Chicago Resumes Call for Protection of Small Business Owners Against Predatory Lenders

February 12, 2016 Chicago City Treasurer Kurt Summers has picked up where Rahm Emanuel left off a year ago. During a January 25th Illinois Senate Financial Institutions Committee hearing named, Small Businesses, lack of access to capital, and predatory lending practices, Summers called for new legislation to protect small business owners from misleading and dishonest predatory lenders.

Chicago City Treasurer Kurt Summers has picked up where Rahm Emanuel left off a year ago. During a January 25th Illinois Senate Financial Institutions Committee hearing named, Small Businesses, lack of access to capital, and predatory lending practices, Summers called for new legislation to protect small business owners from misleading and dishonest predatory lenders.

OnDeck we mean you

Spencer M. Cowan, Senior Vice President for Research, Woodstock Institute, also testified during the hearing and referenced OnDeck specifically. “The terms do not, without calculations that few people can make, let the borrower know that the loan will take a full year to repay with an effective interest rate of just under 70 percent,” he said. Cowan’s position was that banks need to lend more so that small businesses don’t need such alternatives. “If businesses do not have access to loans from banks, then they are probably going to resort to the same types of strategies as consumers who can’t get small loans from banks,” he said.

Cowan cited a report he prepared 18 months ago that examined the relationship between banks and the racial makeup of the small business owners they lend to. The sources he cited about alternative lending were blog posts written by industry critic Ami Kassar.

Treasurer Summers meanwhile recommended the following measures be included in draft legislation to protect small business owners:

- Require loan terms to be clear and unequivocal. Loan terms should be clearly stated using straightforward language and the interest rate should be clearly disclosed as an annualized interest rate or an annual percentage rate (APR).

- Loans should be free from traps. Borrowers should not be hit with new fees on existing principal if they refinance or modify a loan. Borrowers should not be charged interest or periodic costs for the remaining period of the loan if they pay it off early.

- Lenders should be required to display information about the results of their previous loans. This information could be anonymous and in the aggregate, but would give borrowers important data points as they determine whether or not to use a particular lender. If borrowers are able to see that a lender has a pattern of providing loans that are not paid back or have caused businesses to fail, they will be more likely to choose a more reputable lender.

- Conflicts of interest should be disclosed to borrowers. Borrowers should know what types of incentives are driving the lender and whether the broker will receive higher fees for using certain lenders or types of loans.

- Because many of these loans are made online, lenders must take substantial steps to protect the data privacy of loan applicants. Borrower data should not be allowed to be sent to third parties without the written consent of the borrower and lenders should be required to take steps to ensure that the data is encrypted and protected from breaches.

Unsurprisingly, the Illinois Bankers Association (IBA), who was not even invited to the hearing, felt compelled to issue a public statement. In a letter addressed to Chairperson Jacqueline Collins, the IBA was rather protective of their own interests. “We share the Committee’s concern with the proliferation of these under-regulated lenders, sometimes known as ‘fintech’ companies,” they stated. “This relatively new ‘shadow banking’ industry — unlike traditional financial institutions — is in many respects unregulated. Consequently, some bad actors are engaging in predatory lending practices with repayment terms that too often are forcing small business customers into cycles of debt.”

However they tapered down the rhetoric and made a technology-forward plea. “We do think it is important for lawmakers to preserve the benefits of lending innovations, and to ensure that mainstream financial institutions are not prevented from adopting technologies that result in better customer service,” they said. “For example, mobile lending interfaces and faster loan approvals, with appropriate safeguards, provide many potential benefits and match changing customer needs and expectations. We should seek to preserve these innovative solutions that benefit entrepreneurs and small businesses, while at the same time curbing abusive lending practices.”

A public digital transcript of the hearing is not currently available.

The Ghost of Second Source Funding Has Lost a Desperate Court Battle

February 4, 2016The notorious company returned from the dead for one last final stand

For many veterans of the merchant cash advance business, the Second Source Funding name is something they’d rather forget. They were perhaps the largest funding ISO in the industry between 2006 and 2008. And as plenty of ex-employees will tell you, the story ends badly.

For many veterans of the merchant cash advance business, the Second Source Funding name is something they’d rather forget. They were perhaps the largest funding ISO in the industry between 2006 and 2008. And as plenty of ex-employees will tell you, the story ends badly.

Meir Hurwitz, a co-founder of NY based Pearl Capital, immortalized the Second Source years through a Bloomberg exposé about how his own company rose and sold for $40 million. In his tale, he claimed that Second Source founder Sam Chanin still owed him $2 million for the work he performed there. For Hurwitz, the falling out set the stage for the company he would go on to start. For other employees, it was the beginning of a grudge that would stick around for almost a decade.

Chanin has gone so far as to admit on his blog that he became known as “the guy who ripped them off and didn’t pay their residuals.” According to him, it wasn’t his fault. Court records do show Second Source Funding filing a complaint against Cynergy Data back in 2009 for $60 million in damages. Cynergy was the processor behind their lucrative merchant services operation and ultimately where the residuals they paid out to sales agents originated from. The case was dismissed in October of that year because Cynergy declared bankruptcy.

Effectively shuttered by the circumstances, the only reminder of what had once been, was another lawsuit filed by Second Source in September 2012 against a company (and more than 30 co-defendants) that acquired Cynergy Data’s assets. In October of 2009, Cynergy’s assets were reportedly sold to The Comvest Group for $81 million. In the complaint, Second Source sought at least $50 million from them in damages.

It has been approximately seven years since Second Source’s days ended, sources estimate. Users on industry forums were already speaking of the company in the past tense as far back as early 2009. The Second Source website no longer even exists. While ex-employees have long urged old peers to move on from those days, others have been forced to confront their demons.

