CFPB to Collect Data on Small Business Lending, Implement Section 1071 and Circulate RFI

May 10, 2017

Update: We are streaming the hearing LIVE on our home page.

Update: You can download the CFPB’s Request for Information here. A transcript of Cordray’s prepared remarks are at the bottom of the page.

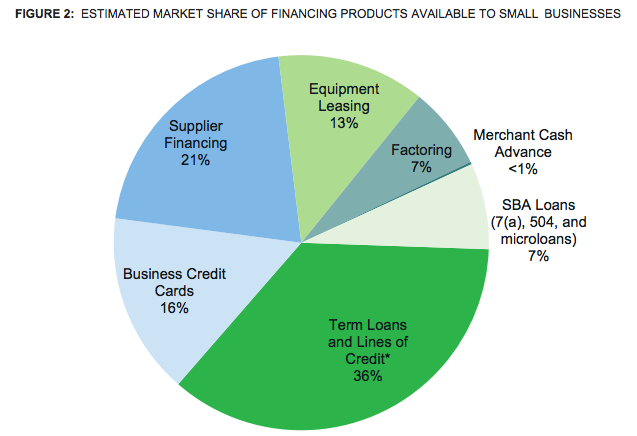

Update: CFPB White paper estimates that merchant cash advances are less than 1% of the small business finance market on an aggregate dollar volume basis, factoring 7%, and equipment leasing 13%. They estimate that the small business financing market is roughly $1.4 trillion in size. They also estimate that there are less than 1.5 million merchant cash advance “accounts” in the US, more than 6 million term loan accounts, and more than 7 million factoring accounts.

Update: The CFPB is releasing a Request for Information (RFI), asking industry participants to define a small business, explain where small businesses seek financing and the kinds of products that are made available to them, reveal the categories of data that small business lenders are using and maintaining, and to provide input on privacy implications that may arise from disclosing information to the CFPB.

Update: The CFPB is indeed announcing their plans to implement Section 1071 of Dodd-Frank.

Beginning at 1:45PM EST on Wednesday, the CFPB will be holding a hearing in Los Angeles on small business lending. According to the agenda, “the hearing will feature remarks from Director Cordray, as well as testimony from consumer groups, members of the public, and industry representatives.”

Sources contend that the director will use the hearing as an opportunity to announce the agency’s plans for the implementation of Section 1071 of Dodd-Frank which grants the CFPB the authority to collect data from small business finance companies. Some critics have characterized the law as an attempt to push affirmative action into small business lending, while others worry the CFPB will attempt to exceed its statutory authority and exact penalties based on the data it collects.

Unless Trump fires Cordray for cause, the director’s term will continue until July 2018.

industry representatives making remarks at the hearing include:

- Todd Hollander, Managing Director, Union Bank

- Makini Howell, Executive Chef and Owner, Plum Restaurants, and Main Street Alliance Member

- Kate Larson, Director, U.S. Chamber of Commerce

- Elba Schildcrout, Director of Community Wealth, East Los Angeles Community Corporation

- Josh Silver, Senior Advisor, National Community Reinvestment Coalition

- Robert Villarreal, Senior Vice President, CDC Small Business Finance

If possible, we will attempt to embed the live stream on our site.

Full transcript of Cordray’s prepared remarks below

Thank you all for coming. It is good to be here again in Los Angeles. Today, the Consumer Financial Protection Bureau is announcing an inquiry into ways to collect and publish information about the financing and credit needs of small businesses, especially those owned by women and minorities. We are well aware of the key role they play in our lives. Small businesses help drive America’s economic engine by creating jobs and nurturing local communities. It is estimated that they have created two out of every three jobs since 1993 and now provide work for almost half of all employees in the private sector. Yet we perceive large gaps in the public’s understanding of how well the financing and credit needs of these entrepreneurs are being served.

As you probably know, Congress provided the Consumer Bureau with certain responsibilities in the area of small business lending. And there is a strong logic behind this. When I served as the Ohio Attorney General, we recognized the need to protect small businesses and nonprofit organizations by accepting and handling complaints on their behalf, just as we did for individual consumers – an approach that proved to be very productive. In addition, the line between consumer finance and small business finance is quite blurred. More than 22 million Americans are small business owners and have no employees. And, according to data from the Federal Reserve, almost two-thirds of them rely on their business as their primary source of income.

Congress specifically has charged the Consumer Bureau with the responsibility to administer and enforce various laws, including the Equal Credit Opportunity Act. Unlike other consumer financial laws, the ECOA governs not only personal lending, but some commercial lending as well. In fact, we have now conducted a number of ECOA supervisory examinations of small business lending programs. Through that work, we are learning about the challenges financial institutions face in identifying areas where fair lending risk may exist, and we are assisting them in developing the proper tools to manage that risk.

In the Dodd-Frank Wall Street Reform and Consumer Protection Act, Congress took a further step to learn more about how to encourage and promote small businesses. To help determine how well the market is functioning and to facilitate enforcement of the fair lending laws, Congress directed the Consumer Bureau to develop regulations for financial institutions that lend to small businesses to collect certain information and report it to the Bureau. The Request for Information we are releasing today asks for public feedback to help us better understand how to carry out this directive in a way that is careful, thoughtful, and cost-effective.

***

We have considerable enthusiasm for this project. In my own case, I have seen firsthand how small business financing can have a big economic impact. When I served as the Treasurer of Ohio, we had a reduced-interest loan program to support job creation and retention by small businesses. The way the program worked was that the state could put money on deposit with banks at a below-market rate of interest, and this deposit was then linked to a same-sized loan to a small business at a correspondingly below-market rate. This so-called “Linked Deposit” program had been authorized more than twenty years earlier, but had gradually fallen into disuse.

