OnDeck Q3 Earnings Report Shows Positive Signs (ONDK)

November 2, 2015 Back when OnDeck was telling analysts that they were focusing on growth, critics said they should be focusing on profitability. Now that they’ve had their second straight profitable quarter, critics are pointing out that loan origination growth has slowed. OnDeck can’t win with them, but this quarter’s results were the closest they’ve come to proving themselves.

Back when OnDeck was telling analysts that they were focusing on growth, critics said they should be focusing on profitability. Now that they’ve had their second straight profitable quarter, critics are pointing out that loan origination growth has slowed. OnDeck can’t win with them, but this quarter’s results were the closest they’ve come to proving themselves.

They originated a little over $482 million worth of loans and reported a profit of $3.7 million. Selling loans through their marketplace to institutional investors is generating immediate income and creating the profits they lacked before.

The reliance on funding advisors (ISOs/brokers) shrank from 20.6% in Q2 to 18.6% in Q3. During the Q&A session, OnDeck CEO Noah Breslow hinted that they may have reached a floor in that ratio. That channel could stabilize and even grow a little bit, he said.

When one analyst asked whether or not loan aggregation platforms were counted under funding advisors or strategic partners, Breslow said they are counted as strategic partners. Only 4% of OnDeck’s loans come from these loan aggregation platforms, the company’s execs admitted, putting to bed any notion that loan aggregators had leverage over OnDeck’s business.

In Q2, analysts became alarmed over the competitiveness of the direct mail channel. This time around, Breslow said the environment hasn’t gotten more or less competitive, that it was about the same. Competition is stabilizing and the advantage goes to the scaled players, he argued after describing their ability to target, analyze, underwrite and fund faster than others. Breslow added that they are not banking on relief from the competition to carry out their long term objectives.

A sentiment discussed on the call but not exactly argued by anyone is that it’s become pretty late in the game for new lenders to start entering the field, the implication being that the long-term competition is already in business, instead of it being some new companies that have yet to form.

The regulatory environment was described by OnDeck as “stable.”

All in all, the results of Q3 were optimistic.

The Industry’s First Small Business Financing Report Revealed

October 25, 2015AltFinanceDaily teamed up with Bryant Park Capital, an investment bank providing M&A and corporate finance advisory services to emerging growth and middle market public and private companies, to conduct the industry’s first comprehensive report.

Our initial findings are drawn from a survey of twenty-seven C-level participants, whose companies primarily offer merchant cash advances and small business loans. Combined, the participants represent more than $1.9 billion in annual origination volume. The survey was sent to over one-hundred eligible respondents, with participation open to all of them equally and included both direct funders and brokers.

- Thirteen respondents reported being on pace to originate $50 million or more in 2015.

- Seven respondents reported being on pace to originate $100 million or more in 2015.

Analyzing the origination volume of participants over a three-year period, the industry was determined to have a:

Compound Annual Growth Rate of 56%.

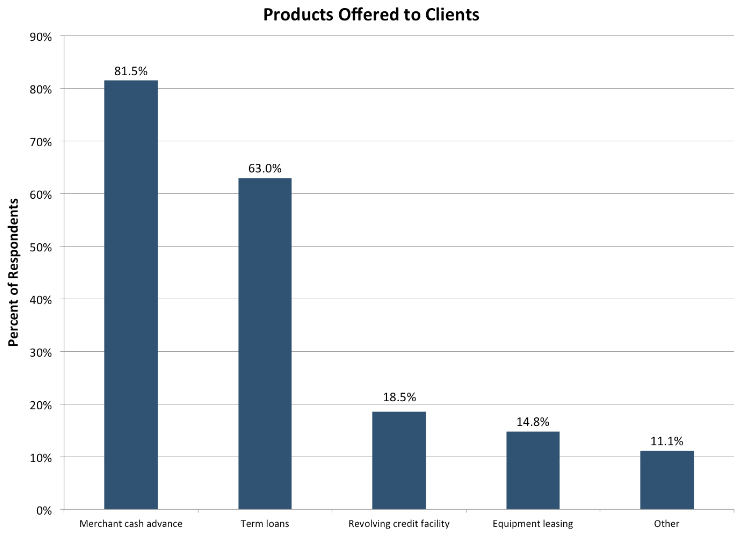

THE INDUSTRY HAS A DIVERSIFIED PRODUCT MIX

Respondents revealed a diversified product mix beyond merchant cash advance. Five participants actually reported originating no merchant cash advances at all and instead offered term loans or other products.

THE INDUSTRY CEOS HAVE A CONFIDENCE INDEX OF 83.7

Based on responses from CEO/participants asked to give their confidence level in the continued success of the small business lending/MCA industry over the next 12 months on a scale of 0–100, with 100 being the highest.