THE GHOST OF MERCHANT CASH ADVANCE PAST

THE GHOST OF MERCHANT CASH ADVANCE PAST

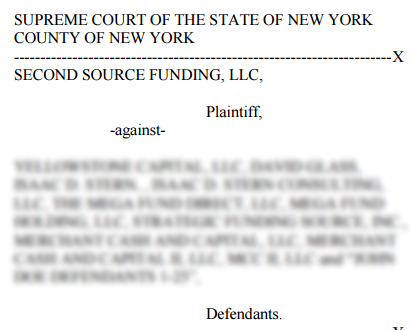

In September of 2014, the very same Second Source Funding emerged through a complaint filed in the Supreme Court of New York against Yellowstone Capital, LLC, 8 named co-defendants and 25 John Doe defendants. Seeking damages in the astounding amount of $360 million, Second Source alleged that Yellowstone’s co-founders stole their “revolutionary business model” of which they describe as using “Independent Sales Offices to leverage economies of scale in marketing and selling a bundle of financial services, including credit card processing and cash advances.” As a result of that and other claims, they were allegedly the reason for “Plaintiff SSF going out of business.”

The ensuing battle was probably one of the most contentious litigations the industry has ever experienced, at least from what can be seen on the docket. In one publicly filed exhibit introduced by Yellowstone, was the draft of a complaint that the plaintiffs had allegedly sent them that named more than 40 defendants. It reads like a yearbook of the merchant cash advance industry in 2009.

Other exhibits are packed with plenty of Second Source era nostalgia, including copies of the entrance exams given to new hires. One test question embodies the culture of the time, when it asked applicants:

What movie is this quote from, “Put the coffee down, coffee is for closers?”

While motions and cross motions at times appear to venture into the arena of insanity, especially considering Second Source went out of business a long time ago, AltFinanceDaily has learned that Yellowstone was vindicated this week in a decision that dismissed all the claims with prejudice. That means they can’t have a do-over. The suit lasted 17 months.

AltFinanceDaily has been quietly following the docket for over a year. We did not ask either party to comment on the decision for the reason being that Second Source may be considering an appeal, or at least they alluded to that in the court transcripts.

In the meantime, the ghost of Second Source reminded a few people in the merchant cash advance industry that the antics of 2006-2008 were more than just tall tales told by grey beard Wall Street guys. Back then the coffee was still for closers only. And back then, the game was so different that some people would still be feeling the effects of it a decade later.

In the meantime, the ghost of Second Source reminded a few people in the merchant cash advance industry that the antics of 2006-2008 were more than just tall tales told by grey beard Wall Street guys. Back then the coffee was still for closers only. And back then, the game was so different that some people would still be feeling the effects of it a decade later.

THEN AND NOW

Yellowstone Capital was one of the first merchant cash advance companies to experiment with the ACH payment method. Today, they originate nearly a half billion dollars a year in funded deals.

If you want to see just how much has changed since the Second Source days, check out this answer to the Second Source exam in 2008.

Q: If a merchant is getting an advance from MCA and can’t switch processors, what can the agent offer this merchant?

A: Lock box

It’s amazing to think that ACH was inconceivable at the time. Touched by ghosts indeed…

Industry Trade Group Coming of Age: The SBFA is Becoming More Political

February 1, 2016By hiring an executive director, the Small Business Finance Association hopes to achieve at least two goals – taking a step toward becoming a full-service trade group and providing a public voice for the alternative finance industry.

Stephen Denis, formerly deputy staff director of the U.S. House Committee on Small Business, went to work in the new role in mid-December, setting up shop with his cell phone and laptop in a Washington, DC, area coffee emporium. He’s the SBFA’s first full-time employee.

Hiring Denis, who also has association experience, represents “the next evolution” of the trade group, according to David Goldin, SBFA president and Capify’s founder, president and CEO.

The SBFA, which got its start in 2008 as the North American Merchant Advance Association, changed its name last year because members have added small-business loans to the their merchant cash advance offerings. Although the trade group’s not exactly new, it has plenty of room to grow and its leadership and members seem open to change.

The SBFA, which got its start in 2008 as the North American Merchant Advance Association, changed its name last year because members have added small-business loans to the their merchant cash advance offerings. Although the trade group’s not exactly new, it has plenty of room to grow and its leadership and members seem open to change.

“The goal is to start from scratch and take a look at everything the association is doing,” Denis told AltFinanceDaily, “and to really build this out to a robust group that represents the interests of small businesses.”

Denis appears optimistic about pursuing that goal. He’s a native of the Boston area and a Harvard University graduate whose first job out of school was as an aide to Republican Sen. John E. Sununu of New Hampshire. After three years in that position, he took a job for two years with a UK-based trade association, traveling frequently to London to inform the group of Congressional action in the United States.

From there, Denis went on to become director of government affairs and economic development for the Cincinnati Business Committee, a regional association that included Fortune 500 companies among its members. After two years in that role, Denis joined the staff of Rep. Steve Chabot, R-Ohio, moving back to Washington and serving as the congressman’s deputy chief of staff during a five-year stint that ended when he joined the SBFA.

While working for Chabot, Denis also became deputy staff director of the House Committee for Small Business, the No. 2 position there, and he has held that job for the last three years. The committee’s tasks include learning as much as they can about small business, including financing, and using the information to advise members of the House on policy initiatives.

The experience Denis has amassed in government should serve the association well because his duties include briefing federal legislators and regulators on how the alternative-finance business works. With Denis as spokesperson, the industry can speak to government with a single voice, Goldin asserted.

“We are going to be aggressive in our outreach to legislators and regulators as well as be active reaching out to local, state governments,” Denis said. The SBFA will “work with other trade groups and small business groups to promote our mission to ensure small businesses have alternative finance options available to them.”

