Layoffs, Big Losses for OnDeck in Q4

February 16, 2017 OnDeck weathered a brutal fourth quarter driven largely by an increase in provision for loan losses which increased to $55.7 million, up from $20.0 million in the comparable prior year period. $18.7 million of this can be attributed to loans with original maturities of 15 months or longer whose performance has deviated or is expected to deviate, the company said. “As a result, the Provision Rate in the fourth quarter of 2016 was 10.2% compared to 5.6% in the comparable prior year period,” the company reported. For the full year of 2016, the Provision Rate was 7.4%, compared to 5.8% in 2015. CFO Howard Katzenberg said on the earnings call that it will likely continue to hover at around the 7% level.

OnDeck weathered a brutal fourth quarter driven largely by an increase in provision for loan losses which increased to $55.7 million, up from $20.0 million in the comparable prior year period. $18.7 million of this can be attributed to loans with original maturities of 15 months or longer whose performance has deviated or is expected to deviate, the company said. “As a result, the Provision Rate in the fourth quarter of 2016 was 10.2% compared to 5.6% in the comparable prior year period,” the company reported. For the full year of 2016, the Provision Rate was 7.4%, compared to 5.8% in 2015. CFO Howard Katzenberg said on the earnings call that it will likely continue to hover at around the 7% level.

The company lost $36.5 million in Q4 and $86.5 million for the year.

To try and turn things around, OnDeck is laying off up to 11% of their staff as part of a “cost rationalization plan.”

James Hobson, their COO, recently announced his resignation and March 15th is his last official day.

On the earnings call, Katzenberg wouldn’t say how many loans in their portfolio were 15 months or longer, but did say that it’s more than a third of their book. This is notable given that this segment is the one in which performance isn’t matching their models and led to the recalibration of loss expectations.

Meanwhile CEO Noah Breslow explained that losses did not stem from their partnership with Chase since Chase held all those loans on their own balance sheet. Breslow said their role in that relationship is servicing.

No origination channel was directly responsible for the loss provision increase. One analyst surmised if perhaps third party brokers or funding advisors, as OnDeck calls them, might be responsible, but the company said that origination channel wasn’t a factor.

Despite the fact that OnDeck is now using the 5th generation of their proprietary OnDeck Score, they were unable to predict performance on loans that now make up more than a third of their portfolio, yet the company said they remain very confident in their scoring model.

“Loans sold or designated as held for sale through OnDeck Marketplace represented 15.8% of term loan originations in the fourth quarter of 2016 compared to 39.8% of term loan originations in the comparable prior year period,” the company reported.

As NY Lending License Proposal Looms, Industry Trade Groups Mobilize

February 13, 2017

The alternative small-business finance community plans to lobby hard against a far-reaching proposed expansion of the New York state lending license. The proposal calls for any person or company that solicits, arranges or facilitates business and consumer loans – or other types of financing – to obtain a license. That could include MCA companies, business loan brokers and ISOs.

Critics claim the expansion, which Governor Andrew M. Cuomo included in his proposed state budget, could trigger a series of ominous and possibly unintended events in the courts and on Wall Street. “It could destroy the industry if the worst comes to fruition,” declared Robert Cook, a partner at Hudson Cook LLP.

Some opponents also contend that the public hasn’t had a reasonable opportunity to respond. “Sneaking a provision with significant impact like this into the budget and not going through regular order is really disturbing,” said Dan Gans, a Washington lobbyist who also serves as executive director of the the Commercial Finance Coalition. “They should allow all the stakeholders to have their voices heard.”

The industry’s trade groups have been quick to react. The Small Business Finance Association has been in contact with New York state legislators to help them understand the ramifications of the proposal, according to Stephen Denis, the trade group’s executive director. Meanwhile, Gans is recommending that the CFC’s board hire an Albany lobbying firm to help advance the industry’s interests.

New York’s current consumer licensing law is written broadly enough to cover any loan to an individual for less than $25,000, even if it’s made for commercial purposes, said Cook. That means the current law could cover loans to sole proprietorships but would not affect loans to corporations, limited liability companies, partnerships or limited liability partnerships, he noted.

Under the proposal in Governor Cuomo’s budget, any type of commercial loan of up to $50,000 would require a license, Cook said. Today, the state requires a license only if a loan carries a simple interest rate of more than 16 percent. Under the budget proposal, all lending would require a license, even if the interest rate is less than 16 percent. Loans made by alternative funders typically carry interest rates of 36 percent to 100 percent, he said.

