Meet the Lending Platform With 0% Interest (Kiva)

January 6, 2016 Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Meet Kiva Zip, the anti-Lending Club because the borrowers are far from anonymous and the yield delivered to investors is negative due to inflation.

Angela’s Boutique, which is a real prospect on the Kiva Zip platform, includes a picture of the owner, her bio, endorsements, and comments from supporters.

According to Jessica Feingold, Kiva’s East Coast Manager of Development, “Kiva is the world’s first and largest crowdfunding platform for social good with a mission to connect people through lending to alleviate poverty and expand economic opportunity.”

And just like Lending Club, contributions as small as $25 are accepted. Obviously structured as a non-profit, “Kiva and its growing global community of 1.2 million lenders has crowdfunded more than $775 million in microloans to over 1.7 million entrepreneurs in 83 countries, all the while maintaining a 98% repayment rate,” according to Feingold.

Normally thought of as an overseas endeavor, Feingold said that “in 2011, Kiva launched Kiva Zip, a pilot program in the US that provides 0% interest crowdfunded loans to small business entrepreneurs.” Their underlying purpose and target market sounds very much like those being served by for-profit alternative lenders. “Kiva doesn’t require a minimum FICO score, collateral, or a minimum operations period for the business,” Feingold said.

Since inception they’ve made loans to over 1,800 borrowers in 47 days states, Peru, and Guam.

Notably, Lending Club promises borrowers that their “identity will at all times remain confidential and not be disclosed to anyone,” according to their website. Kiva by contrast is looking to “instill empathy” in their lenders. “We want to show that whether in East New York or Uganda, underserved entrepreneurs are credit-worthy, and will pay you back,” Feingold said. “All of these features on the Kiva websites enhance our ability to do so.”

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

According to the law, no loan underwriter or other officer or employee of a financial institution, or any affiliate of a financial institution, involved in making any determination concerning an application for credit shall have access to any information provided by the applicant about whether or not the business is women-owned or minority owned.

As small businesses often celebrate the heritage of their founders, and at times that can be the entire reason customers buy from them in the first place, the law has presumably put the small business lending world in an awkward position (and that’s why the law should be repealed). Non-profits like Kiva have embraced the very things that make a small business bankable outside of a credit score, like the owner, their background, and their story.

Borrowers on the Kiva Zip platform don’t raise all the money from strangers though. Their credit-worthiness is based on their ability to recruit friends and family to fund a small portion of their loan. The other lenders though of course may make their decisions based on the numbers or entirely on the perceived cultural, racial, or gender values of the borrower, all of the things that the CFPB is attempting to eradicate in the for-profit arena.

I didn’t ask Kiva any questions about Dodd Frank or Section 1071, but many people might empathize with their empathy approach as a way to fund small businesses that otherwise don’t qualify for bank loans. Its reminiscent of the subjective underwriting that a lot of alternative lenders and merchant cash advance companies employ to get deals done that banks won’t touch.

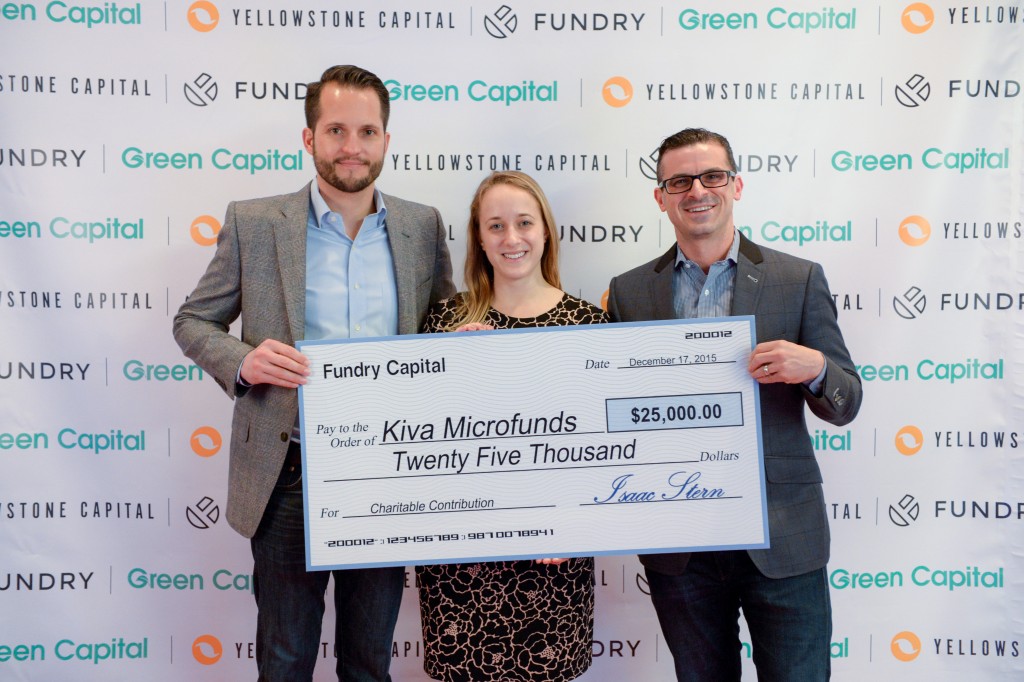

Not so coincidentally, Fundry, Yellowstone Capital’s parent company, donated $25,000 to Kiva just last month to support their cause.

