Russian Startup Blackmoon Wants to Play Middleman in Marketplace Lending

July 6, 2016Russian startup Blackmoon, that screens other company’s loans before selling them to investors, has launched in the US, drawn to the lure of its $1 trillion addressable market. Blackmoon aims to reach a billion dollar in loans by the end of 2017 and is targeting business, consumer, student and car loans.

The company provides ‘marketplace lending as a service’ working as a middleman between debt investors, lenders as well as banks. Its platform brokers deals between balance sheet lenders and investors. The company was founded in Moscow City last year by investor and entrepreneur Oleg Seydak. Seydak was a partner at venture capital fund Flint Capital and managing director of private equity firm FINAM Global.

Cofounder Ilya Perekospky in an interview with Venturebeat said that the US market is ripe with opportunity for companies like Blackmoon. “We believe that existing marketplace lenders have only scratched the surface with respect to the volume of loans being originated in the U.S. today,” he said. “The size of the marketplace lending market is measured in billions of dollars, whereas balance-sheet lender loan origination volume is nearly a trillion U.S. dollars or more.”

Split-Funding MCA and Daily Debit Loans Are Spreading Across the World

July 4, 2016

When banks say no, merchants all over the world are getting funded via non-bank alternatives that resemble products here in the USA. In Hong Kong for example, a special administrative region of China, there are non-bank businesses that offer merchant cash advances and/or daily debit loans.

Having had the opportunity to visit with some of those funders there last week, I was surprised to learn that we spoke the same language. By that I mean that they price deals with factor rates, work with local finance brokers, underwrite files using recent bank statements, do site inspections and more. They even a have decision issued by the highest court in the land that declared merchant cash advances to be purchases, not loans.

Even the pitch is basically the same. “Banks aren’t lending to small businesses,” I heard time and time again in Hong Kong. And that’s probably not going to change any time soon. While the non-bank business financing scene is starting to take off, merchant cash advances in particular have been around there for about seven years already.

Hong Kong’s population is a little less than a third of the size of Australia, where many US-based funders have been expanding to over the last couple years.

OnDeck’s New Marketing Channel: Accountants

June 27, 2016What if accountants replaced loan brokers?

OnDeck has been on it. The New York-based online lending company unveiled a new medium of reaching potential borrowers. Through its ‘Accountant Advisor Program,’ launched in March this year, the lender wants to reach small businesses through accountants, bookkeepers and CPAs.

OnDeck is rolling out the program in Kentucky, Florida and Alabama and recruiting accountants in these states to refer their clients to OnDeck. What do they get in exchange? They can either choose to get a revenue share of 5 percent of the total loan volume, or have OnDeck give the small business a 2 percent discount on the loan cost for loans of up to $500,000 with terms of 3 to 36 months and lines of credit ranging from $6,000 to $100,000.

“We’ve put this program together, realizing that the accountant community is the most trusted advisor to small business,” said Frank Orofino, director of the OnDeck Accountant Advisor Program was quoted as saying.

The company isn’t shaken by the troubled environs of online lending. Earlier this month, (June 16th), the company expanded its operation in Denver buying a bigger office space and hiring staff along side forging new partnerships.

“I think it’s a smart idea to partner with CPAs,” said Justin Benton who runs Lenders Marketing, a lead generation site for loans. “These are people who are helping with taxes and investments. They are going straight to the horse’s mouth,”

Will this new channel yield results?

The Unsung Disruption in Online Lending – Stacking, Litigation and Questionable Debt Negotiators

June 22, 2016

Give a small business two options, a low APR 3-year business loan and a short term loan with a high factor rate, and you’ll find advocates for each product arguing over which is better and why. We’ve been led to believe that it’s one versus the other, that one is good and one is bad, and that’s all there is to the story. Entire business models have been developed along the lines of this thinking, algorithms deployed and merchants funded, along with narratives framed in the mainstream media about why one system is superior to others.

