Learn Merchant Cash Advance or Else…

December 15, 2011If you don’t know about Merchant Cash Advance (MCA), you’re not qualified to work in the payments industry! As indicated by the Electronic Transactions Association (ETA), Certified Payment Professionals (CPPs) should be savvy with MCA financing. According to the ETA: “The [new] CPP program sets the standard for professional performance in the payments industry and is a symbol of excellence. It signifies that an individual has demonstrated the knowledge and skills required to perform competently in today’s complex electronic payments environment.”

CPP candidates can preview exam sample questions in the official handbook, one of which asks:

An established merchant that processes $25,000 in bank card transactions per month has no marketing budget, but has been offered a sponsorship opportunity. What product/solution should the payments professional recommend?

The answer is “merchant funding” AKA MCA. Believe it folks. The MCA financing product is here to stay, has benefitted thousands of businesses, and payment professionals must be well versed in it if they are to become certified.

But there is more than a test to become a CPP.

[The ETA says] to be eligible to sit for the CPP examination, candidates must demonstrate the following qualifications:

|

|||||||||

|

CPP candidates will then be required to sit for and pass a Certified Payments Professional written examination. Upon successful completion of the exam and the attainment of the CPP credential, certificants will be required to meet renewal / recertification requirements every three years, to include continuing professional education from ETA / QSP’s or the successful completion of the test.

|

The next exam dates are May 1 – 31, 2012. You can learn more about registering and what it mean to be a CPP on the ETA’s official site. And don’t forget to learn about Merchant Cash Advance. 🙂

Largest Merchant Cash Advance in History Ends in Default

September 27, 2011 Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

While SFS was given high praise from their peers, some began to speculate if transactions that large were practical. After all, the costly financing of a MCA is priced in accordance with the risk of default, not in accordance with big profits for the financier. When your portfolio is in great shape, it can be easy to forget what the pitfalls are. And since the MCA industry paraded the Las Vegas Mob exhibit as the $4 Million deal that changed everything, we’re eerily reminded of the words by Jeff Mitelman, the CEO of AdvanceIt who was quoted two years ago as asking: “How prepared are you to lose $4 million dollars?”

We won’t pretend to know what led to the downfall of the Las Vegas Mob exhibit or why it went south so quickly. SFS could potentially lose 98% of their investment, a hit that will surely change their outlook on doing large deals in the future. The VegasInc article alleges gross mismanagement and fraud, factors that are difficult to foresee in the course of underwriting.

Industry message boards have been abuzz with comments on the default, with some competitors of SFS being accused of kicking a man while he’s down. “you ought to do smart funding, not just showing off your Balls,” one broker fired off at them. SFS has a stellar reputation and is one of the most knowledgeable firms in the MCA space. We have no doubt they inspected the merits of the deal backwards, forwards, and upside down. But nothing is perfect.

The default is expected to attract attention of the news media, leaving many to wonder how this transaction will be interpreted under the public eye. We assert that it will put to rest any criticism the MCA product has ever received about high costs.

Risk vs. Reward

Back in March when the deal was written, an outsider could claim that SFS just had an easy million handed to them. This view clashes with the Risk vs. Reward philosophy that MCA providers hold dear. To the MCA providers, the question was never “how can I make an easy million?” but rather, “how prepared am I to lose $4 Million?”

Any business that can’t get a bank loan, can’t get one for a reason. There’s a measurable value of risk that’s not worth taking. MCA providers fill the gap but compensate to offset defaults. There’s a term for something like this. It’s called a Happy Medium.

Merchant Cash Advance is the happy medium financing option for small businesses. And for the immediate future it is likely to stay within the small business niche. We all know now what can happen when the concept is applied to a multi-million dollar project. The outcome was not so happy and the loss not so medium.

But it will all even out in the end…

– Merchant Processing Resource

A Line of Credit and a Term Loan are Different Things

August 24, 2011Posted on July 27, 2011 at 12:22 AM

According to Gary Honig on Lendio.com, business owners sometimes ask for one type of financing but describe another. Get the facts and make sure you get what you need:

A line of credit (LOC) is usually considered a short-term loan. The payments are interest-only, based on the outstanding funds in use.

A term loan is a fixed, funding transaction. It is a one-time loan based on cash flow of the business plus certain collateral pledged against the loan.