Kiva’s Feingold (pictured at center above) said in regards to that, “Kiva is thrilled to receive a grant from Fundry to further our work to make credit more affordable.”

Why You Shouldn’t Overlook Selling Merchant Processing

January 4, 2016 Prior to daily fixed payment business loans, there was the traditional merchant cash advance (MCA). The MCA, being the only option, required merchants to tie their need for working capital to that of their merchant accounts, either directly or indirectly, through the use of either split-funding or a lockbox account.

Prior to daily fixed payment business loans, there was the traditional merchant cash advance (MCA). The MCA, being the only option, required merchants to tie their need for working capital to that of their merchant accounts, either directly or indirectly, through the use of either split-funding or a lockbox account.

DIRECT OR INDIRECT?

Split-funding is a direct method that requires the merchant to convert their merchant account over to a chosen Independent Sales Organization (ISO), you could also refer to the ISO as a Merchant Service Provider (MSP). The MCA company contracts with an ISO/MSP who then manages the flow of the merchant’s daily credit card processing volume. A percentage is withheld and forwarded to the buyer of those receivables.

The lockbox is an indirect method to manage the flow of funds. Rather than withhold funds from the ISO/MSP, a separate FDIC insured account is established on the side for all credit card processing receipts to settle into initially, with a percentage of that volume going to the buyer and the remaining amount “swept” into the merchant’s operating account.

Nevertheless, whether directly or indirectly, the merchant account of the business owner was the foundation of the MCA approval and facilitation. Because many MCA companies also offer alternative business loans today with fixed payments, a lot of the new broker entrants do not believe that learning about the field of merchant processing is as important today as it was years ago. However, I disagree with this notion, as the purpose of our industry is the long term relationship with the client, and in many ways the traditional MCA product provides more “benefits and value” to the merchant over time than today’s business loan. Just as new broker entrants get to know all about the MCA, they should also get to know all about merchant processing.

OVER TIME, CAN THE MCA BE THE BETTER CHOICE?

The alternative business loan requires no merchant account conversion as it doesn’t tie the merchant account to the facilitation of the working capital transaction. With these loans, a percentage of gross revenues are approved with fixed terms up to 36 months on daily or weekly payments. The main benefit of this product over the MCA is the awareness of payment frequency and quantity upfront, thus, enabling the merchant to better allocate their cash flow.

However, while the traditional merchant cash advance requires the tie-in of the merchant account, there’s no fixed terms nor fixed payments as it correlates with the merchant’s sales cycle, where they deliver more during busy times, less during slow times.

When selling the merchant the long term aspects of the MCA, why not seek to get their MCA funded using the split-funding method rather than a lockbox? Doing so would provide an additional revenue stream within your client portfolio. To properly seek out this opportunity and be able to consult, convince and convert the merchant over to your MCA firm’s ISO/MSP Partner, you want to fully understand what merchant processing is all about.

WHAT IS MERCHANT PROCESSING?

A merchant account is an unsecured line of credit provided to a business from a registered ISO/MSP. The credit line enables the business to benefit from accepting Visa and MasterCard (V/MC) along with other major bankcards from their customer base, to experience the benefits of acceptance which includes better fraud management, higher average tickets, customer loyalty due to convenience, and more. V/MC are just registered card brands that manage a group of banks called “member banks”, which are banks apart of a listing of V/MC bank associations. The member banks pay V/MC dues and assessments to market their brands. You have different types of member banks, you have the Issuing Banks and then you have the ISO/MSP along with the Sponsoring Banks.

The Issuing Banks issue credit cards with credit limits to consumers after they meet credit criteria. On the processing side, you have the registered ISO/MSP and Sponsor Banks, which approve a merchant for a merchant account and process payments through a front-end authorization network, then settles them through a back-end network.

During the processing of a credit card transaction, there’s a couple of different fees that are charged. Interchange is one of the fees charged, which is how the Issuing Banks are paid. These are wholesale prices for every type of card that a merchant could potentially run at the point of sale, with new interchange pricing charts released in April and October of every year. The ISO/MSPs are paid when they mark-up interchange as well as through fees such as an annual fee, statement fee and batch fee.

WHY IS MERCHANT PROCESSING A UNSECURED LINE OF CREDIT?

The merchant account is indeed an unsecured line of credit, because when a merchant’s customer runs an order on their credit card for $500, the merchant would rather have that entire $500 upfront rather than waiting for the customer to pay off their credit card balance in full, which could potentially take years. As a result, the ISO/MSP deposits the amount in their bank account within 48 hours rather than having the merchant wait until their customer pays their credit card balance in full.

Now, if the merchant’s customer initiates a chargeback of the $500 transaction and the merchant loses the case, the $500 would have to be refunded by the merchant plus the costs of the chargeback which includes a chargeback fee and retrieval fee. If the ISO/MSP goes to get the $500 from the merchant and there’s no money in their account (let’s say the merchant has gone out of business), then the ISO/MSP who underwrote the merchant account is on the hook for the charge.

WHY SHOULD YOU SELL MERCHANT PROCESSING?

