sugarcoat what he is. “I’m not a bank. I’m not a consultant. And I’m not the fairy godmother,” he bluntly told one small business owner. It doesn’t matter if it’s a family owned store or a full fledged corporation, Lemonis is looking to make a deal and make some money. When it comes to business, he is well… all business.

Just as the CFPB hasn’t shut down Shark Tank, (which one has to wonder if they’ll be subject to Reg B of Dodd Frank’s Section 1071) none of Lemonis’ deals have been scrutinized by a Federal Reserve study, nor has the Treasury Department issued an RFI to better understand why entrepreneurs go on the show in the first place.

It’s no wonder then at LendIt 2014, Carroll also said that there wasn’t the same sort of moral hurdle when it came to institutional capital investing in business lenders as opposed to consumer lenders.

Moral was a telling word choice because the morality of certain commercial transactions have recently come under fire by groups claiming to represent small businesses. The premise of their argument is that commercial entities are no more sophisticated than consumers, that a corporation and the average joe are equal in their ability to take risks and make decisions for themselves.

Their evidence is that sometimes in business-to-business transactions, particularly in lending, one side accepts terms that would be considered far outside the norm for consumers, terms that violate a moral threshold. One has to wonder where a loan with an infinity percent interest rate ranks on this morality scale, a deal that’s actually been made and accepted several times on a TV show. Referred to as a “Kevin deal” since they are Kevin O’Leary’s favorite, the borrower is obligated to pay a perpetual royalty on top of repaying the loan itself. In simple terms, it’s a loan that can never be paid off.

In the case of Wicked Good Cupcakes, a business that appeared on Shark Tank in 2012, a mother-daughter team struck a deal that would cost them 45 cents per cupcake in perpetuity to Kevin O’Leary. Many fans criticized them for it and yet the two have said that they have no regrets.

In the case of Wicked Good Cupcakes, a business that appeared on Shark Tank in 2012, a mother-daughter team struck a deal that would cost them 45 cents per cupcake in perpetuity to Kevin O’Leary. Many fans criticized them for it and yet the two have said that they have no regrets.

The fact that Wicked Good Cupcakes decided what made sense for them and was happy about it, damages the storyline that businesses need to be saved from their own decisions. But there’s another problem, government entities themselves may be inadvertently effectuating this false narrative by inferring incorrect conclusions from their own research.

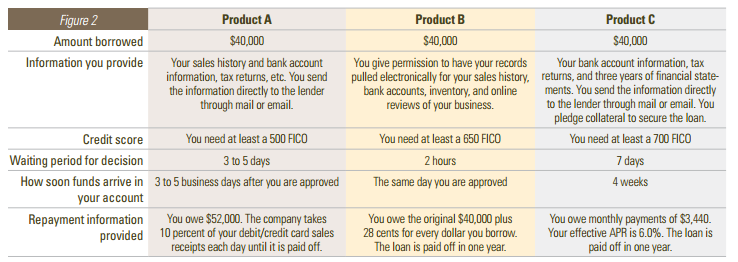

Nowhere is this more evident than in a report recently published by the Federal Reserve Bank of Cleveland that analyzed small businesses and their understanding of “alternative lending.” The report shared the results of two focus groups that had been shown terms for three hypothetical products that supposedly represented actual products in the real world.

Unsurprisingly, the report concedes “when comparing the products, participants initially reported the three were easy to compare and that they had all the information to make a borrowing decision.” But the researchers pressed on until they got an answer that fit their expectations, that small businesses are confused when it comes to money and finance.

In a hypothetical scenario where a commercial entity sold $52,000 of future receivables for $40,000 today, it stated that the “lender” would withhold 10% of each debit/credit card transaction until satisfied. Participants were then asked to guess the interest rate on this loan if they paid it back in one year. That caused a lot of folks to scratch their heads and that’s because it was a trick question.

The question itself introduced conflicting facts and lacked crucial variables to make an intelligent guess. Nevermind that respondents prior to that question said that there was “nothing confusing” about the products presented as is. The original feedback should’ve been enough. Below are some of the responses offered before they were deliberately tricked.

- “Nothing Confusing.”

- “No, it’s pretty straight-forward.”

- “I can’t think of anything more I would need to see, really.”

- “This is enough info for me to make a decision.”

The researchers concluded however that the answers to their trick question suggested there were “significant gaps in their understanding of the repayment repercussions of some online credit products and the true costs of borrowing.”

And while it might be true that they semi-admit to what they did when they wrote, “using only this information, calculating a true effective interest rate would not have been possible without making some assumptions,” the headline that spread thereafter was that small business owners are confused by alternative lenders.