Until now, too many players from the alternative finance industry have been vying for lawmakers’ attention, Goldin said. To make matters worse, some of those seeking to influence government in hearings on Capitol Hill are brokers instead of lenders and thus may not have a perfect understanding of risk and other aspects of the business, he maintained.

“We’re hearing that there are people trying to be the voice of small-business finance that either don’t have a lot of years of experience or they’re not telling the whole story,” Goldin said. “We want to make sure the industry’s represented properly.”

Denis can draw attention away from the “noise” created by unqualified voices and focus on information that Congress needs to make reasonable decisions about the alternative finance business, Goldin maintained.

Besides getting the word out in Washington, the SBFA hopes to convey its message to the general public on “the benefits of alternative financing,” Goldin said. At the same time the group can help make small business owners aware of the finance options, Denis added.

Asked whether hiring Denis marks the beginning of an effort to lobby members of Congress for legislation the association deems favorable to the industry, Goldin said only that additional announcements will be forthcoming.

Asked whether hiring Denis marks the beginning of an effort to lobby members of Congress for legislation the association deems favorable to the industry, Goldin said only that additional announcements will be forthcoming.

Meanwhile, updated “best practices” guidelines might be in the offing to help industry players navigate the business ethically and efficiently, Goldin said. A set of six best practices the association released in 2011 included clear disclosure of fees, clear disclosure of recourse, sensitivity to a merchants’ cash flow, making sure advances aren’t presented as loans and paying off outstanding balances on previous advances.

Addressing other possible steps in the association’s growth, Goldin said the group doesn’t plan to publish an industry trade magazine or newsletter. However, a trade show or conference might make sense, he noted.

Denis said he and the board had not discussed the possibility of a test, credential or accreditation to certify the expertise of qualified members of the industry. However, associations often establish and monitor such standards, so it would be reasonable for the SBFA to do so, he added.

The association might establish a Washington office, Goldin said. “We’ll look to Steve for his thoughts and guidance on that,” he observed. Denis seems amenable to the idea. “Down the road, we would love to open an office and hire more people,” he said.

In Goldin’s view, all of those moves might help the rest of the world comprehend the industry. Understanding the industry requires taking into account the cost of dealing with risk and business operations, he said.

Placing a $20,000 merchant cash advance, for example, requires a customer-acquisition effort that costs about $3,000 and a write-off of losses and overhead of about $4,000, Goldin said. That’s a total of $27,000 even without the cost of capital, he maintained.

“Most people don’t understand the economics of our business,” Goldin continued. The majority of placements are for less than $25,000, he said, characterizing them as “almost a loss leader when you factor in the acquisition costs.”

While spreading that type of information on the industry’s inner workings, Denis will also conduct the day-to-day for the not-for-profit’s affairs. The association’s board of directors will continue to set policy and objectives.

Members elect the board members to two-year terms. Current board members are Goldin; Jeremy Brown of Rapid Advance, who’s also serving as the group’s vice president; John D’Amico, GRP Funding; Stephen Sheinbaum, Bizfi; and John Snead, Merchants Capital Access.

Member companies include Bizfi, BFS Capital, Capify, Credibly, Elevate Funding, Fora Financial, GRP Funding, Merchant Capital Source, Merchants Capital Access (MCA), Nextwave Funding, NLYH Group LLC, North American Bancard, Principis Capital, Rapid Advance, Strategic Funding Source and Swift Capital.

Companies pay $3,000 in monthly dues, which Denis characterizes as inexpensive for a DC-based trade association.

Membership could spread to other types of businesses, Denis said. “I’d like to expand the tent to other industries,” he noted. “The association is trying to represent the interests of small business and make sure they have every finance option available to them.”

But a key purpose of the trade association is to provide a forum for members to come together as an industry, Denis said. “We’re thinking big,” he admitted. “We hope that all members of the marketplace will want to become a part of it.”

Should Funders Pay Lifetime Renewals?

January 24, 2016OPINIONS ARE LIKE A-HOLES RIGHT?

We all know what they say about “opinions” right? They (opinions) are basically like a-holes and everybody has one. I’ve stated a lot of opinions here on AltFinanceDaily over the last couple of months, while some might agree and others disagree, I always try to provide educated opinions to separate commentary from the generic pack of people blurting out comments across industry forums and media publications that might not have firsthand experience on the front lines.

With that being said, it’s in my sole opinion that every funder/lender should offer their independent brokers lifetime renewal compensation despite new deal volume.

BROKER AGREEMENTS SEEM TO CHANGE ON A WHIM

BROKER AGREEMENTS SEEM TO CHANGE ON A WHIM

I’ve been reselling the merchant cash advance and alternative business loan products since November 2009, however, the current program structures/agreements of my funders and lenders look totally different today than they did in the beginning.

It’s almost as if a new agreement is created every 12 – 18 months with similar conditions, but certain terms might have changed, including the compensation of renewals.

Some funders and lenders will start without any provisions related to renewals, basically as long as the client continues to renew, then you will be allowed to collect commissions off the client. But later on down the line, some funders and lenders will change provisions and require certain levels of new deal volume in order to be compensated on renewals going forward. Most broker agreements have terminology listed that states that the funder/lender can change the program at their discretion, however, I believe that at no point in time (other than for particular circumstances of fraud or ethics violations) should a funder take away a broker’s renewal compensation as whatever “good” it’s supposed to be doing (which I still can’t think of any), I believe it does far more damage in return.

YOU CAN’T CLOSE WHAT YOU CAN’T GET APPROVED

Sometimes a broker doesn’t fund a deal within 3 – 12 months because the funder can’t approve any of the submitted deals. If the broker is like myself, I’m going to pre-screen all new applications to see if it fits the underwriting criteria before submitting it, as submitting applications that are outside the criteria does nothing but waste valuable underwriting resources. If they are a somewhat conservative funder, a lot of times a broker just might get too few applicants to fit the box.

