Stacking Lawsuit Results in Settlement Before Trial

June 19, 2018A lawsuit between RapidAdvance and Pearl Capital over tortious interference will not be going to trial after all, AltFinanceDaily has learned. Originally scheduled to begin on June 25th, the parties have reportedly reached a settlement.

Neither party would respond for comment.

RapidAdvance filed its lawsuit against Pearl in November 2015 with the hope that they could set a precedent against “stacking.”

The suit was filed in the Circuit Court of Maryland under Small Business Financial Solutions, LLC v. Pearl Beta Funding, LLC, Case No. 411478-V.

Woman Arrested in Connection With Finance Company Data Theft

June 19, 2018 A woman was arrested in the Bronx this morning and charged with felony computer-related theft. The individual, whose name AltFinanceDaily is not releasing until more information is known, was reportedly stealing customer data from Yellowstone Capital despite not being employed there. The photo shows police officers escorting her out from her home.

A woman was arrested in the Bronx this morning and charged with felony computer-related theft. The individual, whose name AltFinanceDaily is not releasing until more information is known, was reportedly stealing customer data from Yellowstone Capital despite not being employed there. The photo shows police officers escorting her out from her home.

She is the third person to be arrested for stealing data from Yellowstone Capital in the last nine months but she’s the first that was not actually working there at the time.

Yellowstone Capital is arguably the largest merchant cash advance company in the country, according to AltFinanceDaily’s leaderboard. The companies ranked ahead of them are lending companies, not MCA.

Second Annual Alternative Finance Bar Association Conference Draws Lawyers from Afar

June 11, 2018 Attorneys who represent alternative finance companies congregated in New York on Friday for the second annual conference of the Alternative Finance Bar Association (AFBA.)

Attorneys who represent alternative finance companies congregated in New York on Friday for the second annual conference of the Alternative Finance Bar Association (AFBA.)

They came for a day of learning about the latest legal developments pertaining to alternative finance, and MCA in particular. Seminars at the conference had names like: “Credit Facilities 101: What an Alternative Finance Company Can Expect,” “Syndication Relationships: Partner? Participant? Investor?” and “Bankruptcy Developments: The Rise of the Adversary Proceeding.”

“I think it’s like heaven for a new attorney in the MCA world,” said Judith Ramos, who is Corporate Counsel at McKenzie Capital in the Miami area.

Another attorney somewhat new to the MCA space and eager to learn more was Alexis Shapiro, General Counsel at Forward Financing in Boston.

“This was one stop shopping to learn about the latest legal developments in the MCA industry,” Shapiro said.

In one seminar, called “Updates on Recent Case Law,” attorney panelists Steven Berkovitch of ABF Servicing and Adam Stein and Christopher Murray of Stein Adler Dabah and Zelkowitz, discussed the positive impact of the Pearl Beta Funding v Champion Auto Sales decision in New York. They spoke about how judges have dismissed lawsuits against their MCA clients by referencing this decision, which establishes that MCA deals are not loans.

Murray reviewed the current climate with regard to MCA cases in New York, California, Texas and Utah. And one panelist emphasized the importance of simply being knowledgeable about the industry by relating a story of an MCA defense lawyer who, when asked by a judge about the interest rate on a particular MCA deal, fumbled and gave a percentage. (MCA deals do not have interest rates given that payments are subject to change over time).

Later, Gregory Nowak, a partner at Pepper Hamilton, entertained the crowd with a few jokes before diving into the details and the risks of syndication. The conference was held at New York offices of Pepper Hamilton, with expansive views of the Hudson River.

Later, Gregory Nowak, a partner at Pepper Hamilton, entertained the crowd with a few jokes before diving into the details and the risks of syndication. The conference was held at New York offices of Pepper Hamilton, with expansive views of the Hudson River.

“We are energized by the response of so many attorneys from different backgrounds in this emerging and evolving industry,” said one of founders of the AFBA, Lindsey Rohan, General Counsel at Platinum Rapid Funding Group in Long Island.