Under the proposal in Governor Cuomo’s budget, any type of commercial loan of up to $50,000 would require a license, Cook said. Today, the state requires a license only if a loan carries a simple interest rate of more than 16 percent. Under the budget proposal, all lending would require a license, even if the interest rate is less than 16 percent. Loans made by alternative funders typically carry interest rates of 36 percent to 100 percent, he said.

New York already has a criminal usury rate of 25 percent, but lenders have two methods of avoiding that cap, according to Cook. Under one method, the parties to the loan can use a provision called the “choice of law clause” and thus agree that the contract is subject to the laws of a state that does not limit commercial usury rates, he said. Or, using the second method, the small-business finance company can solicit the loan and refer it to a bank in a state without a cap. The bank makes the loan but then sells the loan back to the small-business finance company or an affiliate, he noted.

But adopting the changes proposed in the New York budget could possibly stymie both methods of circumventing the state’s usury laws. Consider the choice of law clause, Cook suggested. The courts could interpret the proposed expansion as an effort by the state to gain more control of commercial lending. That could prompt the courts to refuse to enforce choice of law clauses involving New York state because doing so would violate a significant policy in New York, he maintained. The proposal could also gut the second way around the usury law – the bank model – by requiring employees of out-of-state banks to have a license in order to originate loans or by prohibiting rates in excess of New York’s cap, he said. Both outcomes are speculative but constitute distinct possibilities, he added.

Expanding the license would also grant additional regulatory authority to the New York State Department of Financial Services, Cook maintained. Besides requiring the license, the DFS would have the ability to regulate, supervise and examine commercial lenders, he said. In the past the department has imposed some significant regulations on licensees, including fair lending requirements and cyber security requirements, he said. “They’re a very active regulator,” he contended. “They could require commercial lenders to jump through a lot of hoops that aren’t there today.”

Expanding the license would also grant additional regulatory authority to the New York State Department of Financial Services, Cook maintained. Besides requiring the license, the DFS would have the ability to regulate, supervise and examine commercial lenders, he said. In the past the department has imposed some significant regulations on licensees, including fair lending requirements and cyber security requirements, he said. “They’re a very active regulator,” he contended. “They could require commercial lenders to jump through a lot of hoops that aren’t there today.”

What’s more, time would pass while a company negotiates the initial hoops simply to obtain a license. Qualifying for the current New York license, for example, can take up to nine months, Cook said. “It’s a fairly intensive licensing process that requires a lot of information about the company, the officers and directors of the company,” he noted. “The licensing process is tough in New York.”

The expansion could also limit the industry’s access to capital, Cook warned. Some alternative funders raise money by selling loans or interests in loans on the secondary market. Requiring a license to buy those products could prompt Wall Street to look elsewhere for less-burdensome investment opportunities, he said.

The laundry list of potential bad effects has many in the industry wondering about the state’s intentions toward the industry. “It’s not clear whether the people up in Albany understand the potential effect this has,” Cook said.

To help bring about that understanding, the CFC intends to call upon its members and merchants who have benefitted from alternative finance to visit officials in the state capital, Gans said.

Gans finds reason for optimism as the associations coalesce around the issue. The state Senate in Albany tends to be pro-business, and I am confident we will find allies that will stand up to this, he said.

Denis also seems upbeat about the industry’s efforts to make itself heard in Albany. In Illinois, some legislators failed to differentiate between consumer loans and commercial loans when considering legislation last year, he noted. That might be the case in New York, too, and the SBFA might help them make the distinction, he said. As an example of the differences, he pointed out that business loans often carry high interest rates because of high risk. “We have talked to some folks in Albany, and everyone is receptive to the industry,” he said. Small business is a powerful constituency, he maintains.

Gans, Denis and Cook all said they’re not opposed to legislation or regulation that addresses problems caused by bad actors in the industry, but all three oppose government action that they believe unnecessarily limits members of the industry who are operating in good faith.

The proposed license in New York differs in at least one significant way from the California lending license that many alternative funders have obtained, Cook noted. The California license doesn’t impose a cap on interest rates, he said. If the New York proposal imposed licensing requirements but did not limit interest rates, the industry probably would reluctantly accept it, he suggested.