WHAT DID YOU ACTUALLY SPEND ON MARKETING?

Funders and lenders receive free marketing from brokers because they bring them the deals, so what is the big deal about continuing to pay renewal compensation despite new deal volume? They don’t have to worry about taking the risk of putting marketing capital up on the table with a potential of no return. The person who puts up the capital is the broker, and they should be compensated for the lifetime of the client regardless of new deal volume.

As an independent broker, the individual is a part of the Mom and Pop Network, which is just a group of random brokers who resell for free (100% commission). Not only are funders/lenders receiving the free marketing from the resellers, but they are also receiving free data to utilize in any potential “big data” valuations for sell-off, or “big data” analysis for better market segmentation. In addition, if the broker’s portfolio of merchants (even if it’s just one merchant) didn’t default or the default rate is very low, what is the justification for cutting off the broker just because there was no new deal funded?

RENEWALS ARE THE LIFEBLOOD OF THE BROKER’S INCOME

Once upon a time, during the very early days of MCA, the product was pretty much a one-off project. A merchant had an emergency, they sold off a percentage of their future credit card receivables in exchange for some upfront cash today, and used the cash to address whatever emergency they were facing. If the merchant renewed, it was usually one time (twice if you were lucky) and that was it. Today, it’s a different situation if you set up your merchant based on their proper Paper Grade. Merchants are renewing back-to-back, a lot of times for 3 to 5 years (or more) in a row, which means that the product is becoming more of an integrated portion of their business (similar to the MCA’s Kin A/R Factoring) rather than a one-off occurrence. This means for a broker, there’s a lot of money to be made off of their MCA portfolio going forward and the entire point is to build your portfolio up to a particular size, where you can just “sit back” and solely manage the renewals of the portfolio without being required to continually produce new deals by spending more on marketing.

Take a broker with a portfolio of 25 merchants who renew just about every 6 months (twice a year) with an average funding of $75,000 with 5 points commission per deal. That alone is $3.75 million a year in funding volume and almost $100,000 per year in income, solely off the renewal portfolio. If the broker maintains this portfolio for 10 years in a row, that’s almost $38 million in funding volume and close to $1 million in income. Why on Earth would you want to even threaten to cancel a broker out of the deal when again, it was their ingenuity, rapport building skills and sales skills that are the foundation of the clients coming to the funder to begin with, as well as continuing to renew back-to-back?

YOU ARE ASKING FOR YOUR MERCHANTS TO BE FLIPPED OR STACKED

The broker is the one who has the original relationship with the merchant, thus, the merchant more than likely has more rapport with the broker than they have with anyone in the funder’s organization. Thus, cutting off the broker from the renewal compensation might do nothing but just cause the merchant(s) to be stacked or flipped to another funder/lender.

TELL ME WHICH BROKER IS MORE VALUABLE? BROKER A OR BROKER B?

Okay, so tell me which Broker is more valuable? Is it Broker A or Broker B?

– Broker A: Over the course of one year, Broker A brings in 15 new merchants, with only 4 of those merchants renewing once because the broker didn’t price the merchants in their proper Paper Grade and thus, a competitor stole them away at renewal. This produces a total of 19 advances (new/renewal) and let’s say with the average funding being $50,000 you are looking at volume of $950,000.

– Broker B: Over the course of one year, Broker B brings you only 8 new merchants, but 3 of them renew 4 times back-to-back (12 additional advances), 2 of them renew 3 times back-to-back (6 additional advances), 2 of them renew 2 times back-to-back (4 additional advances), and 1 of them renew only once, for a total of 31 advances (new/renewal). Keeping the average funding at $50,000 you are looking at volume of $1,550,000.

Broker B supplied fewer new deals than Broker A, but Broker B provided an overall higher level of production based on the rapport and proper structure they established with their clients that produced more renewals and advances in total for the funder. Seeing as though in our industry, when funders count their “total volume funded” they include both new and renewal volumes, how can it be that Broker B is not more valuable to a funder than Broker A is? Not saying that Broker A isn’t valuable, but based on potentially cutting off renewal compensation due to a lower amount of new deal volume, they would potentially be cutting off the Broker that offers more value over time.

THE FINAL WORD

Why on Earth would a funder or lender want to kick out a competent broker by cutting off their renewal portfolio? What does it solve to cut off a competent broker, with a low (or no) default rate, just because they didn’t bring in newly funded deals during the previous 3 – 12 months? What does that solve? Does cutting them off somehow produce more margin for the funders? More market share? Savings in some sort of area? As mentioned, the broker is likely to flip the merchants or stack the merchants when this happens, which again, does nothing for the funder in terms of providing any type of benefits or value.

The only justification for cutting off a broker is when they are engaged in unscrupulous acts. But cutting off competent brokers just because they didn’t fulfill some insane new deal volume policy, makes absolutely no sense because at the end of the day, cutting off the brokers will be like cutting off the funder’s relationship with the merchants as well. With the parade of new funders looking to grab market share, what better way to gain it than to partner with competent but dejected brokers, who just got their renewal compensation cut off for not fulfilling some insane new deal policy?

To Syndicate or Not to Syndicate?

January 20, 2016 Someone once asked the question of, “To love or not to love?” But I believe soon every broker will have to ask the question of, “To participate or not to participate?” Is it time we all get into the game?

Someone once asked the question of, “To love or not to love?” But I believe soon every broker will have to ask the question of, “To participate or not to participate?” Is it time we all get into the game?

THE YEAR OF THE BROKER OR THE YEAR OF ROSY PROMISES?

