Stolen Deals? How One Funder Used Technology to Say ‘No More’

March 14, 2017 It’s another chapter in the saga of stolen deals, a problem that shops all over the country seem to be grappling with. For Miami-based Greenbox Capital, company CEO Jordan Fein hoped it was something that they didn’t have to worry about. But believing it was better to be safe than sorry, Greenbox launched a 90-day probe to review all controls and personnel to see if theft existed in their organization and how it was being done. They weren’t too happy with the results, which determined that there was indeed employee theft taking place.

It’s another chapter in the saga of stolen deals, a problem that shops all over the country seem to be grappling with. For Miami-based Greenbox Capital, company CEO Jordan Fein hoped it was something that they didn’t have to worry about. But believing it was better to be safe than sorry, Greenbox launched a 90-day probe to review all controls and personnel to see if theft existed in their organization and how it was being done. They weren’t too happy with the results, which determined that there was indeed employee theft taking place.

Sources across the industry have told AltFinanceDaily that some employees will do things that make it easy to catch them, while others say that their tactics are constantly evolving. Disabling the USB ports isn’t enough, they say, since personal smart phones can be used to covertly steal data by simply taking pictures of a computer screen. Some say that apps like Snapchat are even making it increasingly easy for them to erase the evidence trail.

For Greenbox Capital, the probe convinced them that being a funding company meant they also needed to become a top-notch security company, especially since they are being entrusted with sensitive information. It’s their ISOs’ deals they have to protect, they say. Understanding how important that is, the company designed proprietary software to monitor the actions of all users on their system, which allows them to know who clicked on what when, and for how long. But that wasn’t enough, they insist. They also developed algorithms to detect suspicious behavior and their security team receives an alert whenever it gets triggered.

And it’s not just what someone clicked on or downloaded, they say, since their system also analyzes phone call activity, texting activity, wifi activity and the number of absences from one’s desk. The implication from that, of course, is that they must be incorporating video surveillance, which they confirmed they are.

They’re not alone. Chad Otar, CEO of Excel Capital Management, an ISO based in New York City, says that when it comes to their office, they have “eyes and ears everywhere.” Otar explains that because commission payouts can be so high, even experienced salespeople can feel tempted to risk their jobs to get their hands on good leads. Some will try to use different emails accounts on the office computer, using their private ones to transact information they’re not supposed to. To prevent that, they’re using Google Vault. “It allows us to monitor all emails going out and coming in from everyone’s account that is linked to the server,” he explains. “And if they try to access another email account, it blocks them.”

But even while threats like Snapchat exist, Otar says some employees will take a low-tech approach and hide valuable information in the trash bin and then offer or attempt to “take out the trash.”

For Greenbox, thanks to their new platform, they were actually able to catch two employees who were stealing data and actually selling deals on the black market.

A black market?

A black market?

To put such behavior in perspective, 3 years ago, the name and phone number for someone qualified and interested in working capital could fetch $200 through normal lead channels. These days, sources say it can cost several thousand dollars in marketing just to fund a single deal and that a good lead is worth more than gold.

Greenbox believes that all companies should stop and take a close look at the controls they have in place to catch internal theft. Determined to prevent what they found from ever happening again, they say they now have the tightest internal controls in the industry and advise all businesses to rethink their approach to data security. “As it stands today there is no safer place to send your deals,” company CEO Jordan Fein says.

Of note, readers should stand to realize that getting caught might not just mean embarrassment or termination. Last year, a former MCA sales rep pled guilty to attempted criminal possession of computer related material for being on the receiving end of stolen deal information and using it. Since then, other companies have privately suggested that this was not the only deal-stealing situation that has involved law enforcement and that data theft is a serious offense.

Excel Capital Management‘s Otar says that if you create a sense of pride and loyalty in your workplace, your own employees will report any bad behavior they witness to you.

For Greenbox Capital, they believe their cloud-based system and advanced algorithm is not just about funding more deals, it’s about protecting the integrity of the entire process and maintaining trust.

Stealing deals? it’s not worth the risk.

In Canada, Alternative Business Finance Industry Similar, Yet Different

March 8, 2017 David Gens believes the top 3 alternative small business finance players in Canada are funding between $15 million and $20 million to small businesses a month combined. That’s a small market compared to the US, where the top 3 companies are funding close to a half billion dollars per month. Gens, who has a background in private equity, is the founder, president and CEO of Merchant Advance Capital, a company with around 40 employees in offices in Toronto and Vancouver.