And while it might be true that they semi-admit to what they did when they wrote, “using only this information, calculating a true effective interest rate would not have been possible without making some assumptions,” the headline that spread thereafter was that small business owners are confused by alternative lenders.

But even if that was the case, at what point does confusion become unfair in a purely commercial transaction? And what would be an appropriate remedy?

We’ve been down this road before where federal regulators have set mandatory disclosures in order to bring transparency to a lending environment believed to be obscure. And just recently on September 17th, 2015, the House Committee on Small Business Subcommittee on Economic Growth, Tax and Capital Access pressed community bankers on the impact of such measures dictated by Dodd-Frank.

Congressman Trent Kelly asked if all the added new pages to loan agreements make it easier for their borrowers to understand. “Do they understand what they’re signing?” he asked.

B. Doyle Mitchell Jr., the CEO of Industrial Bank that was speaking on behalf of the Independent Community Bankers of America responded that they do not. “It is not any more clear,” he answered. “In fact it is even more cumbersome for them now.”

If anything, the Federal Reserve study offered compelling evidence that small businesses are happy with the way alternative lenders are currently disclosing their terms. It is only when government researchers tricked them that they became confused. That should say it all.

One consequence of entrepreneurship is that businesses are not created equal in their ability to assess financial transactions and no amount of disclosures or intervention can save them. There must be losers in order for there to be winners.

Case in point, there are lenders out there doing deals so lopsided that they actually turn to each other and say, “I can’t believe she took that.” Such is the case of RuffleButts, a children’s fashion line that appeared on Shark Tank in 2013.

“When they wake up, they’ll realize they messed up,” said Mark Cuban in reference to the deal Lori Greiner proposed and closed. An article on BusinessInsider.com covered the episode and unabashedly concluded, “Shark Tank isn’t a charity. The investors are putting in their own money, so they have every incentive to push to get the best deal possible for themselves.”

Shark Tank has risen in popularity because it is a reflection of a culture that believes dealmaking, both good and bad, is inherent to the endeavor of entrepreneurship. When a bad deal is made, regulators don’t come on the show to urge a do-over.

But what’s dealmaking got to do with the local pizza joint seeking $20,000 that doesn’t have the time to mess around on TV shows? Unlike lenders who refer to their transactions as loans or units, merchant cash advance companies and the agents who negotiate the transactions appropriately refer to their agreements as deals. How else would one label an agreement in which a commercial entity sells future receivables for a mutually agreed upon price?

But what’s dealmaking got to do with the local pizza joint seeking $20,000 that doesn’t have the time to mess around on TV shows? Unlike lenders who refer to their transactions as loans or units, merchant cash advance companies and the agents who negotiate the transactions appropriately refer to their agreements as deals. How else would one label an agreement in which a commercial entity sells future receivables for a mutually agreed upon price?

And if the Federal Reserve study indicated anything, it’s that business owners feel there’s nothing confusing about these deals.

So it would seem that everything as Americans know it, watch it and understand it, is business as usual.

Even Brendan Ross, the president of Direct Lending Investments, was quoted by the BanklessTimes as saying, “I want to emphasize there’s absolutely nothing novel about lending money to businesses. This isn’t some phenomenon we are rediscovering. There isn’t going to be increased regulation because this isn’t new.”

Perhaps the only thing that could be considered new is that loan sizes have gotten smaller and the types of products small businesses can access has diversified. Along the way, some of these new startups have decided to offer products in line with a self-professed moral code, which is to deliberately lend money at a loss and lash out at lenders who seek profit.

There’s a term for lending startups that don’t make money. They’re called “failed startups.” By casting small businesses as being no different from unsophisticated consumers, it’s quite possible that shows like Shark Tank and The Profit would become illegal in the process. Disclosures meant to help make things more transparent could actually make things less clear and more cumbersome, just as they have in the past.

I don’t think anybody is in favor of small business failure or an environment where confusion prevails, including the guys making infinity percent interest loans like Kevin O’Leary. But if the goal is to increase transparency, it should be in a way that businesses on both sides are content with.

The Federal Reserve study showed the system is working well as is and that prescribing mandatory changes to fit some universal standard would only serve to usher in an era of confusion that everyone is trying to avoid. Lenders can always do better to serve their clients, but the free market must prevail. As Mitchell, Industrial Bank’s CEO said when he testified in front of the Small Business Committee, “the problem with Dodd-Frank is you cannot outlaw and you cannot regulate a corporation’s motivation to drive profit at all costs so while it has a lot of great intentions in over a thousand pages, it has not helped us serve our customers any better.”