At its core, however, the program made good sense. Small businesses are often in desperate need of financing to update and expand their operations, and if they can get inexpensive financing, they often can fertilize their ideas for growth and be even more successful. So we diagnosed the program and found that after its initial success, it had become too bureaucratic. We heard from both banks and businesses that the program, which was still paper-based, was so slow and cumbersome that nobody wanted to use it.

So we changed all that. We put the process online, rebranded it as the “Grow Now” program, and made specific commitments to those who wanted to participate in it. We told them they could fill out a typical application in 30-60 minutes, and we promised them they would have a yes-or-no answer on their application within 72 hours. That was not easy, and it required very close coordination with the banks that took part in the program. But we did it, and the “Grow Now” program really took off. Only about $20 million had been allocated when we started, but in less than two years we deployed more than $350 million, helping about 1,500 small businesses create or retain approximately 15,000 jobs across the State.

It was also exciting and interesting to see how the businesses were able to use the loan funds. I can recall a construction business in northeast Ohio that needed a loan to buy a large piece of equipment so the company could compete for new and different jobs. They got the money, they got the equipment, and they thrived. I recall a manufacturer in northern Ohio that needed money to turn their factory sideways on their property so they could utilize more space and employ more people. We funded the build-out, they executed on it, and they met their goals for growth of output, revenue, and jobs. And I recall a company in western Ohio that started out as a caterer, began making their own tents for events, recognized that they might be able to succeed as tentmakers, and needed financing to be able to bid on a major project with the U.S. Department of Defense. We got them the loan, they got the bid, and Inc. magazine named them one of its 500 fastest-growing businesses of that year!

***

The moral of this story is that business opportunity – especially opportunities for small businesses – often hinges on the availability of financing. People have immense reserves of energy and imagination. Human ingenuity is the overwhelming power that allows human beings to reinvent the future and make it so. These forces unleash what Joseph Schumpeter called the “gales of creative destruction” that constantly mold and reshape the patterns of our economic life. Innovation has sharpened our nation’s economic edge for generation after generation, but when credit is unavailable, creativity is stifled.

To make the kind of meaningful contributions they are capable of making to the American economy, small businesses – particularly women-owned and minority-owned businesses – need access to credit. Without it, they cannot take advantage of opportunities to grow. And with small businesses so deeply woven into the nation’s economic fabric, it is essential that the public – along with small business owners themselves – can have a more complete picture of the financing available to this key sector.

Some things we do know. We are releasing a white paper today that lays out the limited information we currently have about key dimensions of the small business lending landscape. According to Census data, and depending on the definition used, there are an estimated 27.6 million small businesses in the United States. We estimate that together they access about $1.4 trillion in credit. Businesses owned by women and minorities play an especially important role in this space. Women-owned businesses account for over one-third (36 percent) of all non-farming, private sector firms. The 2012 Survey of Business Owners, the most recent such information available, indicates that women-owned firms employed more than 8.4 million people, and minority-owned firms employed more than 7 million people. Those are huge numbers: by comparison, in 2014 fewer than 8 million people were employed in the entire financial services sector.

When small businesses succeed, they send constant ripples of energy across the economy and throughout our communities. For example, a 2013 study by the Federal Reserve Bank of Atlanta found that counties with higher percentages of their workforce employed by small businesses showed higher local income, higher employment rates, and lower poverty rates. In order to succeed, businesses need access to financing to smooth their cash flows for current operations, meet unexpected contingencies, and invest in their enterprises to take advantage of opportunities as they arise. Another study found that the inability to obtain financing may have prompted one-in-three small businesses to trim their workforces and one-in-five to cut benefits.

Unfortunately, much of the available data on small business lending is too dated or too spotty to paint a full picture of the current state of access to credit for small businesses, especially those owned by women and minorities. For example, we do not know whether certain types of businesses, or those in particular places, may have more or less access to credit. We do not know the extent to which small business lending is shifting from banks to alternative lenders. Nor do we know the extent to which the credit constraints that resulted from the Great Recession persist and to what extent. The Beige Book produced by the Federal Reserve on a regular basis is a survey of economic conditions that contains a huge amount of anecdotal information about business activity around the country. But it has no systematic data on how small businesses are faring and whether or how much they are being held back by financing constraints.

Given the importance of small businesses to our economy and their critical need to access financing if they are to prosper and grow, it is vitally important to fill in the blanks on how small businesses are able to engage with the credit markets. That is why Congress required financial institutions to report information about their applications for credit from small businesses in accordance with regulations to be issued by the Consumer Bureau. And that is why we are here today for this field hearing.

***

The inquiry we are launching today is a first step toward crafting this mandated rule to collect and report on small business lending data. To prepare for the project, we have been building an outstanding team of experts in small business lending. We are enhancing our knowledge and understanding based on our Equal Credit Opportunity Act compliance work with small business lenders, which is helping us learn more about the credit application process; existing data collection processes; and the nature, extent, and management of fair lending risk. We also have learned much from our work on the reporting of home loans under the Home Mortgage Disclosure Act, which has evolved and improved considerably over the past forty years.

At the same time, we recognize that the small business lending market is much different from the mortgage market. It is even more diverse in its range of products and providers, which range from large banks and community banks to marketplace lenders and other emerging players in the fintech space. Community banks play an outsized role in making credit available to small businesses in their local communities. And unlike the mortgage market, many small business lenders have no standard underwriting criteria or widely accepted scoring models. For these reasons and more, we will proceed carefully as we work toward meeting our statutory responsibilities. And we will seek to do so in ways that minimize the burdens on industry. Our Request for Information released today focuses on several issues.