Who is Really Getting a Merchant Cash Advance?

August 23, 2011

You’ve seen ads like it before: “Get up to $250,000 for your small business today!”

For the local corner deli, that kind of cash may seem too good to pass up. There’s just one catch, many Merchant Cash Advance(MCA) providers cap funding approvals at somewhere in the range of 125% of a business’s monthly credit card processing volume. That means a deli processing $10,000 would be eligible for up to $12,500. ‘Mom and pop’ shops are often left wondering if anyone could ever really get $250,000 or if that figure is just a deceptive marketing gimmick.

/>

/>

The Merchant Cash Advance Resource would like business owners to know that $250,000 is not only possible, but deals of this size and larger are made often. The typical recipients are retail chains and restaurant franchises, but any business generating enough volume in credit/debit card sales is eligible. If there was any doubt about the popularity or legitimacy of the MCA financial product, take a look at some franchise names that have used it:

- Burger King

- Domino’s Pizza

- Hooters

- Subway

- Dunkin Donuts

- Taco Bell

- Denny’s

- Wendy’s

- Meineke Car Care

- Maaco

- Aamco Transmissions

- Curves Fitness

This data was confirmed by researching UCC filings on AdvanceMe, Strategic Funding Source, Merchant Cash and Capital, First Funds, and Business Financial Services.

Every funding provider is not created equal. Some of the oldest players such as AdvanceMe, Merchant Cash and Capital, and Strategic Funding Source are capitalized well enough to do deals up to $1,000,000. Other firms specifically seek out larger businesses such as Bankcard Funding in Long Island, New York. According to a representative there, their average funded deal is $100,000. Others have a comfort range of $5,000 to $75,000 but will bring in outside investors if they need to go beyond that.

Merchant Cash Advance is not just for smaller businesses, nor is it a last resort source of capital. It is an established alternative to bank lending that offers incredibly flexible repayment terms. Despite the benefits, a MCA still has a reputation for being expensive. While we don’t dispute that, we do recognize the need for it. Unlike SBA loans which can carry default guarantees up to 90%, MCA’s are completely backed by private investors. There are no billions of dollars to fall back on, government backed guarantees, or bailouts when things turn ugly.

Over the past few years, some MCA firms simply weren’t able to generate enough profit and closed as a result. In the case of Global Swift Funding(GSF), a MCA provider that dissolved back in 2009, the return on investment simply did not prepare them for the loss they would realize from a very important client.

http://www2.ocregister.com/articles/gantes-money-million-2399154-bankruptcy-restaurants

John Gantes, formerly one of the richest Men in Orange County, California owned 110 restaurants throughout the western part of the U.S. As the economy turned sour, he reportedly started loading up on Merchant Cash Advance funding for each location. In the end GSF cried foul, but they could not sustain operations further.

There is risk on both sides of the equation. A MCA is not for businesses on the fritz, but rather is a tool to acquire inventory, new locations, upgrade equipment, get through a slow season, and grow. While much hype surrounds the minimal paperwork requirements for MCA, businesses seeking in excess of $100,000 should expect a more intensive underwriting process.

“Have detailed financial statements handy and expect some scrutiny of the Balance Sheet,” was advice offered by one underwriter. “We’re going to want to make sure you are using these funds for the right reasons.”

And yet the MCA industry stands by their mantra of making capital accessible to all. With funding amounts reportedly as low as $1,000, and more than 21,000 individual advances made in 2010 alone, there is really no better time for a small business owner to apply.

The funds are there but it’s important to set your own expectations of how much you can access. The corner deli should be able to put $12,500 to good use. Our experience shows that positive sales activity will probably make the funding provider more comfortable to extend a larger amount to you down the road. I think we’d all like to get $250,000 today but in the absence of government backed guarantees, a tumultuous economy, and jittery investors, you’ll need to get your foot in the door first and work your way up.

-The Merchant Cash Advance Resource

http://www.merchantcashadvanceresource.com

Images Copyright (c) of 123RF Stock Photos

The Fork in the Merchant Cash Advance Road

August 23, 2011Originally Posted on April 25, 2011 at 10:48 PM

The Merchant Cash Advance (MCA) industry is growing, albeit slower than some may have you believe. But it’s moving in two opposing directions, a condition that’s making it tougher to describe the financial product itself in general terms. MCAs are becoming more expensive and a lot cheaper at the same time. HUH? You read that right.