Alternative Lenders Are Waiting for a Shakeout

October 28, 2015 Back in April at the LendIt conference in New York, the big consensus was that not all underwriting was created equal and therefore several players wouldn’t survive long enough to make it back to LendIt in 2016. Six months later at Money2020 and so far everyone is still standing.

Back in April at the LendIt conference in New York, the big consensus was that not all underwriting was created equal and therefore several players wouldn’t survive long enough to make it back to LendIt in 2016. Six months later at Money2020 and so far everyone is still standing.

Loan terms are getting longer, rates cheaper and the cost to acquire borrowers higher. Somebody has to be feeling the pressure but in a rather benign economic and regulatory environment, it’s clear skies.

Valuations are soaring. SoFi is valued at more than $4 billion and Kabbage at more than $1 billion.

But Robert Greifeld, the CEO of Nasdaq warned attendees about the validity of private market valuations. “A unicorn valuation in private markets could be from just two people,” he said. “whereas public markets could be 200,000 people.” At best he described a private market valuation as being just a rough indicator.

And some wonder if these valuations are based on just scale, rather than the ability to underwrite more intelligently and efficiently than a bank. OnDeck for example, had a Compound Annual Growth Rate (CAGR) in originations of 159% from 2012-2014 when the average originations CAGR for their peers is currently 56%. But OnDeck has the advantage of time. With nearly a decade of data under their belt, they’ve been able to see what works and what doesn’t.

“You have to have enough bad loans to build a good credit model,” said OnDeck CEO Noah Breslow during a Money2020 panel discussion.

For Aaron Vermut, CEO of Prosper, getting their company to the next level was about having access to institutional capital. As a marketplace, and as a company that almost died several years ago, he pointed out, institutional money was the inflection point for them to grow. The peer-to-peer model that actually depended purely on “peers” is what held their company back.

One thing several lenders seemed to agree on was the limited applicability of FICO. FICO is not the thing to use for a small business loan, said Sam Hodges, Managing Director and Co-founder of Funding Circle. His words didn’t come as a surprise since credit scores are generally the domain of consumer lending.

But doubts about FICO’s ability to predict performance didn’t just come from the commercial finance side. Prosper’s Vermut explained that consumers still think their FICO score is the most important factor in the rate they get. So even though they’ve got a system to predict repayment outside of FICO, they’re kind of forced to incorporate it because consumers are being educated to believe that’s what matters most.

The irony was not lost that as Vermut said that on a panel, he was seated next to Kenneth Lin, the CEO and founder of Credit Karma, a company that educates consumers about credit. “A credit score is one of the most important components of a consumer’s financial profile,” says Credit Karma’s website. Such language puts a tech-based lender with their own scoring model perhaps at odds with what their own prospects believe.

For instance if a potential borrower with a 750 FICO score is offered a high interest rate because the lender’s advanced and more in-depth underwriting determined them to be high risk, they’re going to walk away confused.

That of course begs the question, who needs to change? Those educating consumers about credit scores or the lenders who are moving away from them?

Before educational services shift though, it would probably make sense if the lenders can prove that their non-FICO dependent systems will work in the long run. And the sentiment among many lenders is that there are plenty of flawed models out there that will inevitably fail. That makes a shakeout not just a matter of if, but when.

Six months after LendIt, everybody is still standing. Whispers from in and around Money2020’s halls and exhibit floor revealed that the confident lenders wish the correction would happen sooner rather than later but that they are prepared to wait however long it takes.

Right now, confidence about the future on the commercial finance side came in at an 83.7 out of 100, according to the Small Business Financing Report. While there are no other points of reference to compare that to, industry captains are generally very bullish.

That could mean that for those secretly under tremendous pressure already, you could be left waiting for a shakeout for a very long time.

The Industry’s First Small Business Financing Report Revealed

October 25, 2015AltFinanceDaily teamed up with Bryant Park Capital, an investment bank providing M&A and corporate finance advisory services to emerging growth and middle market public and private companies, to conduct the industry’s first comprehensive report.

Our initial findings are drawn from a survey of twenty-seven C-level participants, whose companies primarily offer merchant cash advances and small business loans. Combined, the participants represent more than $1.9 billion in annual origination volume. The survey was sent to over one-hundred eligible respondents, with participation open to all of them equally and included both direct funders and brokers.

- Thirteen respondents reported being on pace to originate $50 million or more in 2015.

- Seven respondents reported being on pace to originate $100 million or more in 2015.

Analyzing the origination volume of participants over a three-year period, the industry was determined to have a:

Compound Annual Growth Rate of 56%.