First, we want to determine how best to define “small business” for these purposes. Despite the great importance of these firms to our economy, there is surprisingly little consensus on what constitutes a small business. For example, the Small Business Administration, in overseeing federal contracting, sometimes looks at the number of employees, sometimes looks at the annual receipts, and applies different thresholds for different industries. For our part, the Consumer Bureau is thinking about how to develop a definition that is consistent with the Small Business Act, but can be tailored to the purposes of collecting business lending data. So we are looking at how the lending industry defines small businesses and how that affects their credit application processes. Having this information will help us develop a practical definition that advances our goals and aligns with the common practices of those who lend to small businesses.

Second, we want to learn more about where small businesses seek financing and the kinds of loan products that are made available to them. Our initial research tells us that term loans, lines of credit, and credit cards are the all-purpose products used most often by our small businesses. In fact, they make up an estimated three-fourths of the debt in the small business financing market, excluding the financing that merchants or service providers extend to their small business customers to finance purchases of the sellers’ own goods and services. But we want to find out if other important financing sources are also being tapped by small businesses. Currently, we have limited ability to measure accurately the prevalence of lenders and the products they offer. We also want to learn more about the roles that marketplace lenders, brokers, dealers, and other third parties may play in the application process for these loans. At the same time, we are exploring whether specific types of institutions should be exempted from the requirement to collect and submit data on small business lending.

Third, we are seeking comment about the categories of data on small business lending that are currently used, maintained, and reported by financial institutions. In the statute, Congress identified specific pieces of information that should be collected and reported. They include the amount and type of financing applied for; the size and location of the business; the action taken on the application; and the race, ethnicity, and gender of the principal owners. Congress determined that the reporting and disclosure of this information would provide a major boost in understanding small business lending. At the same time, we are sensitive to the fact that various financial institutions may not currently be collecting and reporting all of this information in the context of other regulatory requirements. And we understand that the changes imposed by this rule will create implementation and operational challenges.

So we will look into clarifying the precise meaning of some of these required data elements to make sure they are understood and consistently reported. We will be considering whether to add a small number of additional data points to reduce the possibility of misinterpretations or incorrect conclusions when working with more limited information. To this end, we are seeking input on the kinds of data different types of lenders are currently considering in their application processes, as well as any technical challenges posed by collecting and reporting this data. We will put all of this information to work in thinking carefully about how to fashion the regulation mandated by Congress under Section 1071 of the Dodd-Frank Act.

Finally, the Request for Information seeks input on the privacy implications that may arise from disclosure of the information that is reported on small business lending. The law requires the Consumer Bureau to provide the public with information that will enable communities, government entities, and creditors to identify community development needs and opportunities for small businesses, especially those owned by women and minorities. But we also are authorized to limit the data that is made public to advance privacy interests. So we will be exploring options that protect the privacy of applicants and borrowers, as well as the confidentiality interests of financial institutions that are engaged in the lending process.

***

The announcement we are making today, and the work we are doing here, reflect central tenets of the Consumer Financial Protection Bureau. We are committed to evidence-based decision-making. We aim to develop rules that meet our objectives without creating unintended consequences or undue burdens. We want to see a financial marketplace that offers fairness and opportunity not just to some, but to all. A marketplace that does so without regard to race, ethnicity, gender, or any of the other elements of our fabulous American mosaic. We all know that small businesses are powerful economic engines. They supply jobs that lift people out of poverty or dependence, teach essential skills, and serve as backbones of our communities. So we mean to meet our obligation to develop data that will shed light on their ability to access much-needed financing. It is essential to their future growth and prosperity, and therefore to the growth and prosperity of us all. Because what Cicero observed in ancient Rome still holds true today. He said, “Nothing so cements and holds together all the parts of a society as faith or credit.” Our communities depend on both of those precious things just as much today.

As we launch this inquiry, I want to remind all of you that we value the feedback we get. We take it seriously, consider it carefully, and integrate it into our thinking and our approach as we figure out how best to go forward with this work. So we ask you to share your thoughts and experiences to help us get there. And we thank you again for joining us today.

Fintech Sandbox? States, OCC Mull Regulatory Options

May 2, 2017It’s called the “New England Regulatory FinTech Sandbox.”

State banking regulators across the six New England states are exploring the creation of a regional compact that would allow financial technology companies to experiment with new and expanded products in “a safe, collaborative environment,” says Cynthia Stuart, deputy commissioner of the banking division at the Vermont Department of Financial Regulation.

Stuart asserts that she and her New England cohorts are adroitly positioned and uniquely qualified to oversee laboratories of finance. In Vermont, for example, she heads an agency that oversees regulation and examination of banks, trust companies, and credit unions as well as such nonbank financial providers as mortgage brokers, money transmitters, payday lenders and debt adjusters.

Financial watchdogs at the state level, Stuart observes, “are already witnesses to a wide breadth of financial services offerings and understand how they impact communities and consumers. As technology intersects with financial regulation,” she adds, “state regulators also appreciate the need to be open to technological innovation while balancing risk and return.”

The regional fintech sandbox is the brainchild of David Cotney, the former Massachusetts Commissioner of Banks, and Cornelius Hurley, director of Boston University’s Center for Finance, Law and Policy. The sandbox stitches together elements of Project Innovate, a development program for fintechs inaugurated by the U.K.’s banking regulator, and the European Union’s “passport” model for cross-border banking operations.

