BRIEF: OnDeck Expands in Denver, Invests $5 million in Office Space

June 16, 2016

OnDeck is expanding its Denver hub.

The online lender inaugurated a new office space worth $5 million, that can accommodate 550 people as it plans to add more to its existing staff there of 170. This is OnDeck’s second biggest hub after New York where it employs 300 people.

The state of Colorado and the Denver Office of Economic Development each gave the company $500,000 in 2012. And in August 2015, OnDeck won an additional $10.4 million in job growth incentive tax credits for creating an additional 400 jobs.

“Our goal is to steadily grow the office and invest more in Denver,” said Noah Breslow, the company’s CEO was quoted as saying in the Denver Post. “Denver is a natural fit for OnDeck.”

States like Colorado and New Jersey are wooing new fintech companies to build and expand their bases in the region. Thanks to the Grow New Jersey Assistance Program, merchant cash advance companies including World Business Lenders and Yellowstone Capital relocated from New York City over across the Hudson to Jersey City in exchange for tax credits. Yellowstone, for instance will earn $3.3 million over ten years in tax credits.

BRIEF: Legend Funding Secures $3 million Debt Facility

June 14, 2016New York City-based merchant cash advance company Legend Funding secured a $3 million debt facility from Houston-based investment investment banking firm Ango Worldwide.

Legend provides working capital financing to businesses in the USA and Canada and the company plans to use the funds for expansion. The deal gets Ango some equity and a seat on the board.

“The merchant cash advance industry is experiencing exciting growth and we felt that the legend management team are strongly positioned to take advance of this opportunity,” said Ango CEO John Carson in a news release.

Industry Goes Par for the Course

June 13, 2016Two companies in the industry are sponsoring golfers in this year’s U.S. Open, Mike Van Sickle via Expansion Capital Group (ECG) and Billy Horschel via Lenders Marketing.

Back in February, ECG SVP Steve Beveridge said, “we are excited to announce our partnership with Mike as a member of the ECG team. His motivation, drive, and dedication represent the same core values that ECG admires in our business clients who are pursuing their own individual dreams.” (Below: Van Sickle in an Expansion Capital Group shirt)

Van Sickle is ranked 1,297th in the world.

Horschel by contrast is ranked 55th in the world. Lenders Marketing, a lead generation company, also sponsored Michael McCabe last year during the PGA Tour Barracuda Championship in Reno, Nevada. (Below: McCabe in the green hat and Justin Benton of Lenders Marketing behind him to the left with the glasses over a white hat)

Transparent Pricing Creates a Level Playing Field, says Kabbage’s Kathryn Petralia

June 7, 2016 Loan matchmaking site Lending Tree has joined the Innovative Lending Platform Association (ILPA) to participate in developing a universal small business lending disclosure system to raise transparency with lenders. It will work closely with the association over a 90-day “national engagement period” to create and implement the SMART Box (Straightforward Metrics Around Rate and Total Cost).

Loan matchmaking site Lending Tree has joined the Innovative Lending Platform Association (ILPA) to participate in developing a universal small business lending disclosure system to raise transparency with lenders. It will work closely with the association over a 90-day “national engagement period” to create and implement the SMART Box (Straightforward Metrics Around Rate and Total Cost).

AltFinanceDaily spoke to Kathryn Petralia, cofounder of Kabbage Loans, which is spearheading the association with OnDeck and CAN Capital. Below are the edited excerpts from the interview:

Tell us about how the ILPA came about?

We (OnDeck, CAN Capital and Kabbage) represent the largest non bank lenders. We have collectively lent $12 billion through the course of our businesses and so we thought it will be great for us to make a statement through ILPA. We came from a perspective that there are a lot of different products for small businesses on the market like merchant cash advance, equipment financing, invoice factoring and lines of credit. All of these serve different needs and are ambiguously priced. So we wanted to find some methodology which is transparent to borrowers so they can know the exact price and total cost of borrowing.

We want to keep it open and hope that everyone participates in the disclosure methodology so borrowers can have a clear understanding of the fees they are paying.

What is SMART Box. How does it work?

