Surprise! We Are the Market

January 13, 2013Merchant Cash Advance (MCA) is an alternative to a small business loan. Look around. MCA players have spent so much energy on gaining mainstream acceptance, that we’ve become oblivious to reality. We ARE the small business lending market. There are alternatives out there such as credit cards and SBA loans, but they are industries of their own. Small businesses in 2013 really only have one place to obtain fast unsecured short term financing, and that’s here, the MCA industry. That assumes of course that you agree with our definition of MCA, which we stopped limiting to a purchase of future credit card sales some time ago.

Over the past few months, we began to realize that the only small business lenders making headlines are people we know. Is the country that small or does MCA dominate the market that much?

A glimpse at the sponsored advertisements on Bing in the NYC region:

Where are the multi-billion dollar banks? If $15 a click isn’t in their budget, something is wrong, and it may possibly be due to the fact that business loans aren’t on their priority lists.

Lenders, brokers, and bankers on the front lines can’t stop talking about MCA. It is a recurring theme in their columns:

The alternative financing industry is growing rapidly and, I believe, will continue to grow in 2013. These lenders are extremely entrepreneurial and are leaving the banks behind with their speed and use of technology. Many are backed by premier investment banks and Silicon Valley venture capital powerhouses — investors who understand that entrepreneurs and small-business owners are throwing up their hands in frustration over how long it can take to get a loan from a bank, especially if the loan is backed by the S.B.A. More and more businesses are willing to pay the price of the alternative lenders just to be able to get their capital and move on.

-Ami Kassar

The State of Small Business Lending – NY Times 1/8/13

Ami’s Column on NY Times

Cash advance companies, accounts receivable financiers, factors, and micro lenders all have become increasingly more attractive funders for three reasons: flexibility, use of technology, and speed.

-Rohit Arora

Three Reasons for the Rise of Alternative Lending – Fox Business 11/29/12

Rohit’s column on Fox Business

Here’s a dilemma that might have contributed to the growth of MCA… Banks don’t like offering loans and business owners don’t like applying for them if it’s hard:

There’s a large small business segment that needs and wants to borrow on a commercial basis, but their needs are very small. Business owners want $10,000, $20,000 or $30,000 loan–the average is somewhere around $25,000. Traditionally, that’s been a very unprofitable business for a bank. Some banks argue that they are willing to lose money on those loans because they can make it up in deposits. But what happens when the borrower has no deposits? It’s a very tough balancing act.

– The Federal Reserve Bank of San Francisco

A newsletter report that reveals banks lose money on small business loans

Community Investments Volume 8; No 4; Fall 1996

Business owners say the documentation involved is overwhelming. They’ve also found the qualification terms almost impossible to meet.

– Catherine Clifford

Feedback reveals that a burdensome application process and extensive paperwork requirements are enough to discourage business owners even if the loans carry 0% interest.

CNN 1/26/10

Thousands of researchers publish statistics on bank lending every month. Not only do they all contradict each other but journalists that use this data to make bold claims often fail to acknowledge that an increase in bank lending has nothing to do with the applicants, the economy, or the banks themselves. It has to do with the Government. We all know that the SBA will cover the losses banks incur, but there are programs that go one step further. The Federal Government actually bribes banks to make loans. For example, the Small Business Lending Fund is a dedicated investment fund that encourages lending to small businesses by providing capital to community banks. Meaning, covering the losses on defaults doesn’t seem to be enough, so they’ll actually provide the money to make the loans as well.

Click to see full size on mobile

According to the SBA, small business bank borrowing totaled $584.1 billion in the third quarter of 2012. That number dwarfs the volume produced by the MCA industry, but its not an apples to apples comparison. A loan of $1 million dollars is within the range of a small business loan by the SBA, an amount atypical (though not impossible) in the MCA world. Banks are also prodded and coddled by the Government so much that it has reached the extent that we dare claim they are an extension of the Federal Government itself. There’s some food for thought for the Occupy Wall Street movement! They also conveniently got bailed out when they were on the verge of failure, a safety net that MCA companies don’t have.