In the U.K., the Financial Conduct Authority is supporting both small and large businesses “that are developing products and services that could genuinely improve consumers’ experience and outcomes,” according to a 2015 report by the London agency. In harmonizing the regulatory regime for the sandbox across state lines of Maine, New Hampshire, Vermont, Massachusetts, Rhode Island and Connecticut, the program emulates the EU’s “passport.” Since 1989, a bank licensed in one EU country has been able to set up shop there while – thanks to the “passport” –operating seamlessly throughout the 28 states of the EU (soon to be 27 after “Brexit”).

“It’s still preliminary,” Cotney says of the proposed New England sandbox-cum-passport, “but we’ve talked to the financial regulators in all six states and there’s universal openness. Nobody want to be seen as being a barrier to innovation.”

(Barred by law from lobbying in Massachusetts, Cotney hands off the Bay State duties to Hurley while he meets with regulators and other officials in the five remaining New England states. In March, Cotney was named a director at Cross River Bank, a Fort Lee, N.J.-based, $600 million-asset community bank known for its partnerships with peer-to-peer lenders including Lending Club, Rocket Loans and Loan Depot.)

This nascent effort of financial Transcendentalism in New England is, meanwhile, taking place against the backdrop of an increasingly acrimonious battle between the Office of the Comptroller of the Currency and state banking authorities over the licensing and regulation of fintech companies. At issue is the OCC’s plan announced in a December, 2016 “whitepaper” to issue a “special purpose national bank” charter to nonbank fintechs.

Siding with the OCC are the fintechs themselves, including Lending Club, Kabbage, Funding Circle, ParityPay, WingCash. “A special purpose national bank charter for fintechs creates an opportunity for greater access to banking products, empowers a diverse and often underserved customer base, promotes efficiency in financial services, and encourages industry competition,” Kabbage wrote to the OCC in a sample industry comment to its whitepaper (which is on the agency’s website).

Also on board for the OCC’s fintech charter are powerful Washington trade associations such as Financial Innovation Now, the membership of which comprises Amazon, Apple, Google, Intuit and PayPal, and industry research organizations like the Center for Financial Services Innovation. The U.S. banking establishment also appears largely supportive of the OCC. While qualifying its imprimatur somewhat, the American Bankers Association declared that it “views the OCC’s intent to issue charters as an opportunity to further bring financial technology into the banking system…”

But an irate army of detractors is condemning the fintech charter outright. Consumer groups, small-business organizations, community banks, and state attorneys general number among the furious opposition. No cohort, however, has been more hostile to the OCC’s fintech charter than state banking regulators.

Maria T. Vullo, superintendent of New York State’s Department of Financial Services, has emerged as a firebrand. “The imposition of an entirely new federal regulatory scheme on an already fully functional and deeply rooted state regulatory landscape,” she wrote to the OCC earlier this year, “will invite serious risk of regulatory confusion and uncertainty, stifle small business innovation, create institutions that are too big to fail, imperil crucially important state-based consumer protection laws, and increase the risks presented by nonbank entities.”

Although big-state regulators from New York, California and Illinois have been in the vanguard of opposition, their unhappiness with the OCC is widely shared. Vermont regulator Stuart, who emphasizes the need for regulators “to embrace change,” nonetheless disparages the OCC’s endeavor.

“Of particular concern is the creation of an un-level playing field for traditional, full-service Vermont institutions to the advantage of the proposed nonbank charter,” she told AltFinanceDaily. “The special purpose national nonbank charter would not be subject to most federal banking laws and would be regulated with a confidential OCC agreement. The disparity in regulatory approaches is concerning.”

What had been confined to a war of words – rounds of angry denunciations packed into letters and press releases directed at the OCC — reached fever-pitch last week when, on April 26, the Conference of State Banking Supervisors filed suit against the OCC in federal court. The lawsuit seeks to prevent the agency “from moving forward with an unlawful attempt to create a national nonbank charter that will harm markets, innovation and consumers,” according to a CSBS statement.

Among other things, the conference’s complaint charges that by creating a national bank charter for nonbank companies, the OCC has “gone far beyond the limited authority granted to it by Congress under the National Bank Act and other federal banking laws. Those laws,” the conference’s statement continues, “authorize the OCC to only charter institutions that engage in the ‘business of banking.’”

Under the National Bank Act, the conference’s complaint asserts, a financial institution must “at a minimum” accept deposits to qualify as a bank. By “attempting to create a new special purpose charter for nonbank companies that do not take deposits,” the complaint adds, the OCC is acting outside its legal authority.

Christopher Cole, senior regulatory counsel at the Independent Community Bankers Association – a Washington, D.C. trade association of Main Street bankers known for punching above its weight — asserts that the state banking regulators are on solid ground. “The whole question comes down to what should a bank be for purposes of a national bank charter,” he says in a telephone interview. “The Bank Holding Company Act (of 1956), federal bankruptcy laws, and tax laws – all three – define banks as insured depository institutions. It’s right there in the statutes. So our recommendation,” he says, “is for the OCC to go back to Congress” and ask for the explicit authority to create a fintech charter.

Because the OCC has “short-circuited rule-making” protocol required by another law – known as the Administrative Procedures Act — “the process hasn’t been kosher,” Cole adds.