Different loan products have different fees — some have maintenance fees, some have broker fees, usage fees and so on and they are all structured very differently. It can get very confusing and so we came up with all the products to understand what disclosures would be necessary to know the total cost of borrowing. We’re working with OnDeck and CAN Capital to gather comments and disclose a series of methodologies that will create the ‘Straightforward Metrics Around Rate’ and Total Cost or SMART Box. Those who want to participate will have to disclose it on loan agreements to their customers.

What about disclosures by companies? Would you say the industry needs more regulation on that front?

Kabbage and other companies in the industry are all regulated and go through FDIC audits. We all follow KYC, CIP, FFIEC guidelines that refer to lenders. We all follow these regulations and I would argue vociferously that we are regulated businesses already. All companies are very different and there are a bunch of things happening — states like California, Illinois and New York and CFPB are all taking interest in small business lending and it’s a positive that they recognize the partnership between banks and tech companies. On the general lending side, we have Dodd-Frank and Madden vs Midland which look at lending issues. Some of the regulation is around how loans are sold and some of it is around how they are limited. And on the small business lending side, there is push for more transparency which is the reason we launched ILPA. We wanted to set the standard for what that would look like. And having it done comprehensively is beneficial for us as it gives us a level playing field.

On the consumer lending side, there is transparency but it’s still lacking a comprehensive system that encapsulates the total cost of borrowing. APR is a great metric but the total cost of borrowing must be included.

Give us a snapshot of what the industry looks like to you

All businesses serve different markets, are different in the way they fund their loans and operate in different geographies, so it’s hard to say but in general those who have done a good job at incorporating data and tech and streamlined operative process will have an advantage and will make it through economic turbulence.

What’s your short-term prediction?

Companies that are not well capitalized will have a tough time raising capital in 2016 and we have already been approached by a number of businesses that are looking to sell or find a partnership because they aren’t well capitalized.

Tell us what’s happening at Kabbage?

We have two businesses – the direct lending business which we are trying to grow and the second is the platform business where we have seen sustained growth, with existing partnerships with ING in Europe, Santander in the UK and Scotia Bank in Canada. More partnerships are in the offing – both domestically and in Latin America.

New Funder Doing 12-Month Deals With Weekly Payments (Guess Who)

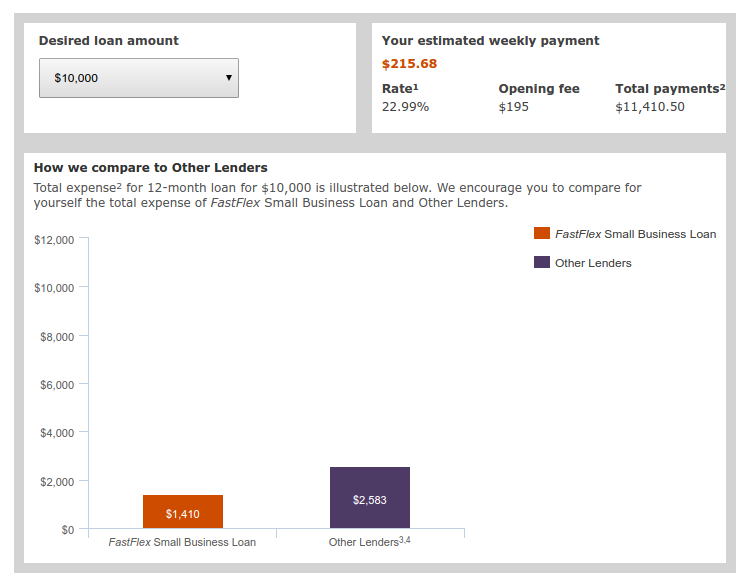

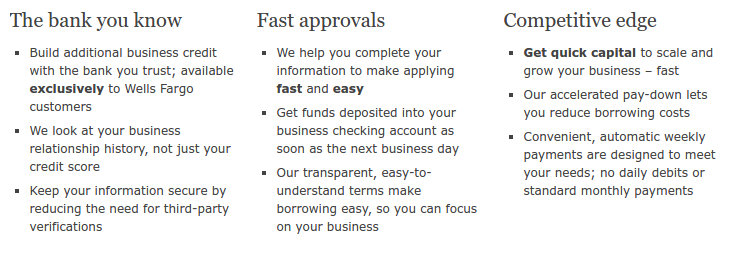

June 3, 2016 Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

Merchants doing at least $4,100 a month in gross deposits are eligible for funding on a 12-month term with weekly ACH debit payments, a new funder revealed. Interest rates start as low as 13.99% but the max funding size is only $35,000. Underwriting decisions can be made instantly online with funds available the next day. “We consider your existing business checking history — not just your credit score,” they advertise.