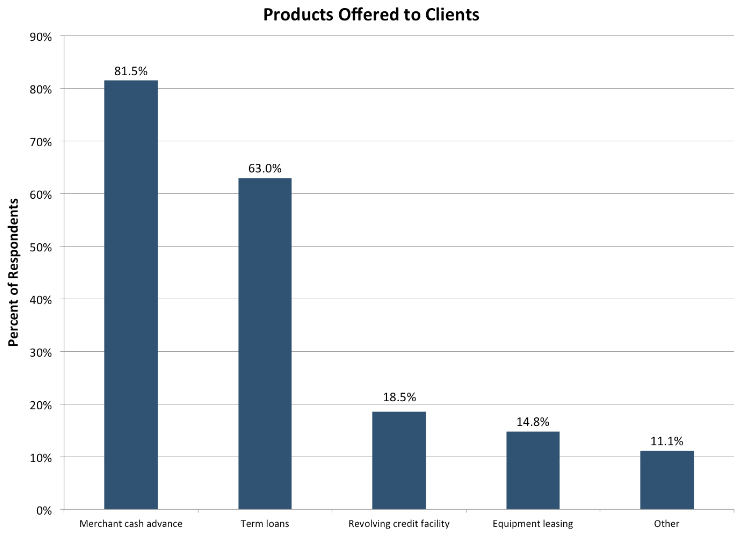

THE INDUSTRY HAS A DIVERSIFIED PRODUCT MIX

Respondents revealed a diversified product mix beyond merchant cash advance. Five participants actually reported originating no merchant cash advances at all and instead offered term loans or other products.

THE INDUSTRY CEOS HAVE A CONFIDENCE INDEX OF 83.7

Based on responses from CEO/participants asked to give their confidence level in the continued success of the small business lending/MCA industry over the next 12 months on a scale of 0–100, with 100 being the highest.

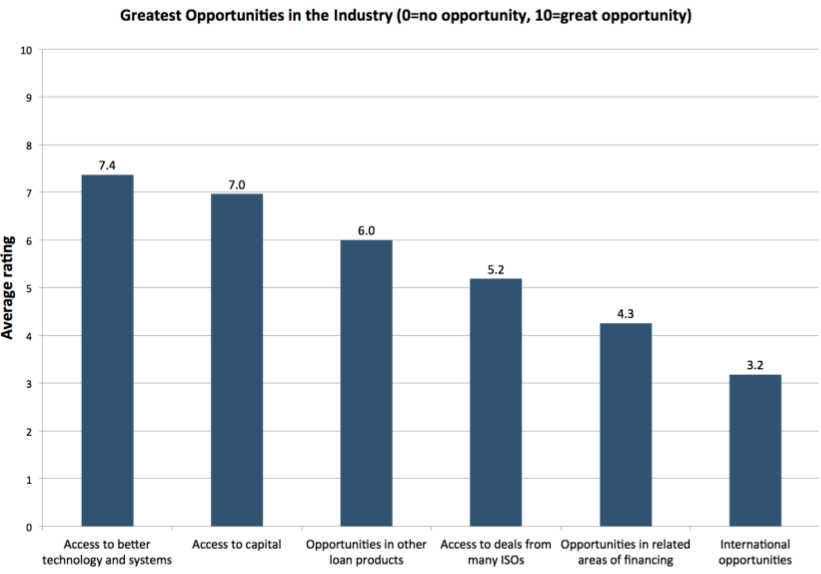

ACCESS TO BETTER TECHNOLOGY AND SYSTEMS IS THE GREATEST OPPORTUNITY IN THE INDUSTRY

Based on responses from participants asked to score the importance of opportunities on a scale of 0–10, with 10 being the highest.