AltFinanceDaily writers such as Sean Murray, Ed McKinley and myself, referred to 2015 as the Year of The Broker, as a stream of new brokers continued to rush into our space to take advantage of the perceived opportunities.

THE YEAR OF PARTICIPATION?

For experienced brokers, I’ve written two pieces so far here on AltFinanceDaily in relation to the broker’s future. I’ve talked about how I believe the future of our industry will be dominated by Strategic Networks and those who utilize these networks efficiently will not just be the dominant players going forward, but they will be pretty much the only “real” players going forward. I also talked about how success in our industry is based mainly on leveraged resources and networks, rather than having some sort of “superior” selling capability.

But with that being said, I wanted to use this article as a way to add to this discussion of the future by outlining my recommendation that experienced brokers “get into the game” when it comes to syndication and deal participation. DeBanked reported back in April of 2015 about how Strategic Funding Source’s syndication network of over 200 partners (at the time) invested over $260 million of their own capital into funded deals. This level of investment, according to the reporting, helped amass significant wealth for the 200 syndication partners that participated. If 2015 was the Year of The Broker, could 2016 be the Year of Participation?

IT’S NOT THE SAME ANYMORE

It’s no longer 2000 – 2013, when quite frankly a broker could amass great income by just strategically utilizing the Uniform Commercial Code (UCC) as a marketing model. But pretty soon the word got out and everybody rushed in to duplicate the methodology. What was once a great idea became a complete waste of marketing dollars.

UCCs are so bad today, that when you call a merchant and just mention the fact that you are from a funding company, they immediately hang up the telephone. Sometimes, I would call and before I would even have the chance to say a word, the staff member on the telephone would ask, “Are you calling about a cash advance?” Once I would reluctantly answer in the affirmative, they would of course immediately inform me to put them on the do not call list, never call again, and either in nice language or a language full of swearing, they would inform me that they aren’t interested and how I’m the 19th guy that has called them this week. This is the result of a merchant getting 20 calls a week from 20 different companies, about 20 different merchant cash advance products.

As a result, brokers are going to have to specialize in the Strategic Networks and leveraged resources that I have been discussing for nearly a year now on AltFinanceDaily. We will also have to juggle the rising marketing costs and increasing pressures on pricing as our industry goes more mainstream. You might not want to operate as a full-fledged direct funder, as I understand that the investment outlay for such a task is significant. But I believe going forward, you aren’t going to be able to “make it” like you used to by solely relying on commissions from brokering deals. You are going to have to get into the game and put some money in deals not just to sustain the amount of income you were making in commissions historically, but to potentially make more money than you ever made before.

A SHOUT OUT TO WBL

Also back in April of 2015, there was a pretty popular online discussion that discussed World Business Lenders’ (WBL) new ISO/Broker acquisition program. I had a conversation by telephone with Lenny Steigman from WBL on April 21st of last year to discuss the program in detail.

One of the things that Lenny mentioned on that call was the notion of the broker’s office requiring a shift in structure in order to survive in the upcoming future. Lenny discussed that brokers who chose to continue to operate on the sidelines relying solely on commissions from brokering deals, without getting involved in some sort of equity or syndication participation, might find the future of their involvement in our space limited as continued growth through strategic networks drive the progression of the industry. I could not agree more with Lenny Steigman. It’s certainly time for a shift and one of those shifts I believe will require more experienced brokers to become syndication partners through putting up a portion of the capital to fund the merchants that they service.

GET YOUR DUCKS IN ORDER

As you prepare for this shift and look to get into the game, make sure that you have your ducks in order:

Legal Representation: This is important, you need an attorney to review your syndication agreements as well as review the legal structure of the funder you are partnering with, to make sure that all of the legal terminologies are outlined properly.

Understand The Deals You Are Funding: Know the type of client you are funding, such as if they are A Paper, B Paper, C Paper, D Paper or E Paper. Your level of risk on the deal in terms of default increases when you get into the higher risk paper grades, thus, make sure you are getting a significant enough “return” on said deals to accommodate the risk you are tolerating.

Examine Your Funder’s Finances: By syndicating, you are doing more than just investing in the merchants that you serve, you are also investing in the financial soundness of the funder you are syndicating with. Make sure your funder is not on the verge of bankruptcy, profitable, and will actually be around a year from now.

Examine Your Funder’s Operational Structure: I’ve talked about the importance of making sure you vet who you partner with in relation to being a broker. Now that you are syndicating, you most definitely make sure you are dealing with a funder that’s “proven.” The funder should have at least 2 years in business, have funded in the eight digits in terms of volume, have a proven and profitable underwriting formula, have an office full of employees, not have a significant amount of bad reviews, be in good standing with the BBB, having an actual online presence, and they should be running a professional and competent organization overall.

Round Up Your Capital: The secret of many of the wealthy has always been their unique ability to utilize the money of other people for their business investments. They find equity investors seeking a return on their capital, invest said capital with a high return and collect a management fee off of the transaction. Or, they borrow money from a creditor at a particular interest rate, invest the monies for a higher rate of return, then pay off the loan with interest and pocket the profits. Whichever way you prefer, how about you utilize OPM (other people’s money) to your advantage (leverage) as well for your participation efforts?

TO PARTICIPATE OR NOT TO PARTICIPATE?

I believe we might be entering the year of participation, which means it’s time for the experienced brokers to join in on the strategic networks which will dominate our space going forward. New entrants who don’t know the space and still can’t spell “merchant cash advance” will be in for a bumpy ride going forward, but those with the experience, it’s time to add to your industry influence by coming off of the sidelines as brokers solely, and becoming broker/syndicates in the truest form.