The name of the funder? Wells Fargo Bank.

The caveat is that applicants must have banked with Wells Fargo for at least 1 year to be eligible. The upside is that little documentation is required to apply outside of the application. The loan is unsecured and the closing fee is only $195. Dubbed FastFlex, the product is clearly meant to compete against online business lenders because well, they mention CAN Capital, OnDeck, and Kabbage in the footnotes on their loan calculator page.

Using their loan calculator, Wells Fargo estimated a 10k loan on a 1.14 over twelve months with weekly ACH payments.

Wells Fargo’s marketing message sounds awfully familiar:

Next day funding, not just your credit score, weekly payments…

Wells Fargo is not alone in their attempts to attack online lenders. Discover Bank for example, is targeting Lending Club directly. By going after the same borrower profile and offering better terms, Discover hopes to cut into Lending Club’s newfound market share.

Unsurprisingly, it is the non-bank prime lenders that will feel the growing bank threat the most. Companies offering small business loans or merchant cash advances to small businesses with damaged credit or complex situations are unlikely to find their target customer pool become bankable any time soon.

It’s Time to End the Phrase ‘Marketplace Lending’ – Because it’s Insane

May 19, 2016

Nobody knows what “marketplace lending” means, including me. That’s kind of ironic considering AltFinanceDaily is for the most part a publication dedicated to it. In fact, the cover of the March/April issue featured a big yellow robot sporting a name tag that actually said, “Hello, my name is Marketplace Lending.” Even the letter I penned that introduced readers to the issue used the phrase not once, not twice, but FIVE TIMES.

The FDIC basically defined it as encompassing all types of financing that include the practice of pairing borrowers over an online platform. Eager to be hip to the industry’s newest lingo, I got on board, and unfortunately perpetuated something that makes almost no sense.

Many companies operating under the marketplace lending umbrella don’t even know that they’ve been lumped into it. It’s become a media buzzword, something to help the simple masses understand so that they will click on a news headline without worrying if the content will only be geared toward the financially savvy.

Imagine shopping for a loan at a supermarket, but ONLINE, and voilà, marketplace lending!

But there are virtually no online platforms that work like that. The simplest explanation to describe a dizzyingly diverse industry is the most incorrect one. Lenders set rates and terms, borrowers don’t choose exactly what they want from a virtual shelf and put them in an imaginary shopping cart. There are however, portals where prospective borrowers can review different offers from different lenders in an Expedia-like environment, but this is really just Online Lead Aggregation 2.0, not a new-age system of lending.

Of course, some adopters of the phrase will point out that the marketplace was supposed to refer to the investor side, not the borrower side. It is investors that can shop for loans or notes that they want to invest in. Indeed, on platforms like Lending Club and Prosper, investors can select individual notes with terms befitting their desires and place them in an online shopping cart for purchase. Behold, the marketplace!

But what if you didn’t deal with retail investors hand-selecting $25 notes at a time? Notably, some online platforms that sell their loans to institutions in giant pools by the thousands or millions believe that such activity constitutes a marketplace because somebody is buying what they’re selling. And so long as somebody is selling something to somebody else at some point, the whole thing might as well be a marketplace. And even if it’s not, referring to it as such anyway will garner more press, attract more investors, and boost valuations.

I mean, would a site like TechCrunch be more likely to write about a FinTech Marketplace Lender or a generic financial company that sold a batch of loans to a bank?

I can tell you firsthand that if a press release submitted to us used the term “marketplace lender” instead of “finance company,” we’d at least check it out, or at least we used to. These days, we are becoming numb to its overuse.

Peer-to-Peer lending was an awesome term and it was descriptive too. Everybody could understand it. But then those platforms had to go and start selling their loans to Wall Street instead of peers and come up with something else to still sound trendy, techie, and disruptive. There’s nothing trendy of course about selling loans to financial institutions. It is a quintessential boring business activity of Wall Street. It is the opposite of disruptive, except in the events where all the loans go bad and the entire economy collapses like in 2008.