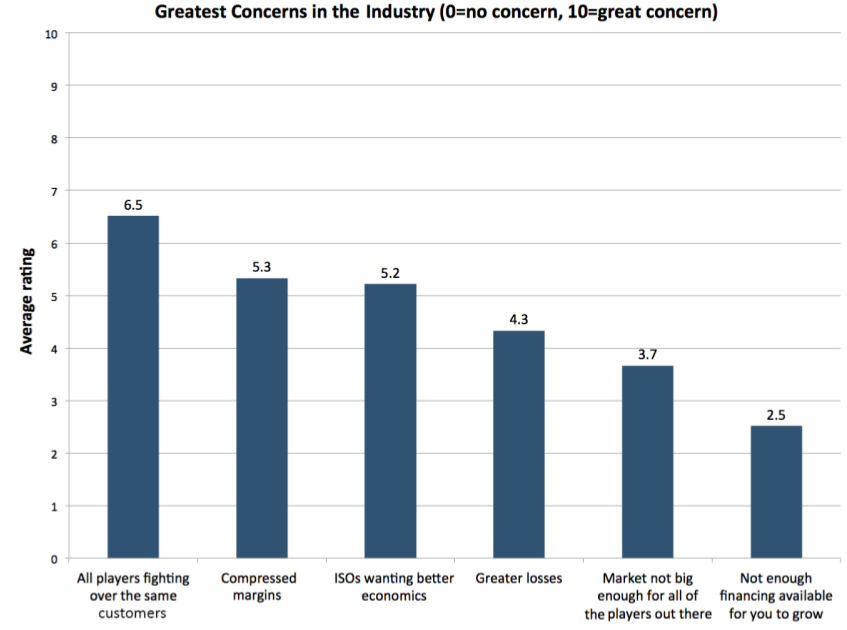

ALL PLAYERS FIGHTING OVER THE SAME CUSTOMERS IS THE GREATEST CONCERN IN THE INDUSTRY

Based on responses from participants asked to score their concerns on a scale of 0–10, with 10 being the highest.

The identities of participants and their individual responses are confidential. Participants were asked a total of 27 questions and had the ability to waive a response to any question, including the disclosure of their identity to the surveyors themselves.

Survey participants are eligible to receive the full anonymized report. Industry players who complete the full survey will automatically receive a full copy of this report. If you are not part of an operating company in the industry and you would like to obtain a copy of the report or participate in the survey, please contact Bryant Park Capital or AltFinanceDaily.

DOWNLOAD THE PDF VERSION

Did Your Deal Slip Out The Back Door?

October 22, 2015Gil Zapata found himself in the right place at the right time to catch someone red-handed at backdooring, the practice of stealing an alternative-funding deal and cheating the original ISO or broker out of the commission.

It seems that Zapata, who’s president and CEO of Miami-based Lendinero, was sitting in a client’s office about three years ago when the phone rang. The call came from an employee of a direct funder that had turned down Zapata’s deal to fund the merchant. Now, the employee was offering funding from another source without notifying Zapata. Fortunately, the merchant didn’t accept the surreptitious funding, Zapata said. “There’s a huge loyalty factor with maybe 50 percent of the clients an ISO has under their belt,” he noted.

It seems that Zapata, who’s president and CEO of Miami-based Lendinero, was sitting in a client’s office about three years ago when the phone rang. The call came from an employee of a direct funder that had turned down Zapata’s deal to fund the merchant. Now, the employee was offering funding from another source without notifying Zapata. Fortunately, the merchant didn’t accept the surreptitious funding, Zapata said. “There’s a huge loyalty factor with maybe 50 percent of the clients an ISO has under their belt,” he noted.

But many merchants sign up for backdoor deals out of ignorance, callousness or desperation, and the problem seemed to gather momentum in the first quarter of this year, according to Cheryl Tibbs, owner of Douglasville, Ga.-based One Stop Funding LLC.

When Tibbs found herself the victim of backdooring a few months ago, the merchant’s loyalty to the ISO prevailed once again. “Because of the relationship we had with the merchant, he let us know and didn’t go along with it,” she said.

Both cases fall into one of the categories of backdooring. This type usually occurs when an ISO or broker submits a deal and the funder declines it, said John Tucker, managing member of 1st Capital Loans LLC in Troy, Mich. An employee of the funder then takes the file and offers it to other funders, often those that accept higher-risk deals. The funder’s employee conveniently forgets to include the originator in the commission, Tucker said. Meanwhile, the employee’s boss might know nothing of the post-denial goings-on.

In another variety of backdooring, ISOs or brokers deceptively claim that they’re direct funders. They solicit deals in online forums, by email message or over the phone, and then they offer the deals to companies that really do function as direct funders. In many cases, the fake funders pocket the entire commission, Tibbs said.

“I’m bombarded with probably 10 emails every day of the week from a supposedly new lender that wants my business, and they’re really just a broker shop like we are,” she maintained.

To guard against both kinds of backdooring, ISOs and brokers should know their funding sources, everyone interviewed for this article suggested. “What we’ve done is tighten up on how we do submissions,” Tibbs said. “We’re very particular about which lending platforms we use.” Although her company has contracts with 60 to 70 funders, it uses only three or four regularly, she noted. “Shotgunning” deals to lots of potential funders invites backdooring, Tibbs said.

To guard against both kinds of backdooring, ISOs and brokers should know their funding sources, everyone interviewed for this article suggested. “What we’ve done is tighten up on how we do submissions,” Tibbs said. “We’re very particular about which lending platforms we use.” Although her company has contracts with 60 to 70 funders, it uses only three or four regularly, she noted. “Shotgunning” deals to lots of potential funders invites backdooring, Tibbs said.