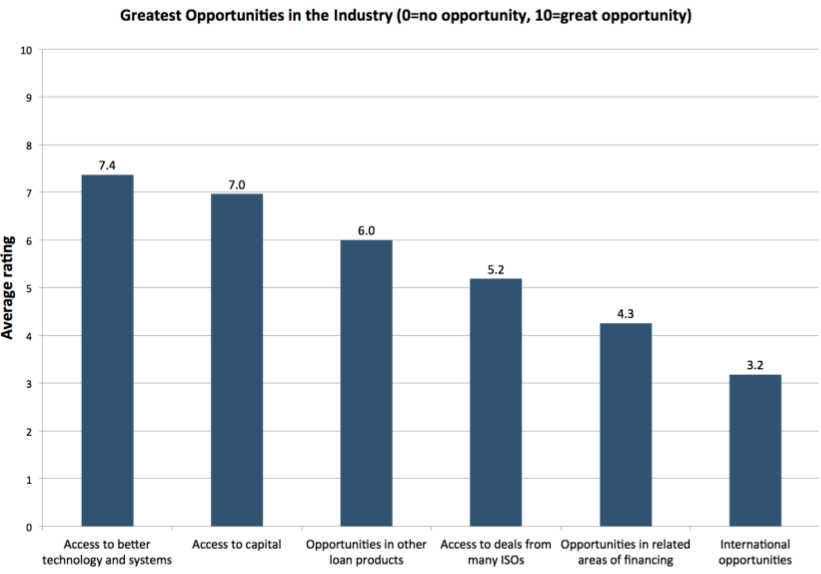

ACCESS TO BETTER TECHNOLOGY AND SYSTEMS IS THE GREATEST OPPORTUNITY IN THE INDUSTRY

Based on responses from participants asked to score the importance of opportunities on a scale of 0–10, with 10 being the highest.

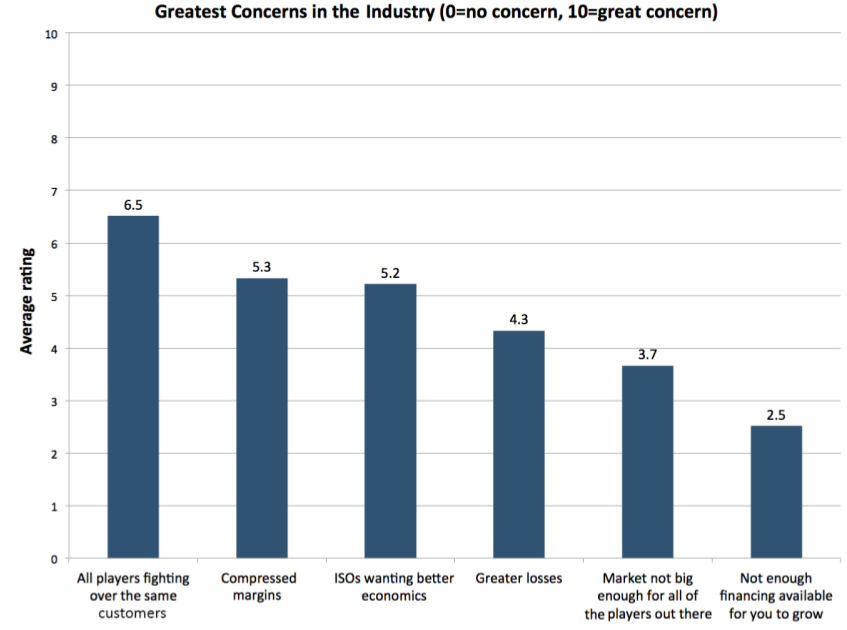

ALL PLAYERS FIGHTING OVER THE SAME CUSTOMERS IS THE GREATEST CONCERN IN THE INDUSTRY

Based on responses from participants asked to score their concerns on a scale of 0–10, with 10 being the highest.

The identities of participants and their individual responses are confidential. Participants were asked a total of 27 questions and had the ability to waive a response to any question, including the disclosure of their identity to the surveyors themselves.

Survey participants are eligible to receive the full anonymized report. Industry players who complete the full survey will automatically receive a full copy of this report. If you are not part of an operating company in the industry and you would like to obtain a copy of the report or participate in the survey, please contact Bryant Park Capital or AltFinanceDaily.

DOWNLOAD THE PDF VERSION

Meet the Source: How Jared Weitz and United Capital Source became one of the industry’s fastest growing shops

October 23, 2015Jared Weitz came from humble beginnings and nearly settled for a humble fate. But associates say an ordinary, uneventful life wouldn’t have suited him – he works too hard and figures things out too quickly.

Almost ten years ago Weitz, 33, was parking cars to earn money for community college. After finishing at St. Johns University, he almost made plumbing his career. But now he’s CEO of United Capital Source LLC, an alternative-finance brokerage with deal flow of between $9 million and $10 million a month and an annual growth rate of over 65 percent.

Business associates, former bosses and his small cadre of employees all seem to revere Weitz for his honesty and straightforwardness. They consider him a personal friend. They say he continues to grow as a businessman and as a human being while taking pleasure in helping others do the same.

Geographically, Weitz has the good fortune to know where he belongs – the city of New York is in his DNA. “Every time I fly back,” he said, “I’m so happy to land.”

His love affair with the city began in Brooklyn. He was born there and raised in a Brighton Beach apartment in the shadow of Coney Island. When he was 16, the family moved to Oceanside on Long Island.

As the second of six children, Weitz had to come up with the money for college on his own. “My older sister and I had to pay our way,” he said. “Everybody else, my dad was able to cover.” He started school at Nassau Community College, selling cell phones and parking cars at night.

But then came an abrupt change. Once Weitz saved enough money, he transferred to Tulane University in New Orleans to pursue a relationship with a woman who was finishing her studies there. He attended classes part-time, worked as the athletic director at the Jewish Community Center, tended bar in a Mexican restaurant and served summonses for a law firm.