—-

Dan Gans at the CFC can be contacted at dgans@polariswdc.com

Stephen Denis at the SBFA can be contacted at sdenis@sbfassociation.org

Robert Cook at Hudson Cook can be contacted at rcook@hudco.com

Analysis: New York’s Lender/Broker Licensing Proposal

February 7, 2017

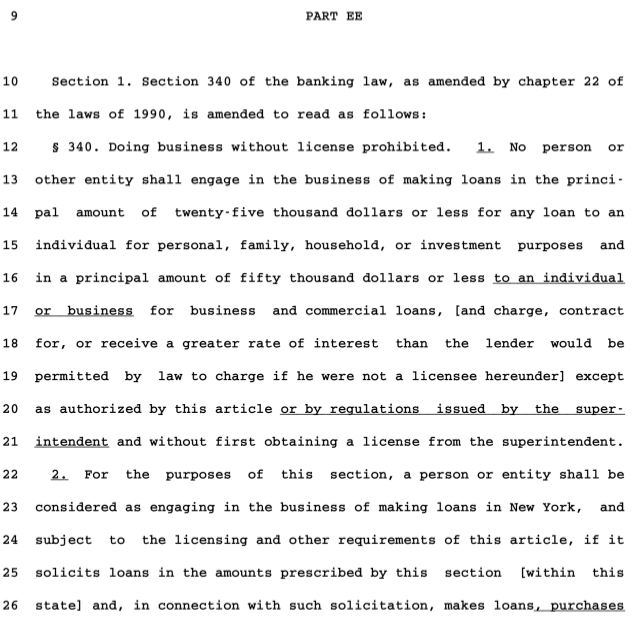

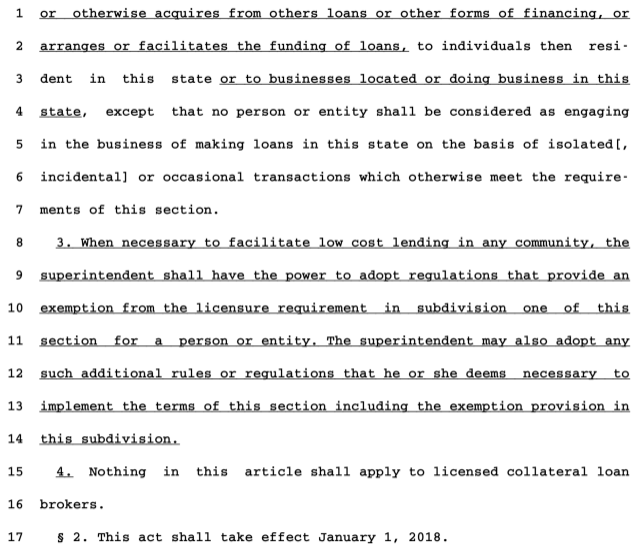

New York Governor Andrew Cuomo’s proposed budget includes a legislative proposal to “allow the Department of Financial Services (“DFS”) to better regulate the business practices of online lenders.”1 This legislation, which would amend Section 340 of the Banking Law, could have a dramatic impact on lending and brokering loans to New York businesses, as such lenders would have to obtain licenses to engage in business-purpose lending and could only charge rates and fees expressly permitted under New York law.2 It may impact the secondary market for merchant cash advances. If passed, the licensing requirements will take effect January 1, 2018.

The proposed law would amend NY Banking Law § 340 to require anyone “engaging in the business of making loans” of $50,000 or less for business or commercial purposes to obtain a license. The term “engaging in the business of making loans” means a person who solicits loans and, in connection with the solicitation, makes loans; purchases or otherwise acquires from others loans or other forms of financing; or arranges or facilitates the funding of loans to businesses located or doing business in New York.

Although the proposed law would require a license only for a person who “solicits” loans and makes, purchases or arranges loans, the DFS takes the position that the licensing law (as currently enacted) applies broadly and that “out-of-State entities making loans to New York consumers . . . are required to obtain a license from the Banking Department.”3 As a result, there is probably no exemption from licensing for a person who does not “solicit” loans in New York.

The potential impact of the legislation is significant.

Potential Impact on Lenders:

Licensing Required and Most Fees Prohibited. New York law already requires a lender to obtain a license to make a business or commercial loan to individuals (sole proprietors) of $50,000 or less if the interest rate on the loan exceeds 16% per year, inclusive of fees. The proposed law would require any person who makes a loan of $50,000 or less to any type of business entity and at any interest rate to obtain a license. And a licensed lender is governed by New York lending law that regulates refunds of interest upon prepayment;4 and significantly limits most fees that a lender can charge to a borrower, including prohibiting charging a borrower for broker fees or commissions and origination fees.5

Essentially, the DFS will regulate lenders who originate loans to businesses of $50,000 or less in the same manner as consumer loans of less than $25,000. The proposed law would exempt a lender that makes isolated or occasional loans to businesses located or doing business in New York.