Tibbs also scrutinizes deals to determine which funder would provide the best fit. That way, fewer deals are declined and thus fewer became candidates for backdooring by unscrupulous funder employees. “We have a system. We scrub it. We do the numbers,” she said of her company’s close attention to underwriting, which helps determine what funders would accept the deal.

Her company also keeps a watchful eye on every deal’s progress. “We know exactly where the deal is, and who’s looked at it,” she said. It also helps to insist upon having a dedicated account rep, Tibbs emphasized. That way she can form a relationship that discourages backdooring.

Perhaps the most basic safeguard comes with determining that the company claiming to fund the deal really has the capital to do it and isn’t just shopping the file to real funders. Tucker advised using Internet searches to turn up evidence that the supposed funder really isn’t another ISO or broker. Searches should reveal press releases on equity rounds that direct funders have received, for example. If open-ended Web searches don’t produce satisfying results, check state registrations, he said.

ISOs and brokers can also prevent backdooring by avoiding sub-agent status, Tucker cautioned. “I don’t know why guys would want to be a broker to a broker,” who could steal commissions, he observed. One exception to the sub-agent problem comes with agents who are just entering the business and are receiving training from a broker, Tucker said. In another exception, sub-agents may find another broker has competitive advantages that aren’t easy to duplicate – like a $20,000 monthly marketing budget to generate sales leads, he continued. Or perhaps the other broker gets low base pricing from a funder that allows for reduced factor rates without sacrificing part of the commission.

Brokers and ISOs can also protect themselves from backdooring – and just in general – by maintaining their relationships with merchants, even those who’ve been denied funding from four or five sources, Zapata said. An increase in revenue or jump in credit worthiness can qualify them a few months later, and other brokers or funders may be soliciting them in the meantime, he said.

Brokers and ISOs can also protect themselves from backdooring – and just in general – by maintaining their relationships with merchants, even those who’ve been denied funding from four or five sources, Zapata said. An increase in revenue or jump in credit worthiness can qualify them a few months later, and other brokers or funders may be soliciting them in the meantime, he said.

Then there’s the possibility of collective action against backdooring. An association or some other entity representing the industry could compile a database of companies accused of backdooring, Tibbs said. “Just as there’s a black list of merchants that have been red-flagged from getting merchant cash advances, there should be some type of database of funders that frequently backdoor deals – that way, ISOs know to stay away from them,” she maintained.

The database would also prompt owners and managers of direct-funding companies to crack down on employees who use nefarious tactics, Tibbs continued, because the heads of companies would want to stay off the list.

But finding the financial support and staffing for such a database might prove difficult, according to Tucker. He noted that the card brands, such as Visa and MasterCard, maintain a match list of merchants barred from accepting credit cards. But the card brands have vast resources and a keen interest in the list, he said.

Requiring funders to pay to register might discourage ISOs and brokers from posing as funders, Tibbs suggested. But that, too, would require an infrastructure and would demand financial investment, sources said.

Still, everyone interviewed agreed that the industry should police itself with regard to backdooring instead of inviting federal regulators to enter the fray. “The federal government will mess with pricing without understanding every merchant can’t get low factor rates because there’s too much risk on the deal,” Tucker warned.

Perhaps extending the protection period in funding applications would help guard ISOs and brokers, Zapata said. But he cautioned that making the time period too long could interfere with the free market.

Keeping backdooring in perspective also makes sense, Zapata said, noting that merchants often receive multiple funding offers because everyone in the industry is basing phone calls on the same Uniform Commercial Code filings regarding distressed merchants.

Alternative Business Funding’s Decade Club

October 22, 2015 The working capital business is a very different animal now than it was a decade or so ago when many of today’s established players were just starting out.

The working capital business is a very different animal now than it was a decade or so ago when many of today’s established players were just starting out.

“At that time, the industry was a bunch of cowboys. It was an opportunistic industry of very small players,” says Andy Reiser, chairman and chief executive of Strategic Funding Source Inc., a New York-based alternative funder that’s been in business since 2006. “The industry has gone from this cottage industry to a professionally managed industry.”

Indeed, the alternative funding industry for small businesses has grown by leaps and bounds over the past decade. To put it in perspective, more than $11 billion out of a total $150 billion in profits is at risk to leave the banking system over the next five plus years to marketplace lenders, according to a March research report by Goldman Sachs. The proliferation of non-bank funders has taken such a huge toll on traditional lenders that in his annual letter to shareholders, J.P. Morgan Chase & Co. chief executive officer Jamie Dimon warned that “Silicon Valley is coming” and that online lenders in particular “are very good at reducing the ‘pain points’ in that they can make loans in minutes, which might take banks weeks.”