According to the SBA, small business bank borrowing totaled $584.1 billion in the third quarter of 2012. That number dwarfs the volume produced by the MCA industry, but its not an apples to apples comparison. A loan of $1 million dollars is within the range of a small business loan by the SBA, an amount atypical (though not impossible) in the MCA world. Banks are also prodded and coddled by the Government so much that it has reached the extent that we dare claim they are an extension of the Federal Government itself. There’s some food for thought for the Occupy Wall Street movement! They also conveniently got bailed out when they were on the verge of failure, a safety net that MCA companies don’t have.

Subtract the Federal Government’s meddling and there is only one profitable form of B2B lending, Merchant Cash Advance. That is of course again if you accept our definition. There are many young B2B lending firms that claim to be an alternative to MCA, who then go on to describe their product in a manner that is textbook MCA.

Our thesis may be debatable and lacking in concrete proof, but we’re not writing dissertations here. Business owners are increasingly looking to the Internet for loan information and it’s obvious what they’re finding. One would expect a quick Internet search to bring up ads for the billion dollar powerhouses, you know the ones that are given millions to lend out and then millions again when the loans go bad. Instead we find companies owned by friends or friends of friends. The small business loan market isn’t run by anonymous Wall Street kingpins, it’s run by a small community of entrepreneurs that all started from the ground up. Only the community isn’t so small anymore. There was once a handful of MCA companies claiming to be an alternative to a small business loan. Now there are a handful of companies claiming to be an alternative to MCA. It doesn’t take a genius to figure out why that is. After years of fighting to be recognized in the market, something remarkable happened, we became the market itself…

– Merchant Processing Resource

../../

Movember Rocked!

December 1, 2012 Movember: Mo’ Merchants, Mo’ Deals

Movember: Mo’ Merchants, Mo’ Deals

The pre-holiday season is usually big in the Merchant Cash Advance (MCA) industry but this year seemed different. We’ve been saying that we’ve entered a new era for a long time, but it’s finally starting to seem real. It feels like 2007 again in a way, when everybody was getting rich and nobody even knew what the heck they were selling. It took years for account reps to finally stop referring to advances as loans and by then it was too late because the ACH loan industry was born.

E-mails like this don’t happen very much anymore:

You know… the ones where the deal would be blatantly shotgunned to multiple companies at once. The major broker shops would “accidentally” CC everyone instead of BCC to let the funders know who was in charge.

That’s not to say that deals don’t get shopped, Some do, but the circumstances have changed. To minimize the risk of being flooded with bad paper, funders ask resellers to put their money where their mouth is. The syndication game has become THE game in town and it’s led to Super ISO networks like the Factor Exchange. A user on the DailyFunder that seems to be intimately familiar with Factor Exchange is quoted as explaining the model like this:

The “mom and pop” ISOs and “Onesy-Twosey” brokers are backed by one giant ISO network and The Factor Exchange assumes half of the risk by syndicating 50% on nearly ever deal…

The massive volume of FEX submissions to lenders gives the ISOs power to negotiate for better rates and terms, One point of submission reaches 15+ lenders, the merchants credit is only pulled once, and the commission is passed straight through to the ISOs because FEX makes their money from participation.

Companies like this empower the smaller brokerages…

Who Did Mo’ Deals in Movember?

Yellowstone Capital broke their single day funding record… TWICE. This actually happened on back to back days. Executive management reported that they funded approximately $3 million in 48 hours.

Who Got Mo’ Money?

Wall Street wizard and business professor, Steven Mandis acquired a stake in Bethesda-based RapidAdvance. The news is all the more interesting with the fact that RapidAdvance is easily one of the top 5 largest players in MCA. Single individuals don’t exactly just walk through door and buy a stake in companies like this. Mandis is taking on a Strategic Advisor position and it’s our guess Rapid is about to enter another major phase of growth.

Who Got Mo’ Likes?

Merchant Cash and Capital’s (MCC) facebook fan page has gotten thousands of Likes since the third week of Movember when they announced their charity campaign. For every new Like until December 7th, MCC is donating $1 to the American Red Cross to help people that were affected by Hurricane Sandy.

Who Got Mo’ Wins?

RapidAdvance was the first team to clinch the playoffs in the MCA industry fantasy football league for charity. Something tells us that Mandis is behind their incredible winning streak.

Who got Mo’ Leads?

You did if you bought leads from either one of our lead advertising partners, Meridian Leads or SmallBusinessLoanRates.com.

Lendio has also been making a splash on the MCA lead scene with Dave Young being a big contributor on DailyFunder. To discuss pricing, he can be reached at dave.young[at]lendio.com

Who lied Mo’?