Many members of Congress are also expressing outrage at the OCC. Not only have Democratic Senators Sherrod Brown of Ohio and Jeff Merkley of Oregon strenuously objected to the OCC’s fintech charter, but on March 10, 2017, Jeb Hensarling, the chairman of the House Financial Services Committee, fired off a “hold-your-horses” letter to Comptroller Thomas J. Curry. Signed by 34 House Republicans, the March 10 letter reminded Curry that his term of office would officially be up at the end of April, 2017, and urged him not to “rush this decision” regarding the fintech charters.

Many members of Congress are also expressing outrage at the OCC. Not only have Democratic Senators Sherrod Brown of Ohio and Jeff Merkley of Oregon strenuously objected to the OCC’s fintech charter, but on March 10, 2017, Jeb Hensarling, the chairman of the House Financial Services Committee, fired off a “hold-your-horses” letter to Comptroller Thomas J. Curry. Signed by 34 House Republicans, the March 10 letter reminded Curry that his term of office would officially be up at the end of April, 2017, and urged him not to “rush this decision” regarding the fintech charters.

“If the OCC proceeds in haste to create a new policy for fintech charters without providing the details for additional comment, or rushing to finalize the charter prior to the confirmation of a new Comptroller,” the letter from Hensarling et alia declares, “please be aware that we will work with our colleagues to ensure that Congress will examine the OCC’s actions and, if appropriate, will overturn them.”

Never mind the stern letter from Chairman Hensarling, or the fact that an impressive array of Congressmembers on both sides of the aisle are bipartisanly unhappy, or that state banking regulators’ have filed suit, or that Curry’s replacement as Comptroller is overdue: the OCC is pushing ahead. The agency will play host to a bevy of financial technology companies and other financial institutions on May 16 for two days of get-acquainted sessions in its San Francisco office.

Billed as “office hours,” the West Coast meetings will consist of one-on-one, hour-long informational meetings “to discuss the OCC’s perspective on responsible innovation,” Beth Knickerbocker, the OCC’s acting chief innovation officer, says in a press release.

The office hours, Knickerbocker adds, “are an opportunity to have candid discussions with OCC staff regarding financial technology, new products or services, partnering with a bank or fintech company, or other matters related to financial innovation.”

Back in New England, Hurley, the Boston University law professor advocating the regional sandbox, says: “No one knows where fintech is going. But one place it’s not going is away.”

What IOU Financial Revealed in its Earnings Statement

April 29, 20172016 was a weird year for online lenders and IOU Financial, who lends to small businesses, fared no differently. Loan origination volume for the year was $107.5 million, down 26.5% from 2015. Revenues were up due to the company retaining more of their loans on balance sheet but losses were up as well.

Here are the most interesting statistics we found:

- 93% of their loan volume came from brokers

- 15% of merchants in their portfolio were classified as specialty trade contractors and home building renovation

- 14% of merchants in their portfolio are based in Florida (more than New York and New Jersey combined)

- Their borrowers have been in business for an average of 11.4 years

- Their average loan size is $69,695

- Their average loan term is 12 months

- They sold $60.8 million of loan receivables in 2016, down from $137.3 million in 2015

- The company has loaned $415 million to small businesses since inception

- The company had 53 full-time employees at year-end

IOU Financial is the only lender that AltFinanceDaily is tracking whose stock is down year-to-date. At close on Friday, company shares were down more than 28% for the year.

Re-Banked

April 23, 2017

Just a few years ago, the financial services community was fixing for a battle of David and Goliath proportions—with scrappy, upstart online lenders threatening to rise up and vanquish the fearful and mighty brick and mortar banks. Instead, the unexpected happened: a number of well-respected online lenders and banks set aside their battle arms and began looking for ways to collaborate with their rivals—offloading loans, making referral agreements and establishing more formal partnerships, for example.

“In the real world, sometimes David wins. Sometimes Goliath wins. Just as plausibly, sometimes both sides carve up a market and they often have different offerings that target unique customers,” says Brayden McCarthy, vice president of strategy at Fundera, a New York-based marketplace for small business lending that works with a variety of lenders, including traditional banks.

Certainly, the change didn’t happen overnight. But over time, both online lenders and banks have been forced to tailor their expectations more closely to market realities. Despite their fast growth trajectory, several online lenders have come to realize that they lack several things many banks have, namely a strong, time-tested brand, a solid customer base and ample capital. Banks, meanwhile, have realized that their slow start out of the gate with respect to technology is a severe competitive disadvantage, and that they need more nimble, savvy partners to stay in the game.

Given these shifts, more and more online lenders and banks are taking the approach that if you can’t beat ‘em, join ‘em. Although some industry leaders are actively pursuing strategies that put them in direct competition with banks, partnerships of varying degrees between traditional banks and alternative players are increasingly common. As a result, the lines separating the two are getting increasingly blurry.

“Market forces are acting as a shotgun at the wedding. Whether the two sides are entirely comfortable with the marriage is irrelevant, they need one another,” says Patricia Hewitt, chief executive of PG Research & Advisory Services LLC in Savannah, Georgia. “They’re stronger together than they are alone.”

The evolution of Square is a prime example. The San Francisco-based company really packed a punch in the merchant services world with its mobile card reader designed for small businesses. From there, the payments company sought additional ways to diversify, eventually turning to merchant cash advance as a way to help small business customers obtain funds quickly. Then, in March of last year, Square moved into online lending, teaming up with Celtic Bank of Utah to offer small business loans online. The partnership got off to a running start. In its most recent earnings report, Square said it facilitated 40,000 business loans totaling $248 million in the fourth quarter of 2016—up 68 percent year over year—while maintaining loan default rates at roughly 4 percent.