But then came an abrupt change. Once Weitz saved enough money, he transferred to Tulane University in New Orleans to pursue a relationship with a woman who was finishing her studies there. He attended classes part-time, worked as the athletic director at the Jewish Community Center, tended bar in a Mexican restaurant and served summonses for a law firm.

The relationship with the woman fizzled, but Weitz made lasting friendships during his days down south. His old roommate in New Orleans, who now practices law in Atlanta, serves as counsel for United Capital Source.

When Weitz had been in New Orleans for two years, Hurricane Katrina struck. He evacuated to Houston, where he stayed in a Holiday Inn for two weeks before realizing he wouldn’t be able to return to southern Louisiana anytime soon. The magnitude of the devastation was just too great.

Shouldering the duffel bag of belongings he had managed to pack on his back during the evacuation, he returned to New York, enrolled in St. John’s University and began working in sales for Honda Financial Services and parking cars.

Weitz had started school expecting to become a teacher. He had grown up with younger siblings and liked leadership roles, which convinced him teaching would be a good fit.

Still, many of his college jobs had required him to sell. As a bartender, for example, he promoted drink specials. As an athletic director he convinced people to sign up for classes. “Everything that I took to naturally wound up being in the sales, marketing and finance arena,” Weitz observed.

When he was nearly finished at St. John’s, Weitz was parking a car for an acquaintance who offered him a job as a union plumber. Suddenly, he was making $27 an hour and had health benefits. “It was a big breather for me,” Weitz recalled.

He quit his three jobs and labored as a plumber from 7 a.m. to 3 p.m. School started at 3:30 p.m. for him and stretched into the evening. But when he finished his degree, working as a teacher for $35,000 to $40,000 a year no longer seemed attractive.

Besides, his plumbing work didn’t center on toilets. On typical commercial plumbing jobs he did things like install air, medical and gas lines in hospitals. He was reading blueprints and bidding for jobs. A promotion to foreman didn’t seem that far off.

At about the same time, near the end of 2006, a friend, Mike Caronna, landed a job at Bizfi, formerly known as Merchant Cash and Capital (MCC), The company, which had just started and had only a few employees, was looking for underwriters.

As fate would have it, Weitz fell into a conversation with a fellow union plumber, one who had been on the job for 30 years. The older man reminded him that his wages would never climb much higher than they were right now. The veteran plumber then showed the younger man his hands, bent from decades of holding tools. “That got me thinking,” Weitz said.

He asked his friend Caronna to arrange a job interview at MCC. He got an offer and took a 90-day leave from his plumbing job to give the world of finance a try. “After about two weeks, I knew it was for me,” he said of the alternative-finance industry. It was by then the beginning of 2007.

Weitz excelled as an underwriter, and the company CEO, Stephen Sheinbaum, picked him and four others for a sales contest. Sheinbaum gave them some leads and turned them loose. Weitz won the competition but asked his boss to help him gain experience in business development and operations before taking on a sales position.

Sheinbaum was happy to comply. “He is one of the best and the brightest in the space,” he said of Weitz.

So, at age 25, Weitz found himself building a business development department by cultivating relationships with ISOs and persuading them to send business to MCC. “It was amazing,” he said of those days. “That was a big opportunity.”

Weitz learned the mechanics of the business. He found that the right ISO can originate good deals and a bad ISO can ruin deals. He learned the politics of when to talk, when to remain silent and when to let someone vent.

Then Weitz and a good friend at MCC, Anthony Giuliano – who’s now managing partner of Sure Payment Solutions – worked out how they could improve the MCC sales effort. They pitched Sheinbaum on the idea of having a second internal sale force, and that led to the birth of Next Level Funding (NLF), a division of MCC.

Weitz and Giuliano each owned 10 percent of NLF, and MCC owned 80 percent. “I’m 26, about to be 27, and I’m like, ‘You did it, Man,’” Weitz said as he looked back.

After about four months, NLF absorbed MCC’s original sales division. Next, Giuliano and another executive, Paul Giuffrida, decided to leave MCC. Weitz felt torn. He felt an allegiance to Giuliano and respected Giuliano’s knowledge of programming – a subject that was alien to him. Yet Sheinbaum had provided Weitz a series of opportunities.

Weitz stayed at MCC but felt he deserved to become chief sales officer. When that didn’t happen, he sold his shares back to the company at a dramatically reduced price to extricate himself from a non-compete clause and set off to start United Capital Source (UCS).

With a five-figure investment, Weitz and his then partner, started UCS in January of 2011 in a 250-square-foot office in Long Beach, L.I. Weitz invested about 90 percent of the money he had saved while working at MCC.

Jon Baum left NLF with Weitz and became the first UCS employee. Within a week or two, Danielle Rivelli, left NLF to join UCS, and Weitz put the remaining 10 percent of his savings into the business to meet the expanded payroll. Today, Baum and Rivelli are UCS sales managers.

Jon Baum left NLF with Weitz and became the first UCS employee. Within a week or two, Danielle Rivelli, left NLF to join UCS, and Weitz put the remaining 10 percent of his savings into the business to meet the expanded payroll. Today, Baum and Rivelli are UCS sales managers.