AFBA’s other founders are Kate Fisher, partner at Hudson Cook outside of Baltimore, Patrick Siegfried, Assistant General Counsel at Rapid Advance in Bethesda, MD, and Murray, attorney at Stein Adler outside of New York City.

Robert Cook, one of Hudson Cook’s founding partners, was at the conference. He told AltFinanceDaily that he remembered back in 2006 when an investment bank client asked his firm to do due diligence on a merchant cash advance company.

Robert Cook, one of Hudson Cook’s founding partners, was at the conference. He told AltFinanceDaily that he remembered back in 2006 when an investment bank client asked his firm to do due diligence on a merchant cash advance company.

“We didn’t know what that was,” Cook said. “The client looked around for a law firm that had experience with MCAs. They couldn’t find any. So they came back to us and said, ‘You’re going to have to learn.’”

More than a decade later, MCA is no longer so obscure and the AFBA has at least three more planned events in 2018. The next event will be a cocktail reception on October 24th.

For more information, contact: Tiffany@LRohanlaw.com

AltFinanceDaily was also a sponsor of the second annual AFBA conference.

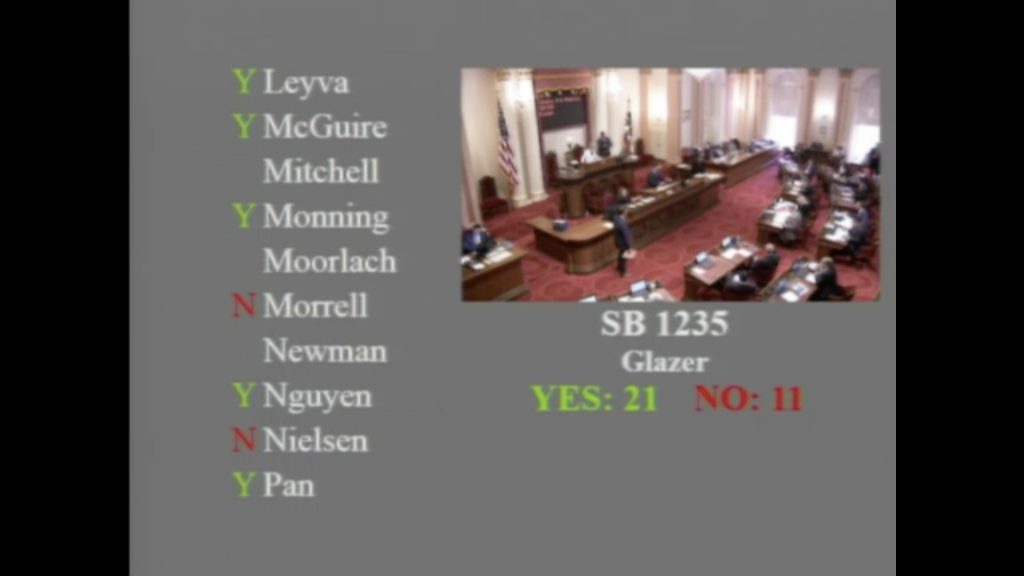

Commercial Financing Disclosures Bill Approved in the CA Senate

May 31, 2018The use of an annualized cost metric on loan and non-loan contracts alike is now one step closer to becoming the law in the State of California. On Thursday, SB 1235 was approved on the Senate floor. The bill calls for commercial finance companies to disclose an Estimated Annualized Cost of Capital. In previous hearings, the bill’s author, Sen. Steve Glazer (D), stated that it was his intention that this apply to merchant cash advances as well.

“This estimate includes all charges and fees incurred for the financing, assuming you make all payments when scheduled and adhere to the terms of the agreement. This number is based on the estimated term. If the actual term is shorter than estimated, the annualized cost of capital may be higher than shown. If the actual term is longer than estimated, the annualized cost of capital may be lower. This is not an Annual Percentage Rate (APR).”