David Gens believes the top 3 alternative small business finance players in Canada are funding between $15 million and $20 million to small businesses a month combined. That’s a small market compared to the US, where the top 3 companies are funding close to a half billion dollars per month. Gens, who has a background in private equity, is the founder, president and CEO of Merchant Advance Capital, a company with around 40 employees in offices in Toronto and Vancouver.

“We don’t view ourselves as directly competing with banks,” Gens says, suggesting that his target market is less than prime. It’s a point that his counterparts in the US have made often. But there’s a slight difference with that approach in their market, he adds. “Most Canadian consumers are prime.” And unlike the US, the banks are not necessarily portrayed as the enemy in Canada where five major ones dominate the market.

“It’s exceptionally difficult for an alternative small business lender to build a brand,” said Jeff Mitelman, CEO of Montreal-based Thinking Capital, on a panel at the LendIt Conference. Despite that, his company has funded half a billion dollars to 15,000 unique businesses over the last 10 years. A panelist besides him half-joked however, that there is such an inherent conservatism with Canadian small business owners that some don’t even want to grow and are content with running lifestyle businesses.

But of the deals that are getting done, they’re often acquired through direct marketing. “The ISO market is not like it is in the US,” Gens says. “There’s just a handful of them.” Where there are ISOs though, competitive pressures usually follow. He says that they’re competing on at least 50% of the deals they work on, in part because of these ISOs. Stacking is happening in Canada too, he admits. “It’s not as crazy as it is in the states,” he contends. “Philosophically, it doesn’t align with our business.”

Some deals in Canada are actually being facilitated by US ISOs, he acknowledges, before clarifying that they should be aware that they will get paid in Canadian dollars, which at present are worth about a three quarters of an American dollar. They are in a different country after all.

Gens and others like Bruce Marshall, vice president of British Columbia-based Company Capital, agree that OnDeck’s push into Canada has been good for the entire industry. Six months ago, Marshall said, “We are happy that some of the bigger US players are coming up here and they are spending millions of dollars on advertising. These companies raise awareness of the industry to a higher level and with us being a smaller company, we can ride on their coattails.”

Over time, they believe alternatives will become more mainstream. For Gens, part of that is about doing right by the customer. “We pride ourselves on being very transparent,” he says. There are no hidden fees with their products and they can make things easy like use APIs to access a merchant’s bank statement history, provided an applicant wants to do it that way. “More than 50% of merchants are still submitting bank statements,” he says. That trend is still pretty much true in the US as well. “There’s a much lower incidence of fraud in Canada,” he asserts. It’s a nation of small businesses he’s content to serve.

Innovative Lending Platform Association and Coalition for Responsible Business Finance Join Forces

March 5, 2017NEW YORK, Early Release — The Innovative Lending Platform Association (ILPA) and the Coalition for Responsible Business Finance (CRBF) today announced they are joining forces and will now operate as the ILPA – the leading trade organization representing a diverse group of online lending and service companies serving small businesses. Joining ILPA’s existing members, OnDeck® (NYSE: ONDK), Kabbage® and CAN Capital, are CRBF member companies Breakout Capital, Enova International’s (NYSE: ENVA) The Business Backer™, PayNet and Orion First Financial. United by a shared commitment to the health and success of small businesses in America, the newly expanded ILPA is dedicated to advancing best practices and standards that support responsible innovation and access to capital for small businesses.

In addition, leading national small business organizations that formerly served as the CRBF Advisory Board will now represent small business customers as formal advisors to the ILPA. The Advisory Board includes individuals from the National Federation of Independent Business (NFIB), the National Small Business Association (NSBA), the Small Business & Entrepreneurship Council (SBE Council), the U.S. Chamber of Commerce, and new representatives from the Association for Enterprise Opportunity (AEO). These small business organizations have provided key input into the collective group’s best practices and standards initiatives over the past year, ensuring that the needs of their small business constituents are addressed.

The expanded ILPA remains committed to advancing online small business lending education, advocacy and best practices. In October, the ILPA introduced the SMART Box™ (Straightforward Metrics Around Rate and Total cost), a first-of-its-kind model pricing disclosure and comparison tool launched in partnership with the AEO. The SMART Box is focused on empowering small businesses to better assess and compare finance options and is now available for broader adoption by lending platforms. More details can be found at: http://innovativelending.org/smart-box/

As a leading voice for responsible business funding, CRBF launched in January 2016 with the mission to create a concrete code of ethics for the industry and to educate policymakers on the value of non-bank small business financing. The organization outlined responsible and transparent business practices for both providers as well as customers, and the expanded ILPA has leveraged that work to formulate an updated industry Code of Ethics that will guide the ILPA moving forward.