When using split funding for a merchant cash advance deal, if you switch over their processing to an ISO/MSP that your MCA firm currently split funds with, you are looking at collecting the long term residuals from the processing and the compensation from future merchant cash advance renewals. In addition, split funding is much more efficient than using a lockbox, as a lockbox usually adds 1-2 business days to the settlement process for everyone involved. Withsplit funding, the merchant can continue to receive their processing deposits as normal.

There are different types of payment processing technologies depending on what the merchant needs, if they need a stand-alone solution then that’s available in the form of a landline terminal, wireless terminal, computer software or virtual terminal. If the merchant needs a comprehensive solution then that’s also available in the form of point-of-sale systems or operational management technologies, both of which integrate merchant processing into the system and other operational aspects such as accounting, payroll, human resources, etc.

Why not just have the merchant switch over their processing to an ISO/MSP that your MCA firm currently split funds with, and collect recurring merchant processing residuals along with recurring income from merchant cash advance renewals? After all, recurring income is the lifeblood of our business.

Year of The Broker Concludes – 2015 Recap

December 31, 2015 It was the Year of the Broker, a phrase that often conjured up images of easy money and inexperience. Lenders like OnDeck reacted by reducing their dependence on them. Responsible for 68.5% of their deal flow in 2012, OnDeck only sourced 18.6% of their deals from brokers in the third quarter of 2015.

It was the Year of the Broker, a phrase that often conjured up images of easy money and inexperience. Lenders like OnDeck reacted by reducing their dependence on them. Responsible for 68.5% of their deal flow in 2012, OnDeck only sourced 18.6% of their deals from brokers in the third quarter of 2015.

But there’s money being made. One broker is on pace to do more than $100 million worth of deals annually after working as a plumber eight years ago. Another went from sleeping in his car to driving a Ferrari. Meanwhile, brokers like John Tucker are basically saying just the opposite. Tucker has repeatedly taken to AltFinanceDaily to preach things like “minimalism,” a practice of living below your means to a point where you can survive, and telling everyone it’s okay to embrace the satisfaction of a middle class life.

So is it the end of days or just the beginning?

In October, initial survey results of top industry CEOs revealed a confidence index of 83.7 out of 100, but out there on the street for the little guy, it’s been a tumultuous year. Things like commission chargebacks have hit brokers at unexpected times, with several funders privately telling us over the year that rogue brokers have closed their bank accounts or frozen the ACH debits in order to avoid giving the commissions back.

In 2015, brokers sued their sales agents and sales agents sued their employing brokers. Deals got backdoored, deals got co-brokered, and soliciting deals anonymously got banned from industry forums. Stacking continued mostly unfettered but is being pursued in the court system by funders allegedly injured by it. Brokers took over Wall Street and are supposedly being watched by regulators. Oh, and robo-dialing? Brokers should probably steer clear of that, just as underwriters should ditch paper bank statements.

It’s a lot to manage. Sometimes for a broker, just losing a deal can make them so sick that they have to go home. That’s apparently what happens when you don’t answer the phone fast enough. At least one said there’s no room left for more competitors so if you were thinking of starting a brokerage now, $2,000 won’t be enough.

But things could be worse. In 2015, IOU Financial was under attack by Russian nuclear scientists, a story that was more truth than exaggeration. In the end, Qwave Capital acquired a 15% stake in IOU.

An OnDeck class action lawsuit that looked bad at first turned out to be mostly based on the words of a convicted stock manipulator with a short position in the stock. The case is still ongoing and OnDeck’s stock price is down 50% from their IPO.

In 2015, two guys lost God but found $40 million (although numerous sources say that number is off).

“Madden” no longer means the football video game and Section 1071 is not a seating area in a stadium.

An RFI turned out to be something not to LOL about. Despite an overwhelming response from lenders and funders, the Treasury isn’t completely sold.

Things weren’t so automated in 2015 despite the cries of technological disruption. Maybe that’s why it feels like 1997. Manual underwriting still dominated and bank statements still matter as much as they ever did. God declined loan applications, Google rigged the search results, and a mayor declared war on merchant cash advance (and then never spoke about it ever again after being re-elected).

Things weren’t so automated in 2015 despite the cries of technological disruption. Maybe that’s why it feels like 1997. Manual underwriting still dominated and bank statements still matter as much as they ever did. God declined loan applications, Google rigged the search results, and a mayor declared war on merchant cash advance (and then never spoke about it ever again after being re-elected).

Lobbying coalitions formed. NAMAA became the SBFA. The CFPB lied and community bankers testified.

But things are looking up. Brokers can obtain outside investments, get acquired, or make millions through syndication.

Bad Merchants are now ending up in more than one bad database, though a deal for the ages slipped through the cracks. Other merchants went to jail. Square went public and brought merchant cash advances along with them. The industry beamed its message through Times Square and one Democratic congressman has asked God to bless it all.

It was a crazy year. Marketplace lending became an acknowledged term (and the name of a conference) and already companies under that umbrella have been linked to presidential candidate (and desperate loser) Jeb Bush and the San Bernardino Terrorists. The FDIC had a few things to say and SoFi went triple-A. Marketplace lending is making a lot of people money, but when looking at the tax implications is there something funny?