Me-Too Lenders Reject The Opportunity to be Unique

January 15, 2016 IMITATION IS THE BEST FORM OF FLATTERY

IMITATION IS THE BEST FORM OF FLATTERY

You know they say that the imitation is the best form of flattery, the only problem is that flattery is insincere praise, or praise only given to further one’s own selfish interests.

Surely new funders and lenders in our space are looking to further their own selfish interests by stealing away market share from existing players, which is perfectly fine seeing as though we operate in a free market society. However, what doesn’t make sense to me is thinking that you can steal away a competitor’s clientele by looking, sounding, and behaving exactly like he does.

THEY ALL SOUND THE SAME

I have no idea how many direct funders are present in our space today, but from what I’ve heard it’s well into the hundreds, and I receive recruiting emails along with invites on LinkedIn from these new players all of the time. What’s strange about just about all of these new players is that they all sound, specialize in, and operate the same as my current funders, leaving me scratching my head wondering why in the hell should I bring my volume over to you, if you do nothing different? I can hear them now:

– “John, we can consolidate your merchant’s balances as long as they net 50%!” (This isn’t anything new, the 50% net rule has been around for 17 years.)

– “John, we can approve some of your merchants for as low as a 1.12!” (This isn’t anything new, A+ and A Paper merchants have been receiving proper risk based pricing for years now.)

– “John, you will receive a dedicated account manager!” (This isn’t anything new, funders and lenders have been providing their broker houses with dedicated ISO Managers for around 17 years.)

– “John, we can fund just about every deal if the deal makes sense!” (This could be a new concept, the problem is that I have heard this before, only to submit a “restricted industry” merchant and it be declined just like it’s declined everywhere else.)

– “John, we fund deals as small as $5,000 to as high as $5 million!” (This isn’t anything new, this has been the standard funding range for years now. Plus, it’s rare that a broker in our space would get a merchant that needs $5 million, as those merchants would usually rely on the traditional lending system.)

– “John, we get deals done fast!” (Everybody says this, the reality is that unless a lender has automated the majority of their closing process as well as eliminated many portions of said closing process, then that means they are still doing a good chunk of it “manually”, which means it will always take 2 – 10 business days to complete everything.)

NOT EVERY “DIRECT FUNDER” IS A “DIRECT FUNDER”

There are a number of small firms that might market themselves as a direct funder, but the reality is that all they do is fund their deals through some type of syndication platform. My definition of a direct funder or lender is one that has built their own underwriting platforms and produced their own formulas to complete merchant cash advance transactions or alternative business loans. Thus, to be a direct funder (based on my definition), it’s going to “cost you something” in terms of real investment in your infrastructure, your people, as well as needing to raise millions of dollars in lending capital.

OUR TRUE PURPOSE IS DISRUPTION

Understand that our true purpose here on the alternative side of the debt financing space is to innovate how financing is underwritten, approved and delivered, seeking to steal market share away from traditional lending systems. The media calls this process “disruption.” Our system is so efficient, that with one of our industry’s most popular platforms, a small business owner can go online at 11:30 a.m. to apply for a loan, get an approval by 12:15 p.m., then complete their entire closing process online by 12:25 p.m. Within 60 minutes, a small business can start, sign for, and close their small business loan application for amounts including $25k, $75k, $150k, $200k, etc., and receive the funds in their bank accounts the next morning. The traditional lending system cannot underwrite, approve and deliver financing with this amount of efficiency, speed and proficiency.

IF YOU ARE GOING TO BE A DIRECT FUNDER, WHY NOT CONTRIBUTE TO CHANGING THE GAME?

Various reports on marketplace lending have estimated that the global lending size of our space is near $60 billion per the end of 2015, but it’s also estimated that by 2020 we will be near $300 billion of the total global lending market (includes lending on the consumer and commercial sides). Understanding this, what baffles me with new funders and lenders, is why in the hell are you going through the hassles of setting up your own platform, raising millions of dollars in lending capital, and setting up an experienced underwriting team, only to come into the market and do absolutely nothing different?

That makes absolutely no sense. You have the technology, the people, the capital and the formula behind you, so please add a unique contribution to our space to assist our industry as a whole (consumer and commercial side) in growing to this $300 billion in global lending metric by around 2020.

SPECIALIZATION RECOMMENDATIONS

When you enter the market and send brokers information on your program, it should be clear what separates you from everybody else and what your unique role will be going forward in helping our space achieve this $300 billion in global lending metric. Here are a couple of recommendations off the top of my head that you could utilize for specialization:

#1.) A True High Risk Funder/Lender

How about actually funding industries that nobody else will fund? I’ve seen this promoted before but I’m talking about going all the way by taking a look at our market’s standard underwriting practices across the board, then asking the question of, “What merchants are being pushed out and why? How can we start saying YES to these merchants rather than saying NO like everybody else is doing?” You could begin by putting together a list of industries on just about every funder or lender’s restricted list, then trying to figure out how to fund these categories with risk based pricing.

#2.) Bring Efficiency To Global Lending

How about funding in countries that other funders aren’t funding in? Basically, bringing the efficiency of the US market to the global markets in a way that currently is lacking? It’s hot over here in the US market with many players and competitors, but what about in the UK, Australia, China, etc.?

#3.) A Completely New Product

How about creating a new alternative working capital product that we’ve never heard of before?

#4.) Further Lowering Of Pricing

How about find a way to continue bringing down your cost of operations, administration and lending, so that brokers are able to have lower base pricing to increase profitability on lending to merchants, even those in A+ and A Paper categories? This can also help open up the market to attract higher credit grade merchants due to the lower pricing available, but still with “liberal” underwriting procedures.