The expansion of the ILPA follows a period of broad stakeholder engagement and a demonstrated shared commitment to serving small businesses. With this unification, the cross-industry effort to bring innovative and responsible solutions to improve access to capital for Main Street small businesses continues to gain momentum.

“Fostering responsible innovation and empowering small businesses to better assess and compare finance options are priorities for the ILPA. We are delighted to join forces with the CRBF as we work together to advance small business online lending education, advocacy and best practices,” said Noah Breslow, Chief Executive Officer, OnDeck. “We are proud to be part of this growing cross-sector effort to help improve capital access on behalf of small businesses across the United States.”

“The combination of these leading organizations represents a landmark moment in the industry, signifying how major players in the small business lending space are increasingly aligned on values and best practices that benefit small businesses,” said Carl Fairbank, founder and chief executive officer, Breakout Capital. “Founded on the fundamental principles of responsible lending, education and transparency, Breakout Capital is thrilled to partner with other premier players in the industry who share our vision and believe that a unified industry voice can promote small business success more effectively. “As a founding member company of CRBF, The Business Backer is thrilled with the merger between the CRBF and the ILPA,” said Jim Salters, president of The Business Backer and CRBF Advisory Board member. “The move creates an even larger platform of industry leaders with a common voice to help ensure small businesses have access to honest and transparent funding sources.”

“The ILPA was launched as a self-regulatory exercise and is focused on empowering small businesses with clear and transparent ways to compare financing options,” said Rob Frohwein, co-founder and chief executive officer of Kabbage. “Kabbage and the ILPA are excited to join with the CRBF in order to advance ubiquitous industry standards. Together, we are eager to continue working with regulators and policymakers to expand small businesses’ ability to easily access technology-driven financing products.”

“Access to capital is a high priority for America’s small businesses. As our economy grows, small business owners need diverse sources of capital to hire new employees and expand their businesses. The U.S. Chamber of Commerce applauds the innovative capital providers in the ILPA for their dedication to fueling growth on Main Street,” said Tom Sullivan, vice president, small business, U.S. Chamber of Commerce.

“CAN Capital has been a supporter of transparency throughout our 19 year history, and we are excited to see the ILPA expand as it continues to support small business owners,” said Parris Sanz, chief executive officer of CAN Capital.

“Small business lending continues to be stubbornly elusive for many small firms and what we need is not just more lending, but better lending options,” said Todd McCracken, National Small Business Association president and chief executive officer. “This merger will expand on efforts to connect small business with a variety of fair and responsible lending resources.”

“We are excited to be part of an organization whose purpose is to create a vibrant, healthy, small business lending marketplace that serves the engine of the U.S. economy – small businesses,” said David Schaefer, chief executive officer of Orion First Financial. “As a loan servicer to small business lenders, we are particularly enthusiastic that the ILPA is embracing a diverse membership and participation from small business associations through its Advisory Board.”

“SBE Council looks forward to partnering with the expanded ILPA to continue advocating for the innovative and responsible sources of funding to which entrepreneurs and small businesses need access,” said Karen Kerrigan, president and chief executive officer of the Small Business & Entrepreneurship Council.

“It is critical that these and other responsible lenders come together to advance initiatives like SMART Box,” said Connie Evans, president/chief executive officer of the Association for Enterprise Opportunity. “The time is ripe for united voices and action to give more people the opportunity and the tools to realize a brighter future for their businesses.”

Together, the members of the expanded ILPA have provided access to more than $14 billion dollars in capital to small businesses to help drive growth and hiring.

I Got Funded, OMG I’m a Merchant!

March 3, 2017 I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced AltFinanceDaily’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, AltFinanceDaily is truly a small business first.

I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced AltFinanceDaily’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, AltFinanceDaily is truly a small business first.

Independently owned, there are no investors in the company to turn to for assistance. And that’s not such a bad thing if you know at all what it can be like to have partners. At the end of last year, we did what hundreds of thousands of small businesses around the country have done, we got funded by a marketplace lender. Through that experience, I found myself wearing a brand new hat, one that says “merchant” on it.