According to CNN’s statistics, 247 million people in the U.S. went shopping on Black Friday. That’s equal to the entire American population over the age of 14. Something doesn’t smell right with these numbers. It’s our guess that CNN is using Mitt Romney’s polling experts. 😉

But someone else lied just a little bit Mo’. On Movember 26, 2012, PRWeb published a release that claimed ICOA Inc., a small tech company in Rhode Island was acquired by Google for $400 Million. The release turned out to be a hoax as part of a stock pump and dump scheme. Many critics have been left wondering why PRWeb didn’t do anything to verify its authenticity. Considering PRWeb is such a widely used PR service in the MCA space, we can testify that they’ll pretty much publish anything so long as you pay the fee. Some smaller companies use it as part of their SEO campaigns, which explains why there are so many strange looking releases out there that seem to repeat the same keyword in every sentence.

ABC Funding Co Just announced a program that will help small businesses in need of cash by providing these small businesses in need of cash with a special type of financing that will hep them if they are a small business in need of cash. Not exactly New York Times material…

Will Movember be followed by Make-a-lot-of-Doughcember? We’ll find out!

– Mo’chant Processing Resource

../../

The Bubble That Wasn’t

August 17, 2012“The smaller the loan, the more likely a lender will deny it. The denial rate for applications for small loans (less than $100,000) was more than twice as high as it was for bigger loans.”

– CNNMoney 8/16/12

In early 2009, a very wise friend of mine gave me a bit of advice. As an ex-stock broker who made his fortune in the 80s, he’d seen his fair share of bubbles. And so he bestowed upon me his wisdom that the Merchant Cash Advance (MCA) industry’s days were numbered. “It’s got 6-8 months left of life in it and then it’ll go away. Everyone’s in freakout mode right now but things will go right back to the way they were and banks will push you right out of a job,” he lectured me. My expression didn’t change, for he wasn’t the first one to sing me this cautionary tale. He continued on, “You’re a nice guy so I suggest in the next few months, you go out and get into another line of work. You can always look at this experience as a wild ride but MCA is a fringe industry borne out of the financial crisis.” I thanked him for looking out for me and went home that night to mull over what he and a few others had been saying.

No one wants to believe their thriving business is part of a bubble that will inevitably burst. But at the same time, no one wants to later on be perceived as that naive fool that couldn’t see an obvious end coming either. And while the career itself seemed honorable and sustainable (helping small businesses get financing), there were a lot of pivotal moments along the way that made me think for a second that at any day I could be told to pack up my stuff and go home because there was suddenly no more demand for MCA.

No one wants to believe their thriving business is part of a bubble that will inevitably burst. But at the same time, no one wants to later on be perceived as that naive fool that couldn’t see an obvious end coming either. And while the career itself seemed honorable and sustainable (helping small businesses get financing), there were a lot of pivotal moments along the way that made me think for a second that at any day I could be told to pack up my stuff and go home because there was suddenly no more demand for MCA.

I am reminded of the time when a Craigslist Ad was answered by over 500 recently laid off mortgage brokers and underwriters. Some had literally been hired to underwrite mortgages, only to be told days later that their division was closing down. Similarly, there were hot shots from the payday loan industry who stopped by to learn what our business was all about. These people looked like they had been punched in the gut and told stories of major success followed by unforeseen ruin as states legislated them out of business overnight. And still others had the mentality that MCA was a get rich quick scheme and went on to run their own funding companies or brokerage offices into the ground within a matter of months. They cursed the MCA gods and the bubble they believed they were a victim of, ignoring the reality that they had poorly managed themselves into oblivion.

As the 6 to 8 month timeline for destruction expired and the light shone on those still standing, I realized I had made the right choice by sticking it out. MCA was not a progeny of the financial meltdown. Heck, the product itself had already been around since the late 1990s and had gained significant popularity around 2005 when other players began entering the market. It also had none of the trademark signs of a bubble. If financing businesses was a bubble, there would be no such thing as banks today. Business financing has been around for literally thousands of years. MCA firms just catered to the ones that banks ignored and by 2008 that included nearly every small business in the country. One could argue that the growth rate of MCA would eventually slow down, supporting the claim with the same wisdom I had heard nearly a year before, that everything would return to “normal.”

