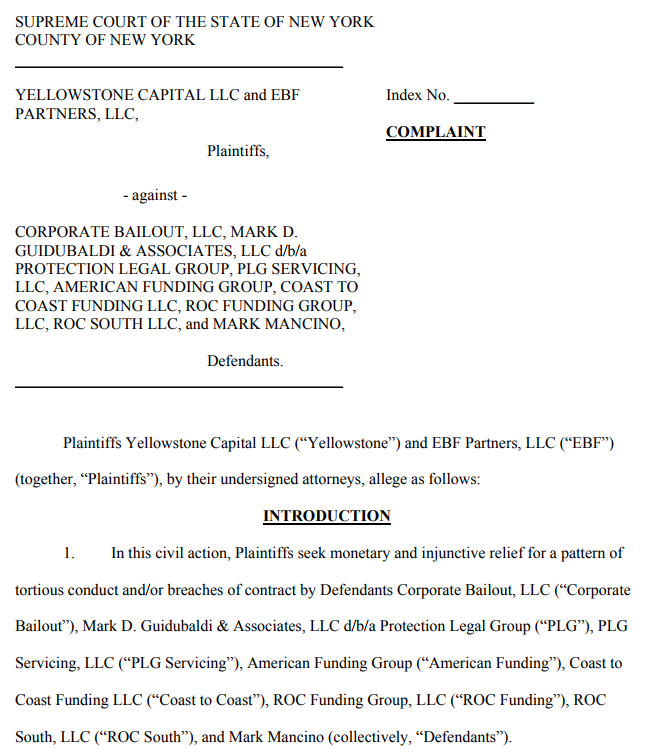

ISOs Alleged to Be Partners in Debt Settlement “Scam” in Explosive Lawsuit

September 28, 2017 ISOs and brokers referring deals to debt settlement companies should pay attention to a lawsuit that was filed in the New York Supreme Court on Wednesday. In it, plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) allege that certain ISOs are culpable partners in a scam that nefarious debt settlement companies are perpetrating on small businesses.

ISOs and brokers referring deals to debt settlement companies should pay attention to a lawsuit that was filed in the New York Supreme Court on Wednesday. In it, plaintiffs Yellowstone Capital and EBF Partners (“Everest Business Funding”) allege that certain ISOs are culpable partners in a scam that nefarious debt settlement companies are perpetrating on small businesses.

The debt settlement companies “mislead the merchants as to the services they will perform and the cost to the merchant, and they also conceal their relationships with the ISO Defendants and the fact that they or their affiliates are introducing these same merchants to merchant cash advance providers like Plaintiffs only to later induce those merchants to breach their agreements with their cash advance providers,” the complaint states.

Among the named defendants are:

- Corporate Bailout, LLC

- Mark D. Guidubaldi & Associates, LLC dba Protection Legal Group

- PLG Servicing LLC

- American Funding Group

- Coast to Coast Funding, LLC

- ROC South, LLC

- Mark Mancino

Several defendants are already best known for running an office “so sexually aggressive, morally repulsive, and unlawfully hostile that it is rivaled only by the businesses portrayed in the films ‘Boiler Room’ and ‘The Wolf of Wall Street,’” according to a salacious story that graced the back cover of the New York Post last month.

One paragraph of the complaint summarizes the allegedly collaborative scheme like this:

American Funding, Coast to Coast, […] (the “ISO Defendants”) are independent sales organizations (“ISOs”), companies that ostensibly support the merchant cash advance industry by brokering merchant agreements for companies like Plaintiffs. The ISO Defendants are anything but the proverbial “honest brokers.” As alleged below, they have partnered with companies that purport to offer debt relief services to merchants who have agreements with merchant cash advance companies like Plaintiffs. In practice, for these companies, “debt relief” is a code word for deceiving merchants to breach their existing agreements with Plaintiffs and to instead pay fees to these debt relief entities. In short, they scam merchants into believing that they can save them money when, in fact, they leave these merchants in financial shambles, while causing Plaintiffs to suffer millions of dollars in losses and future los[t] profits.