On December 1st, my company received a deposit for $35,000. It was a loan from Square Capital and I didn’t pursue it for a story, but rather to facilitate cash flow at the busiest time of the year. I was moving into a larger office on the same floor of our building and the hustle and bustle of the pre-holiday craze was upon us. The circumstances may come off a bit cliché, simulated even, but there it was at the right time and the right place, an email telling me that my business had been “selected.” If you’ve ever wondered if that kind of marketing works, it must, because a half hour after reading through the materials, I made an educated decision and applied for a loan.

The higher-ups at Square Capital, those above the underwriting department, might have no idea that they even funded us (our legal name is different from our trademark publication name). And I haven’t reached out to them for comment because I didn’t want to turn this into a PR stunt or get them riled up about my account. But if you work at Square and you’re reading this now, you don’t need to hold your breath. Everything seemed to work just as the press releases, ads, and executives claim it does. Phew! That’s good for you, but it was also very good for me.

The most pleasant surprise was that our business got approved for the maximum amount advertised in their email. Here’s how it went down:

11/29/16

1:34 PM

Received email offering a business loan up to $35,000 to repay over 12 months

2:01 PM

Applied for $35,000, which consisted of logging into my Square account and tapping a button

8:02 PM

Got approved for $35,000

11/30/16

Square sent out the funds via ACH

12/1/16

Received full loan deposit in my business bank account

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

As a small business owner, I calculated whether or not it made sense to pay a set fee for $35,000 over that time period and determined it did. An APR would not have impacted my decision, nor would I really have found it helpful in determining the supposed true cost. The true cost is already there in black and white, the total dollars I agreed to pay.

Two things guided me, speed and economics. I wasn’t motivated to shop around to try and get the absolute best deal, just one that made economic sense with the least amount of work in the shortest amount of time. It sounds ironic to write that, especially as someone who has a bachelor’s in both Accounting and Finance but if you’re someone who works 7 days a week like I do, well maybe you’d understand my thought process. If I was applying for a million bucks, then yes, I’d shop and think on it pretty hard, but in my circumstances, a few thousand dollars in fees is relatively small stakes for the company. Besides, I was using the money proactively, as a positive tool.

I knew my patience for waiting was thin. For example, an experience with one of my banks earlier in the year had already left me rattled. I had asked to extend the limit of a business credit card and I was told that in order to do so, I’d have to visit the bank branch where I had originally signed up for the card (I don’t even live near that branch anymore) and that I would have to bring financial statements with me to present for review. By the way, this was for a limit increase to an amount that was much less than $35,000.

I learned that day that the rumors about (some) banks are true. They wanted me to visit a branch… and bring paperwork… for some kind of unspecified analysis… in 2016. Lo and behold I never showed up, and was more entrenched in my belief than ever before that the world needed to become de-banked and soon.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

Alas, the entire process really all just came down to clicking a button online. I kept waiting for the catch, for them to let me down, to come up short of all the promises that the Fintech revolution has made about changing the world, but it never happened. A month later, Square withdrew their first payment from our account. Like I said earlier, I was satisfied with the entire process and it was a big help. Had I been given the option however, I might’ve opted to structure the arrangement differently and sold a portion of our future sales proceeds rather than simply borrow money. Allow me to explain.

It’s entirely possible that the next 12 months of business won’t pan out the way I project. If my sales drop, I still have to make the fixed monthly payment in accordance with my loan terms regardless. Not so when selling future sales since the delivery of those funds to the buyer is entirely tied to actual sales activity. A structure like this, what many consider a merchant cash advance, is actually what Square used to offer up until early 2016.

When the pace of sales slow down, delivery of the sales proceeds slows with it. When the pace of sales increases, so too does the delivery to the buyer. And if I went out of business, well then the buyer would get what they purchased, nothing.

Merchant cash advances are harder to bundle up and securitize though because there are no maturity dates nor is there even a guarantee the buyer will get what they purchased in full. They’re investments with loads of uncertainty built in for the buyer, and that’s probably why Square switched to loans and also probably why the cost of my loan was relatively inexpensive. They’ve minimized the uncertainties.

Nonetheless, the loan I ultimately got, is just fine. In the moment that I needed it, the process couldn’t have been any simpler or any faster. The banks have met their match. I got funded and loved it, now it’s your turn.