#5.) A More Efficient Alternative Asset Based Lending Product

How about creating a more efficient alternative asset based lending product, that competes with the current crop of alternative asset based lenders? The current crop that we have today has a lot of inefficiencies within their product, such as having the merchant put up luxury items or even their house to obtain approval, but still charging the merchant rates that resemble traditional merchant cash advance factor rates or even higher. Shouldn’t the fact that a merchant is putting up tangible collateral lower the risk on the deal, which should also lower the pricing and extend the term? So I say, how about some innovation be done in this area so more of these products could be sold?

#6.) Innovation in Factoring, Purchase Order Financing and Equipment Leasing

How about providing accounts receivable factoring, purchasing order financing and equipment leasing, but finding a way to provide such services in an innovative fashion that’s different than the current crop of funders or lenders offering said services?

#7.) A Real Alternative Based Line Of Credit

There are certainly alternative line of credit programs out in our market today, but they are not as efficient as they should be. How about you create a real alternative based line of credit that would resemble something similar to a credit card line of credit, where the merchant can take it out and have it on the side, without it interfering with that of other financing programs such as a merchant cash advance or an alternative business loan?

#8.) Innovation In Consumer Lending

I know that regulations are much higher on this side, but could it be possible for you to find a way to create some innovative consumer lending products as well?

THE FINAL WORD

You have the technology, the people, the capital and the formula, so why in the world do you want to copy a current player instead of doing something different?

While I’m not saying that you shouldn’t also offer said programs of the current players to steal market share away from them, it’s just my opinion that the biggest opportunity today for new funders and lenders is to specialize in other niche areas that aren’t being catered to by our current market players.

Doing so should allow you to come in, specialize, make a name for yourself, and brand your organization as the “go to” funder/lender for (insert innovative concept here) for years to come. It might take you some time to “perfect” your unique brand and approach, but as long as you have investors that believe in your concept, you should be able to survive through the growing pains. To quote Herman Melville, always remember the following: It is better to fail in originality than to succeed in imitation.

Online Lenders Plummet Simultaneously to All-Time Lows

January 14, 2016 If it was involved in online lending, investors dumped it on Wednesday January 13th. LendingTree, a consumer lending platform, dropped nearly 30% for the day despite reporting positive results.

If it was involved in online lending, investors dumped it on Wednesday January 13th. LendingTree, a consumer lending platform, dropped nearly 30% for the day despite reporting positive results.

OnDeck closed at a new all-time low of $7.33, a drop of almost 14% for the day.

Lending Club also closed at a new all-time low. They finished at $8.86, after a comparably modest drop of 6.5%.

Enova International, the company that acquired The Business Backer back in August, closed at an all-time low. At $5.58, their stock dropped 3.13% for the day.

Square, a payments company with a substantial merchant cash advance operation, was down 4%, but they did not break the record for the all-time low they had just set six day earlier.

Yirendai, a Chinese peer-to-peer lender on the New York Stock Exchange, also managed to escape an all-time low despite being down 1.55%. Their all-time low record was also set just six days earlier.

For comparison’s sake, the S&P 500 was down 2.5% on the day. The continuous beating for online lenders, which can’t seem to catch a break in the market, is especially ominous because the economy is not in a recession and there are no indications that any of their business models are legitimately threatened. Nearly a decade since the beginning of the financial crisis, it’s apparently still cool to hate lenders. For LendingTree in particular, the precipitous drop on POSITIVE news was ugly enough to make the headlines in the New York Post. “LendingTree stock was sliced, diced, creamed and puréed,” the Post wrote.

Out there, the little guys who took a leap of faith to support fintech disruption seem like they’re preparing to riot in the streets:

$lc $ONDK ipo underwriters should be in prison

— TheMoneyTeamTMT (@TheMoneyTeamTMT) Jan. 13 at 03:42 PM

This is absurd $LC …this stock is either complete sh*t or we're going to have a monster rally

— Alex (@ROIRogers) Jan. 13 at 03:25 PM

$LC $ONDK new lows… starting to trade like a big recession is already here

— Mark Holder (@StoneFoxCapital) Jan. 13 at 01:42 PM

— BasicNews (@BasicNews) Jan. 13 at 11:49 PM

$SQ Here's another garbage company with bloated forward earnings, all these p o s stocks headed way lower

— QEBubble (@QEBubble) Jan. 13 at 05:18 PM

$LC F* this!

— Don Juan (@fluppy) Jan. 13 at 02:56 PM

$LC selling into oblivion. wtf

— Bork Bork (@calicat) Jan. 11 at 05:00 PM

Perhaps contributing to the damage in Lending Club’s case is that company executives have been dumping their shares over the last several months despite the stock constantly hovering near all-time lows. It certainly doesn’t show a lot of short-term confidence that something is going to change soon.

Insider selling is not the issue in OnDeck’s case which hasn’t really had any. While they were most likely just collateral damage from today’s unyielding carnage, Noah Breslow proclaimed on Squawk Box prior to the opening bell that OnDeck was regulated like a “non-bank commercial lender,” one of those rare characterization departures from their supposedly being a tech company. Aside from that was the sobering letdown that disrupting banks may have never been the goal for them or for online lenders. In a recent article by Broadmoor Consulting’s Todd Baker, he argued that “disruptor” has been the wrong word used to describe many of these companies and that their potential may only go as far as to digitally “enable” banks who are struggling with lagging technology to enable themselves in the modern era. Sound boring? Maybe there’s something bigger in play.

A Recession Could Turn Marketplace Lending Into The Hunger Games

January 13, 2016 When you don’t have the upper hand, one strategy is to partner up with opponents whose skills complement yours in order to compete with everyone else. But partnerships, while essential to self-preservation in an ultra competitive environment, are fleeting on the road to victory. When the field starts to narrow, it’s only a matter of time before truces are cancelled. The enemy of your enemy is your friend until they eventually become your enemy as well. Katniss Everdeen was not a lender last I checked, but her story is not so different.