“’DEBT RELIEF’ IS A CODE WORD FOR DECEIVING MERCHANTS TO BREACH THEIR EXISTING AGREEMENTS”

Central to the plaintiffs’ claim is that they have ISO agreements with the defendants and that the defendants’ conduct is a breach of those agreements. The three causes of action alleged are tortious interference with contract, conversion, and breach of contract. Plaintiffs claim that 100 merchants with more than $3 million in outstanding balances are in breach of their contracts because of the defendants’ conduct.

The complaint was prepared and filed by attorneys at Proskauer, a 142-year old law firm founded in New York City.

Debt Relief Under Fire

The small business debt relief industry has been marred by scandal in recent years. In an unrelated criminal matter being handled in the Western District of New York, the owner of Corporate Restructure Inc. (no ties to Corporate Bailout) is currently residing in the Niagara County Jail awaiting trial on charges of conspiracy to commit mail fraud, wire fraud, bank fraud and money laundering for failing to deliver the debt relief services it charged for. In that case, United States vs. Sergiy Bezrukov, Bezrukov advertised that he could reduce a merchant’s short term debt by up to 75%. He is facing up to 30 years in prison. He was also previously a merchant cash advance ISO.

Two other MCA funding companies, Pearl Gamma Funding and Pearl Beta Funding, filed a lawsuit last November against another debt relief company that calls itself Creditors Relief. The complaint in that case also alleges tortious interference with contract and is still pending.

Meanwhile, a lawsuit filed in May by famous TCPA litigant Craig Cunningham against Corporate Bailout and Mark D Guidubaldi & Associates LLC went unanswered, according to court records. Cunningham, who alleged violations of telemarketing laws, filed for a default judgment against Corporate Bailout on September 12th.

Taking Advantage

Both Yellowstone Capital and Everest would not comment on the lawsuit they filed, citing pending litigation. Sources close to them, however, contend that both companies take matters that involve merchants being taken advantage of very seriously.

“When our own ISOs work directly in concert with companies that induce merchants to breach our contracts, that’s a problem,” said one source who did not wish to be named and was speaking generally about the recent introduction of debt relief service companies to the industry. “They’re taking advantage of businesses that can’t afford to be taken advantage of.”

An email sent by AltFinanceDaily to Mark Mancino early Thursday afternoon, an individually-named defendant alleged to be affiliated with the other defendants, has not yet received a response. This story may be updated if a reply is received.

A COPY OF THE COMPLAINT CAN BE VIEWED HERE.

C-level Credit Exec Leaves Lending Club for Affirm

September 21, 2017Lending Club’s Chief Credit Officer and Interim General Manager, Sandeep Bhandari, has joined fintech lender Affirm, according to Affirm CEO Max Levchin. Levchin posted the following on LinkedIn:

I am excited to announce and welcome Sandeep Bhandari to Affirm, Inc. as Chief Strategy and Risk Officer (CSRO).

Sandeep joins us from Lending Club where he was the Chief Credit Officer (CCO). Prior to Lending Club, he was at Capital One for many years, where he was Assistant Chief Credit Officer at Capital One Bank (Credit Risk Management) and Venture Partner (Capital One Ventures). Prior to that Sandeep held a variety of roles requiring expertise in strategy, credit risk management, marketing, product development, and underwriting across several lines of business including consumer and small business credit card, auto lending, and mortgage and home equity lending.

We are excited for Sandeep to join us for our next phase of rapid growth and to help us fulfill our mission of delivering honest financial products that improve lives.

The move comes on the heels of Lending Club announcing their “most advanced and predictive credit model ever.” Bhandari was responsible for credit strategy and overall credit risk management at Lending Club and presumably would’ve overseen that.

Talkative investors on the LendAcademy forum were not immediately sold on Lending Club’s new system, however. Some users bemoaned that Lending Club is ignoring common sense in favor of data. In one instance, the CEO of PeerCube referenced an interest rate anomaly alleged to be discovered in Lending Club’s pricing as “Data-driven but knowledge-unaware.”