The first month UCS was open, it funded $240,000 in deals. “It just felt good to be on my own and start funding deals,” Weitz said. From the beginning of UCS, he won praise from funders for bringing them the right kind of deals with merchants who were likely to repay.

“He really has the pulse of the marketplace and what a lender is looking for,” said Todd Sherer, who handles business development for Entrepreneur Growth Capital. “He doesn’t waste time giving you transactions that don’t fit in your box.”

That’s because doing things right means a lot to Weitz. “He is one of the most straightforward, honest, high-integrity people I have met in the industry,” said Steven Mandis, adjunct associate professor at the Columbia University Business School and chairman of Kalamata Capital LLC.

He’s won the OnDeck seal of approval. “OnDeck has a rigorous and extensive background check process as part of our broker certification process,” said Paul Rosen, OnDeck’s chief sales officer. “Jared Weitz and United Capital have passed our screens and process and are currently active brokers for OnDeck.”

And with time, Weitz has learned patience. He was sometimes short with funders when he started his company but has matured into a pleasant person to deal with, said Heather Francis, CEO of Elevate Funding. “I’ve seen that growth with him,” she said.

All of those good qualities soon came together to help UCS succeed. Within four months of its launch, the company rented a 1,500-square-foot office in Garden City and hired two more people. Next came a 3,200-square-foot office in Rockville Centre and three more employees.

“The company was growing and gaining traction,” Weitz recalled. “I bought out my original partner.” Since then, Vincent Pappalardo has invested in UCS and become a minority partner.

Meanwhile, the lease was expiring on Long Island, and Weitz felt the time had come to move to Manhattan. That would enable the company to draw employees from throughout the region and not just Long Island.

“We decided to bite the bullet and pay the excess money to move to the city because we believed it would be better for the business,” Weitz said. He added two people and rented a 5,500-square-foot space near Penn Station in the Garment District in September of 2014.

Within three months of making the move to Manhattan, business doubled. “Being in a faster-paced environment caused the business to go through another growth phase,” he said. After nine months in the city, UCS is now taking over a whole 8,500-square-foot floor of the same building.

Within three months of making the move to Manhattan, business doubled. “Being in a faster-paced environment caused the business to go through another growth phase,” he said. After nine months in the city, UCS is now taking over a whole 8,500-square-foot floor of the same building.

UCS remains a small shop in terms of headcount with 21 people, but the company’s funding numbers equal the output of many brokerages five times its size. Twelve of the UCS employees work in sales, with the others engaged mainly in underwriting, operations and customer service.

Less than 2 percent of UCS’s funding volume comes from broker business. “We self-generate all of our business,” Weitz said, declining to elaborate too much on his company’s marketing efforts.

“My salespeople – bar none – are the best in the industry,” he claimed. “Much like the Navy has the SEALS and the Army has the Rangers, there are groups in the industry that can do triple or quadruple what other people do because that’s just the way they are.” His people fund an average of $750,000 per month per person in new business, while his renewals reps fund well into the 7-figure range per person.

UCS salespeople achieve their results because they have detailed knowledge of the industry, Weitz said. The staff’s understanding of alternative finance doesn’t end with sales but also includes underwriting and finance, he noted. “That’s what makes you a very good and knowledgeable sales rep,” he maintained.

His salespeople don’t just tell a client what he or she wants to hear. They take the time to understand the client’s financial situation. “They know how to read a profit and loss statement, a balance sheet and tax returns,” Weitz said.

ARE THE BEST IN THE INDUSTRY”

While 90% of Weitz’s sales team has a college degree, most of the salespeople have come from outside the industry, he said, noting that one was with Sleepy’s, the mattress company. Another was selling memberships at a gym, one worked for a credit card processing company, two were barbers and one had just graduated from college.

UCS doesn’t make double-digit commissions because the company isn’t over-charging merchants, Weitz maintained. The company does not obtain excess funding that a customer can’t afford or increase the factor rate to dangerous levels, he noted.

“You’re not really helping the merchant” by providing too much capital, Weitz asserted. “You’re sucking the blood out of him before he goes away. That’s not why I’m in business.”

A clean record will also prove beneficial when federal regulation comes to the industry, he said. Integrity in the workplace can also spill over into other parts of a person’s life, Weitz believes.

As UCS grew larger and Weitz grew older, he saw his employees rent their first apartments and then buy their first homes. He learned then that he had taken on more responsibility than was apparent to him at first.

As UCS grew larger and Weitz grew older, he saw his employees rent their first apartments and then buy their first homes. He learned then that he had taken on more responsibility than was apparent to him at first.

To accommodate the employees he added a human relations department and commissioned a company handbook. He’s also started marketing, finance, operations and other departments.

He’s lost only four employees because he pays them well, respects their time and doesn’t view their youth as a liability.

Meanwhile, talking daily to merchants and hearing about their heartaches and triumphs has humbled and matured Weitz. Seeing how the merchants’ choices panned out or fell short also shaped him and helped him grow up a little, he said.

Weitz has found time in his 70-hour workweek to meet his future bride. They’re planning to wed next year, and he plans to invite his entire staff. “It wouldn’t feel right without them,” he said.

Weitz has skipped the Ferrari, Rolls Royce and mansion because he didn’t feel he needed them. But even without those status symbols, it’s clear that Weitz has avoided settling for a humble fate.