Today’s world is anything but the world of yesterday. The unemployment rate in July was 8.3% and according to a survey reported by CNN, “[Today], the option most often sought by businesses — opening a new credit line — face[s] the lowest approval rate at 13%” Banks never did return to their old ways, nor does it seem likely that they will any time soon. Those that doubted MCA’s longevity in 2009, including those who left the industry altogether back then in fear, did not foresee the many roads of evolution that would allow it to thrive.

Years ago, an MCA was easily defined as a purchase of future sales that would ideally be completed in 6 to 9 months. Virtually every provider offered identical terms and costs, which stymied competition and eventually created stereotypes that would come to haunt the image of MCA for quite some time. For a while, America had a hard time envisioning MCA as anything but a 1.38 factor rate that was available to those that fit a certain credit criteria and processed a minimum amount of credit card sales monthly. So imagine the shock some small business owners felt when approved by RapidAdvance, a veteran MCA firm, for a ::gasp:: small business loan. A loan?! could it be? Yes, MCA has been semantically broadened to include many forms of short term lending. And then there’s Florida based Merchant Cash Group that became famous with their Fast Funding program, a financing option for businesses that fell outside the box for traditional MCAs. Some companies don’t even require businesses to accept credit cards as a form of payment. “Credit card sales? Who cares how much they’re doing in credit card sales?!” Would you ever imagine an MCA rep making such a statement in 2009?

MCA is still widely considered to be tied to credit card processing and it doesn’t ever need to officially evolve away from that. Withholding a percentage of sales directly from a payment processor is what initially allowed the many business owners that were horrible at making monthly payments suddenly eligible to receive capital. But for all the changes that have been applied to the financing product itself, something has changed with the companies offering it as well.

Competitors used to be ultra secretive about their practices. An MCA firm could be underwriting an application that another MCA firm funded the day before. Sure, the merchant wasn’t supposed to hop around and do this with more than one company at a time, but the other firm wouldn’t even confirm if they funded them if you asked. One of the great failures of the past was the lack of cooperation amongst the players in the industry. An ‘every man for himself’ mentality hurt more than it helped in a business that was struggling to create its identity in the mainstream world of finance. The North American Merchant Advance Association (NAMAA) sought to correct that through data sharing and the promotion of common standards. Some of the major members have years of experience under their belt including Merchant Cash and Capital, Strategic Funding Source, RapidAdvance, and Merchant Cash Group. These firms have been around the block and back. “MCA bubble? What bubble?,” they’ll say with 100% confidence in their tone.

So why a boring history lesson on MCA today? It’s only fitting on the day that CNN declared the bursting of the social media bubble, that I re-visit a decision I made 3 years ago. “I’m just looking out for you kid,” a mentor once told me. Bad advice for sure. This year, I am noticing many people that left MCA years ago are coming back. After so much time has passed, they are STILL getting in early on something that’s going to be huge, rather than coming back to ‘manage the decay’ (did I just take a swipe at Obama?!). VCs are having a field day trying to get in on it. Accel Partners recently forged an equity deal with Capital Access Network with the ultimate goal of what I’m guessing is to one day go public.

So why a boring history lesson on MCA today? It’s only fitting on the day that CNN declared the bursting of the social media bubble, that I re-visit a decision I made 3 years ago. “I’m just looking out for you kid,” a mentor once told me. Bad advice for sure. This year, I am noticing many people that left MCA years ago are coming back. After so much time has passed, they are STILL getting in early on something that’s going to be huge, rather than coming back to ‘manage the decay’ (did I just take a swipe at Obama?!). VCs are having a field day trying to get in on it. Accel Partners recently forged an equity deal with Capital Access Network with the ultimate goal of what I’m guessing is to one day go public.

The only things bubbly in MCA these days are the excited account reps, underwriters, and support staff that are working to get America’s small businesses humming again. Some have taken to wearing their FUNDED pants 7 days a week. I know I have practically worn mine out.

I’m always struck now by the college grads that ask me if this business is sustainable. Their anxious parents are worried sick that their babies are going to be caught up in some bubble and be out of a job 6 to 8 months from now. To this I offer a few words of wisdom. “Providing small businesses with capital isn’t going away anytime soon. Sure, the product might evolve and the economy will change, but the fundamental demand for short term financing is here to stay. You seem like nice parents so I’d hate to see your kid get involved in some other industry at the end of its life cycle. He or She is getting in early on something big, something long lasting, something that has become a permanent staple of the American financial system.” Good advice for sure.

