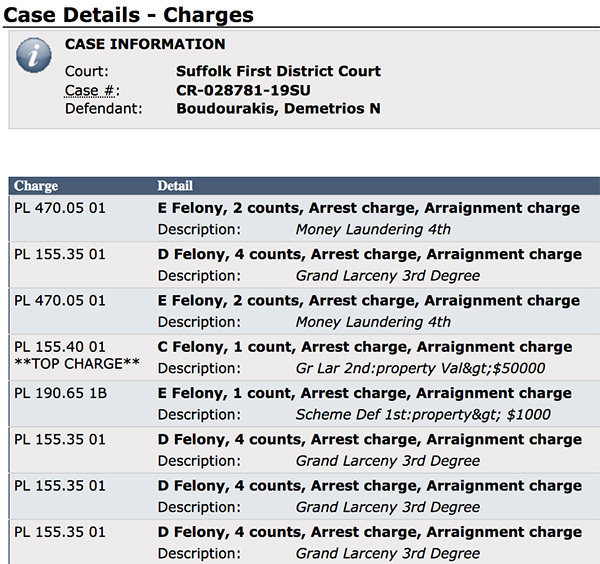

Long Island Business Loan Brokers Arrested in Bust

June 13, 2019 The owner of a Long Island based ISO/loan brokerage and several employees have been arrested, Newsday reports. Demetrios Boudourakis, whom deBanked has previously reported on, is charged with grand larceny, money laundering and other crimes for his role in an advance fee loan scheme. Boudourakis allegedly led a fraud ring that stole more than $2 million from small business owners nationwide. Six other defendants have also been charged with related crimes. They include Nadim Afzali of Hicksville, Tanya Balbi of Farmingdale, Christopher Looney of Bethpage, Joseph Johnson of Brentwood, Jude Brun of Elmont, and Michelle Soccodato of Hicksville.

The owner of a Long Island based ISO/loan brokerage and several employees have been arrested, Newsday reports. Demetrios Boudourakis, whom deBanked has previously reported on, is charged with grand larceny, money laundering and other crimes for his role in an advance fee loan scheme. Boudourakis allegedly led a fraud ring that stole more than $2 million from small business owners nationwide. Six other defendants have also been charged with related crimes. They include Nadim Afzali of Hicksville, Tanya Balbi of Farmingdale, Christopher Looney of Bethpage, Joseph Johnson of Brentwood, Jude Brun of Elmont, and Michelle Soccodato of Hicksville.

The investigation began last year and involved numerous agencies, including the Suffolk and Nassau police and sheriff’s departments, New York State Police, the FBI and the Drug Enforcement Administration.

The investigation began last year and involved numerous agencies, including the Suffolk and Nassau police and sheriff’s departments, New York State Police, the FBI and the Drug Enforcement Administration.

According to Newsday, “Boudourakis and his associates, through the dark web, obtained the names of people who had been denied loans. They would then call those people to tell them they had qualified for loans but would have to pay interest and fees upfront.”

According to Long Island Business News, law enforcement agents who executed search warrants at several locations recovered electronic equipment, three handguns, a sawed-off shotgun and a pill press. The investigation leading up to the bust included court-authorized eavesdropping and audits of financial records and physical and electronic surveillance.

Previously, AltFinanceDaily reported that JTT Funding, Boudourakis’ company, had been accused of forging a Confession of Judgment and impersonating rival companies. Those were civil cases, not criminal cases. Court records show that those cases remain ongoing.

Among the company names the ring used in the alleged scheme were Federal Business Lenders, Federal Business Funding, JTT Funding, JTT Global Holdings, Inc. Blackrock Funders, Inc. and Blackrock, Inc. It is possible that some of those names closely resemble names of competitors and the actual companies have not been accused of any wrongdoing.

Boudourakis is a retired MMA fighter. His nickname in the ring was “The Tyrant.”

ForwardLine, One of the Original Funding Companies, is Back

June 5, 2019 Steve Carlson, CEO, ForwardLine

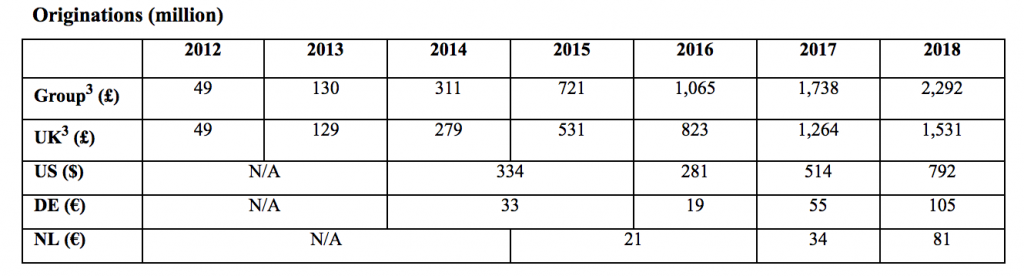

Steve Carlson, CEO, ForwardLineForwardLine Financial originated well over $65 million in loans in 2018, according to CEO Steve Carlson. ForwardLine would not share its origination numbers, but Carlson said the company is comfortably on the AltFinanceDaily list of top originators. ($65 million is the lowest origination number on the list).