Peer-to-Peer lending was an awesome term and it was descriptive too. Everybody could understand it. But then those platforms had to go and start selling their loans to Wall Street instead of peers and come up with something else to still sound trendy, techie, and disruptive. There’s nothing trendy of course about selling loans to financial institutions. It is a quintessential boring business activity of Wall Street. It is the opposite of disruptive, except in the events where all the loans go bad and the entire economy collapses like in 2008.

The FDIC specifically said that marketplace lending can encompass unsecured consumer loans, debt consolidation loans, auto loans, purchase financing, real estate loans, merchant cash advance, medical patient financing, and small business loans. This wildly diverse list, which even includes a non-loan product, will obviously have platforms in every category where people or businesses can get paired with a source of funds via the Internet. It’s 2016. It’d be weird if you couldn’t search for financing online. You can do everything else on the Internet. Just because a search happens online shouldn’t mean that the resulting options should be thrown together in some special broad category of lending and then be judged according to what all the other sectors do.

None of this is said to diminish the technological feats that many platforms have achieved. People and businesses can access capital in much faster and more convenient ways than ever before. Their growth and success is America’s economic gain. Jobs have been created and borrowing costs reduced. Hooray, perhaps, for marketplace lending.

The problem is merely the characterization that anyone lending to anyone else these days must also be a marketplace. That makes no sense.

Who will be the first to stop the madness?

Defrauding Fintech Lenders Leads to Conviction

May 8, 2016 It’s not just collection firms and attorney demand letters that deceptive borrowers need to be wary of. In the Western District of Tennessee, Preston E. Byrd was convicted on six counts after defrauding RapidAdvance and Windset Capital out of more than $100,000 collectively.

It’s not just collection firms and attorney demand letters that deceptive borrowers need to be wary of. In the Western District of Tennessee, Preston E. Byrd was convicted on six counts after defrauding RapidAdvance and Windset Capital out of more than $100,000 collectively.

According to the original indictment filed in August of last year, “Byrd did knowingly devise and intend to devise a scheme and artifice to defraud Windset Capital and RapidAdvance by means of false and fraudulent pretenses, representations and promises.” As part of that, Byrd submitted fake bank statements, a fake lease agreement and other misleading documents. He faked his own name, calling himself Jason Hester, and pretended to be the landlord of the property in question, confirming falsely to underwriters that a lease existed and was in good standing.

In reality, he had no business location.

Once Byrd received the funds from each company, he wired portions of the ill-gotten proceeds to other accounts.

The jury convicted him on three counts of wire fraud and three counts of engaging in monetary transactions in criminally derived property. The trial concluded on March 24th of this year and Byrd is expected to be sentenced on June 16th.

The case is unique because the sole victims were fintech lenders and the criminal charges were brought by United States Attorney Edward L. Stanton III.

On his twitter account, Byrd describes himself as a “multifamily housing developer, entrepreneur, business consultant, public speaker, mentor, yogi, and (some might say) a cool dude.” Not mentioned there however is that Byrd was previously convicted of wire fraud in 2003 and that he also lost a lawsuit brought by Arvest Bank for fraud.

The criminal case # concerning Byrd with Rapid and Windset is 2:15-cr-20025-JPM

Stairway to Heaven: Can Alternative Finance Keep Making Dreams Come True?

April 28, 2016

The alternative small-business finance industry has exploded into a $10 billion business and may not stop growing until it reaches $50 billion or even $100 billion in annual financing, depending upon who’s making the projection. Along the way, it’s provided a vehicle for ambitious, hard-working and talented entrepreneurs to lift themselves to affluence.

Consider the saga of William Ramos, whose persistence as a cold caller helped him overcome homelessness and earn the cash to buy a Ferrari. Then there’s the journey of Jared Weitz, once a 20 something plumber and now CEO of a company with more than $100 million a year in deal flow.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

Their careers are only the beginning of the success stories. Jared Feldman and Dan Smith, for example, were in their 20s when they started an alt finance company at the height of the financial crisis. They went on to sell part of their firm to Palladium Equity Partners after placing more than $400 million in lifetime deals.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

The industry’s top salespeople can even breathe new life into seemingly dead leads. Take the case of Juan Monegro, who was in his 20s when he left his job in Verizon customer service and began pounding the phones to promote merchant cash advances. Working at first with stale leads, Monegro was soon placing $47 million in advances annually.