But to hear the men and women in the phone rooms tell it, when given a choice between one funding option or the other, small businesses are often choosing both at the same time. Reuters said that stacking is the latest threat to online lenders, and in many ways they’re right. The practice isn’t new of course, the tendency for merchants to take on multiple layers of capital (often times in breach of other contracts) has been a central cause of tension between funding companies for the last few years. But the reason the story is bubbling over into traditional news media now as the latest threat, is because opponents of stacking assumed that the practice would be eradicated by now. There was this false sense of hope that government agents in black suits would show up one day unannounced after hearing that a merchant had taken a third advance or loan despite having not yet satisfied the obligations of the previous two. And when that didn’t happen, some of the models heralded as better for the merchant started to show cracks. What happens to the forecasts when the merchants priced ever so perfectly for a low rate long term loan go and take three or four short term loans almost immediately after? Back in October, Capify CEO David Goldin argued that long dated receivables were already dangerous to a lender regardless because the economy could turn south. “You’re done. You’re dead. You can’t save those boats. They are too far out to sea,” he told AltFinanceDaily.

Sue everyone?

When it comes to disruption, nothing has changed the game as much as stacking, and companies must prepare for the likelihood that it could be around forever. That means forming a long-term business model that is equipped to deal with this practice. Several lawsuits have been waged in an attempt to generate case law to deter it, including one filed last year in Delaware by RapidAdvance against a rival. Patrick Siegfried, assistant general counsel of RapidAdvance told the Wall Street Journal last fall, “we’re doing it to establish the precedent,” he said. “This kind of thing is happening more and more.” At the time, a motion to dismiss the case entirely was pending. RapidAdvance since won that motion but only by a hair and with a judge that was very reluctant to move the case forward.

Last October, MyBusinessLoan.com, LLC, also known as Dealstruck, sued five companies at once, a mix of lenders and merchant cash advance companies after one of their borrowers defaulted, allegedly because of actions carried out by the co-defendants. They were greeted with several motions to dismiss for failure to state a claim.

Even if these funding companies don’t win, simply letting the world know that they’ll sue rivals for stacking can act as a deterrent. But it’s an expensive tactic, especially when some defendants are more than happy to litigate the claims. Litigation is definitely an underrated cost of doing business for online lenders and merchant cash advance companies. In one recent case, a merchant challenged the legitimacy of a contract with Platinum Rapid Funding Group, a company whom they sold a portion of their future receivables to. The merchant asked the judge to recharacterize the contract to a loan so that they could try to use a criminal usury defense. The judge refused in a well-written decision that called the merchant’s attempt to do that “unwarranted speculation.” But even with the precedent of a favorable ruling, countless merchants have attempted to come up with strategies to wriggle their way out of their agreements, sometimes with ample legal counsel at their side.

Debt negotiators and questionable characters

Stacking has become a cost of doing business, but something else is creeping in as well. An entire cottage industry of “debt negotiators” has set their sights on online lenders and merchant cash advance companies, and at times these self-professed business experts don’t even realize there’s a difference between the two. One MCA funder told altfinancedaily earlier this week that a merchant in default claimed to be represented by Second Wind Consultants, a debt restructuring firm that lists one Don Todrin as the CEO on their website. Not mentioned among Todrin’s accolades is that he is a disbarred attorney who pled guilty to federal bank fraud charges in 1994, according to an old report by the Boston Globe, after he filed at least nine false financial statements to acquire $1.4 million in loans.

Another purported debt negotiation firm, who has the irked the ire of merchant cash advance companies, is apparently trying to assert affiliation to a native American tribe and invoke tribal immunity in response to lawsuits against them, according to court filings in New York State.

And only three weeks ago, an attempted class action against a merchant cash advance company failed because each named class representative had waived its right to participate in a class action in exchange for business financing. The initial action, before being moved to federal court, was brought by a merchant represented by an attorney who had just been reinstated to practice law, following a long suspension for pleading guilty to identity theft.

On top of it all, there are merchants themselves that act in bad faith, with some preying on the perceived vulnerabilities of an online-only experience. In the November/December 2015 issue of AltFinanceDaily Magazine, attorney Jamie Polon said some applicants don’t even own businesses at all, they just pretend to. “They’re not just fudging numbers – they’re fudging contact information,” he told AltFinanceDaily. “It’s a pure bait and switch. There wasn’t even a company. It’s a scheme and it’s stealing money.”

Weeding out bad merchants is a job for the underwriting department but for the good merchants seemingly deserving of those 3-5 year loan programs, the future is not as easy to predict as it once was. They might stack regardless, no matter how favorable the terms are. And given that government agent ninjas aren’t likely to drop down from the sky to stop them any time soon, many funding companies are faced with hard choices. Are the initial forecasts still valid? Is it economically feasible to turn the client away for additional funds because they breached their original agreement, all while the cost to acquire that customer in the first place was really high? Do you sue your rivals, make them look bad in the press, or lobby for regulations that will hurt them? How do you handle the new breed of debt negotiators who use the same UCC lead lists as lenders and brokers?