By: Sean Murray

Founder of Merchant Processing Resource (../../)

Began career in the MCA industry in August, 2006

P.S.

The FUNDED pants do exist and were created by Next Level Funding in early 2010.

It Might Be You

August 8, 2012You are innocently eating your bologna sandwich in the lunchroom when some of your fellow elementary school friends start to giggle. You giggle a little too just because you usually all laugh at things together, even though you’re not exactly sure what the joke was. “Damn,” you think to yourself. “I got all caught up in my bologna sandwich and I missed something.” Soon others begin to laugh. You laugh nervously with them, but take a couple quick glances around the room to try and locate the source of the humor. You spot nothing, but realize the chuckles are spreading like wildfire. Some people are looking at you as if they are suspicious that you might be the only one that doesn’t GET it. So instead you double down on your laughter as if to prove you’re enjoying the joke more than they are. “I’m enjoying whatever it is we’re all laughing at more than you are!,” you say under your breath. This only makes the crowd more raucous and by now everyone is starting to point in your direction.

“Ohhhhh crapppp…”

And then you find out it is you. There you are, sitting in the cafeteria, munching on a bologna sandwich with a grade school level obscenity drawn on the back of your shirt. You don’t know who drew it or when it happened, but you quickly learn it was done in red marker, particularly the kind from the 1980s that smelled like cherry, caused dizziness, and made your nose bleed after 15 seconds. There’s always somebody getting picked on, you just never thought it would be you.

Smells Sooooo Gooddddd

“Ohhhhh crapppp…”

It might be you. Every year or so, the MCA industry welcomes in a couple new big players. There’s always one that funds more, pays more, bends more, and brags more as they quickly cut into the marketshare that established funders have had for years. Suddenly they’re the hottest thing in town, that is until about 6 months later when they start telling their “loyal” broker shops to stop sending in new deals for a while. As the newbie’s joyride comes to an end, the established funders roll their eyes and continue on the way they always have, responsibly.

It might be you. Every year or so, the MCA industry welcomes in a couple new big players. There’s always one that funds more, pays more, bends more, and brags more as they quickly cut into the marketshare that established funders have had for years. Suddenly they’re the hottest thing in town, that is until about 6 months later when they start telling their “loyal” broker shops to stop sending in new deals for a while. As the newbie’s joyride comes to an end, the established funders roll their eyes and continue on the way they always have, responsibly.

We’re not here to point anyone out or to suggest that brokers purposely send bad paper to an inexperienced funder. It’s just easy to spot the amateurs. Sadly, most people laugh at them behind the scenes until the funder calls it quits, completely unaware that they’ve been wearing a “kick me” sign on their back for months.

This could be an uncomfortable topic for some, but this rapid rise and fall scenario plays out across many industries. If your business is less than two years old, ask yourself this: Is your success a result of awesomeness or do you smell a tinge of red cherry marker?

—————

Does anyone know what the truth is anymore? These contradictory articles were both published yesterday by reputable news media outlets:

Banks Keep Lending Standards Tight For Small Firms

Fed Says Banks Ease Standards On Business, Consumer Loans

Is affirmative action coming to a funder near you?

Dodd-Frank’s small business lending time bomb

Growth in the usage of MCAs (selling future sales for cash upfront) is taking a huge chunk of market share away from traditional lenders.

Some crusty old reporters remain clueless as to why fewer and fewer businesses are turning to their banks for loans. Professor Scott Shane in BusinessWeek fumbled through his recent 700 word article in which he makes several unconvincing arguments for credit cards as being the new holy grail for business owners. Ultimately, he concedes that the decrease in small loans to businesses might simply be a benign statistical anomaly. This guy is a professor??!! Borrow, Borrow, Loan, Loan, Loan. Some people still can’t imagine a world where leveraging can happen without a borrower and a lender.