Prosper Marketplace Closes Loan Purchase Agreement for up to $5 Billion of Loans with Consortium of Institutional Investors

February 27, 2017SAN FRANCISCO–(BUSINESS WIRE)–Prosper Marketplace, a leading online consumer lending marketplace, today announced that it has closed a deal with a consortium of institutional investors to purchase up to $5 billion worth of loans through the Prosper platform over the next 24 months. The investors in the consortium are affiliates of each of New Residential Investment Corp., Jefferies Group LLC and Third Point LLC, and an entity of which Soros Fund Management LLC serves as principal investment manager. The consortium will also earn an equity stake in the company based on the amount of loans purchased, further aligning the group with Prosper’s future growth and success. Warehouse financing of up to $1 billion will be provided by a syndicate of lenders including Credit Suisse, Deutsche Bank, Goldman Sachs and Morgan Stanley.

“We’re very pleased to be working with this consortium of investors, and believe they will be great long-term partners as we continue to build a large-scale business,” said David Kimball, CEO, Prosper Marketplace. “This deal gives us the funding stability and additional capital markets expertise we need to continue to grow our marketplace and achieve profitability in 2017.”

Prosper has maintained positive momentum since the second half of 2016, with monthly loan originations growing steadily since July. In addition, the Prosper loan portfolio is delivering solid returns to its institutional and individual investors, with an estimated net return of 7.86%<> for January 2017. Prosper continues to diversify its investor base, and is focused on bringing new banks and other institutional investors onto the platform.

Financial Technology Partners (FT Partners) served as strategic advisor to Prosper Marketplace and its Board of Directors on this transaction. DV01 will be the loan data agent to the consortium.

About Prosper Marketplace

Prosper’s mission is to advance financial well-being. The company’s online lending platform connects people who want to borrow money with individuals and institutions that want to invest in consumer credit. Borrowers get access to affordable fixed-rate, fixed-term personal loans, and investors have the opportunity to earn attractive returns via a data-driven underwriting model. To date, over $8 billion in personal loans have been originated through the Prosper platform for debt consolidation and large purchases such as home improvement projects, medical expenses and special occasions.

Prosper launched in 2006 and is headquartered in San Francisco. The lending platform is owned by Prosper Funding LLC, a subsidiary of Prosper Marketplace. Loans originated through the Prosper marketplace are made by WebBank, member FDIC. Visit www.prosper.com and follow @Prosperloans to learn more. Prosper notes offered by Prospectus.

1 Estimated return on January 2017 production is 7.86% according to the Prosper Performance Update: January 2017

Contacts

Prosper Marketplace:

Sarah Cain, 415-593-5474

scain@prosper.com

Confidence Stable For Small Business Lenders and MCA Companies

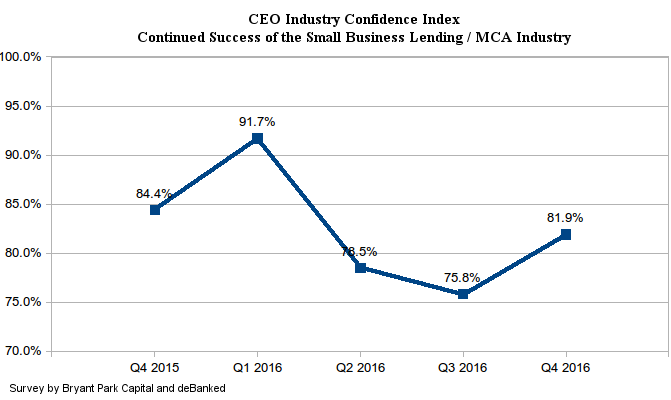

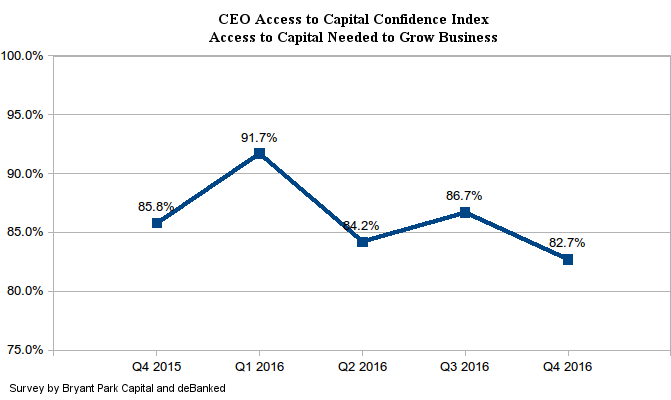

February 26, 2017Recent events may be putting a slight damper on the confidence of industry CEOs in being able to access capital needed to grow their businesses, but continued success of the industry in general is ticking back up. This data is according to the latest survey conducted by Bryant Park Capital and AltFinanceDaily of small business lending and merchant cash advance company CEOs.