In 2015, the big boys shared their wisdom and their figures. Turns out, it was beyond hyperbole. Brokers experienced an incredible rise or they pawned their ferrari to the other guys. Some focused on a specific crop, while others are trying it over the top. California sucked, John Tucker tucked, and one lender got totally F*****. In 2015 some funders got tanked, so in 2016 we’ll all be AltFinanceDaily.

Happy New Year!

The First Ever Comprehensive Industry Report is Now Available

December 29, 2015 Months ago, investment bank Bryant Park Capital teamed up with us to conduct the first ever industry CEO survey of its kind. A sample of the initial findings were distributed at Money2020 in Las Vegas. Eligible participants that disclosed their identities to the surveyors have already received a complementary copy of the full anonymized report.

Months ago, investment bank Bryant Park Capital teamed up with us to conduct the first ever industry CEO survey of its kind. A sample of the initial findings were distributed at Money2020 in Las Vegas. Eligible participants that disclosed their identities to the surveyors have already received a complementary copy of the full anonymized report.

Today, those that either weren’t eligible to take the survey or missed the deadline to participate, can buy a copy of it.

With a sample size of small business funding companies that originate more than $2 billion annually, the final report reveals the industry’s Compound Annual Growth Rate, Average Annual Revenues, Average Annual EBITDA, Portfolio Loss Rates, Approval Rates, M&A Expectations, Valuation Expectations, Syndication Data, and much more.

This report is highly recommended for all funders and ISOs seeking to raise capital or for those that want to eventually sell their company. It’s also a must-have for any company that seeks to set short-term or long-term goals, that wants to compare themselves against the industry, or is creating a realistic business plan.

Investors in the industry also stand to benefit from this data.

If you are interested in buying the full report, e-mail sean@debanked.com.

The original report sample for public distribution

Mentioned in Forbes

Bryant Park Capital’s professionals have completed approximately 400 assignments representing an aggregate transaction value of over $80 billion.

Brokers: It’s Okay To Delay Starting A Family

December 25, 2015 WE HAVE NO “MINIMUM” GUARANTEE

WE HAVE NO “MINIMUM” GUARANTEE

The debate to increase the minimum wage across the board in the US to $15 per hour has been going on for quite some time now, with marches in the street from fast food workers, people protesting by walking off the job, and strong political debate with passionate views on both sides.

What’s been strange to me about this debate, in relation to the argument of those that are in favor of increasing the minimum wage, is their reference to workers being “slave labor” by working excessively hard and long, but not making enough in a lot of cases to support a household. The reason this has been strange to me is because for close to 9 years, I operated on a 1099, independent, 100% commission basis, as a solopreneur managing my own one man show sales office. I received no salary, base pay, hourly pay, “floor”, nor company benefits (even though I am fully insured individually). The Harvard Business School report from July 2014 by Karen Gordon Mills and Brayden McCarthy, said that there’s 23 million businesses in the country that do not have any employees and are classified as Solopreneurs.

So, should myself and the other 23 million Solopreneurs in this country all be marching and protesting as well? And if so, marching and protesting against who? I work for 1ST Capital Loans, LLC, but I’m also the sole managing director, member and employee of said entity, so as a result, I should be marching and protesting against myself? We as independent brokers have no minimum guarantee or minimum wage, which not only makes the minimum wage debate strange, but it also points to another reality in that adding a family to our chaotic situation might not be optimal at this time.

RUNNING YOUR OWN SHOP IS VERY DIFFICULT

Running your own show is probably the hardest job you will ever have in your life. Having to juggle the various components of it with no established “minimum wage” just chokes out far too many independent brokers. Some of those various components include but surely aren’t limited to:

- Having to manage regulations, laws and other legal aspects

- Having to manage accounting, insurance and tax related aspects

- Having to design your own business plan and ROI formulas

- Having to come up with your own way of creative financing

- Having to manage your vendor, supplier along with partner negotiations and agreements

- Having to design your market strategy, solutions and spend time actually selling them

On top of this, you might have to deal with pet peeves of your Funder and Lender Partners, which could include them cheating you out of commissions, clawing back commissions after 45 days, cutting you off from your renewal and residual portfolios, among other things. These things rob you out of the hard earned commissions for deals that you fought for in one of the most competitive markets in the country (using your own capital, creativity, time and energy) to win.

MAKE A FAMILY NOW, OR DELAY DOING SO JUST A LITTLE BIT LONGER?

With all of the aspects of building your broker office that must be managed on your own, with no minimum guaranteed wage, benefits or true assistance, the next question becomes, how do you manage a family through the very early stages of all of this chaos? The reality is that there’s only so much time in the day. If you are just starting out your own shop and if you don’t currently have a present family to take care of, putting the creation of a family on hold might be your best bet. I once expressed that it was okay to be a piker, then I expressed that it was okay to be a minimalist, today I’m telling you that it’s okay to delay starting a family.

THE MILLENNIAL GENERATION FACES A LOT OF STRUCTURAL CHALLENGES

It seems as though most of the newer brokers in our space are a part of the Millennial Generation.