When you don’t have the upper hand, one strategy is to partner up with opponents whose skills complement yours in order to compete with everyone else. But partnerships, while essential to self-preservation in an ultra competitive environment, are fleeting on the road to victory. When the field starts to narrow, it’s only a matter of time before truces are cancelled. The enemy of your enemy is your friend until they eventually become your enemy as well. Katniss Everdeen was not a lender last I checked, but her story is not so different.

Just last year, OnDeck partnered up with Chase while Fundation partnered up with Regions bank. Dozens of other “lenders” have partnered up in a different way with WebBank, Bank of Internet and Celtic Bank. Marketplace lending platforms that serve as centralized matchmakers have partnered up with hundreds of lenders and merchant cash advance companies. And Wells Fargo has had an arrangement with CAN Capital for what seems like forever.

Bank of America however, has vowed to fight on alone. According to the Wall Street Journal, BoA CEO Brian Moynihan “has no plans to partner with online or alternative lenders in part because of potential dings to its reputation.” Is that decision at their own peril?

While 2015 became the year of alternative lenders gushing about partnerships with banks (and that supposedly being the plan all along), Broadmoor Consulting Managing Principal Todd Baker relegated these alleged disruptors to a lesser status he refers to as “enablers.” Baker posits that OnDeck’s future for example, “may be brighter as a technology provider to banks than as a freestanding finance company subject to the vagaries of economic, credit, liquidity and regulatory cycles.” While perhaps not intentional, he seems to suggest that overtaking banks through technological innovation was unlikely and that alternative lenders are destined to a life of impotence, one that merely “enables” the competitors they were never going to beat.

Somewhere out there in the arena, Baker’s best friend Mike Cagney of SoFi is gearing up to win the 2016 Hunger Games. By openly admitting that banks like Wells Fargo and First Republic are the enemy, Cagney exhibits the ferocity one would expect of a tribute from District 2. SoFi has made nearly $7 billion in loans and wants their borrowers to leave their banks.

Behind the scenes, the Head Gamemaker is threatening to shower the arena with regulations and rising interest rates. While the alternative lending contestants partner up to ensure survival at least until the later rounds, there is potential trouble brewing in and around Panem, another recession. To hear most companies tell it, they would welcome a recession because they believe their models are built to withstand boom and bust cycles. Indeed, the atmosphere at Money2020 was exactly that, that it would be really convenient if the weak could hurry up and die already.

We should however consider that the consequences of a recession may go one step further and tip the scales of lending in a way that the “enablers” almost unwittingly become the new masters few now believe they’re destined to be. The Royal Bank of Scotland chief credit officer for example has already gone on record and told the public to sell bloody everything and prepare for the impending end of the world. 2016 will be a “cataclysmic year,” Andrew Roberts said. Fortune and Forbes have run less harrowing stories in recent days but warned that China, declining oil prices, and market signals indicate a recession could happen this year or the next. Reuters says we’re just facing a little thing called a “profit recession.” But whether these issues are false flags or indications of something more, an environment where credit once again becomes frozen in the traditional banking system could mean a suspension of partnerships between banks and alternative lenders. For alternative lenders that rely entirely on traditional banks for capital to begin with, the end for them will be swift and painful.

For those that don’t, let’s just say there’s a certain long-term advantage to being open for business when everyone else is closed. The merchant cash advance industry for example, which operated in an abyss between 1998 and 2008, suddenly awoke like a sleeping dragon during the Great Recession. In what is now a $7 billion/year industry or a $20 billion/year industry depending on how you define a merchant cash advance, the concept is now widely accepted as an alternative to traditional financing, even if at times criticized.

Foundation Capital’s Charles Moldow believes that “marketplace lending” will be a trillion dollar industry by 2025. “Consumers are fed up,” writes Moldow in his white paper. “Banks are no longer part of their communities. Rates are high for borrowers and not even keeping up with inflation for depositors. During the Great Recession of 2008-2009, when consumers and small businesses needed access to credit more than ever, many banks stopped offering loans and lines of credit.”

71% of Millenials would rather go to their dentist than listen to what banks are saying, according to Viacom’s Scratch. 33% believe they won’t need a bank at all in 5 years.

The presumption is often that banks will prevail in the lending tug-of-war anyway because they are more or less tasked by the federal government to be the arbiters of all lending activity. An economy where consumers and businesses regularly conducted their finances outside the purview of the banking system would be a nightmare scenario for a government that relies on the ability to monitor and control everything. Ergo alternative lenders should partner up with these banks, “enable them” and surrender to a future of impotence in which their only purpose is to serve their masters until perhaps one day the banks replace them with something else.

With alternative lenders still operating unfettered for now, today’s developing regulatory pressure would in all likelihood be traded for support in a recession, even if that support came in the form of willful ignorance.

If Millenials would already rather get a root canal than talk to their bank, then it’s probably not a good time for banks to become even less friendly, as would happen in a recession. The timing of one in the near future is almost to be expected considering how long it’s been since the last one, but the next one could be one of those transformative moments in history in which the world actually comes out looking a little bit different. Make no mistake, today’s alternative lenders are disruptive, they’ve just been playing the game rather safely. Partner up, work together, “enable” if they must, whatever it takes to ensure their survival into the later rounds. From student loans to consumer loans to business loans, 2016’s tributes are a force to be reckoned with.

There was only supposed to be one victor of the 74th hunger games, the banks. And there was always one until one year there were two. They surprisingly weren’t there to serve and enable their master either. The system that always was, was irreversibly disrupted.

The next recession could produce a similar outcome. Partnering with banks now seems like a great idea, but absent an actual merger or acquisition, they should be considered temporary alliances. You know what that means…

To the marketplace lenders and the technologies that power them, happy 2016! And may the odds be ever in your favor.