Affirm and Lending Club differ. Whereas Lending Club targets the credit card refinancing market, Affirm helps consumers finance purchases. Last month, Affirm and Walmart were reportedly in talks to offer financing to consumers.

The Google Battle for Lending and SMB Finance Keywords

September 14, 2017The online lending battle is at least in part being fought online. Below is a chart of organic page 1 rankings in Google for some of the industry’s biggest players, banks, and the SBA. (Hat tip to Fundera and NerdWallet):

| Keywords | OnDeck | Kabbage | Fundera | Lending Club | NerdWallet | National Funding | Traditional Banks | SBA.gov |

| business loan | 1 | 9 | 3 | 5 | 4,7 | 6 | ||

| merchant cash advance | 2 | 3 | 4 | 8 | ||||

| working capital | 9 | 4 | ||||||

| commercial loan | 3 | 2,7 | ||||||

| small business loans | 2 | 3 | 5 | 7 | 1 | |||

| business line of credit | 3 | 2 | 11 | 1,4 | 6,7,8,9,10 | 5 | ||

| fast business loan | 1 | 4 | 2 | 5,6 | ||||

| business loan with bad credit | 7 | 1 | 2 | 3 |

The Top 10 Google Search Results for Merchant Cash Advance in February 2012 compared to now:

| February 2012 | September 2017 |

| MerchantCashinAdvance.com | Wikipedia |

| Yellowstone Capital | OnDeck |

| Entrust Cash Advance | Fundera |

| Merchants Capital Access | NerdWallet |

| Merchant Resources International | Businessloans.com |

| American Finance Solutions | Bond Street |

| Nations Advance | Capify |

| Bankcard Funding | National Funding |

| Rapid Capital Funding | CNN |

| Paramount Merchant Funding | CAN Capital |

The top result in 2012 is a great example of how much easier it was to game Google’s system back then. After achieving rank #1 for MCA and 300 other related keywords, MerchantCashInAdvance.com, which was just a lead generation site, sold for $75,000 in December 2011. The site was later clobbered by Google Penguin for black hat SEO and banished from visibility.

A major shift has obviously taken place over the last 5 and a half years. Is the search results game rigged to advance Google’s own interests? Three years ago I put forth my theory on that.

One thing that’s different between then and now is that Google now has 4 paid links above the organic search results as opposed to 3 and the paid links blend in more with the organic results. With the organic results pushed further down the page, they’re not as visible as they were five years ago.

Read my previous analyses on the industry’s search war over the years:

December 2015 Google Serves Low Blow to Merchant Cash Advance Seekers

March 2015 Google Culls Online Lenders – Pay or Else?

October 2014 Merchant Cash Advance SEO War Still Raging

August 2014 Six Signs Alternative Lending is Rigged: Do Lending Club and OnDeck have a helping hand?

October 2013 Google Penguin 2.1 takes swing at the MCA industry

August 2013 Your merchant cash advance press release may be hurting you

December 2012 Is Google your only web strategy?

July 2012 The other 93% [of leads]

April 2012 The SEO war continues

February 2012 The SEO War for Merchant Cash Advance: The first story on this topic

Reaction to Lending Club’s New Credit Model

September 13, 2017The few retail investors discussing the recent change Lending Club made to their credit model weren’t exactly optimistic, according to comments on the Lend Academy forum. Of particular concern is grade inflation wherein borrowers who previously scored a C or lower may now find themselves in the A or B category.

“We expect loan volume to shift toward higher quality grades (grades A and B) because some borrowers will qualify for lower interest rates under the new model,” Lending Club stated in an email last week.

Retail investor sentiment may not be all that important, however, as capital from self-managed accounts on the platform has waned after peaking in the first quarter of 2016. In Q2 of 2017, self-managed accounts only accounted for 13% of the capital used to fund loans. The majority came from banks and institutions.

LeaseQ and ARF Financial Partner to Automate Hospitality Equipment Financing

September 12, 2017BOSTON (Sept. 12, 2017) – LeaseQ, an online marketplace connecting business owners, equipment sellers, and lenders to make selling and financing equipment fast and easy, today announced a national partnership with ARF Financial, the only FDIC-compliant financial lender that provides short-term, unsecured business loans and lines of credit for restaurant/hospitality business owners and retailers nationwide.