Generation Y (The Millennial Generation) begins usually around 1981 and lasts until about 1995, the Generation that follows (Generation Z) are those that were born just after 1995. Being a Millennial myself, I tend to keep abreast of many of the issues facing my generation, and while I currently do not have a family that I’m responsible for, I believe that many Millennials would agree that it’s seemingly more difficult today than ever before to manage a family:

- We Are Over-Educated and Under-Employed: We are in fact the most educated Generation, but some reports state that over 50% of us are under-employed, which means we are mainly a Generation of the over-educated and under-employed, saddled with student loan debt.

- Lack Of Security and Stability: Prior Generations had the luxury of working for one company, in one location and in one city, for the vast majority of their working career, and be able to retire with a pension, 401k, and strong retirement benefits from Social Security. Our Generation has no such securities, as many of us will have to change careers and work locations often during our working career, making it nearly impossible to seemingly ever purchase a home because purchasing a home only makes sense when you can estimate “staying put” in one area for at least 10 years. Also the lack of pensions, strong 401k plans, and the fact that we might not receive strong Social Security benefits further complicates the security issue.

- Our Cost Of Living Continues To Sky Rocket: From food to energy, from property taxes to rent, from insurance premiums to healthcare costs, from college tuition to day care expenses, our cost of living continues to skyrocket.

- Our Opportunities Are Being Stolen Away: Wages and business opportunities are either stagnant or flat out decreasing due to the rise of global competitive forces and IT/robotic automation stealing away our opportunities for income advancement.

So while you are trying to juggle the issues of building your broker office, you are also having to deal with competitive global forces and IT automation, along with the rising cost of living, along with deficiencies in job/income security and stability. So how in the world do you add a family of let’s say two kids on top of this chaos? Regardless of whether or not you are married or a single parent, the costs and risks of managing a family within this chaotic situation are significant.

IT’S OKAY TO DELAY STARTING A FAMILY

If you already have a family, obviously you can’t “give them back” and start over, so if you are seeking to enter this space and build your broker office, you are just going to have to find a way to juggle all of the chaos that’s present. However, if you are like me (a Millennial and Broker within this space), that hasn’t yet created a family, if you are still in the early stages of constructing your office, renewal and residual portfolios, then I would say that it’s “okay” to delay starting a family considering all of the chaotic issues that you would be facing today.

How long to delay such a very important choice is a personal one that you would have to manage, but for some of us, the choice might come down to opting out of creating a family altogether.

Got a Ferrari or Fine Art? If So, You May Have More Leverage Than You Think

December 23, 2015If you own a Ferrari, fine art or expensive wine, getting access to capital may be easier than you think.

Although it’s still a niche market, luxury asset-backed lending has been gaining traction lately, particularly with small and mid-size business owners. These executives are enticed by the ability to use certain high-priced valuables as a means of getting large amounts of cash quickly and often at a lower cost than other funding sources.

“People are increasingly learning that this is another option. It’s not for everybody, but it’s another option,” says Tom McDermott, chief commercial officer at Borro, a New York-based asset-backed lender that deals exclusively with luxury asset-based loans.

It’s notable that luxury asset-based lending by alternative funders is gaining ground at a time when unsecured money is so easy to come by. There are several reasons business owners are attracted to the idea of leveraging their valuables to attain cash. First off, they don’t need stellar credit or a proven track record in business to qualify. Secondly, they can typically get larger sums of money and at better rates than they might through other financing channels. A third reason is that many of them have already tapped out other funding options and leveraging their assets allows them to obtain additional funds quickly.

“A lot of small business owners have assets, so it’s something else for them to utilize in getting access to attractive small business financing,” says Steven Mandis, chairman of Kalamata Capital LLC, an alternative finance company in Bethesda, Maryland.

Here’s how the process typically works at most luxury asset-based lenders. Say a business owner wants to borrow against a high-priced item such as a top-of-the-line car, fine art or wine, jewelry or a luxury watch. First the luxury-based lender hires a third-party to appraise the item. Generally, depending on the asset and its marketability, lenders will lend 50 percent to 70 percent of the asset’s value. If the owner moves forward, the item or items are held and insured in a lender’s secure storage area until the loan is paid back. Default rates on these types of loans are relatively low, lenders say.

“People don’t want to put their house at risk when they need capital,” says McDermott of Borro. “They’d rather lose the Maserati or a lovely piece of art than the house,” he says. And even then, it doesn’t happen very often, he says. Borro clients only default on their loans about 8 percent of the time, McDermott says.

Barriers to Entry

To be certain, luxury-based lending is not a business that every funder wants to be in. For starters, there are a lot of regulatory hoops a funder has to jump through in order to do it. You need a pawnbroker’s license and a second-hand dealer license. You also need a secure facility or facilities to house the collateral, have secure ways of transporting the valuables, and you need to carry large amounts of insurance for the transfer of the items as well as during the holding period.

Indeed, keeping the items secure is critical. PledgeCap, a Lynbrook, New York-based funder, says on its website that it uses “cutting edge technology, top of the line bank vaults and armed guards” to keep a customer’s items safe. What’s more, all items are insured during transit and storage. All items are shipped through secured and insured FedEx shipping vendors for pickups and drop-offs.

“There aren’t a lot of players in the market because there are a lot of operational and legal requirements to adhere to. There are a lot of barriers to entry,” says Gene Ayzenberg, the company’s chief operating officer.