The burgeoning growth of alternative providers is certainly driving banks to rethink how they do business. But increased competition is also having a profound effect on more seasoned alternative funders as well. One of the latest threats to their livelihood is from fintech companies, like Lendio and Fundera,for example, that are using technology to drive efficiency and gaining market share with small businesses in the process.

“Established lenders who want to effectively compete against the new entrants will need to automate as much decisioning as possible, diversify acquisition sources and ensure sufficient growth capital as a means to capture as much market share as possible over the next 12 to 18 months,” says Kim Anderson, chief executive of Longitude Partners, a Tampa-based strategy consulting firm for specialty finance firms.

Of course, there is truth to the adage that age breeds wisdom. Established players understand the market, have a proven track record and have years of data to back up their underwriting decisions. At the same time, however, experience isn’t the only factor that can ensure a company will continue to thrive over the long haul.

WORKING TOWARD THE FUTURE

Indeed, established players have a strong understanding of what they are up against—that they can’t afford to live in the glory of the past if they want to survive far into the future.

“With every business you have to reinvent yourself all the time. That’s what a successful business is about,” says Reiser of Strategic Funding. “You see so many businesses over the years that didn’t reinvent themselves, and that’s why they’re not around.”

Strategic Funding has gone through a number of changes since Reiser, a former investment banker, founded it with six employees. The company, which has grown to around 165 employees, now has regional offices in Virginia, Washington and Florida and has funded roughly $1 billion in loans and cash advances for small to mid-sized businesses since its inception.

One of the ways Strategic Funding has tried to distinguish itself is through its Colonial Funding Network, which was launched in early 2009. CFN is Strategic Funding’s secure servicing platform which enables other companies who provide merchant cash advances, business loans and factoring to “white label” Strategic Funding’s technology and reporting systems to operate their businesses.

“When you’re in a commodity-driven business, you have to find something to differentiate yourself,” Reiser says.

FINDING WAYS TO BE DIFFERENT

That’s exactly what Stephen Sheinbaum, founder of Bizfi (formerly Merchant Cash and Capital) in New York, has tried to do over the years. When the company was founded in 2005, it was solely a funding business. But over the years, it has grown to around 170 employees and has become multi-faceted, adding a greater amount of technology and a direct sales force. Since inception, the Bizfi family of companies has originated more than $1.2 billion in funding to about 24,000 business owners.

Earlier this year, the company launched Bizfi, a connected online marketplace designed specifically to help small businesses compare funding options from different sources of capital and get funded within days. Current lenders on the platform include Fundation, OnDeck, Funding Circle, CAN Capital, SBA lender SmartBiz, as well as financing from Bizfi itself. Financing options on the platform include short-term funding, equipment financing, A/R financing, SBA loans and medium term loans.

Earlier this year, the company launched Bizfi, a connected online marketplace designed specifically to help small businesses compare funding options from different sources of capital and get funded within days. Current lenders on the platform include Fundation, OnDeck, Funding Circle, CAN Capital, SBA lender SmartBiz, as well as financing from Bizfi itself. Financing options on the platform include short-term funding, equipment financing, A/R financing, SBA loans and medium term loans.

Sheinbaum credits newer entrants for continually coming up with new technology that’s better and faster and keeping more established funders on their toes.

“If you don’t adapt, you die,” he says. “Change is the one constant that you face as a business owner.”

David Goldin, chief executive of Capify, a New York-based funder, has a similar outlook, noting that the moment his company comes out with a new idea, it has to come up with another one. “If you’re not constantly innovating you’re in trouble,” he says. “It’s a 24/7 global job.”

Capify, which was known as AmeriMerchant until July, was founded by Goldin in 2002 as a credit card processing ISO. In 2003, the company began focusing all of its efforts on merchant cash advances. Four years later, the company made its first international foray by opening an office in Toronto. The company continued to expand its international presence by opening up offices in the United Kingdom and Australia in 2008. The company now has more than 200 employees globally and hopes to be around 300 or more in the next 12 months, Goldin says. The company has funded about $500 million in business loans and MCAs to date, adjusted for currency rates.

THE CULTURE OF CHANGE

Five or six years ago, Capify’s main competitors were other MCA companies. Now the competition primarily comes from fintech players, and to keep pace Capify has made certain changes in the way it operates. From a human resources standpoint, for instance, Capify switched from business casual attire to casual dress in the office. The company has also been doing more employee-bonding events to make sure morale remains high as new people join the ranks. “We’ve been in hyper-growth mode,” he says.