Sure, things like marketing costs are going up and the capital markets are less inviting than they used to be. But once loans and deals are funded, making sure those agreements are lived up to can take time, resources, and undoubtedly a lot of lawyers. And realistically, these issues aren’t likely to change any time soon. Help, in whatever relief form some are hoping for, is not on the way. How’s that for disruption?

Starting an ISO Shop? Here’s What You Need to do Differently

June 17, 2016 It’s not news that commercial finance brokers are hurting and some are even calling it quits. The industry that didn’t ask for more than a phone and a sharp sales acumen from anyone wanting to start an ISO shop is now stifled with competition. The low barriers to entry that welcomed new companies is causing a seismic shift in the way brokers do business. While some are ready to leave, most are still grappling with the changing times.

It’s not news that commercial finance brokers are hurting and some are even calling it quits. The industry that didn’t ask for more than a phone and a sharp sales acumen from anyone wanting to start an ISO shop is now stifled with competition. The low barriers to entry that welcomed new companies is causing a seismic shift in the way brokers do business. While some are ready to leave, most are still grappling with the changing times.

What’s different about the business now? Almost everything, some say. Gil Zapata who runs a four year old ISO shop, Lendinero, says clients were desperate for money when he started. However he doesn’t think of the competition as fierce but just messy. “There are brokers and ISOs entering and clogging up the system,” he said, “They are obviously fly-by-night and get pulled into it thinking the industry is a fast money maker but it’s really not.”

Competition did what competition does, drove prices and commissions down, costs up and hacked the product. For instance, daily payment ACH loans strongly tied to historical cash flow history didn’t exist. Neither did fancy verbiage for them. The onslaught of online lenders that entered the industry didn’t help either.

OnDeck started selling term loans, which had some similarities to other daily payment products, said Chad Otar, founder of New York-based MCA company Excel Capital Management. “ISOs, on their part have to be careful while pitching these products to clients, explain the contract clearly to avoid penalty.”

The competition has also led to loan stacking, much to brokers’ and lenders’ contempt. And the online lending ilk of Lending Club, Prosper and OnDeck cannot escape it either. Last week, (June 10th), Reuters ran an article calling stacking the latest threat to online lenders where “soft credit inquiries” and “patchy reporting” results in multiple lenders making loans to the same borrower, diminishing the ability to pay.

“Deals become impossible to structure and it becomes difficult for lenders to keep clients on the books when there are second and third names,” said Zapata. The proliferation of loan products that succeeded as a result of competition was a double edged sword. While there are more products to be sold, there are not enough borrowers to lend to.

From a funder’s perspective, that means acquiring and retaining a customer on price rather than an ongoing relationship. “The increased competition has led to commoditization of the MCA,” said Sol Lax, CEO of New York-based business funder Pearl Capital. “It was an exotic financial instrument 5 years ago and the ability to set up shop was restricted. That has changed.”

The ISOs are increasingly reliant on renewals, thanks to the high marketing costs. “A real differentiating factor is whether an ISO syndicates, their default rate, and their renewal rate. All of it is intertwined so that ISOs need to view their business more like investors and less like brokers,” Lax said.

So what would ISOs have done differently? Otar says he would have started an industry coalition similar to the Innovative Lending Platform Association. “I would have tried to pull a Godfather and formed a coalition with other companies and self regulate.”

For Zapata, doing things differently would have meant finding an early backer. “If I had to do this over, I’d have a good investor behind my back,” he said. “Find someone who knows the business and have a good game plan. If you don’t have deep pockets, your chances are minimal.”

Balance Letters, Payoff Letters, And Not Letting Go

June 10, 2016

The following is a guest-authored opinion piece on the business financing space

Everyone is struggling to keep their head above the water. Just imagine the scene in the movie Titanic. Currently we are in the scene where they zoom out to show the ship sinking slowly with more people in the water trying to survive than on the ship. “Never letting go” is something everyone is doing and clinging on to whatever floats is the only way to survive. The decline in submissions and quality of funded deals is one aspect that many Funding Companies are realizing. No one is letting go of a piece of their portfolio without a fight.