Putting Things in Perspective

Luxury asset-based lending is only a small subset of the overall asset-based lending market, which as a whole has been gaining ground in the past few years. After getting badly burned in the most recent recession, many lenders have come to appreciate the security blanket that collateral offers. According to the Commercial Finance Association’s quarterly Asset Based Lending Index, U.S. ABL loan commitments rose 7.2 percent in the second quarter, compared with the year-earlier period. In addition, new ABL credit commitments were 6.3% higher than the same period a year ago.

“Asset-based lending at one time used to be the lending of last resort. Now it’s the type of lending that it is accepted globally,” says Donald Clarke, president of Asset Based Lending Consultants Inc., a Hollywood, Florida-based company that provides due diligence services for lenders. “Today, everybody wants an asset.”

There’s not a lot of public data to gauge the size of the luxury market within the broader asset-based lending market. But a 2014 report that focuses on art lending gives more perspective to at least one facet of luxury asset-based lending.

Thirty six percent of the private banks polled said they offer art lending and art financing services using art and collectibles as collateral. That’s up from 27 percent in 2012 and 22 percent in 2011, according to the report by consulting firm Deloitte and ArtBanc, a company that provides art sales alternatives, valuations and collections management services.

Meanwhile, 40 percent of private banks said this would be a strategic focus in the coming 12 months, up considerably from the 13 percent who named this as a priority in 2012.

These market changes are likely driven by client demand. The Deloitte/ArtBanc survey found that 48 percent of establishes art collectors polled said they would be interested in using their art collection as collateral for a loan, up from 41 percent in 2012.

Many big banks won’t touch asset-based lending deals unless they are worth north of $5 million. Some community banks will do smaller deals, but many don’t have the necessary infrastructure or skill sets, explains Clarke, of Asset Based Lending Consultants. This, of course, leaves an opening for alternative funders to capture market share.

Luxury asset-based lending expected to experience growth

Some lenders say they expect demand for luxury asset-based loans to continue to increase over time as more people accumulate big-ticket items and they become more aware that they can satisfy their capital needs by leveraging those assets. “A lot of times they don’t even know they have this option available to them,” says Ayzenberg of PledgeCap.

He says most of his company’s customers are small and mid-size business owners. Often they have temporary cash flow issues, but bank loans aren’t necessarily an option for them for any number of reasons. For instance, some may have bad credit. Others may have excellent credit but not enough of a business track record to qualify for a bank loan. Others may not have the cash flow to secure the amount of money they need, or they may need the money very quickly. Asset-based lenders can generally make the money available within a day, whereas bank loans require a lot of paperwork and can take months to obtain.

Mandis, of Kalamata Capital, says his company has seen an increased willingness by business owners to put up their luxury assets as collateral in order to get larger amounts of money at more favorable terms. Many times business owners have a high-priced asset that they don’t want to sell and pay a tax or can’t easily unload within a short-time frame. By borrowing against the luxury asset, they will get the capital to take advantage of a short-term opportunity and make an attractive return quickly without having to worry about finding a buyer or paying taxes on the sale of the asset, he explains.

Certainly luxury asset-based lending is not for every customer. Not only do you have to have a valuable asset to be used as collateral, but you also have to be willing to part with the item while the loan is outstanding. The risk of default and not getting the item back may also be a barrier for some people.

“I would be very hesitant to put up my wife’s diamond ring for my business. I don’t think it’s typically someone’s first choice,” says Ami Kassar, chief executive and founder of Multifunding LLC, a company in Ambler, Pennsylvania that helps small businesses find the best loan for their business. He remembers considering this option for a client only once in the past several years and the client ultimately chose another funding source.

But companies that focus on luxury asset-based lending say there is a viable market for their services that will continue to grow as more people hear about it and use it successfully to fulfill their funding needs. People have been taking their small items to pawn shops for many years. Working with a licensed lender to leverage their larger and often more expensive items gives them an option they may not have had previously. “You can’t just drive a tractor into a local pawnshop and say, ‘Here just put this in your safe,’” says Ayzenberg of PledgeCap.

Also, unlike pawn shops, luxury asset-based lenders say they aren’t looking to sell the items to make a quick buck and will only sell the item as a last resort if a customer defaults and they can’t reach agreeable terms. “We want them to keep their items,” says Ayzenberg whose company has been in business since 2013. For every 100 loans, there are only a small percentage of customers that default and lose the items, he says.

Every lender runs their business slightly different. At Borro, for example, loans typically range between $20,000 and $10 million and span in time frame from three months to three years. Rates start in the mid-teens and are based on the size of the loan, the time frame and how easy the asset would be to sell. In order to work with Borro, the asset typically has to be worth more than around $40,000, McDermott says.

Borro, which has been in business since 2009, deals with customers directly. But it also gets a good number of referrals from other lenders. Let’s say a customer needs $500,000 and a particular lender can only offer a maximum of $350,000. That lender might refer the client to Borro, which kicks in $150,000 based on the value of a leveraged asset. The referring company gets a commission based on the loan value and doesn’t lose the whole deal. “It’s a way to keep your customers tied in with you,” McDermott says, adding that Borro has no intention of getting into other types of lending. “We complement each other. We don’t compete.”