Here is how to calculate the Estimated Annualized Cost of Capital as set forth in the bill:

Here is how to calculate the Estimated Annualized Cost of Capital as set forth in the bill:

(1) Divide the total dollar cost of financing by the total amount of funds provided.

(2) Multiply the result in paragraph (1) by 365.

(3) Divide the result from paragraphs (1) and (2) by the term or estimated term of the financing in days.

(4) Multiply the result from paragraph (3) by 100.

(5) The result from paragraph (4) shall be labeled “The Estimated Annualized Cost of Capital.”

In addition, commercial finance companies will also have to disclose the total dollar cost of the transaction and the total amount of money the merchant will receive net of all fees.

The bill must now pass through the solidly Democrat-controlled Assembly and be signed by the Governor to become the law.

Uplyft Updates Logo and More

May 31, 2018 Uplyft Capital announced the launch of its new branding yesterday, including a new logo and website.

Uplyft Capital announced the launch of its new branding yesterday, including a new logo and website.

“We were looking for a sleek, stylish icon that would have brand recognition in the industry as simple and fun, but also uplifting,” said CEO Michael Massa.

The rising purple arrow represents growth for small businesses, “looking to get out of the current box they are in,” according to the press release.

“All of our online portals have been revamped and redesigned,” Massa said, “our client, investor and partner portals.”

Massa prides the company he founded in 2012 for its innovation. Uplyft, which provides cash advance exclusively, uses Artificial Intelligence for underwriting and signing up new ISO partners electronically.

“We need to evolve in order to keep up with demand,” he told AltFinanceDaily.

Uplyft has a direct sales team of about 25 people and roughly 500 ISO sales partners, according to Massa. Headquartered in Miami, the company employs about 45 people altogether with a small office of three people in New York.

Why Small Businesses Sought Financing in 2017, and Why They Were Denied

May 24, 2018 Nearly 60 percent of small businesses applied for financing in 2017 because they wanted to expand their business or pursue new opportunities, according to the latest report by the Federal Reserve. Forty-three percent of small businesses sought financing for operating expenses while 26 percent sought capital for refinancing. Nine percent had a different reason.

Nearly 60 percent of small businesses applied for financing in 2017 because they wanted to expand their business or pursue new opportunities, according to the latest report by the Federal Reserve. Forty-three percent of small businesses sought financing for operating expenses while 26 percent sought capital for refinancing. Nine percent had a different reason.

Of course, not all applications are funded. Forty-six percent of small businesses received all the financing they sought, 12 percent received most (more than 50 percent) of it, 20 percent received some (less than 50 percent) of the financing they desired and 23 percent were denied financing altogether.

Of the reasons why merchants were denied funding, “Having insufficient credit history” ranked number one, according to the report. A very close second was “Having insufficient collateral,” followed by “Having too much debt already.” After that, in descending order, came “Low credit score,” “Weak business performance” and “Other.”

The “Having insufficient collateral” category does not apply for MCA financing, but the other categories do. According to Nick Gregory, founding partner at Central Diligence Group, which provides MCA underwriting services, “Having too much debt already” is perhaps the main reason why merchants seeking cash advances get declined.

“A lot of times the merchants are overleveraged,” Gregory said.

He explained that if a merchant also has something like two MCA arrangements (or positions) already, that merchant likely has taken on too many contractual obligations which will often be a reason to decline the application. In Gregory’s experience, another common reason for declining an MCA financing application is “Weak business performance.”

Contradictory to the Federal Reserve report’s top reason for denying financing to a small business borrower, Gregory said that “Having insufficient credit history” is seldom a reason to deny MCA financing. This disconnect likely comes from the fact that the report includes all types of small business financing, with MCA accounting for just seven percent. The number maybe seem small, but it continues to increase while small business applications for factoring have decreased.