Potential Effect on Choice-of-Law. The proposed law could lead courts to reject contractual choice-of-law provisions that select the law of another state when lending to New York businesses. With new licensing requirements and limits on loans to businesses, a court could reasonably find that New York has a fundamental public policy of protecting businesses from certain loans, and decline to enforce a choice-of-law clause designating the law of the other state as the law that governs a business-purpose loan agreement.

For example, the holding of Klein v. On Deck6 might have come out differently if New York licensed and regulated business loans at the time the court decided it. In the Klein case, a business borrower sued On Deck claiming that its loan was usurious under New York law. The loan contract included the following choice-of-law provision:

“[O]ur relationship including this Agreement and any claim, dispute or controversy (whether in contract, tort, or otherwise) at any time arising from or relating to this Agreement is governed by, and this Agreement will be construed in accordance with, applicable federal law and (to the extent not preempted by federal law) Virginia law without regard to internal principles of conflict of laws. The legality, enforceability and interpretation of this Agreement and the amounts contracted for, charged and reserved under this Agreement will be governed by such laws. Borrower understands and agrees that (i) Lender is located in Virginia, (ii) Lender makes all credit decisions from Lender's office in Virginia, (iii) the Loan is made in Virginia (that is, no binding contract will be formed until Lender receives and accepts Borrower's signed Agreement in Virginia) and (iv) Borrower's payments are not accepted until received by Lender in Virginia.”

The court concluded that this contract language showed that the parties intended Virginia law to apply. However, the court also considered whether the application of Virginia law offended New York public policy. The court compared Virginia law governing business loans against New York law governing business loans, and decided that the two states had relatively similar approaches. As a result, the court found that upholding the Virginia choice-of-law contract provision did not offend New York public policy.

The loan amount in the Klein case was above the $50,000 threshold for regulated loans in the proposed New York law, so this exact case would not have been affected. However, the court’s analysis in the Klein case would have been the same for loans of $50,000 or less. Accordingly, the new law could cause a New York court to reject a contractual choice-of-law provision.

Effect on Bank-Originated Loans. This proposed law apparently would not directly affect loans made by banks that are not subject to licensing under the statute.7 But, the law would require non-banks that offer business-purpose lending platforms that partner with FDIC-insured banks to obtain a license to “solicit” loans. And, it is possible, that the DFS could later, by regulation or examination, prohibit such licensees from soliciting loans at rates higher than permitted under New York law.

Potential Impact on Merchant Cash Advance Companies:

The proposed law imposes a license requirement if a person “purchases or otherwise acquires from others loans or other forms of financing.” New York law does not define the term “other forms of financing.” However, the DFS may consider merchant cash advance transactions to be a regulated transaction for which licensing is required.

As written, only purchasing or acquiring other forms of financing, such as a merchant cash advance, might require a license. As a result, the proposed law only has the potential for affecting the sale and syndication of merchant cash advances. It is unclear whether buying only a portion of a merchant cash advance, or “participation” could require a license, or if only purchasing the entire obligation could require a license.

Potential Impact on Brokers:

Because the new law would require a license to “arrange or facilitate” a business loan of $50,000 or less, ISOs and loan brokers would need a license. As mentioned above, a licensed lender is prohibited from charging broker fees or commissions. It is not clear at the moment whether an ISO or loan broker could contract directly with the borrower for a commission.8

1 See https://www.budget.ny.gov/pubs/executive/eBudget1718/fy18artVIIbills/TEDArticleVII.pdf, page 243. Although not discussed in this article, the proposal would also impose new licensing requirements on certain consumer lenders.

2 A licensed lender may impose a rate in excess of the 16% civil usury limit in New York, but is still subject to the 25% criminal usury limit. See, New York Banking Law § 351(1) and New York Penal Law § 190.40.

3 See http://www.dfs.ny.gov/legal/interpret/lo991206.htm The term “solicitation” of a loan includes any solicitation, request or inducement to enter into a loan made by means of or through a direct mailing, television or radio announcement or advertisement, advertisement in a newspaper, magazine, leaflet or pamphlet distributed within this state, or visual display within New York, whether or not such solicitation, request or inducement constitutes an offer to enter into a contract. NY Banking Law § 355.