As for what comes next, UCS is said to be developing an online marketplace to take their business to the next level, though Weitz declined to provide specific details about how it will work. “We’re on pace to do more than $100 million worth of deals a year,” Weitz said. “And as far as we’ve come, I feel like this is still just the beginning.”

Did Your Deal Slip Out The Back Door?

October 22, 2015Gil Zapata found himself in the right place at the right time to catch someone red-handed at backdooring, the practice of stealing an alternative-funding deal and cheating the original ISO or broker out of the commission.

It seems that Zapata, who’s president and CEO of Miami-based Lendinero, was sitting in a client’s office about three years ago when the phone rang. The call came from an employee of a direct funder that had turned down Zapata’s deal to fund the merchant. Now, the employee was offering funding from another source without notifying Zapata. Fortunately, the merchant didn’t accept the surreptitious funding, Zapata said. “There’s a huge loyalty factor with maybe 50 percent of the clients an ISO has under their belt,” he noted.

It seems that Zapata, who’s president and CEO of Miami-based Lendinero, was sitting in a client’s office about three years ago when the phone rang. The call came from an employee of a direct funder that had turned down Zapata’s deal to fund the merchant. Now, the employee was offering funding from another source without notifying Zapata. Fortunately, the merchant didn’t accept the surreptitious funding, Zapata said. “There’s a huge loyalty factor with maybe 50 percent of the clients an ISO has under their belt,” he noted.

But many merchants sign up for backdoor deals out of ignorance, callousness or desperation, and the problem seemed to gather momentum in the first quarter of this year, according to Cheryl Tibbs, owner of Douglasville, Ga.-based One Stop Funding LLC.

When Tibbs found herself the victim of backdooring a few months ago, the merchant’s loyalty to the ISO prevailed once again. “Because of the relationship we had with the merchant, he let us know and didn’t go along with it,” she said.

Both cases fall into one of the categories of backdooring. This type usually occurs when an ISO or broker submits a deal and the funder declines it, said John Tucker, managing member of 1st Capital Loans LLC in Troy, Mich. An employee of the funder then takes the file and offers it to other funders, often those that accept higher-risk deals. The funder’s employee conveniently forgets to include the originator in the commission, Tucker said. Meanwhile, the employee’s boss might know nothing of the post-denial goings-on.

In another variety of backdooring, ISOs or brokers deceptively claim that they’re direct funders. They solicit deals in online forums, by email message or over the phone, and then they offer the deals to companies that really do function as direct funders. In many cases, the fake funders pocket the entire commission, Tibbs said.

“I’m bombarded with probably 10 emails every day of the week from a supposedly new lender that wants my business, and they’re really just a broker shop like we are,” she maintained.

To guard against both kinds of backdooring, ISOs and brokers should know their funding sources, everyone interviewed for this article suggested. “What we’ve done is tighten up on how we do submissions,” Tibbs said. “We’re very particular about which lending platforms we use.” Although her company has contracts with 60 to 70 funders, it uses only three or four regularly, she noted. “Shotgunning” deals to lots of potential funders invites backdooring, Tibbs said.

To guard against both kinds of backdooring, ISOs and brokers should know their funding sources, everyone interviewed for this article suggested. “What we’ve done is tighten up on how we do submissions,” Tibbs said. “We’re very particular about which lending platforms we use.” Although her company has contracts with 60 to 70 funders, it uses only three or four regularly, she noted. “Shotgunning” deals to lots of potential funders invites backdooring, Tibbs said.

Tibbs also scrutinizes deals to determine which funder would provide the best fit. That way, fewer deals are declined and thus fewer became candidates for backdooring by unscrupulous funder employees. “We have a system. We scrub it. We do the numbers,” she said of her company’s close attention to underwriting, which helps determine what funders would accept the deal.

Her company also keeps a watchful eye on every deal’s progress. “We know exactly where the deal is, and who’s looked at it,” she said. It also helps to insist upon having a dedicated account rep, Tibbs emphasized. That way she can form a relationship that discourages backdooring.

Perhaps the most basic safeguard comes with determining that the company claiming to fund the deal really has the capital to do it and isn’t just shopping the file to real funders. Tucker advised using Internet searches to turn up evidence that the supposed funder really isn’t another ISO or broker. Searches should reveal press releases on equity rounds that direct funders have received, for example. If open-ended Web searches don’t produce satisfying results, check state registrations, he said.

ISOs and brokers can also prevent backdooring by avoiding sub-agent status, Tucker cautioned. “I don’t know why guys would want to be a broker to a broker,” who could steal commissions, he observed. One exception to the sub-agent problem comes with agents who are just entering the business and are receiving training from a broker, Tucker said. In another exception, sub-agents may find another broker has competitive advantages that aren’t easy to duplicate – like a $20,000 monthly marketing budget to generate sales leads, he continued. Or perhaps the other broker gets low base pricing from a funder that allows for reduced factor rates without sacrificing part of the commission.

Brokers and ISOs can also protect themselves from backdooring – and just in general – by maintaining their relationships with merchants, even those who’ve been denied funding from four or five sources, Zapata said. An increase in revenue or jump in credit worthiness can qualify them a few months later, and other brokers or funders may be soliciting them in the meantime, he said.