“We are unique in having our own sales organization, and LeaseQ gives our loan consultants around the country a lease product with instant quotes,” ARF Financial CEO Steve Glenn said. “Now we are a one stop lender offering additional products to satisfy our customers funding needs for their businesses.”

Innovations in the equipment finance industry will continue to increase flexibility and convenience for customers, according to the Equipment Leasing and Finance Association’s (ELFA) Top 10 Equipment Acquisition Trends for 2017. Automation fuels advances in instant quotes, soft credit pulls, same-day approvals, one-day funding and blockchain for secure, multi-party transactions – many of which are available today through LeaseQ and ARF Financial.

“You can finance a car in an hour, but not a walk-in freezer to start or expand a restaurant,” said Vernon Tirey, co-founder and CEO of LeaseQ. “One-day funding is a trendy thing to say in equipment financing, but when the restauranteur or hotel manager presses the button to get financing, it has to work. We’re advancing our technology and partnering with lenders like ARF Financial who understand the value of automation to make it happen.”

LeaseQ and ARF Financial offer automated, flexible equipment financing for hospitality merchants who are frustrated with the time it takes to get a bank loan, or who cannot get a bank loan at all, including those:

- Expanding a facility

- Upgrading equipment

- Adding a location and renovating the property

- Managing working capital, and more

There are currently 150 lenders on the LeaseQ platform serving 28 vertical markets. Learn more at www.leaseq.com.

About LeaseQ

LeaseQ is an online marketplace connecting businesses, equipment sellers, and equipment finance companies to make selling and financing equipment fast and easy. The LeaseQ platform is a free, cloud-based SaaS solution with a suite of on-demand software and data solutions for the equipment leasing industry. LeaseQ provides business process optimization (BPO) and information services that streamline the purchase and financing of business equipment across a broad array of vertical industry segments. Learn more at www.leaseq.com.

About ARF Financial

ARF Financial LLC is a California licensed lender that sources short-term business loans and lines of credit for restaurant/hospitality and retail merchants nationwide. Since 2001, ARF has filled the void between traditional bank financing and less attractive venues of obtaining capital, giving merchants the ability to maintain control of their business, be more profitable and meet their financial goals. The company is managed and staffed by industry veterans with extensive experience in restaurant finance and small to medium retail industries.

For more information on their services, visit their website at www.arffinancial.com. You may fill out their contact form at www.arffinancial.com/contact, call 1-866-702-4430, or send an email to funding@arffinancial.com for inquiries.

ShopKeep Joins the MCA Crowd. Are Loans Next?

September 8, 2017

ShopKeep, an iPad-based cloud-connected technology company designed around POS and payments for small businesses, is expanding into MCAs with the launch of ShopKeep Capital in recent days. With its move into funding ShopKeep joins an area that competitor Square already operates in. But while both companies have unlocked the secret of customer acquisition they are not targeting the same small businesses.

Meanwhile this latest move into MCAs is just a step in what ShopKeep CEO Michael DeSimone describes as an evolution, one that could potentially lead to small business lending sooner than later.

“We had a lot of interest from our customers,” said DeSimone, referring to the nearly 25,000 small businesses that are on ShopKeep’s payment and software platform. ShopKeep Capital extends funding offers to eligible small businesses on the ShopKeep platform, and funding is approved within a couple of days.

Playing Field

ShopKeep is entering a space – MCAs — that is only getting more crowded, with the recent addition of iPayment, for instance. And while ShopKeep and Square operate in a similar market segment, they’re targeting different SMBs.

“Our customers tend to be larger than Square and more complex in their business models,” said DeSimone, pointing to the example of a restaurant with numerous employees and multiple locations. On average, customers on the ShopKeep platform generate sales of $350,000 per year.

As a payments company, ShopKeep’s customer acquisition strategy is tied directly to its software and payments businesses.