4 NY Banking Law § 351(5).

5 NY Banking Law § 351(6).

6 Klein v. On Deck Capital, Inc., 2015 N.Y. Misc. LEXIS 2231 (June 24, 2015).

7 See NY Banking Law § 14-a; 3 NY ADC 4; NY Gen. Oblig. Law § 5-501.

8 See NY Gen. Oblig. Law § 5-531 that limits fees that brokers can charge on non-mortgage loans to not more than 50 cents per $100 loaned.

Katherine C. Fisher is a partner in the Hanover, MD office of Hudson Cook, LLP. Kate can be reached at 410-782-2356 or by email at kfisher@hudco.com.

OnDeck’s COO Announces Resignation Prior to Q4 Earnings

February 3, 2017OnDeck COO James Hobson notified the company on Friday that he is resigning to “pursue another opportunity.” According to the 8-K filed with the SEC, it will become effective on March 15, 2017.

Hobson started at OnDeck in 2011 and became the COO in 2012.

The announcement comes weeks before OnDeck is expected to disclose their Q4 and full-year 2016 report. In Q3, the company had shifted to keeping more loans on their own balance sheet, while increasing their reliance on third party brokers for business. They had also reported a GAAP net loss of $16.6 million for the quarter, bringing the 2016 Q1 – Q3 total losses to $47.1 million.

New York’s Proposed Budget Slips In Sweeping Regulation of Non-bank Business Lending and Finance

January 28, 2017In New York, Governor Cuomo’s 309-page budget proposal includes a handful of sentences tucked in towards the end (Part EE) that would revise Section 340 of the state’s banking law. And the implications are broad, given that it calls for any person or entity involved in the soliciting, arranging or facilitation of business and consumer loans or other forms of financing to be licensed in order to engage in such activity. It appears that MCA companies as well as business loan brokers and ISOs would be directly impacted.

If it passes, the regulator tasked with overseeing that would be the New York Department of Financial Services. It would be effective January, 2018.

For consumer loans, it applies to loans $25,000 and under. For business financing, $50,000 and under.

AltFinanceDaily’s Top 10 Most Read Stories of 2016

December 28, 2016

If 2015 was the year of the broker, well then 2016 was the year of readjusted expectations. The following are the top 10 most read stories of 2016 per our online analytics, some of which surprised even us. Either way, here’s what you read and shared on our website the most in 2016 in descending order:

10: Do Bank Statements Matter in Lending? Business Lenders and Consumer Lenders Disagree

A 2015 story, it was the 10th most read in 2016. One thing the lending revolution has taught us is that a borrower’s bank statements can mean everything or nothing at all.

9: Should I start an ISO with only $2,000?

Even though this was published two full years ago, it managed to be the 9th most read story of 2016. The short answer to this question is no, don’t start an ISO with such a small budget especially not in 2016 or 2017.

8: Lending Club Class Action Lawsuit Predicated on Madden v Midland Risk

A big story early in the year was Madden v Midland, and the impact an appellate court ruling could have on marketplace lenders who rely on chartered banks to make loans for them in 50 states. This particular post and related ones attracted a lot of readers in 2016.

7: Business Loan Brokers and MCA ISOs Call it Quits

For the first time ever, brokers and ISOs began to say farewell to an industry faced with oversaturation.

6: Merchant Cash Advance Accounting – A How To Guide

Published two full years ago, the merchant cash advance accounting guide managed to be the 6th most read article on AltFinanceDaily in 2016. The article is meant for MCA funders bookkeeping, not for merchants who use merchant cash advances.

5: Lending Club Borrowers Are Paying Off Really Early – And There’s Something Weird About It

Lending Club’s loan borrowers pay off their loans early at a freakish level. I pondered this in a blog post in February and the trend has not changed. To date, I’ve had 975 borrowers pay off early, nearly double since the time this was published.

4: Platinum Rapid Funding Group Sets Annual Funding Record

An astounding amount of visitors were interested in Platinum Rapid Funding Group’s 2015 origination volume. An announcement that the company had originated $100 million in deals was the 4th most read story of 2016.

3: Merchant Cash Advance Definitely NOT a Loan, New York Judge Rules

Yet another post referencing Platinum Rapid Funding Group, was a decision issued in a New York trial court. In it, a judge opined at length about the nature of purchasing future receivables.

2: Shakeup at CAN Capital – CEO and 2 other Execs Put on Leave of Absence

Despite being less than a month old, this story on its own was the 2nd most read of 2016, technically followed by this one and this one, both also about CAN’s recent issues. We combined them into one story for the purpose of this list since they were all related to the same event.