Brokers and ISOs can also protect themselves from backdooring – and just in general – by maintaining their relationships with merchants, even those who’ve been denied funding from four or five sources, Zapata said. An increase in revenue or jump in credit worthiness can qualify them a few months later, and other brokers or funders may be soliciting them in the meantime, he said.

Then there’s the possibility of collective action against backdooring. An association or some other entity representing the industry could compile a database of companies accused of backdooring, Tibbs said. “Just as there’s a black list of merchants that have been red-flagged from getting merchant cash advances, there should be some type of database of funders that frequently backdoor deals – that way, ISOs know to stay away from them,” she maintained.

The database would also prompt owners and managers of direct-funding companies to crack down on employees who use nefarious tactics, Tibbs continued, because the heads of companies would want to stay off the list.

But finding the financial support and staffing for such a database might prove difficult, according to Tucker. He noted that the card brands, such as Visa and MasterCard, maintain a match list of merchants barred from accepting credit cards. But the card brands have vast resources and a keen interest in the list, he said.

Requiring funders to pay to register might discourage ISOs and brokers from posing as funders, Tibbs suggested. But that, too, would require an infrastructure and would demand financial investment, sources said.

Still, everyone interviewed agreed that the industry should police itself with regard to backdooring instead of inviting federal regulators to enter the fray. “The federal government will mess with pricing without understanding every merchant can’t get low factor rates because there’s too much risk on the deal,” Tucker warned.

Perhaps extending the protection period in funding applications would help guard ISOs and brokers, Zapata said. But he cautioned that making the time period too long could interfere with the free market.

Keeping backdooring in perspective also makes sense, Zapata said, noting that merchants often receive multiple funding offers because everyone in the industry is basing phone calls on the same Uniform Commercial Code filings regarding distressed merchants.

Some Small Business Funders Are Pivoting or Closing Shop

October 20, 2015 One of the unique insights AltFinanceDaily gets as a company that sends a lot of email and snail mail to folks in the industry is the rejection rate. One day an entrepreneur is telling us all about their new lending business and the next day the Post Office returns their magazine for a vacant address. Sometimes there’s a change in the model or a partnership didn’t work out. Other times lead generation became too hard or too many merchants defaulted very early on. The truth is, as much as the industry is growing, some companies are pivoting or closing their doors.

One of the unique insights AltFinanceDaily gets as a company that sends a lot of email and snail mail to folks in the industry is the rejection rate. One day an entrepreneur is telling us all about their new lending business and the next day the Post Office returns their magazine for a vacant address. Sometimes there’s a change in the model or a partnership didn’t work out. Other times lead generation became too hard or too many merchants defaulted very early on. The truth is, as much as the industry is growing, some companies are pivoting or closing their doors.

At Lend360, there were whispers around the trade show floor that acquisition costs have spiked and it was being felt on the bottom lines. Broker houses are opening, closing, merging with each other and being acquired. Funders have reacted by giving them lines of credit to either help them grow or stay afloat, hoping that their sources of deal flow don’t fall apart.

On one conference panel titled, A Discussion of Best Practices: Advancing The Cause for Business Finance, veteran underwriter and industry consultant Andrew Hernandez of Central Diligence Group, said he’s watched a lot of new entrants in this industry make mistakes. “We’ve seen guys lose their shirt,” he said. He explained that too often small business funding companies look to cut their acquisition costs in the wrong places, like simply paying less for leads or paying brokers lower commissions. That only works to a point. “Underwriters can help keep the cost of acquisition down by funding the right deals and trying to get good deals done,” he said.

The owner of one funder summed up his dilemma for me, my brokers are making more on a deal than I am and I’m the one taking all the liability on it. Maybe I should become a broker instead. Not that there would be anything wrong with that. For some companies in this industry, the best path forward is achieved through trial and error. For example, World Business Lenders’ Alex Gemici said at the conference that they started off by making unsecured loans and now only do loans secured by real estate. Gemici also said he believes the industry is heading for a major shakeout within the next three years and that irrational exuberance keeps him up at night.

If he’s right, an economic downturn could squeeze out a lot of players that are already feeling the pinch of high acquisition costs.

For those newer to the industry, they might not remember that the effects of the 2008-2009 financial crisis and ensuing recession was brutal. More than half of the providers of merchant cash advances went out of business, some within weeks when their credit lines were pulled.

A lot of the “industry leaders” of 2008 aren’t around anymore: First Funds, Fast Capital, Second Source, Merit Capital, iFunds, Summit, Infinicap, Global Swift Funding, and more.

Given the favorable economic climate and regulatory environment, this is a bad time to be struggling. 2015 may be one of the last years to pivot in a major way before it’s too late.

Is Online Lending Really Just Offline Lending?

October 19, 2015 Two weeks ago the Wall Street Journal postulated that online lending’s biggest beneficiary was the U.S. Postal Service. “In July alone, Lending Club mailed 33.9 million personal-loan offers,” it said. “The average monthly volume of personal-loan offers sent through the mail has more than doubled in two years to 156 million in the year through July from 73 million in the same period in 2013,” it added.

Two weeks ago the Wall Street Journal postulated that online lending’s biggest beneficiary was the U.S. Postal Service. “In July alone, Lending Club mailed 33.9 million personal-loan offers,” it said. “The average monthly volume of personal-loan offers sent through the mail has more than doubled in two years to 156 million in the year through July from 73 million in the same period in 2013,” it added.