“This leverages our ability to understand the small business data flowing through our POS platform and manage it the way we do payments based on the premise of greater visibility into their business by the virtue of our payments platform,” said DeSimone.

He is quick to point out that ShopKeep is built on technology, and he said like every other part of the economy tech is disintermediating some parties and bringing others closer to the outcome they desire.

“The closer you are to the actual customer, the more your opportunity is to be able to be top of mind when they need something,” he said. “They have huge amounts of interaction with us. This level of interaction predicated on technology is really what creates the ability to have a relationship with the merchant to then be able to offer them a range of different products and services.”

DeSimone describes ShopKeep more as a technology play than a funder.

DeSimone describes ShopKeep more as a technology play than a funder.

“We have a lot of information most other providers of capital aren’t going to have unless they ask merchants to do a lot of work,” said DeSimone, pointing to an underwriting model that is almost 100% automated.

“We’ve built it to be largely pre-underwritten We only offer advances based on running the merchant through our underwriting model to see who comes up as a good candidate for ShopKeep Capital and making it available to them. We continually tweak the algorithm to make sure we are not being too tight or too loose,” he added.

Funding is the third revenue stream for ShopKeep, with software and payments representing the other two legs of the revenue stool. Meanwhile ShopKeep Capital is turning to its balance sheet to fund MCAs, but that is not the long-term plan.

“Currently it’s coming off our balance sheet, but it won’t be for very long. We have had several discussions with funding partners. And we expect over time we will migrate to more of a loan product and away from MCAs. We will explore the features and benefits of both to understand both our perspective and that of our customers,” said DeSimone, adding that there could be more clarity about the direction of this evolution in the next six months.

If ShopKeep does move into loans, the company could open up the platform to investors. “They are debt funds looking for returns and specific underwriting criteria. They will buy an advance or a loan eventually from what we originate. That’s the model we think we’ll go toward,” he said.

Something DeSimone and other lenders might want to keep in mind is a credit gap that exists among small businesses today, as described by Karen Mills, a senior fellow at Harvard Business School and former administrator of the U.S. SBA.

“There is no doubt that online lenders have identified an important segment that is not getting enough access to credit, but data also shows that borrowers are less satisfied with the interest rates and repayment terms from online lenders than from traditional banks. So even if small businesses are getting the loan, if it is not at an appropriate price, we should still consider this a credit gap,” Mills said.

Future Plans

While loans could be the next growth phase for ShopKeep Capital, this could be one of many new directions that the payments company takes. For instance, with key competitor Square, which boasts a market cap of approximately $10 billion, in pursuit of obtaining a bank charter, they could have company someday.

“It’s an interesting idea. It’s still very early for us but we’re not ruling anything out at this point,” DeSimone said.

For the near term, however, he is focused on ShopKeep Capital, for which he expects to make a couple of key hires for soon. “In my mind, this helps us to be more competitive with Square. I think it’s a really good service for our customers and it fits very well into the other pieces of our business,” said DeSimone.

You’re Under Arrest: Funder Takes Extreme Measures to Counter Data Theft

September 4, 2017

An employee of Yellowstone Capital was arrested last month, according to a source who witnessed the events. At the company’s behest, local police entered Yellowstone’s Jersey City office and handcuffed a female employee who was believed to be engaged in the theft and misappropriation of financial data.

A spokesperson for Yellowstone would not comment on the events nor release the name of the accused. AltFinanceDaily nevertheless obtained a photo of the individual being escorted out by police. We’ve blurred out her face to protect her identity. Several of those present, who spoke on the condition of anonymity, said that she had been employed by the company for several years.

When asked more generally about the risks of data leakage in the industry, Yellowstone Capital CEO Isaac Stern said that his company is operating on the edge of hyper vigilance. “Yellowstone is investing tons of time, money, and effort to prevent data theft,” Stern said. “We are doing everything in our power, everything, to address it, and we have even enlisted the assistance of an outside security firm.”

The incident does not stand alone. Last year, a man on Long Island pled guilty to attempted criminal possession of computer related material after being implicated in a merchant cash advance backdooring scheme.