Alternative funding can provide a second chance, too. When Isaac Stern’s bakery went out of business, he took a job telemarketing merchant cash advances and went on to launch a firm that now places more than $1 billion in funding annually.

All of those industry players are leaving their marks on a business that got its start at the dawn of the new century. Long-time participants in the market credit Barbara Johnson with hatching the idea of the merchant cash advance in 1998 when she needed to raise capital for a daycare center. She and her husband, Gary Johnson, started the company that became CAN Capital. The firm also reportedly developed the first platform to split credit card receipts between merchants and funders.

BIRTH OF AN INDUSTRY

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Competitors soon followed the trail those pioneers blazed, and the industry began growing prodigiously. “There was a ton of credit out there for people who wanted to get into the business,” recalled David Goldin, who’s CEO of Capify and serves as president of the Small Business Finance Association, one of the industry’s trade groups.

Many of the early entrants came from the world of finance or from the credit card processing business, said Stephen Sheinbaum, founder of Bizfi. Virtually all of the early business came from splitting card receipts, a practice that now accounts for just 10 percent of volume, he noted.

At first, brokers, funders and their channel partners spent a lot of time explaining advances to merchants who had never heard of them, Goldin said. Competition wasn’t that tough because of the uncrowded “greenfield” nature of the business, industry veterans agreed.

Some of the initial funding came from the funders’ own pockets or from the savings accounts of their elderly uncles. “I’ve met more than a few who had $2 million to $5 million worth of loans from friends and family in order to fund the advances to the merchants,” observed Joel Magerman, CEO of Bryant Park Capital, which places capital in the industry. “It was a small, entrepreneurial effort,” Andrea Petro, executive vice president and division manager of lender finance for Wells Fargo Capital Finance, said of the early days. “A number of these companies started with maybe $100,000 that they would experiment with. They would make 10 loans of $10,000 and collect them in 90 days.”

That business model was working, but merchant cash advances suffered from a bad reputation in the early days, Goldin said. Some players were charging hefty fees and pushing merchants into financial jeopardy by providing more funding than they could pay back comfortably. The public even took a dim view of reputable funders because most consumers didn’t understand that the risk of offering advances justified charging more for them than other types of financing, according to Goldin.

Then the dam broke. The economy crashed as the Great Recession pushed much of the world to the brink of financial disaster. “Everybody lost their credit line and default rates spiked,” noted Isaac Stern, CEO of Fundry, Yellowstone Capital and Green Capital. “There was almost nobody left in the business.”

RAVAGED BY RECESSION

Perhaps 80 percent of the nation’s alternative funding companies went out of business in the downturn, said Magerman. Those firms probably represented about 50 percent of the alternative funding industry’s dollar volume, he added. “There was a culling of the herd,” he said of the companies that failed.

Life became tough for the survivors, too. Among companies that stayed afloat, credit losses typically tripled, according to Petro. That’s severe but much better than companies that failed because their credit losses quintupled, she said.

Who kept the doors open? The firms that survived tended to share some characteristics, said Robert Cook, a partner at Hudson Cook LLP, a law office that specializes in alternative funding. “Some of the companies were self-funding at that time,” he said of those days. “Some had lines of credit that were established prior to the recession, and because their business stayed healthy they were able to retain those lines of credit.”

The survivors also understood risk and had strong, automated reporting systems to track daily repayment, Petro said. For the most part, those companies emerged stronger, wiser and more prosperous when the crisis wound down, she noted. “The legacy of the Great Recession was that survivors became even more knowledgeable through what I would call that ‘high-stress testing period of losses,’” she said.

ROAD TO RECOVERY

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

The survivors of the recession were ready to capitalize on the convergence of several factors favorable to the industry in about 2009. Taking advantages of those changes in the industry helped form a perfect storm of industry growth as the recession was ending.

They included making good use of the quick churn that characterizes the merchant cash advance business, Petro noted. The industry’s better operators had been able to amass voluminous data on the industry because of its short cycles. While a provider of auto loans might have to wait five years to study company results, she said, alternative funders could compile intelligence from four advances within the space of a year.

That data found a home in the industry around the time the recession was ending because funders were beginning to purchase or develop the algorithms that are continuing to increase the automation of the underwriting process, said Jared Weitz, CEO of United Capital Source LLC. As early as 2006, OnDeck became one of the first to rely on digital underwriting, and the practice became mainstream by 2009 or so, he said.