For many A/B paper (for those who go by the grade system) or the Prime to Sub-Prime, 1st position companies know what I am talking about and it’s time to come clean on the truth and the real perception of why things are the way they are.

You can’t get that payoff letter because that Funding Company does not want to let go of their good paying Merchant. Whether the funding was originated from a Broker or organically, that Business is in bed with that funding company and did not have any intention of breaking a relationship until the option was brought to their attention. Whether this Merchant was solicited by another Broker or the Merchant decided to take it upon themselves to seek additional funding, there is one thing that will most often happen.

As soon as the Funding Company receives a request for a payoff letter or balance letter, they will ask why it is needed or delay the process in releasing one or not give one at all until the Merchant is 100% positive and the reasoning and demand is final. Is there anything wrong with this?

To a Broker? Yes. To a Business Owner? No. As many Brokers will fight and try to justify the circumventing of their Merchants, in this case, this is not circumventing at all. The Business has a contract with the Funding Company and until they have a zero balance, that Funding Company has the right to review their account and offer additional funds or discounts to keep their business. This is how it is with any company. Try calling your cable company to cancel your service. What do they do first? They transfer you to the reconciliation department to try to appease you, offer you free or discounted features, and find out what they did wrong or what company you are switching to. Companies are always trying to improve their service and give their clients the best experience.

Throughout the years, if the original Funding Company could offer a better rate or term than what the competing offer is, it has always been in the best interest of the Merchant to continue with that original Funding Company. It is NOT in the best interest nor is it ethical to put the Merchant in another position that will hurt the business or “double up” contracts to equal an amount if ONE company cannot adhere to the request. “Stacking” by offering a second position is one thing, squeezing in as many positions is another, and over time it has hurt many 1st position Funding Companies.

Fast forward to now, the rise in funded accounts that have “defaulted” may have fallen victim to the promises of something better. There is no one educating or clearing the air that there probably isn’t something better… but that advice won’t make anyone commissions and those Funding Companies still rely on Brokers to bring in submissions.

There has been no recourse on this issue, rather growth, and those who have paved the way have found their path covered in dirt. Stomping in this path are other funding companies who have adopted practices from veterans but feel the need to set hierarchy to something they can’t control.

So, with that said, who really sets the rules to what is fair when we are all walking on egg shells? The cost of acquiring a customer and the cost of losing one is an expensive and tricky loss. It is safe to say that once a Merchant is stacked- there is no going back. Should ethics rule over the choices and fate of a Business? Should we put more emphasis on realistic expectations before and after a Business is funded?

A simple request for a payoff letter can open a can of worms. The underlying factors of the difficulties companies face in our industry are all brought upon by the decisions we make when working with each Merchant. At the end of the day you have to ask yourself- am I helping or am I hurting the Business?

‘As Reality Kicks in, Companies Have to be Discplined,’ Says Fora Financial’s Dan Smith

May 25, 2016

Starting a financial company couldn’t have come at a more inauspicious time for two friends that have known each other since college. Jared Feldman and Dan Smith started Fora Financial in June 2008 and today their company has provided $450 million to over 9,500 small businesses. It recently launched PRISM, a proprietary scoring and decisioning framework and secured a credit facility. Founders Smith and Feldman spoke to AltFinanceDaily about working with Palladium, recent industry news and did some crystal ball gazing. Below is an excerpt from the interview

What does the industry look like to you, with its myriad of players and the recently surfaced problems?

JF: There are a lot of players but I don’t know how much business they are originating. It might sound greater than it actually is. While there is no doubt that competition exists, it is still from the usual cast of characters who have been around for quite some time. However the competition is driving up acquisition costs, possibly some irrational buying from some companies which then trickles down and causes some ISOs and brokers to fail.

DS: Our competitors and we have felt things change in the market in terms of regulation and capital. The influx of capital that came in with the new players is starting to contract a little bit and the lending companies like ourselves are controlling the amount they lend. There has been a lot of artificial growth in the industry – a lot of companies trying the test and learn strategy to see how deep they can buy into the market but they struggle to maintain profits.

And what will be the aftermath of these changes we see in the next six to twelve months?

DS: The reality is starting to kick in and companies will have to be disciplined about their underwriting models and be wise about where they spend their money in order to to grow and sustain profits.

What then should be the top priority for lenders now?

JF: Two top priorities that lenders should focus on is A) To build out a compliance framework and B) securing a long-term credit facility apart from the already mentioned disciplined underwriting making risk, analytics and data capabilities strong.