CAN Capital in New York, another player in the alternative small business finance space with many years of experience under its belt, has also grown significantly (and changed its name several times) since its inception in 1998. The company which began with a handful of employees now has about 450 and has offices in NYC, Georgia, Salt Lake City and Costa Rica. For the first 13 years, the company focused mostly on MCA. Now its business loan product accounts for a larger chunk of its origination dollars.

This year, the company reached the significant milestone of providing small businesses with access to more than $5 billion of working capital, more than any other company in the space. To date, CAN Capital has facilitated the funding of more than 160,000 small businesses in more than 540 unique industries.

Throughout its metamorphosis to what it is today, the company has put into place more formalized processes and procedures. At the same time, the company has tried very hard to maintain its entrepreneurial spirit, says Daniel DeMeo, chief executive of CAN Capital.

One of the challenges established companies face as they grow is to not become so rule-driven that they lose their ability to be flexible. After all, you still need to take calculated risk in order to realize your full potential, he explains. “It’s about accepting failure and stretching and testing enough that there are more wins than there are losses,” says DeMeo who joined the company in March 2010.

ADVICE FOR NEWCOMERS

As the industry continues to grow and new alternative funders enter the marketplace, experience provides a comfort level for many established players.

“The benefit we have that newcomers don’t have is 10 years of data and an understanding of what works and what doesn’t work,” says Reiser of Strategic Funding. With the benefit of experience, Reiser says his company is in a better position to make smarter underwriting decisions. “There are many industries we funded years back that we wouldn’t touch today for a variety of reasons,” he says.

Experienced players like to see themselves as role models for new entrants and say newcomers can learn a lot from their collective experiences, both good and bad. Noting the power of hindsight, Reiser of Strategic Funding strongly advises newcomers to look at what made others in the business successful and internalize these best practices.

One of the dangers he sees is with new companies who think their technology is the key to long-term survival. “Technology alone won’t do it because that too will become a commodity in time,” he says.

Over the years Strategic Funding has learned that as important as technology is, the human touch is also a crucial element in the underwriting process. For example, the last but critical step of the underwriting process at Strategic Funding is a recorded funding call. All of the data may point to the idea that a particular would-be borrower should be financed. But on the call, Strategic Funding’s underwriting team may get a bad vibe and therefore decide not to go forward.

“We look at the data as a tool to help us make decisions. But it’s not the absolute answer,” Reiser says. “We are a combination of human insight and technology. I think in business you need human insight.”

Seasoned alternative funding companies also say that newbies need to implement strong underwritingcontrols that will enable them to weather both up and down markets.

The vast majority of newcomers have never experienced a downturn like the 2008 Financial Crisis, which is where seasoned alternative financing companies say they have a leg up. Until you’ve lived through down cycles, you’re not as focused as protecting against the next one, notes Sheinbaum of Bizfi. “Every 10 years or 15 years or so, there seems to be a systemic crisis. It passes. You just have to be ready for it,” he says.

Goldin of Capify believes that many of today’s start-ups don’t understand underwriting and are throwing money at every business that comes their way instead of taking a more cautious approach. As a funder that has lived through a down market cycle, he’s more circumspect about long-term risk.

One of the biggest problems he sees is funders who write paper that goes two or three years out. His company is only willing to go out a maximum of 15 months for its loan product, which he believes is s a more prudent approach. He questions what will happen when the economy turns south—as it eventually will—and funders are stuck with long dated receivables. “You’re done. You’re dead. You can’t save those boats. They are too far out to sea,” Goldin says.

One of the biggest problems he sees is funders who write paper that goes two or three years out. His company is only willing to go out a maximum of 15 months for its loan product, which he believes is s a more prudent approach. He questions what will happen when the economy turns south—as it eventually will—and funders are stuck with long dated receivables. “You’re done. You’re dead. You can’t save those boats. They are too far out to sea,” Goldin says.

Having a solid capital base is also a key to long-term success, according to veteran funders. Many of the upstarts don’t have an established track record and need to raise equity capital just to stay afloat—an obstacle many long-time funders have already overcome.

Goldin of Capify believes that over time consolidation will swallow up many of the newbies who don’t have a good handle on their business. Hethinks these companies will eventually be shuttered by margin compression and defaults. “It can’t last like this forever,” he says.

In the meantime, competition for small business customers continues to be fierce, which in turn helps keep seasoned players focused on being at the top of their game. Getting too comfortable or complacent isn’t the answer, notes DeMeo of CAN Capital. Instead, established funders should seek to better understand the competition and hopefully surpass it. “Competition should make you stronger if you react to it properly,” he says.