Just as the technology was becoming widespread, capital began returning to the market. Wealthy investors were pulling their funds out of real estate and needed somewhere to invest it, accounting for part of the influx of capital, Weitz said.

At the same time, Wall Street began to take notice of the industry as a place to position capital for growth, and companies that had been focused on consumer lending came to see alternative finance as a good investment, Cook said.

For a long while, banks had shied away from the market because the individual deals seem small to them. A merchant cash advance offers funders a hundredth of the size and profits of a bank’s typical small-business loan but requires a tenth of the underwriting effort, said David O’Connell, a senior analyst on Aite Group’s Wholesale Banking team.

The prospect of providing funds became even less attractive for banks. The recession had spawned the Dodd-Frank Financial Regulatory Reform Bill and Basel III, which had the unintended effect of keeping banks out of the market by barring them from endeavors where they’re inexperienced, Magerman said. With most banks more distant from the business than ever, brokers and funders can keep the industry to themselves, sources acknowledged.

At about the same time, the SBFA succeeded in burnishing the industry’s image by explaining the economic realities to the press, in Goldin’s view.The idea that higher risk requires bigger fees was beginning to sink in to the public’s psyche, he maintained.

Meanwhile, loans started to join merchant cash advances in the product mix. Many players began to offer loans after they received California finance lenders licenses, Cook recalled. They had obtained the licenses to ward off class-action lawsuits, he said and were switching from sharing card receipts to scheduled direct debits of merchants’ bank accounts.

As those advantages – including algorithms, ready cash, a better image and the option of offering loans – became apparent, responsible funders used them to help change the face of the industry. They began to make deals with more credit-worthy merchants by offering lower fees, more time to repay and improved customer service. “The recession wound up differentiating us in the best possible way,” Bizfi’s Sheinbaum said of the changes.

His company found more-upscale customers by concentrating on industries that weren’t hit too hard by the recession. “With real estate crashing, people were not refurbishing their homes or putting in new flooring,” he noted.

Today, the booming alternative finance industry is engendering success stories and attracting the nation’s attention. The increased awareness is prompting more companies to wade into the fray, and could bring some change.

WHAT LIES AHEAD

One variety of change that might lie ahead could come with the purchase of a major funding company by a big bank in the next couple of years, Bryant Park Capital’s Magerman predicted. A bank could sidestep regulation, he suggested, by maintaining that the credit card business and small business loans made through bank branches had provided the banks with the experience necessary to succeed.

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Smaller players are paying attention to the industry, too, with varying degrees of success. Predictably, some of the new players are operating too aggressively and could find themselves headed for a fall. “Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify’s Goldin. “There’s going to be a shakeout. I can feel it.”

Some of today’s alternative lenders don’t have the skill and technology to ward off bad deals and could thus find themselves in trouble if recession strikes, warned Aite Group’s O’Connell. “Let’s be careful of falling into the trap of ‘This time is different,’” he said. “I see a lot of sub-prime debt there.”

Don’t expect miracles, cautioned Petro. “I believe there will be another recession, and I believe that there will be a winnowing of (alternative finance) businesses,” she said. “There will be far fewer after the next recession than exist today.”

A recession would spell trouble, Magerman agreed, even though demand for loans and advances would increase in an atmosphere of financial hardship. Asked about industry optimists who view the business as nearly recession-proof, he didn’t hold back. “Don’t believe them,” he warned. “Just because somebody needs capital doesn’t mean they should get capital.”

Further complicating matters, increased regulatory scrutiny could be lurking just beyond the horizon, Petro predicted. She provided histories of what regulation has done to other industries as an indication of the differing outcomes of regulation – one good, one debatable and one bad.

Good: The timeshare business benefitted from regulation because the rules boosted the public’s trust.

Debatable: The cost of complying with regulations changed the rent-to-own business from an entrepreneurial endeavor to an environment where only big corporations could prosper.

Bad: Regulation appears likely to alter the payday lending business drastically and could even bring it to an end, she said.

Still, regulation’s good side seems likely to prevail in the alternative finance business, eliminating the players who charge high fees or collect bloated commissions, according to Weitz. “I think it could only benefit the industry,” he said. “It’ll knock out the bad guys.”