PledgeCap also focuses exclusively on asset-based lending. The company typically funds loans between $1,000 and $5 million. The length of each loan is four months. Customers don’t have to pay every month, though most do. For every month the loan is outstanding customers pay a rate of 3 percent on average. Other fees, payable at the end of the loan, are assessed based on costs PledgeCap incurs and depend on factors such as the cost of insurance, the appraisal fee and the cost of transporting the item to the secure facility.

PledgeCap also focuses exclusively on asset-based lending. The company typically funds loans between $1,000 and $5 million. The length of each loan is four months. Customers don’t have to pay every month, though most do. For every month the loan is outstanding customers pay a rate of 3 percent on average. Other fees, payable at the end of the loan, are assessed based on costs PledgeCap incurs and depend on factors such as the cost of insurance, the appraisal fee and the cost of transporting the item to the secure facility.

By contrast, Kalamata Capital, which has been in business since 2013, offers asset-backed loans in connection with several other small business financing options—such as working capital loans, SBA loans, lines of credit, merchant cash advance and invoice factoring—to give customers more flexibility in terms of rates.

In Kalamata’s case, it will evaluate the cash flow and other assets of a small business for financing options. Kalamata then combines both the amount it would lend against an asset and the amount it would lend to the small business, possibly giving the business a lower rate—and more options—in the process.

While it’s not a type of funding that works for everyone, Mandis, the chairman of Kalamata, expects to see continued growth in this area. “I don’t think the loan market for luxury assets is as large as many of the traditional small business finance areas, but it is something that can be helpful to small business owners,” he says.

World Business Lenders Rings in 2016

December 18, 2015On December 8th, World Business Lenders (WBL) wrapped up 2015 and prepared for the coming new year at their annual shareholder meeting hosted at the Waldorf Astoria in New York City. The event, which was mostly restricted to company employees, referral partners and shareholders, featured some out-of-town guest speakers including BFS Capital CEO Marc Glazer and RapidAdvance Chairman Jeremy Brown.

On a panel moderated by WBL Managing Director Alex Gemici, Brown and Glazer expressed their optimism for the industry’s future, but to some extent heeded caution. Brown specifically made reference to his prediction of a bursting bubble but conceded that he might have been off by a year or two. Glazer reminded the audience that both executives had weathered the financial crisis so that they had witnessed firsthand how a recession can affect their businesses, and made them stronger because of it.

WBL CEO Doug Naidus made a similar admission in his presentation, in that he thought that the bubble of unsecured lending would burst in 2015 but that it hadn’t happened yet. Still, he thinks it’s right around the corner. One of their primary hedges against a correction is that they secure their loans against real estate. Naidus has a background in mortgage lending so it’s a market they’re familiar with.

Another one of their key strategies is the franchise model. Over the last two years, WBL has acquired commercial finance brokerages and converted them into originating houses for their collateralized loan program. It has had a really positive impact on their growth and on their margins, according to information disclosed at the event. It’s expected that they will continue to pursue more acquisitions.

The sentiment of the event was rather festive and optimistic, with WBL enjoying a positive trajectory of growth and success.

The Broker’s Future Part Two

December 16, 2015THE ROBOTS ARE COMING

Merriam-Webster and Dictionary.com both agree, that a “robot” is a machine that is created to do the work of a person, carrying out a complex series of actions automatically, all controlled by a computer. Sometimes a robot can resemble a human being in likeness, but often times a robot is simply a piece of software, a piece of hardware, a piece of machinery, or a cloud based infrastructure called the internet (online networks). Professor Kaku is a futurist from City College of New York, a futurist is someone who makes what one would consider “fairly accurate” predictions about what the future holds and how these future events might emerge from present day events. Professor Kaku believes the following:

Merriam-Webster and Dictionary.com both agree, that a “robot” is a machine that is created to do the work of a person, carrying out a complex series of actions automatically, all controlled by a computer. Sometimes a robot can resemble a human being in likeness, but often times a robot is simply a piece of software, a piece of hardware, a piece of machinery, or a cloud based infrastructure called the internet (online networks). Professor Kaku is a futurist from City College of New York, a futurist is someone who makes what one would consider “fairly accurate” predictions about what the future holds and how these future events might emerge from present day events. Professor Kaku believes the following:

The job market of the future will consist of those jobs that robots cannot perform. Our blue-collar work is pattern recognition, making sense of what you see. Gardeners will still have jobs because every garden is different. The same goes for construction workers. The losers are white-collar workers, low-level accountants, brokers, and agents.

A RECAP OF PART ONE

Back in June 2015, I did an article for AltFinanceDaily about the Broker’s Future, speculating if the good times were indeed over for the brokers as it pertains to their level of profitability and survivability going forward.

- I examined the 2000 – 2007 and 2008 – 2013 time periods, speculating that the “Era of the Broker” was indeed between the 2000 – 2013 period.

- Then, I examined the current time period which begins around the middle of 2014, that is seeing so much of a mass new entrance of brokers into the space, that AltFinanceDaily had to compose a cover story on the phenomenon for the March/April edition of AltFinanceDaily Magazine. The only issue with this current time period is that, in my sole objective opinion, we are in the “Era of the Strategic Networks”, and no longer in the “Era of the Broker.”