Last week, the company announced that it secured a $100 million credit facility from Credit Suisse AG and Neuberger Berman private equity funds. This is the company’s largest credit facility to date. Its previous credit facility was with East West Bank and that relationship is still in place.

ForwardLine is a direct marketer that provides working capital loans of up to $200,000 to small businesses.

Carlson told AltFinanceDaily that ForwardLine, which was founded in 2003, has been scaling its business dramatically over the past year and a half. This is no coincidence. Instead, Carlson said this is the result of years worth of planning following a majority investment in ForwardLine in 2015 by a private equity firm called Vistria Group.

“We spent 2016 and 2017 very thoughtfully building out a technology platform, a data infrastructure, and a management team to scale the business,” Carlson said. “We’re now actioning on that plan. So this is all part of a multi-year strategy.”

A company statement said that the company’s loan performance in 2018 was record-breaking. ForwardLine increased year-over-year total originations by over 300% in the first quarter of 2019.

Carlson said that the new facility will be used primarily to grow the business. ForwardLine is located in Woodland Hills, CA, and it employs 110 people, more than half of whom work in the sales department. Other employees include underwriters and data and analytics people.

Funding These Franchises? Read This First

May 29, 2019

United States Senator Catherine Cortez Masto is concerned with the abilities of four major franchises to repay business loans, according to a letter penned to the Small Business Administration. They include Subway, Complete Nutrition, Dickey’s Barbecue, and Experimac. The issues raised should be on the radar of every provider of capital.

For Subway, Cortez Masto cites a New York Post article that alleged Subway Restaurants is plotting to put its own franchisees out of business through the enforcement of minor handbook violations. A whopping 1,108 Subway stores closed last year alone.

For Complete Nutrition, the franchisor is reportedly dismantling its own franchise. Cortez Masto says it first raised the prices of goods, wiping out franchisee profit margins. Following that, it eliminated its franchise model altogether, took away their franchisees’ POS systems, removed their locations from the Complete Nutrition website, and informed Complete Nutrition customers that the stores had been sold and to order online going forward instead of from the stores. At least 12% of SBA loans made to Complete Nutrition locations have been charged off.

For Dickey’s Barbecue, the franchise is experiencing more stores closing than opening. Cortez Masto suspects that the franchisor is providing misleading and inaccurate information to potential franchisees, resulting in failed stores and bankrupt business owners. A franchise blogger says, “The Dickey’s business model seems odd, continually selling new franchises to replace closed units, but seemingly doing little to fix the profit structure so existing franchisees survive.”

For Experimac, Cortez Masto says that most of the SBA loans made to Experimac were originated by Celtic Bank and that to-date 23% of these loans have failed.

OnDeck Slips To #3 in Tight Pack of Top Small Business Lenders

May 3, 2019 With most 2019 Q1 earnings in for public companies, the industry’s biggest lenders are off to the races. Square reported on Wednesday that Square Capital, its business lending arm, originated $508 million in loans in the first quarter of the year. Meanwhile, OnDeck originated $636 million this quarter, according to its earnings report released yesterday. Kabbage, which is not a public company, has been trailing very closely behind OnDeck for the last few years but someone familiar with the company said that Kabbage’s originations in the first quarter of this year surpassed OnDeck’s.

With most 2019 Q1 earnings in for public companies, the industry’s biggest lenders are off to the races. Square reported on Wednesday that Square Capital, its business lending arm, originated $508 million in loans in the first quarter of the year. Meanwhile, OnDeck originated $636 million this quarter, according to its earnings report released yesterday. Kabbage, which is not a public company, has been trailing very closely behind OnDeck for the last few years but someone familiar with the company said that Kabbage’s originations in the first quarter of this year surpassed OnDeck’s.

Then there is PayPal, which has not released official origination numbers for 2019 Q1. But earlier statements from PayPal that they had surpassed a billion dollars in quarterly small business funding in 2018 (already more than OnDeck), would put it in the #1 slot for originations. Additionally, a comment made by PayPal CEO Dan Schulman during the company’s earnings call last week implied that its Q1 2019 earnings are again over a billion dollars.