You started working with private equity firm Palladium last year. Tell us more about where you are with that?

DS: We got into this great partnership and a fund of theirs gave us the capital to grow our business and it aligned with everything we had in our 100 day plan – we wanted to build our regulatory compliance framework, close on a credit facility and bring some key people onboard — all of which we have accomplished. Working with Palladium teaches us how to run a disciplined company and we have already been entertaining M&A opportunities.

What do you think of the hybrid model approach that some lenders take ?

DS: Hybrid model is a great idea in theory and there are concerns with every approach — of holding everything on balance sheet and then buyers buying the loans. There is a lot that goes into capital raising and we have done what we know well and have continued to organically grow our balance sheet. It’s not to say that we have not considered other options but for now, we are focused on getting the right cost structure.

JF: If you have the credit facility with the right cost structure, that is a cheaper cost of capital than what the marketplace is selling these loans for but we are considering options for diversifying our capital sources and we would like to add some kind of market element but that might be in the future. Maybe in the first quarter of 2017.

Online Lending APR ‘SMART Box’ To Apply To Loans, Not Merchant Cash Advances

May 5, 2016

OnDeck, Kabbage and CAN Capital have launched an initiative to make online loan shopping easier. Dubbed the SMART (Straightforward Metrics Around Rate and Total Cost) Box, these lenders plan to present small businesses “with a chart of standardized pricing comparison tools and explanations, including various total dollar cost and annual percentage rate metrics that enable a comprehensive pricing comparison of loans of equivalent duration.”

The Box, clearly meant to increase transparency, was explained in an ironically confusing way, particularly where it said it would include annual percentage rate metrics. An Annual Percentage Rate (APR) is indeed a representation of several metrics and thus it wasn’t clear if the Box would just include some of these individual metrics and conveniently leave out the APR itself.

OnDeck CEO Noah Breslow for example told Forbes only six months ago that annual terms don’t make sense. “The APR overstates the actual cost of the loan to the borrower,” he said. He was not alone in thinking that way. Several studies have concluded too that merchants don’t always even know what APR represents. Lendio for example, found that two-thirds of small businesses selected the total dollar cost of a loan as the easiest to understand. Only 17.4% said the APR was the easiest.

And there’s another thing, the fact that CAN doesn’t just do loans, they also do a significant amount of merchant cash advances. What role could an APR have there? While the Box’s final system won’t be decided until after the conclusion of a 90-day national engagement period that begins next month, one can only imagine that it might have a Schumer Boxer feel to it.