Even SoFi, the San Francisco-based online lender that has been pointedly outspoken in its anti-bank rhetoric, now has bank-like aspirations. In February, the lender acquired mobile banking startup Zenbanx, giving it the ability to offer checking accounts and credit cards in 2017. Also in February, SoFi teamed up with Promontory Interfinancial Network to enable community banks to purchase super-prime student loans originated by the online lender. Large banks have been buying SoFi loans for several years.

COLLABORATION IS THE WAVE OF THE FUTURE

Many see collaboration between banks and online lenders as a logical step in the industry’s evolution. Online disrupters have forever changed the face of lending—in the same way that online brokerage shaped the financial advisor industry, according to Bill Ullman, chief commercial officer of Orchard Platform.

“There’s a tendency to want to view things as either black or white, online lenders vs. banks. The reality is that the entire financial services industry is undergoing a transformation with technology as the core driver,” he says. “I am of the view that both traditional financial services companies and fintech players can survive and thrive,” Ullman says.

For its part, Orchard recently inked a deal with Sandler O’Neill that provides access to the Orchard platform for the investment bank and brokerage firm’s bank and specialty finance clients. The deal is expected to help small banks better evaluate their options with respect to online lending opportunities.

Partnerships between online lenders and banks take many forms. Some of them are behind the scenes, where marketplaces sell loans to banks or banks informally refer customers. Others are more public. For example, in September 2015, Prosper and Radius Bank of Boston teamed up to offer personal loans to certain customers through the bank’s website using the Prosper platform. Customers can borrow from $2,000 to $35,000 in this manner.

Then in December 2015, JPMorgan Chase and OnDeck joined forces in order to dramatically speed up the process of providing loans to some of the banking giant’s small business customers. In April 2016, Regions Bank and Avant announced a partnership to better serve customers who don’t meet Regions’ credit criteria.

Avant’s customers typically have a credit score between 600 and 700, while Regions sets the bar higher. “The benefit for banks is that they do not need to worry about a platform taking away customers that meet their own credit criteria,” according to Carolyn Blackman Gasbarra, head of public relation at Avant.

She notes that Avant expects to replicate this model with more banks in 2017. “Lately many platforms and banks have come to realize their counterparts are more friend than foe,” she says.

Given the changing tides, industry watchers expect to see more relationships develop between online lenders and banks over time. These could include referral agreements, technology licensing arrangements, formalized revenue-sharing partnerships and perhaps even outright acquisitions.

PARTNERSHIP ADVANTAGES

Certainly, working together can be mutually beneficial for both online lenders and banks. For new online lenders and other fintech players, partnering with an established bank allows them to bypass significant regulatory and compliance hurdles because the necessary requirements are already in place.

“Why jump through all the hoops when you can just have a buddy system with an existing lender?” says Kerri Moriarty, head of company development at Cinch Financial, a Boston-based company dedicated to helping people make smarter investment decisions.

Fintechs that license their technology to banks still have to meet the high standards of third-party vendors determined by bank regulators, notes Stan Orszula, co-head of the fintech team at the Chicago law firm Barack Ferrazzano Kirschbaum & Nagelberg LLP.

“But it’s still less onerous than being a direct lender,” says Orszula, who works closely with banks and fintech providers on legal, regulatory and corporate issues. “They are learning that they need banks. They really do.”

Even seasoned online lenders that have a regulatory framework in place can benefit from bank relationships by using banks’ established brands as leverage. “Everyone knows Chase, Bank of America and American Express,” says McCarthy of Fundera. “They have a solid name and a solid in-built customer base to be able to offer product to them,” he says.

Teaming up with a bank gives added credibility to an online lender, at a time when the public’s confidence has faltered due to highly publicized troubles at certain firms. “Partnering has a very important signaling effect that these online players are here to stay,” McCarthy says.

Banks, meanwhile, need the nimbleness and innovation that online lenders provide. “Banks realize they have to catch up with the fintech disrupters,” says Mark E. Curry, president and chief executive of SOL Partners, which provides strategic management and information technology consulting services to financial services companies.

DIFFERENT TYPES OF PARTNERSHIP OPPORTUNITIES ABOUND

When it comes to partnerships between banks and online players, there are numerous options. In the small business lending space, for example, McCarthy of Fundera says he expects banks to continue buying loans from online lenders, as they have been for many years. He also expects more banks will route declined applicants to online lenders or online loan brokers. “This is a partnership that will allow them to make up some incremental revenue by referring business,” he says.

In addition, McCarthy says he expects banks to make products available through online marketplaces and use an online lender’s technology for online loan applications. He also expects banks will use online lenders’ technology for underwriting and servicing loans.

Years ago, before John Donovan joined Bizfi, he recalls talking to a salesman for a large national bank. The bank didn’t offer a lending product that he could give to small businesses and the salesman was losing customers as a result. “That’s where we see a lot of those opportunities,” says Donovan, chief executive of the online marketplace for small business loans.

For instance in March 2016, Bizfi partnered with Western Independent Bankers, a trade association, for over about 600 community and regional banks, to link small business clients to financing options through Bizfi. Many banks don’t offer small business loans below $150,000, whereas the average loan Bizfi does is $40,000, Donovan says, adding that the company would like to develop additional relationships similar to its agreement with Western Independent Bankers.

In the future, he predicts fintechs will continue to be more receptive to the idea of working with banks and vice versa, as the industry digests the impact of deals that are still in their early days.