1: The Closer – Meet the Yellowstone Capital Rep That Originated $47 Million in Deals Last Year

The #1 most read story on AltFinanceDaily in 2016 was a profile about a salesman at Yellowstone Capital. Juan Monegro, who originated $47 million worth of deals in 2015, was also recently reported to have matched that number again in 2016.

The Twelve Days of Funding

December 20, 2016

On the Twelfth day of funding, my true love gave to me

Merry Christmas, Happy Hanukkah and may all your deals fund!

A Q4 To Remember – A Timeline

December 18, 2016In case you haven’t noticed, it’s been an interesting few months for alternative finance. The below timeline is an expanded version of what appears in the print version of our Nov/Dec magazine issue.

9/27 Able Lending secured $100 million in debt financing

9/30 The FTC won a judgement of $1.3 billion against payday loan kingpin Scott Tucker, its largest ever award through litigation

10/11 The United States Court of Appeals for The District of Columbia ruled the CFPB’s organizational structure unconstitutional. To remedy, the agency will either have to convert its one-person directorship to a multi-member commission or the director will have to report to the President of the United States. The CFPB is appealing the decision.

10/13 Affirm secured $100 million in debt financing

10/14

- CircleBack Lending was reported to have ceased lending operations

- Goldman Sachs unveiled its new online consumer lending division, Marcus

10/20 CommonBond secured a $168 million securitization deal

10/24 Bizfi announced that John Donovan had joined the company as CEO. Donovan was the COO of Lending Club from 2007 to 2012.

10/25

- Expansion Capital Group announced new management team. Vincent Ney, the company’s majority shareholder became the CEO

- Lendio raised $20 million through a new equity round led by Comcast Ventures and Stereo Capital

- Lending Club announced its foray into the $1 trillion auto refinancing market

11/1

- Cross River Bank raised $28 million in equity led by Boston-based investment firm Battery Ventures along with Silicon Valley venture capital firms Andreessen Horowitz and Ribbit Capital

- Square beat earnings estimates and extended $208 million through 35,000 loans in Q3

11/3

- OnDeck announced earnings, continued use of balance sheet to fund loans and extended $613 million in Q3

- Independent merchant cash advance training course goes live, allowing brokers and underwriters to earn a certificate

11/4 SEC concluded its investigation into Lending Club

11/7 Lending Club announced earnings and a deal to sell $1.3 billion worth of loans to a National Bank of Canada subsidiary

11/8 CFG Merchant Solutions secured a $4 million revolving line of credit

11/9 Donald Trump became the President-Elect

11/11

- Fintech leader Peter Thiel joins the executive committee of Trump’s transition team

- Kabbage appointed Amala Duggirala as Chief Technology Officer and Rama Rao as Chief Data Officer

11/14 Prosper’s CEO Aaron Vermut, stepped down

11/16

- UK-based p2p lender Zopa applied for a banking license

- Small business lender Dealstruck reportedly ceases lending operations

- Former Lending Club CEO revealed to be launching a new rival, Credify

11/17

- LiftForward secured a $100 million credit facility

- Prosper filed their Q3 10-Q, revealing that they only originated $311.8 million in loans for the quarter compared to $445 million in Q2

- The IRS sent a broad request to Coinbase, the nation’s largest bitcoin exchange, as part of a hunt for tax evaders

- PeerStreet raised a $15 million Series A funding round led by Andreessen Horowitz

11/18 P2Bi raised $7.7 million in venture financing

11/22 LendIt announced the first ever industry awards event

11/29 Three C-level executives at CAN Capital are placed on a leave of absence after the company identified assets that were not performing as expected

12/2

- Total Merchant Resources secures $20 million in private equity, launches wholesale funding division

- Bitcoin-based P2P lending platform BitLendingClub shuts down

- OCC announces they are moving forward with a special purpose national charter for fintech companies

12/8 Former CEO and co-founder of World Wrestling Entertainment tapped to run Small Business Administration

12/9 OnDeck announced new $200 million revolving credit facility with Credit Suisse

12/12 Knight Capital Funding announced new Chief Data Scientist

12/13 Fifth Third Bank is reported to buy a stake in franchise marketplace lender ApplePie Capital

12/14 BlueVine raised $49 million in Series D funding

12/15

- Swift Capital named Tim Naughton as Chief Legal Officer

- John MacIlwaine, Lending Club’s Chief Technology officer, submitted his resignation to the company to pursue another opportunity

12/16 CAN Capital is reported to have laid off more than 100 employees