PayPal’s estimated originations number represents its US and international originations, including their business financing products available in the UK, Australia, Germany and Mexico. Likewise, OnDeck’s number represents originations from the US along with its smaller markets in Australia and Canada.

Square Capital operates exclusively in the US, so its originations number is US-only. And Kabbage’s undisclosed estimated originations number represents purely US originations.

| Company Name | 2019 Q1 Funding Volume |

| PayPal | $1,000,000,000+ |

| Kabbage | $650,000,000* |

| OnDeck | $636,000,000 |

| Square | $508,000,000 |

Has PayPal Eclipsed OnDeck in Small Business Loans?

April 26, 2019

It’s been said that Kabbage is on pace to surpass OnDeck in small business loan originations, but PayPal has already done it.

When PayPal announced a working capital program in the Fall of 2013, few were predicting that the initiative would propel them to the top of the small business lending charts. Just two years later, however, the payment processing giant had already loaned more than $1 billion to small businesses.

Today, that number is over $10 billion, according to a comment made by PayPal CEO Dan Schulman on the company’s Q1 earnings call.

That figure would suggest that they had loaned approximately $9 billion from Fall 2015 to the end of Q1 2019. OnDeck, by comparison, loaned $7.5 billion since Fall 2015 through Q4 2018. Several other data sources, including previous statements from PayPal that they had surpassed more than a billion dollars in quarterly small business funding in 2018 (already more than OnDeck), indicate that PayPal has become #1 on the AltFinanceDaily small business funding leaderboard.

PayPal’s growth was helped in part by its acquisition of Swift Capital in 2017.

Two of the top four are payment processors:

| Company Name | 2018 Originations | 2017 | 2016 | 2015 | 2014 | |

| PayPal | $4,000,000,000* | $750,000,000* | ||||

| OnDeck | $2,484,000,000 | $2,114,663,000 | $2,400,000,000 | $1,900,000,000 | $1,200,000,000 | |

| Kabbage | $2,000,000,000 | $1,500,000,000 | $1,220,000,000 | $900,000,000 | $350,000,000 | |

| Square Capital | $1,600,000,000 | $1,177,000,000 | $798,000,000 | $400,000,000 | $100,000,000 | |

| Funding Circle (USA only) | $500,000,000 | |||||

| BlueVine | $500,000,000* | $200,000,000* | ||||

| National Funding | $427,000,000 | $350,000,000 | $293,000,000 | |||

| Kapitus | $393,000,000 | $375,000,000 | $375,000,000 | $280,000,000 | ||

| BFS Capital | $300,000,000 | $300,000,000 | ||||

| RapidFinance | $260,000,000 | $280,000,000 | $195,000,000 | |||

| Credibly | $180,000,000 | $150,000,000 | $95,000,000 | $55,000,000 | ||

| Shopify | $277,100,000 | $140,000,000 | ||||

| Forward Financing | $125,000,000 | |||||

| IOU Financial | $91,300,000 | $107,600,000 | $146,400,000 | $100,000,000 | ||

| Yalber | $65,000,000 |

*Asterisks signify that the figure is the editor’s estimate

Lending Club Calls It Quits On Underwriting Small Business Loans

April 23, 2019

Lending Club will no longer be underwriting small business loans, according to Lending Club Head of Communication VP Anuj Nayar. The company will still accept applications for them, but will direct them instead to Opportunity Fund and Funding Circle in exchange for referral fees. Less established businesses, or those with lesser credit, will be sent to Opportunity Fund, while more established businesses with better credit will go to Funding Circle.

According to Nayar, there will be no layoffs. Some employees who had worked in small business underwriting will move elsewhere within Lending Club while others will become contractors for Opportunity Fund. Opportunity Fund is a non-profit with the mission of investing in small businesses that have been shut out of the financial mainstream. It is backed by major financial institutions including Bank of America, Goldman Sachs and the JP Morgan Chase and Knight Foundations. In fiscal year 2017, Opportunity Fund made over $92.5 million in loans to more than 2,900 small business owners.

“[These two partnerships] enables us to both deliver greater value to our applicants and capture a new revenue stream for Lending Club, while further simplifying our business and setting the stage for more partnerships and innovations for Club Members,” said Lending Club CEO Scott Sanborn.

The new revenue stream Sanborn refers to is the referral fees Lending Club will get from its new funding partners when they fund loans sent to them from Lending Club. And Lending Club’s business will be streamlined as it jettisons small business lending backend operations. They will now focus exclusively on consumer loans, which has been the company’s primary business since it was founded in 2006.