Confidence in the industry’s continued success bumped back up to 81.9% in Q4, while confidence in being able to access capital reached its lowest level since the survey’s inception. Still, at 82.7%, it’s high.

In late November of 2016, CAN Capital, one of the industry’s largest companies, encountered problems that caused the company to suspend funding. Several of their competitors since then have reported a boost in submission volume, which they partially attributed to that event.

Pressure on companies to merge or exit the market may also be kindling optimism for larger players who stand to gain market share.

Catching Up With Marketplace Lending – A Timeline

February 20, 2017This is the expanded update to the timeline of events taking place in the industry.

12/16 Chicago-based Argon Credit filed for bankruptcy

12/20 Bizfi announced that it had surpassed $2 billion in originations since inception

1/4 Strategic Funding integrated US operations of Capify

1/9 Two US Senators protested the OCC’s plans to create a limited fintech charter

1/11 Funding Circle announced a new $100 million equity round led by Accel

1/12 Marketplace Lending Association announced 11 new members

1/16

- The WSJ broke a story revealing that CAN Capital had breached its covenants with its big-bank creditors, laid off about 250 staffers, hired a restructuring firm for assistance in negotiating with creditors, and hired Jefferies Group for advice on strategic alternatives

- NY proposed broad changes to its lender licensing laws

1/17

- OnDeck announced a partnership with Wex, a provider of corporate and small business payment solutions

- New York Department of Financial Services protested the OCC’s plans to create a limited fintech charter

1/18 Credible raised $10 million in a Series B round from investors that included Ron Suber, the president of Prosper Marketplace.

1/19

- LendIt announced finalists of its first ever industry awards

- Sean Murray of AltFinanceDaily selected as a finalist for Best Journalist Coverage

1/20

- Fifth Third announced a partnership with QED Investors to advance fintech strategy

- President Trump issued an executive order freezing all new regulations

1/25 loanDepot surpassed $100 billion in loans

1/26 LendingRobot launched a marketplace lending hedge fund

1/30 Prosper Marketplace’s EVP of capital markets, Eric Thaller, departed from the company

2/1 Prosper Marketplace appointed new CFO, Usama Ashraf

2/4 OnDeck announced departure of COO James Hobson

2/8

- Breakout Capital announced a $25 million credit facility

- Lendio announced that it had facilitated $240 million in funding last year

2/13 OnDeck announced a partnership with payroll company Wave

2/14 Lending Club reported a $146 million loss for the year and an increase in bank funding

2/16

- OnDeck reported a $86 million loss for the year, layoffs

- The DC circuit decided to rehear the PHH v CFPB case

Legal Battles to Keep an Eye On

February 18, 2017CFPB

The CFPB’s organizational structure might not be unconstitutional after all. The D.C. Circuit which originally concluded it was unconstitutional, has decided to rehear the case. Oral arguments on the matter are scheduled to take place on May 24, 2017. A detailed summary of the issues can be found on The National Law Review.

TCPA law

Serial litigant Craig Cunningham is one of two petitioners behind the challenge to an FCC interpretation of what constitutes “prior express consent.” Specifically, the petitioners want to get rid of implied consent resulting from a party’s providing a telephone number to the caller. The FCC has called upon the public to comment. If the FCC indeed decides to narrow the scope of their interpretation, it would become easier for litigants like Cunningham to bring lawsuits. Read a longer brief of the issue here.

New York Lending License

Governor Cuomo’s budget proposal contains changes to Section 340 of New York’s banking law and it has the potential to completely change the alternative landscape in the state. Read a full analysis here.

Platinum Rapid Funding Group Ltd v VIP Limousine Services Inc. and Charles Cotton

After a landmark trial court decision surrounding merchant cash advance last year, plaintiff Platinum Rapid Funding Group went on to obtain a judgment against defendants in an amount exceeding $100,000. However, filed papers on the docket show the case may be heading to the Appellate Division.

Merchant Funding Services, LLC v. Volunteer Pharmacy Inc

Merchant cash advance companies may find themselves having to answer for an unfavorable ruling issued in Westchester County, New York, in which a judge vacated a Confession of Judgment and voided the underlying future receivables transaction. A more in-depth brief can be read here. Notably, the judge in that decision was the same one that decided Pearl Capital Rivis Ventures, LLC v. RDN Construction, Inc.