—————

Have you ever tried to peg down what exactly is happening in the credit markets? The National Federation of Independent Business has already done a lot of the work for you. A few clues:

- Small-business owners are increasingly employing personal rather than business cards for business purposes

- Fifty-seven (57) percent of small employers attempted to obtain credit from a financial institution in the last 12 months, a nine percentage point increase from 2010 with the demand for lines and cards each rising more than one-third. The demand for line renewals and loans were flat. More attempts resulted in more rejections rather than more small-business owners obtaining credit

- Poorer credit risks were more likely to try to borrow in 2011 than better credit risks, other factors equal. A number of financial factors, such as credit score, differentiate the two groups. Men and owners of larger small businesses were also more likely than their counter-parts to try to borrow

Download the full 76 page NFIB January 2012 report

—————

Some MCA underwriters hate when merchants state they aim to use the funding proceeds for “cash flow” as if its unspecific nature was code for betting on the horses. In the traditional lending world, businesses have been offering that up as a purpose for decades. From the NFIB Report:

– Merchant Processing Resource

../../

Do You Work in The Merchant Cash Advance Industry?

March 28, 2012It’s a good time to be employed in the Merchant Cash Advance industry. Without doing any formal research on the sweeteners being offered to agents, we frequently see some of the enticing ads:

Share in the Profits!

Get an iPad!

Work with a TRUE DIRECT FUNDER

and so on…

But forget the iPad boys and girls because you can go to the freaking olympics! Someone forwarded us this advertisement from Infinity Capital Funding which apparently is offering anyone that funds over $125,000 in deals through April 30th, two tickets to the 2012 London Olympics, free flights, hotel, $2,000 in cash, and a VIP helicopter tour. We’re inclined to believe that funding 125k will enter you into a raffle to win this package considering medium-sized ISOs could surpass that target with no sweat. Hopefully this plug reaches Infinity and they can clarify this for us.

The last time we saw a sales prize on that scale was in August 2009, when 1st Merchant Funding was offering a free Mini Cooper to any ISO that funded more than $1 million with them in the span of 120 days. Nobody ended up getting the car.

But not everyone in this business is an agent. There are countless underwriters, portfolio managers, secretaries, assistants, callers, bookkeepers, and other individuals that drive this industry day in and day out. It’s important work and we salute you. That doesn’t stop the account managers, sales representatives, and brokers from getting all the attention though. So what IS IT that these brokers do anyway? It depends on who you ask…

This image was created by the staff of Entrust Cash Advance, a veteran Merchant Cash Advance firm in New York City. They’ve been in the industry since 2007 and from what we gather by the image, they’ve got it figured out.

AltFinanceDaily would like to hear more from companies about any incentives, rewards, and prizes you’re offering. Send any information regarding this to webmaster@merchantprocessingresource.com

– AltFinanceDaily

../../

Does Your Mom Sell Merchant Cash Advance?

February 4, 2012Five years ago, everyone seemed to add the phrase, “but I also do mortgages on the side” in response to questions about their career.

“I’m a stockbroker, but I also do mortgages on the side.”

“I’m a school teacher, but I also do mortgages on the side.”

“I’m a stay at home mom and a loving wife, but I also do mortgages on the side.”

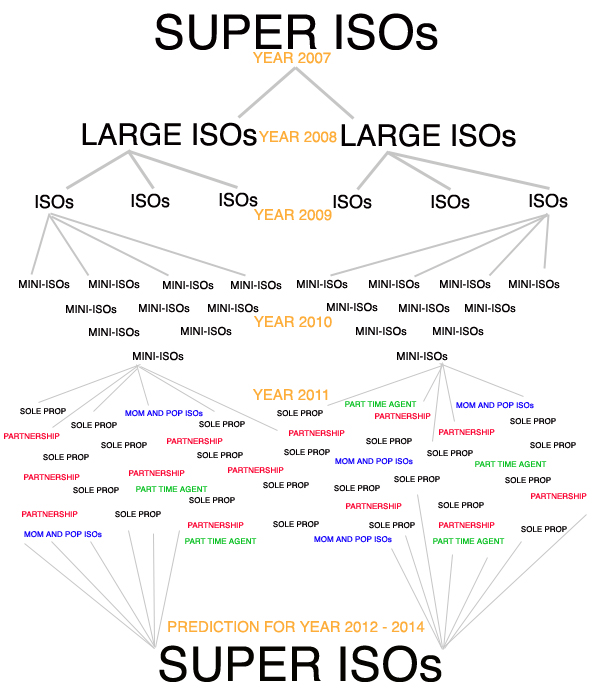

Times have changed and today the new side gig is reselling Merchant Cash Advance (MCA), at least in the New York metropolitan area. The Independent Sales Office (ISO) model is dissipating into a few thousand sole proprietors, all of whom are competing for the same prospects. Most of them started at one of the larger ISOs or funding sources and have over time traded it for the opportunity to work for themselves. Others have pushed it aside as a part time gig while earning a living in another line of work.