FINDING STRATEGIC GROWTH OPPORTUNITIES

As banks and online lenders become increasingly accustomed to working together, there may be more opportunities for strategic acquisitions. For instance, Sandeep Kumar, managing director of Synechron, a global consulting and technology firm, expects to see banks—especially mid-tier players that don’t have the resources to innovate like big banks buying lending-related start-ups. He says banks will likely be most interested in companies that can help them with AI and other techniques to pinpoint where they should spend more efforts on cross-selling and customer profiling, for example. “There are many start-ups in this area that have very compelling technology,” he says.

On the other hand, Chris Skinner, an independent commentator at The Finanser Ltd., a research and consulting firm in London, points out that the two cultures don’t always mesh. “Quite a few startups have young, entrepreneurial founders that would loath the idea being acquired by a bank. So it really depends on the circumstances,” he says.

Valuation differences between large banks and leading online lenders may also be a sticking point for some deals, Ullman of Orchard points out. Banks’ concern over their valuation “will place a certain amount of restraint and discipline on the tech M&A activities they pursue,” he says.

ANTICIPATING TROUBLE IN PARADISE

While increased collaboration between online lenders and banks sounds good on the surface, John Zepecki, group head of product management for lending at D+H in San Francisco, urges both sides to proceed with caution. “You have to find an arrangement where you don’t have conflict,” he says. “If your innovation partner also is a competitor, it’s a challenge. If you have an inherent conflict, it doesn’t get better over time.”

That’s one reason why companies like Chicago-based Akouba have come on the scene. In Akouba’s case, its goal is to provide banks with the technology such that they don’t have to partner with an online lender that has the potential to compete for business. “We don’t compete with the bank in any way whatsoever,” says Chris Rentner, the company’s founder and chief executive.

Akouba’s business lending platform—which the American Bankers Association endorsed in February—provides banks with leading edge technology that integrates the bank’s own unique credit policies into a convenient, online process—from application to documentation— all the way to closing and funding. The bank uses its own credit policies, originates its own loans and owns the entire brand and customer relationship.

Rentner says he started the business with the idea in mind that the online lending model wouldn’t be sustainable long-term and that working alongside banks—as opposed to competing head to head— was the direction to go. “The idea that they could somehow get all of the consumers out of the banking world and onto their platforms was never going to happen. That’s why we exist today,” he says.

Sneak Peek at the Mar/Apr 2017 Issue of AltFinanceDaily

April 11, 2017 In the March/April 2017 issue of AltFinanceDaily magazine, we delve into the industry’s latest trend, the push back towards traditional banking. The featured story is titled accordingly as “Re-Banked” and our many sources lay out a compelling narrative. Our cover, a sketch of a young tech CEO shedding the hoodie to reveal the suit-and-tie attire of a banker underneath, was one of several pieces of art we commissioned for this issue.

In the March/April 2017 issue of AltFinanceDaily magazine, we delve into the industry’s latest trend, the push back towards traditional banking. The featured story is titled accordingly as “Re-Banked” and our many sources lay out a compelling narrative. Our cover, a sketch of a young tech CEO shedding the hoodie to reveal the suit-and-tie attire of a banker underneath, was one of several pieces of art we commissioned for this issue.

And for you brokers out there, we’ve got something really special, the inside scoop on the latest way that reps are winning deals. Today’s broker is hanging up the phone and texting merchants instead and the merchants are responding in kind. Phone calls and emails are going the way of the fax machine when it comes to gathering documents and pitching offers. The lesson we learned from the several people we interviewed is that when merchants want to know what’s next, send a text.

There’s more of course, so if you haven’t already subscribed to our free print magazine, make sure you do so here. This issue has already printed and shipped so you’ll be getting it very soon.

We hope you enjoy it!

Subscribe FREE

For Factoring, Different Spin, Same Issues as MCA

April 10, 2017

They called it the 2017 Factoring Conference, but an MCA professional would’ve hardly noticed. On the agenda was news about Dodd-Frank’s Section 1071, the now-dead NY lending legislation, usury litigation, confessions of judgment, stacking, fintech and gripes about brokers. And yet factors and MCA companies still largely live separate lives.

The underlying differences between the two industries are as much cultural as they are contractual. The International Factoring Association’s directory reports having nearly twice as many members from Texas as they do from New York. They also list having more members from Utah than they do New Jersey. Compare that to our own readership at AltFinanceDaily in which website visitors and magazine subscribers are most heavily concentrated in New York, California, Florida and New Jersey. Texas ranks 8th for subscribers and Utah is much, much farther down. And while purely based on my unscientific observation, I’d wager a bet that the average age of a factoring company owner is at least a decade older (probably much more) than the average age of an MCA company owner.

Differing philosophies between the two industries are perhaps exacerbated by this generational and demographic gap.

On a fintech disruption panel at the factoring conference last week, Pearl Capital CEO Sol Lax told attendees that the MCA industry was not only innovative but ultra competitive. “You either need to evolve or become a phone booth,” he said. Other panelists explained that today’s average small business is focused on speed and simplicity and that they’ve built their models around that.

But factoring has survived the test of time. In the latest issue of The Commercial Factor, Jeremy B. Tatge traces the first factoring agreement in America to 1628. “This spirit has endured and survived wars of independence, such as the American Revolution, two World Wars in the Twentieth Century, and even down to the present day (NATO being but one of many examples),” he writes.

Will technology finally break that spirit or will today’s stereotypical young MCA company owner from New York and Florida eventually find themselves becoming older, wiser, and ready to lay down roots in the midwest? Will they trade the Las Vegas conferences for honky tonks in Cowtown?

I don’t believe that such a transition even has to happen. Whatever differences the two industries have, they are united by common causes and issues and can evolve together.