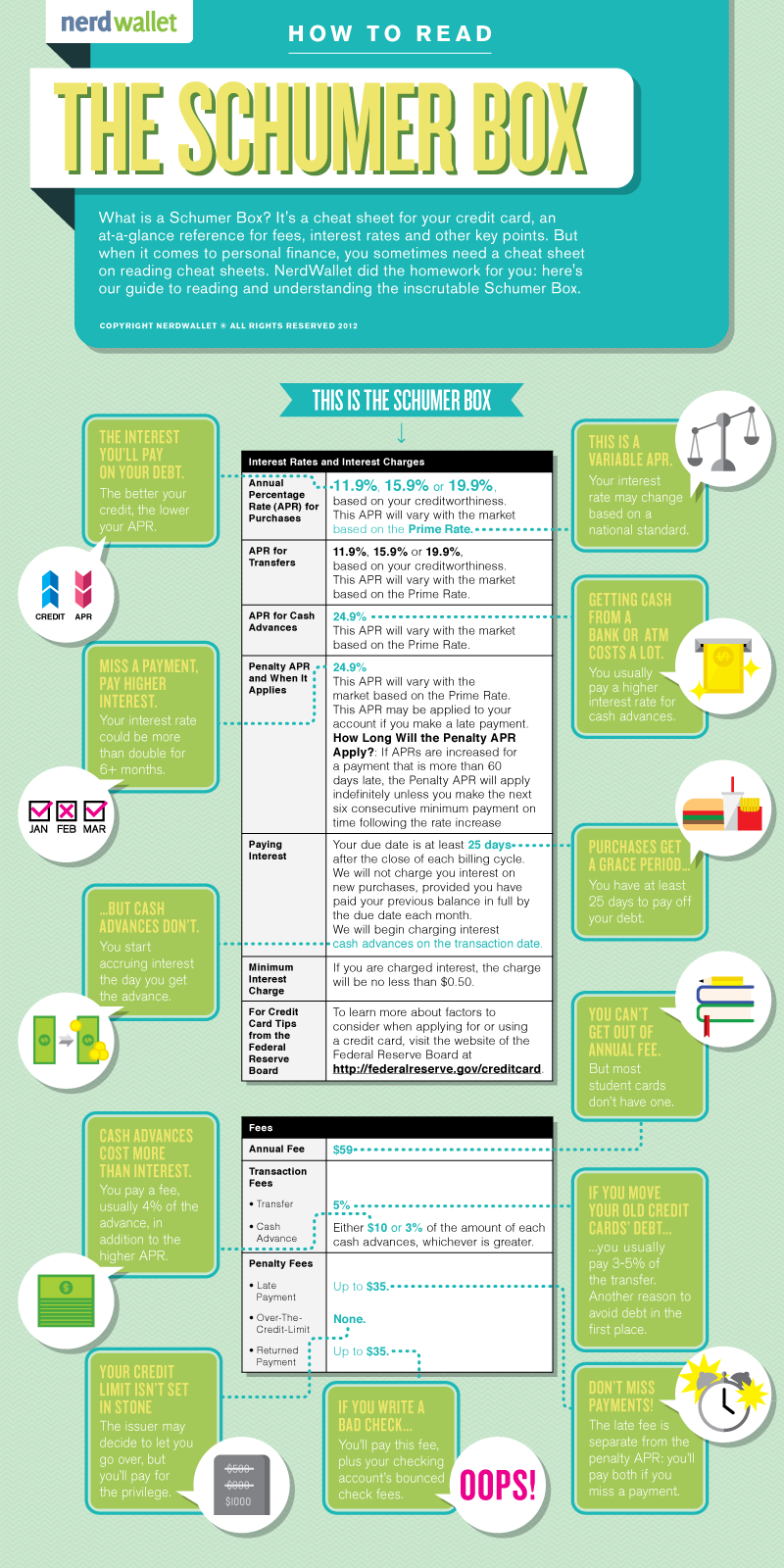

A Schumer Box explained:

Via: NerdWallet

The syntactic ambiguity in the announcement however was unintentional. A spokesperson for the group (Known as the Innovative Lending Platform Association) said that the SMART Box will indeed include Annual Percentage Rates.

But that’s where loans are concerned…

When AltFinanceDaily asked about merchant cash advances, Daniel Gorfine, vice president and associate general counsel of OnDeck; Parris Sanz, Chief Legal Officer of CAN Capital and Azba Habib, assistant general counsel of Kabbage, submitted the following joint response:

“As part of the SMART Box initiative, we are interested in engaging with providers of MCA products. Based on consistent assumptions about a small business’s future sales volumes and its ability to deliver the contracted amount of receivables within the period of time estimated during underwriting, the SMART Box could apply to MCA products.”

So long as SMART Box disclosure is voluntary, an MCA company could perhaps employ their own version of it. It just might come sans APR given the product’s history with state regulations. The Association is emphatic however that this concept could be used by MCA companies and others in the small business financing space. After all, the initiative is rooted in transparency for the small business owner, they say.

In September, the Association “will encourage those interested in promoting the responsible development of the small business lending industry to voluntarily adopt or support the model disclosure.”

Given the level of influence these companies have on the industry, the voluntary nature of the SMART Box has the potential to spark an industry-wide box revolution. MCA companies however would need to structure transparent disclosure around their contractual frameworks. But even that could be a good thing. One commercial financing broker for example, posted a redacted service fee agreement to the DailyFunder forum earlier this week that purported to show another broker trying to charge a merchant a 26% premium (26% of the funding amount) for their work. Despite this unusually high cost, the charge itself was hard to find, hidden among fine print on an otherwise benign looking page. Naturally, others in the industry did not respond kindly to it. Even other brokers referred to it as “outrageous,” “nonsense,” or “bs.”

Their reactions make clear that there is a desire for transparency even among the group most often blamed for the lack thereof. Some of the industry’s forward thinkers have told AltFinanceDaily that a system like a SMART Box is the future of the industry whether one agrees with it or not. And if not for the sake of small businesses and regulators, then for the sake of being able to compete fairly against companies that may be relying on truly hidden fees.

SMART Box. All aboard the transparency train?