BFS Co-founder Returns as Temporary CEO

May 23, 2018 Chairman and co-founder of BFS Capital Marc Glazer has assumed the role of Interim CEO. The former CEO, Michael Marrache, is no longer at the company.

Chairman and co-founder of BFS Capital Marc Glazer has assumed the role of Interim CEO. The former CEO, Michael Marrache, is no longer at the company.

“We’re on a nationwide search to find an individual that we feel will be an excellent candidate to continue BFS’s track record as a market leader and help grow the company,” Glazer said.

Founded in 2001, BFS is a veteran in the merchant cash advance industry. More than five years ago, the company began offering a business loan product, which now accounts for more than half of its revenue.

Glazer told AltFinanceDaily that when BFS started offering its loan product, it widened its customer base significantly such that a sizable percentage of its customers are now business to business companies. Glazer said that MCA funding would not work for these kinds of customers because many of them get paid by check or get paid in larger amounts, but not on a daily basis.

Glazer said that working with ISO partners has always been a critical part of the BFS business model. What does Glazer look for in an ISO?

“Ultimately, you want to work with ISOs that view the relationship with not only the funder, but the merchant, [in mind,]” he said. “We look at ourselves as a responsible funder and put out offers that we not only think help the merchant, but that have payment terms that the merchant can afford. And the ISOs that we look for are ones that do the same kind of matching with the merchant.”

BFS has funded 400 different types of merchants, from florists to nail salons. But Glazer said that a big portion of the company’s customer base comes from either the hospitality industry or parts of the construction industry, including plumbing. To date, BFS has delivered more than $1.75 billion in total financing to small and mid-sized businesses, including $300 million funded in 2017. Loans are typically offered through the company’s banking partner, Bank of the Internet, according to Glazer.

BFS is headquartered in Coral Springs, FL and has an office in New York and one in southern California. It also includes a wholly owned subsidiary in the UK called Boost Capital. Altogether, BFS employs about 200 people with the majority of employees at its Florida office.

Sneaky Debt Settlement Company Temporarily Restrained by Judge

May 20, 2018 A debt settlement company has sunk to new lows, according to a petition filed by Yellowstone Capital in Nassau County. Defendants SMCA, Inc. DBA Settle My Cash Advance, Thassos.com Corp DBA Thassos.com, and George Alexander, have been accused of fraudulently transferring funds owed to Yellowstone Capital to themselves while trying to mask the evidence in the process.

A debt settlement company has sunk to new lows, according to a petition filed by Yellowstone Capital in Nassau County. Defendants SMCA, Inc. DBA Settle My Cash Advance, Thassos.com Corp DBA Thassos.com, and George Alexander, have been accused of fraudulently transferring funds owed to Yellowstone Capital to themselves while trying to mask the evidence in the process.

Unlike other purported debt settlement schemes, the Settle My Cash Advance defendants are alleged to have first actively coached a merchant to hide his money in new bank accounts rather than pay his judgment. This, according to emails attached as exhibits, included instructions by the defendants on how to cover up the paper trail so that the money could not be traced. Once this was successfully carried out, the defendants then absconded with the merchant’s money, leaving him broke and the judgment still unpaid.

According to the merchant’s sworn affidavit, Settle My Cash Advance lured him into believing that they not only had a relationship with Yellowstone but that they would also reduce the judgment entered against his business by 25% – 70%.

“SMCA (Settle My Cash Advance) told me to transfer all funds, as my business and I earned them, to SMCA to hold them for us so that Yellowstone could not collect on its judgment,” the merchant wrote. “The deal that SMCA represented to me was that SMCA would take the funds, hold them in trust, and use them to settle our obligations with Yellowstone for a small contingency fee.”

What happened instead is that the defendants ran off with the money held in trust and did nothing to help with Yellowstone, the documents say.

Presented with the facts laid out before it, the Court ordered that the funds held by Settle My Cash Advance be restrained pending a May 30th hearing.