Backdooring is industry jargon for when a broker submits a potential deal to a funder and that file ultimately leaks out to third parties whom the broker did not authorize to handle the information. Often times brokers will point their fingers at the funder for mismanaging data they suspect is escaping out the back door. Such accusations can be detrimental to a funder’s reputation not only with the broker community but also with customers they advance funds to. That’s why some funders are taking data security to new levels.

Greenbox Capital, for example, a funder in Miami, FL told AltFinanceDaily back in March that their company designed proprietary software to monitor the actions of all users on their system, which allows them to know who clicked on what when, and for how long. They also developed algorithms to detect suspicious behavior and their security team receives an alert whenever it gets triggered. Greenbox had initially conducted a 90-day probe and discovered that two employees were stealing data. They don’t want that to ever repeat itself.

Using a cell phone to take pictures of confidential data may not help rogue employees evade detection, according to several funders who have said there are methodologies to spot this behavior but declined to explain what they are. And the risk of getting caught may not merely be termination, as evidenced by arrests that have taken place thus far. These funders say there have been other arrests over the last few years but that the companies did not want to draw attention to them.

Indeed, of the two backdooring-related arrests AltFinanceDaily has reported on now, neither would officially confirm them.

“We take ISO information extremely serious,” Yellowstone’s Stern explained, lamenting that the value of deal data can inevitably foster rogue behavior, which they are constantly monitoring for.

Put another way, the personal information of a single performing client could be worth as much as $10,000 or more if it gets into the wrong hands. That’s because it could be used to offer that client a loan, advance or other service. The profit could come in the form of a commission, interest, RTR, a closing fee, or even something more nefarious like stealing their identity.

“We know about the pressure people face to illegally transmit data,” Stern said. “They think we don’t know, but we know the industry. Ultimately we will catch you.”

Credibly Selected to Service Bizfi’s $250M Portfolio

August 30, 2017

Credibly also announced that it has crossed the $500 million milestone in capital deployed to tens of thousands of SMBs across the U.S. This is separate from the $250M portfolio the company is now servicing from BizFi.

“Acquiring the servicing rights of BizFi’s portfolio is a testament to our data-driven approach and laser focus on the working capital needs of small businesses,” said Ryan Rosett, Credibly’s Founder and Co-Chief Executive Officer. “We welcome our new customers and are committed to ensuring that their growth capital needs are met.”

In addition to servicing the BizFi portfolio, Credibly is working with both sales partners and merchants to provide additional working capital to the businesses in BizFi’s portfolio. Credibly’s data science team has the ability to analyze BizFi’s twelve years of data and remittance history, which will allow Credibly to better service both the BizFi and Credibly portfolios. Further, BizFi’s data enhances Credibly’s risk management, scoring models, and portfolio management tools.

The Small Business Association (SBA) estimates that traditional banks still reject approximately 90 percent of SMB loan applications. Since 2010, Credibly has emerged as a proven platform that leverages data science and analytics to provide SMBs with a simple and intuitive way to access critical working capital. The company addresses the fundamental capital needs of SMB owners across a broad credit spectrum and through every stage of a business’s life cycle.

Main Street SMBs across a wide variety of industries that include restaurants, retail stores, salons, spas, dry cleaners, auto body shops, and doctors’ offices, all rely on Credibly to secure the necessary capital they need to grow.

Credibly has achieved widespread industry recognition for its risk management, data technology, and data driven approach. For more information on Credibly, please visit www.credibly.com.

About Credibly

Founded in 2010 and with offices in Michigan, Arizona, Massachusetts, and New York, Credibly is a best-in-class Fintech platform that leverages data science and analytics to improve the speed, cost, and choice of capital available to small businesses in the United States. Credibly is dedicated to creating a superior customer experience that meets the needs of all small businesses, regardless of product need or credit profile.

Learn more at www.credibly.com. Follow Credibly @credibly360.

Media Contact:

Tracy Rubin / Olivia Levis

JCUTLER media group

323-969-9904

tracy@jcmg.com / olivia@jcmg.com