These figures have some people concerned that there is no network effect for these lending platforms. Last month, Timothy Puls, an equity analyst for Morningstar, said that the value of a company like Lending Club doesn’t grow just because more users are on the platform. That means a continuous stream of marketing is essential since they’ll always need to find new borrowers to sustain the business.

To illustrate how sensitive lenders are to this, OnDeck CEO Noah Breslow spoke to the increasing competitiveness of direct mail in their 2nd quarter earnings call and argued their strategy was to “break through the clutter” and “better communicate our value proposition.” Analysts on the call were concerned by that, which prompted a question by Christopher Brendler of Stifel, Nicolaus & Company during the Q&A session.

Question by: Christopher Brendler of Stifel, Nicolaus & Company

You mentioned in the direct channel about a response rate, talking about a response rate to direct mail. Can you talk about the response rate that you are seeing in that channel? It seems like from an outsider’s perspective we’ve gotten more competitive and it sounds like you’ve had a little bit of a struggle there. We just want to see if there is any color you could add on what the competitive environment is having on the direct channel.Answer by: Noah Breslow of OnDeck

I think what we are seeing really is just an intensified set of activities and you can’t really isolate it down to any single or couple of competitors but it’s sort of both in the offline direct mail channel, we are seeing increased mail volumes over where they were six months ago. And then in the online channel we are seeing increased bidding and so forth for Google Adwords and the like.

Nothing to worry about when it comes to that mail stuff though right? Google Adwords, facebook, instagram, and snapchat are where the real action comes from for online lenders, you might think.

According to Marlette Funding CEO Jeffrey Meiler, that’s not the case. In the WSJ, he admits that 90% of the billion dollars in online loans they’ve originated have come from offline channels.

And maybe that’s because the term online lender might be a red herring. Online lenders don’t only exist in cyberspace, they have offices in the real world just like banks do. And sure, they have websites, but then again so do banks. When you start to boil it down, online lenders look a lot like every other business in existence today. And while it may not be typical for a small business owner to walk into the office of an online lender to get funding, several lenders have said this happens. And for the brokers that arrange business loans, it’s pretty common for them to visit the actual businesses and meet with the owner(s). Not a very online experience…

It may be fashionable to say what separates banks from online lenders is that you have to walk into a bank to apply for a loan, but that’s often just not the case. Most banks offer loans through the form of credit cards both online and through direct mail and they’ve been doing this for decades. The only difference is now they’re competing with other lenders that don’t have local branches for the customer to walk into it, the online lenders. And maybe that’s what the difference is, being branchless could be what defines an online lender.

For now though, a heck of a lot of online lending seems to be originated offline.

Leads vs. Data: Do You Know What You’re Buying?

October 11, 2015 One important aspect of being a broker is your ability to generate qualified leads. At the core of a broker’s business, he/she is really just a lead generator for their network of funders, functioning as a way to improve their funder’s profitability through the acquisition of new clientele.

One important aspect of being a broker is your ability to generate qualified leads. At the core of a broker’s business, he/she is really just a lead generator for their network of funders, functioning as a way to improve their funder’s profitability through the acquisition of new clientele.

While I once questioned if brokers truly knew what they were selling when it came to the merchant cash advance product, my next question is in relation to the purchase of what vendors refer to as “Leads.” I want to know, do you (as a broker) know what you’re buying?

While it’s apparent that you can produce qualified leads internally, can you truly produce the same externally? With the various companies that pop up (seemingly overnight) without domain names, without professionally designed websites or with just the use of a Gmail/Yahoo Email Address, can you truly trust the claims that most of them make in terms of their ability to sell you qualified leads? Maybe so, maybe not, but I believe if we begin with the proper connotation of a “lead” vs. a “data record”, then it might help to truly determine what you’re purchasing from these external sources.

WHAT IS DATA?

Data is business intelligence, which is either generic or specialized information on a business or a group of businesses that are within a sales professional’s generic target market. It would be up to the sales professional to take this data, turn it into a sales pipeline (leads), convert a percentage of those pipeline listings into application submissions, and a portion of those applications into funded deals. Data can come in the form of generic listings such as those from the Yellow Pages or specialized listings such as those from court houses, financing requests and UCC records.

So for example, a UCC record is a data record, not a lead. You would buy let’s say 2,000 UCC records and after running through them via a predictive dialer internally, you might filter off 130 interested prospects which creates your sales pipeline, which is what you would now call “leads.” Then through following up on those 130 interested prospects, you might convert let’s say 20 – 30 of them into application submissions and fund 6 – 9 of them.

WHAT IS A LEAD?

A lead is an actual interested prospect in the services/products that you specifically have to offer. This means they have seen your specific ad or marketing piece, and have specifically expressed interest in what you have to offer. These can only be generated in-house through:

- Running through Data Records as explained above.

- Using other forms of direct marketing such as mailers, email marketing and through directly contracted referral sources who resell your product/company.

- Using indirect marketing options such as banner ads, radio ads, TV ads, print ads, billboard ads, SEO related concepts, and Pay-Per-Click, where the prospect will see or hear the ad and respond to you directly through filling out a form, giving you a call, shooting you an email, etc.