It’s encouraging to see that the entrepreneurial spirit is alive and well in the city that never sleeps, but riding solo has its disadvantages. For instance, marketing budgets are more constricted. This inhibits the ability to attract clients, especially when competing against a sizable ISO, who likely has thirty times more to spend on advertising, systems, and service.

It’s encouraging to see that the entrepreneurial spirit is alive and well in the city that never sleeps, but riding solo has its disadvantages. For instance, marketing budgets are more constricted. This inhibits the ability to attract clients, especially when competing against a sizable ISO, who likely has thirty times more to spend on advertising, systems, and service.

And yet, I haven’t heard many complaints from independent agents, which may mean the MCA industry is far from over-saturated. Sixteen of my former co-workers have gone on to start their own MCA ISOs. I even know a pair of twin brothers that run ISOs independent of each other. Some of these newly formed mini-ISOs (less than five people) break apart and each member seems to go on and repeat the cycle.

The Derailing of the Shakeout

In early 2008, it was predicted that low budget marketing would cause a massive shakeout of MCA resellers. David Goldin, the CEO of AmeriMerchant published the following in his blog:

There is another train of thought that is inevitable to fail – those that thought they can sell business cash advances with minimal capital expenditure, meaning hiring unqualified salespeople using inexpensive marketing techniques such as voice broadcasting (with these providers giving the same data to 100s of phone rooms) to dial hundreds of thousands of businessses an hour with a prerecorded message. (Merchants around the country are getting 3 – 5 prerecorded calls a day). The challenge is the quality of anyone that is going to press ‘2’ on their phone for money tends to be “lower hanging fruit” and lower quality deals. With the recent credit crunch and many merchant cash advance funding companies tightening up, some merchant cash advance agents were seeing approval rates as low as 15%-20%. There is no way they can survive and stay in business with that kind of approval rate.

Back then, it was quite popular to have a hundred sales agents in a single room making phone calls. Overhead was the biggest part of the budget, which in places like New York City, could consist of tens of thousands of dollars in rent alone. Add that to all the money that was spent on technology, payroll, dialers, and commissions, and it became really easy to generate a net loss.

With the emergence of mini-ISOs, many are foregoing traditional overhead expenditures such as the renting of a centralized office. Technology costs are also being eliminated since most people already own a personal computer and a cell phone, the only two tools really necessary to interact with prospects. As for state of the art auto dialers? Well, many agents are completely fine using inexpensive resources such as phone books or public UCC filings. Ask around in the MCA industry and you’ll learn just how prevalent this practice is.

There are so few barriers to entry in the MCA industry, that it catches a lot of folks from other financial fields off guard. We receive a dozen e-mails a month from mortgage brokers, stockbrokers, and insurance agents asking what licensing requirements they will need to sell MCA. There are none of course, but they more are shocked to learn that there are no regulations to abide by either. Take your cell phone, throw in your e-mail, spend twenty bucks on a website and you’re an official MCA reseller! It’s just that easy. Thousands of people are getting in on it.

Who is Who?

The flood of resellers and fly-by-night agents is making it increasingly difficult to know where all the MCA money is actually coming from. Here on the Merchant Processing Resource’s website, we’ve created transparency by listing the largest direct funding providers. Need to know if that UCC filing is MCA related? We can help you with that too.

We’re also working on creating an official directory of resellers, for which there will be some requirements for inclusion. That means if you’ve e-mailed us on this topic already and you haven’t heard from us yet, be patient. You will be contacted soon with instructions on how to become an approved MCA reseller.

Consolidation

In the meantime, the increasing fragmentation also presents an incredible buying opportunity. Large ISOs that are looking to add to their portfolios and leverage the brand names that mini-ISOs have created should be able to buy them out at very affordable prices. When this practice starts to happen, it’ll be interesting to see what the market value of mini-ISOs are. Could a business owned by two individuals with a pool of two hundred clients be worth $50,000? $100,000? $300,000? Once someone sets the bar, we should prepare for a year of consolidation, and the little guys will get gobbled up by the big ones. A lot of folks could end up walking away very rich or disappointed. Perhaps now is a good time for your Mother to go into the MCA business for herself and flip the value created for a nice profit a year from now.