Enrolling a Merchant’s “Debt” May Be Harmful… to the Merchant

March 29, 2017 How would you like to make $12,000 on a single referral?, a flyer directed at business finance brokers asks. This ad wasn’t offering a commission for brokering a loan or advance, but rather for enrolling a merchant’s debt into the company’s restructuring program. Debt restructuring, negotiation, or settlement is a booming cottage industry these days. Some of these debt restructuring companies promise ISOs that they will be completely discreet with referrals. Others offer them commission bonuses for achieving certain enrollment targets. It’s a way to monetize declined deals, they typically say.

How would you like to make $12,000 on a single referral?, a flyer directed at business finance brokers asks. This ad wasn’t offering a commission for brokering a loan or advance, but rather for enrolling a merchant’s debt into the company’s restructuring program. Debt restructuring, negotiation, or settlement is a booming cottage industry these days. Some of these debt restructuring companies promise ISOs that they will be completely discreet with referrals. Others offer them commission bonuses for achieving certain enrollment targets. It’s a way to monetize declined deals, they typically say.

For merchants, the allure of a restructuring company’s help might just be payment terms tied to their monthly budget. That’s allegedly what one NJ firm’s agreement says, in fact. “I hereby authorize [the company] to negotiate my unaffordable business debts and to enter into affordable repayment terms on my behalf based on my monthly budget,” reads a document submitted in a New York Supreme Court case involving Creditors Relief. And based on the marketing materials AltFinanceDaily has reviewed from several similar companies, their definition of debt is so broad that it can even include things that aren’t debt, like merchant cash advances, for example.

Even if the restructuring company held a critical view of MCAs and believed them to be loans, treating them as such for the purpose of negotiation might actually cause harm to their customers. That’s because a well-formed MCA contract already offers payment adjustments at regular intervals to appropriately match a merchant’s sales activity. Depending on what the language says, a merchant might just have to call their funder and ask them to reduce the debits to reflect their current sales activity. And yes this goes for ACH-only deals. Even ones that could appear to have fixed payments do not actually have fixed payments. This is basically how all MCAs work by the way, so if you are a broker or funder and this all sounds foreign to you, you need to take this course ASAP.

The point is this: a merchant need not pay a fee to an outside company to restructure anything when sales drop because a free remedy already likely exists and is a key benefit to MCAs in the first place. And yes, I’m talking about MCAs with daily ACH debits. If you’re confused by this, you need to take this course ASAP.

The best advice a restructuring firm can give a merchant struggling with an MCA due to slow sales is to tell them to look for a reconciliation clause in their contract that explains how to get the payments reduced. Once the merchant finds it, have them call the funder and execute it. There’s no need to enroll anything, negotiate anything, risk breaching a contract, or pay a broker tens of thousands of dollars in commissions. The debt restructuring firm might not want merchants to simply take advantage of what they’re already entitled to however, because they stand to make no money that way. In this regard, mischaracterizing future receivable sales as loans only serves to carry out their agenda to confuse merchants about what their rights might be under those agreements.

I myself, am occasionally contacted by merchants who claim to be facing hardship and in one instance where a merchant had spoken to a negotiator, the negotiator didn’t tell him that the remedy he sought was already a natural provision of his contract. I helped him find it. He didn’t have to pay any fees which would’ve gone to pay someone a huge commission or end up in some crazy situation where he’s being sued for breach of contract. Think about this the next time you encounter a distressed merchant. Not everything is debt and that can be very much to the merchant’s benefit.

If you work for a debt restructuring, settlement, or negotiation company, you should probably take this course too. It will help you understand MCA agreements and what remedies merchants already have at their disposal.

Brief: New York’s Attempt to Over-Regulate Lenders Downgraded to Doubtful

March 14, 2017 The Governor’s budget bill has encountered resistance up in Albany, sources say, specifically Part EE that aimed to amend New York’s banking law and impose sweeping licensing restrictions on all types of lending and finance. Analysts felt that the language could have vast unintended consequences beyond just online lenders, including factoring, commercial lenders and brokers, merchant cash advance and the securitization markets.

The Governor’s budget bill has encountered resistance up in Albany, sources say, specifically Part EE that aimed to amend New York’s banking law and impose sweeping licensing restrictions on all types of lending and finance. Analysts felt that the language could have vast unintended consequences beyond just online lenders, including factoring, commercial lenders and brokers, merchant cash advance and the securitization markets.

The passage of this proposal now looks doubtful. The Assembly, one of two branches of the State’s legislature, introduced their own version of the budget on March 13th and removed the language.

“The Assembly rejects the Executive proposal granting DFS regulatory authority over any online lenders doing business in New York State,” the bill says. Notably, they also rejected “the Executive proposal to authorize enforcement of Insurance, Banking, and Financial Services Law against unlicensed individual or businesses, including bringing a civil action.”

The Senate echoed same. “The Senate denies the Executive proposal to authorize the Superintendent of the Department of Financial Services to expand the regulation of small loan lenders,” their bill states.

Industry trade groups, namely the Commercial Finance Coalition (CFC), had mobilized quickly to tell their members’ stories up in Albany two weeks ago. One of the group’s concerns was that they had not been consulted in advance, nor given any time to engage in a discussion about the proposal.

“They should allow all the stakeholders to have their voices heard,” said Dan Gans, CFC’s executive director. With the proposal’s chances of making it through the final budget by the March 31st deadline waning, the group and others may finally get an opportunity to do just that at some point later in 2017. According to The CFC, they are looking for additional companies to support them in that endeavor. Anyone interested in finding out how they can help should contact Dan Gans at dgans@polariswdc.com.