Lending Club expanded into small business lending several years ago, but this component of its business never really took off, and was declining over the last few years. At the end of December 2016, Lending Club’s non-consumer loan originations (including small business loans) accounted for 10% of its business. In December 2017, it was 9%. And in the fourth quarter of 2018, it was 7%.

Nayar said that these new partnerships will allow Lending Club to focus even more on consumer lending. Headquartered in San Francisco, Lending Club has lent more than $44 billion to 2.5 million customers.

Competition Steps Up in Canadian Small Business Lending Market

March 11, 2019 Last week’s announcement by Funding Circle that it will establish an operation in Canada later this year is part of a trend of large non-Canadian funders entering or expanding into the Canadian market, according to Adam Benaroch, President of CanaCap, a small business funder based in Montreal.

Last week’s announcement by Funding Circle that it will establish an operation in Canada later this year is part of a trend of large non-Canadian funders entering or expanding into the Canadian market, according to Adam Benaroch, President of CanaCap, a small business funder based in Montreal.

Funding Circle started in the UK and expanded outwards to the US, Germany, and The Netherlands, but the UK still comprises of more than 60% of their global origination volume. Their foray into Canada is a good thing for small business owners and lenders, according to Paul Pitcher, founder and CEO of SharpShooter, a funder based in Toronto.

“I see it as win-win,” Pitcher said.

He said that a win for Canadian small business owners is a win for SharpShooter because it means more potential merchant clients. Pitcher said that he loves OnDeck, a rival, is in Canada, in part because OnDeck’s marketing has helped educate Canadian merchants about alternative lending products.

Similarly, Benaroch said he thinks that big companies entering the Canadian market will affect CanaCap positively. For instance, Benaroch said that CanaCap hopes to capture companies that get turned down from OnDeck. And perhaps CanaCap can also capture merchants that are declined by Funding Circle.

Funding Circle’s loan originations by country by year

Funding Circle’s loan originations by country by year

Benaroch noted that not all outside funding companies have succeeded in Canada, often because they never established a physical presence there. But Funding Circle will be opening a physical office in Toronto.

“We have been evaluating options for expansion over the last year,” said Tom Eilon, who will be Managing Director of Funding Circle Canada. “Canada’s stable, growing economy coupled with good access to credit data and a progressive regulatory environment, made it the obvious choice. The most important factor [in coming to Canada] though was the clear need for additional funding options among Canadian SMEs.”

Funding Circle’s announcement comes on the heels of OnDeck’s December 2018 acquisition of Evolocity Financial Group, a small business funder based in Montreal. While OnDeck started operating in Canada as early as 2015, CanaCap’s Adam Benaroch said that the acquisition of Evolocity is a significant step for OnDeck because Evolocity has an ISO channel in Canada. That runs counter to Funding Circle’s model of mainly going direct to merchant, at least in the US.

Small Business Funders Court Florists Before Valentine’s Day

February 14, 2019 Earlier this month, LendingTree published results from a survey they conducted about consumer spending on Valentine’s Day.

Earlier this month, LendingTree published results from a survey they conducted about consumer spending on Valentine’s Day.

The main takeaway is that men are planning to spend almost two and a half times more than what their significant others (of either gender) expect them to spend. So there might be some nice surprises today! On average, according to this survey, men plan to spend $95 today for their significant others, while women plan to spend $41. Also according to this survey, those who are engaged plan to spend $92 on their significant other, people in the dating stage of relationships plan to spend $88, and married people plan on spending $57. (The average for men is increased by spending based on generation.)

Regardless, Director of Personal Loans at LendingTree, Michael Funderburk, said that these amorous expenses are typically not large enough to show any spike in consumer borrowing. Small business borrowing, however, is a different story. As might be expected, there is a noticeable spike in borrowing from florists, among other small businesses that cater to the holiday.

Chad Otar, CEO of New York-based Excel Capital, a small business funder, said that they always fund more florists, chocolate shops and gift shops leading up to Valentine’s Day because these merchants need additional money to buy more inventory. Excel’s team of a little under 20 includes an in-house sales team that Otar said markets to these kinds of businesses in the weeks before Valentine’s Day.

The larger Reliant Funding, which has a sales team of about 100 people, makes an active marketing push before Valentine’s Day to reach more than 13,000 U.S. florists in its database, according to its Chief Marketing Officer Steve Kietz.

“Our business with these firms increases before Valentine’s Day and Mother’s Day,” Kietz said. “We see lots of repeat business from those firms as they stock up for peak season. [And] we increase our mail and digital marketing activities to sync with when florists will be most responsive.”

Houston-based Accord Funding, doesn’t have an in-house sales team. Still, its CEO, Adam Beebe, said that while they don’t track submissions by merchant category, they do underwrite florists with seasonality in mind.