ISOs on Steroids

The popularity of co-funding or syndication is also allowing the remaining large ISOs to really flex their muscles in a way they weren’t able to in 2008. Syndication is where an ISO is able to invest their own capital in the MCA deals they close. For instance, on an advance of $20,000, $15,000 of it might come from the MCA funding source, and the remaining $5,000 from the ISO themselves. As long as these accounts perform well, syndicating can create a supernatural rate of growth. This further whets the appetite for opportunities to expand.

So why are mini-ISOs a buying opportunity? Customer loyalty is something big companies can’t always shake, no matter how much is spent courting them. Furthermore, these mini-ISOs tend to have historical performance records on their clients, data that is incredibly valuable. Should a Super ISO invest $20,000 in a small business that has never used MCA before or should they invest it in a business that has responsibly used MCA for two years with no issues, exhibits fierce loyalty, and has a proven record of success? The opportunity to participate in funding that business now and repeated times in the future should be worth a lot.

The Unknown

There are other forces at work that may reshape the industry in a way we can’t predict. The incredible rise of micro-lending is cannibalizing the MCA market, but is also allowing ISOs to offer a variety of financial products to a larger pool of businesses. One New York City MCA funding source privately revealed that micro-loans now make up 80% of their monthly funding volume, a stunning shift from their MCA-only portfolio of 2010.

The growing popularity has also caught the attention of regulators and in some states, the purchase of future credit card receivables is being governed by existing lending laws. The day may come when every agent needs a license to sell, but until then, thousands of people are playing the biggest game in town, helping small businesses get funding to grow. Are you a part of it?

– AltFinanceDaily

../../

The Stigma of Merchant Cash Advance?

September 6, 2011Bankcard Funding, a Long Island based Merchant Cash Advance (MCA) provider, recently blogged about the “stigma” of Merchant Cash Advance. While we don’t deny that there is one, we don’t agree with their basis for it.

To quote them:

“Many people do not believe that a merchant cash advance is a legitimate type of financing. This is because many merchant cash advance companies take advantage of naïve clients who are uneducated in the process, take them for a ride, and then focus on the next“sucker.” NOTE: As of 9/13, we noticed that they have updated their article and the above quote no longer appears.

This is a weak argument, especially since it inflames the target market’s concerns. If you market your company by claiming everyone in the industry is a scam artist except yourself, you’re not going to reassure your prospects. But Bankcard Funding is not alone in their assessment so maybe they’re on to something. We’ve heard similar rhetoric in private groups on LinkedIn where seasoned professionals vented their frustrations. Some of the anonymous comments include:

This guy is screwing it up for me!

This guy is screwing it up for me!

It seems too many industry professionals are casting the blame on malevolent third parties. If the competition was as evil as you think, then your work should be cut out for you. Business owners are intelligent people. That’s why they’ve managed to successfully work for themselves. If given the choice between a malicious salesman and an honest one or a good deal and a bad deal, they’re inclined to go with the honest guy with the good deal.

The point being… If you feel that you are losing prospects because the competition is muddying up the industry’s reputation, you simply need to sell better. If the few evildoers (and there’s a bunch in every industry) are defining the industry itself, then it’s time to rethink your marketing strategy. The companies with the highest rates and the nonsensical fees shouldn’t be beating you. If anything, they should be making it easier for you to grow.

So the good guys have a marketing problem and it’s about time we addressed that…again. Reread The Colossal Marketing Failure of the Merchant Cash Advance Industry in which we highlight some of the problems in advertising.

Some people have asked us about the purpose of the erotic photos we used in it. Why did you notice them? Did they stand out? Did you think about what the point of it was? If it got you wondering at all, then we did our job. Junk mail and cold calls don’t get your prospects to think about anything.

If we are to redefine the image of the industry, then the vehicle in which the message is delivered needs to change. Big financial firms like Bank of America have so many businesses applying for loans, that they can barely keep up with the demand. That’s the way it should be for MCA providers, especially given the state of the economy.

The only people claiming there’s a stigma are the ones selling the product. Guess what? That’s not a winning strategy…