- I concluded the article in June with the following: those just now trying to come in and ride the wave will soon discover that just like with the Stock Market, the real money has already been made and most of the future returns are already capitalized.

AN INTRODUCTION TO PART TWO

My analysis shows that the current time period is all about Strategic Networks, which are mainly three networks to be exact, which include the following, all designed to produce competitive market advantages, positioning, strategies, qualified leads, etc:

- The Center Of Influence Network: this includes entities such as banks, credit unions, processors, accountants, VCs, credit bureaus, etc., that allow access to exclusive leads, exclusive data, equity financing, debt financing, mergers, etc.

- The Mom and Pop Network of random independent agents across the country who resell on a 100% commission basis, providing free marketing in a way that collectively they produce a significant amount of volume (even though individually most of the agents cannot make a living from this activity).

- The Online Network with exclusivity on the growing online marketplace of merchants seeking financing, education and options via the internet.

For Part Two Of The Broker’s Future, I want to focus in on The Online Network, which in my opinion will be one of the main destroyers of opportunities in our space for the majority of brokers going forward.

DEATH OF A B2B SALESMAN

For about $499, you can read a very comprehensive report from Forrester on the death of B2B salespeople. Forrester predicts that by 2020, over 1 million B2B salespeople will lose their jobs to the growing force of IT/Robotics, which includes various forms of technology, automation and of course the internet in general through E-commerce.

In relation to our industry of merchant services, merchant cash advance and alternative business loans, I don’t believe that we have to wait until 2020 to see significant changes, I believe these changes are already in full effect and the major players within our space are the ones that are truly capitalizing on The Online Network, giving them major exclusivity on the growing online marketplace of merchants seeking financing, education and options via the internet.

MERCHANT SERVICES HAS BEEN AFFECTED

The Online Network phenomenon has totally destroyed the feet on the street MLS (merchant level salespeople) over on the merchant services side. Before the rise of the Online Network, MLS were valuable to merchants as information on merchant processing, interchange, how the bankcard transactional process worked, etc., were not readily available and most banks did not handle direct sales of the service. So the MLS would park their car down the street, randomly walk into merchant locations, and provide the education via brochures, terminal samples, etc.

They would explain how the merchant processing process works, how accepting credit cards could boost sales through more impulse purchases and consumer convenience, and more. The MLS would then go over the different options of payment processing technology, commit the merchant to a 24 – 48 month lease of the technology, and make his/her commission off the leasing sales and eventually also off the residuals. However, the rise of the Online Network completely shattered this business model:

- The Online Network now allows the merchant to comprehend merchant services on his own, without the help of the MLS, by researching interchange and conducting his own “rate analysis”. The merchant can also now see the true cost of the processing equipment, thus to no longer sign up for leases for $100 a month for 24 months ($2,400) for a $350 terminal at best.

As a result, the MLS can no longer prospect on “rate savings” nor prospect based on the equipment such as through leases or even through free terminals anymore, due to the merchant’s knowledge that the terminal is worth $350 at best. As a result, the direct sales of merchant services has become a value-add to other services, requiring yesterday’s MLS to transform into something totally different such as a financing or payroll specialist, trying to convert merchant accounts over on the side, as part of the sale.

ALTERNATIVE LENDING HAS BEEN AFFECTED

The merchant cash advance and alternative business loan products are more popular today than they have ever been before, due mainly to the massive media attention that they have received with companies going public, CEOs landing interviews on major media outlets, talking heads debating the products across a number of media mediums, and more. 7 – 15 years ago (2000 – 2008), if you were to look up a product online called “merchant cash advance”, you would not have produced many search results. As a result, to inform and educate the merchant on the product, you needed an actual human being (a broker) to sit down and explain the nuances of said services referred to as “split funding”, “revenue purchases”, and “holdback percentages.”

Compare this to today, where a simple search for “merchant cash advances” gives you pages upon pages of articles, promotional ads that follow you across the internet, company websites, press releases, and more. The merchant can easily learn about the merchant cash advance as well as other new forms of alternative financing by going online and scrolling through the vast amount of information. They can educate themselves on the products, companies, and payback procedures. They can fill out a form and get 10 quotes from 10 companies within a couple of hours and in a lot of cases, receive funding from one of the companies by the next business day. The phenomenon is so big that companies in our space are now just referred to as “Online Lenders,” totally shunning the fact that many operate with traditional brick and mortar locations and still employ brokers to still resell the products like they did “in the old days”.

THE FUTURE

Based on my sole objective analysis, The Future is going to be all about the three networks of Strategic Partnerships, which includes The Online Network. Without a shadow of a doubt, those that control these networks will be the major players going forward, as they will have the leveraged resources, knowledge, experience, financing, and connections that the newer market entrants just do not have.

The 80/20 dynamic will continue, where 20% of the players produce 80% (or more) of the production, and the other 80% of the players will fight over the remaining 20% (or less) of the production, which just will not be enough to sustain profitability going forward.

As fast as these new entrants rush in, will be as fast as they burn out. Burning through their savings and retirement funds, and/or running up the utilization rate on their credit cards, trying to take advantage of a “market opportunity” that they “heard about”, but is pretty much already capitalized on, by those who have been here long before they came on the scene.