I firmly do not believe you can purchase Leads externally, I believe they can only be generated in-house using direct or in-direct marketing procedures listed above.

HOW TO ADDRESS LEAD GENERATION COMPANIES?

HOW TO ADDRESS LEAD GENERATION COMPANIES?

So when a company comes to you selling “leads,” you should ask them are they selling “leads” or are they selling “data” records? Because they can only be selling YOU leads if they have specifically marketed your specific company and products to said generic target market, and generated interested parties to your specific company and products.

So what about companies that generate what they deem to be “leads” for the “service” that you offer in a generic fashion? For example, people that sell insurance would see people selling insurance Leads, people that sell equipment leasing will see people selling equipment leasing leads, and of course people that sell merchant cash advance will see people selling merchant cash advance leads.

I am still of the belief that these are not leads, but data records, it’s just a different type of data record similar to that of a UCC. A UCC is a more specialized type of data record that tells you more in-depth information on the current situation of the prospect in particular, such as the fact that they took out a cash advance on XYZ date with XYZ funder. This is more specialization than let’s just say a basic Yellow Pages listing, which just has the company’s name, address and telephone number. But both the UCC record and the Yellow Pages listing are still data records.

The “product specific leads” that are sold are usually just a listing of individuals who filled out various online forms requesting some type of particular product, service or financing vehicle. In my opinion, these are not leads, but still data records that will list only the generic information on the company and the date/time they requested more information “generically” on the product or service in particular.

You (as the broker) still have to call these leads and sell them on your company, your product, your pricing, your platform, etc. This means similar to UCC records, if you get 2,000 of these records, you might only convert 130 to interested prospects, which would now be the official “leads.” Then of course from there through following up on those 130 interested prospects, you might convert let’s say 20 – 30 of them into application submissions and fund 6 – 9 of them.

HOPEFULLY NO ONE IS OFFENDED

HOPEFULLY NO ONE IS OFFENDED

This article might offend some individuals who are in the “Lead Generation” business, but I explicitly want to state that my intention is not to cause distress. I firmly believe that the vast majority of the time, when one is purchasing “leads” from an external source, they are indeed only purchasing data records. As a result, such disclosure should be made and such pricing structures modified.

The purpose of this article is so that brokers can know what they are purchasing ahead of time, to make sure that the price they’re paying fits their ROI analysis.

The last thing any vendor would want (in my opinion) is to have a bunch of angry online reviews from brokers who paid $3.00 a piece for your 2,000 “leads,” that only converted to 130 truly interested parties, and then only produced 20 – 30 completed application submissions.

Creditor Fails to Navigate Usury Law “Minefield”, Ordered to Refund $1.3 Million to Debtor

October 5, 2015 A recent court decision demonstrates the complexity and dangers faced by creditors attempting to navigate California’s usury laws. In the case, a lender agreed to purchase a debtor’s promissory note from a bank and refinance it for a lower amount. The entity that the lender used to purchase the note from the bank was a licensed California real estate broker. Simultaneously with the purchase of the note by the first entity, the lender assigned the note to a second entity under its control. Later the debtor defaulted on the note and filed bankruptcy.

A recent court decision demonstrates the complexity and dangers faced by creditors attempting to navigate California’s usury laws. In the case, a lender agreed to purchase a debtor’s promissory note from a bank and refinance it for a lower amount. The entity that the lender used to purchase the note from the bank was a licensed California real estate broker. Simultaneously with the purchase of the note by the first entity, the lender assigned the note to a second entity under its control. Later the debtor defaulted on the note and filed bankruptcy.

In the bankruptcy proceeding, the lender filed a claim against the bankruptcy estate for the remaining amount due on the note. The debtor objected to the claim and argued that the interest rate that had been charged by the lender was usurious. As such, the debtor asked that the court order the lender to refund the usurious interest that had been paid.

While the lender agreed that the rate charged on the note exceeded the maximum rate set by California’s usury law, the lender argued that the purchase of the note had been arranged by a licensed real estate broker and therefore the transaction was exempt from the usury restrictions. After a two day trial, the court found in favor of the debtor and order the lender to refund over $1.3 million to the debtor.

In its decision, the court noted that the California legislature had provided an exemption from the applicability of California’s usury laws by exempting “any loan or forbearance made or arranged” by a licensed real estate broker and secured by real estate. The court went on to explain, however, that the exemption only applies where the broker was acting on behalf of another. Where a broker is acting as a principal, the exemption does not apply.

After examining the relevant loan documents, the court found that the purchase of the note by the first entity had been done on its own behalf and not on behalf of the entity to which the note was later assigned. The court rejected the lender’s argument that the lender had done little to formally structure the transaction as a broker-principal arrangement simply because it controlled both entities and knew it would be transferring the note following the purchase from the bank. For that reason, there was no “need to report anything to [itself]”. The court was unpersuaded by this argument and stated that “[t]he usury laws present a minefield that people in the [lender’s] position, with their… status as licensed brokers, can readily navigate. This time they did not navigate carefully.”

In light of this case, lenders doing business in California should be careful to “navigate carefully” the complex usury laws of that state, lest they too become a victim of its “minefield” of statutory dangers.

In re Arce Riverside, LLC, 2015 Bankr. LEXIS 3275 (Bankr. N.D. Cal. Sept. 28, 2015)