Originally aimed at business owners with poor credit, the risk of default or delinquency was overcome by withholding a percentage of sales revenue directly. As the credit crisis and Great Recession took hold, it attracted businesses of all credit backgrounds and today it’s widely accepted as a lending alternative, rather than a solution to poor credit.

As MCAs pushed forward to compete for customers normally accustomed to bank credit lines, the cost was stiffly resisted. These businesses had a tough time envisioning their financing terms to be anything outside of some percentage over the Prime Rate. Since a MCA is supposed to be structured as a sale, there is no APR equivalent, no timeframe, no amortization, nor any real familiarities of a loan. As the past couple years have passed, the product is more publicly understood, but for it to actually catch on, the costs had to come down. Many funding providers now refer to such high credit, low cost accounts as premium, platinum, preferred, gold, etc.

While the margins earned on high credit accounts shrank, funding providers were dealing with another challenge simultaneously, defaults. Whether the business owner intentionally interfered with their credit card processing or the store went out of business altogether, bad debt in the MCA world was mounting…FAST!

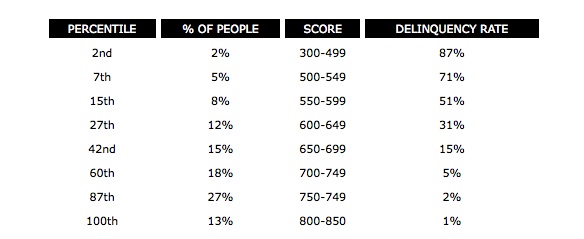

No matter which company ran the figures or how secret these portfolio statistics were, every funding provider came to the same realization. The lower the credit score of the business owner, the greater the chance of a problem. Why this came as any surprise, is a surprise in that of itself. The Fair Isaac Corporation (FICO) will have you know that any individual with a score below 499 has an 87 percent chance of being delinquent on a credit payment within the next 2 years. Delinquent, is defined as a payment of 90 days or more past due.

But wait… if a MCA is not a loan, nor does it depend on the business owner to make payments, then how can there be a risk of delinquency? Intentional manipulation of the revenue flow back to the funding provider can be relatively easy to do. A business owner could use spare POS equipment to accept card payments for which the funding provider is not aware of and therefore prevent the collection of funds. That’s a method known as splitting, and serious consequences can result when discovered. (Read more on what happens in the case of default or deliquency on a MCA in a previous article)

But outside the scope of malice, there’s the traditional reason, the inability to make payments. If the suppliers and wholesales aren’t being paid, then the business isn’t going to have inventory on hand to sell. If the rent isn’t being paid, then there’s not going to be any location to generate these sales. Essentially, the funding provider has a mutual interest in the business being able to satisfy ALL of their obligations, not just the MCA itself.

If there is an 87% chance that suppliers, landlords, or other essential creditors will not be paid on time in the next 2 years, then there’s an excellent probability that the business will be unable to operate at the same level. With no collateral as protection, the MCA industry has adapted to the challenge by raising the cost. Business owners with poor credit can expect funds to be expensive and the terms to be more restrictive. Lower funding amounts, higher withholding percentages, and the sacrifice of any negotiation is the price the MCA industry has set to make funding to the maximum risk group possible. These programs, which are now often referred to as starter advances, don’t work for everyone so the pros and cons should be weighed prior to executing a contract.

Both the premium advances and starter advances have experienced extraordinary growth to the point where they have become niches of their own. There are now starter advance companies and premium advance companies. Funding providers like Strategic Funding Source have taken the product a step further and reportedly did a MCA for an exhibit at the Tropicana Hotel in Las Vegas for $4 Million. Contrast that with deals that are struck for as little as $750. And we can’t fail to mention that some have taken it back to the basics, a loan. ForwardLine in Woodland Hills, CA lends money to businesses which are then repaid in accordance with a predetermined, fixed pace through the card sales. They have reintroduced concepts like APR back to the finance world.

If we continue at the current pace, MCAs will become less expensive, more costly, a lot bigger, and markedly smaller. We’ve come to the fork in the road for what the Merchant Cash Advance industry seeks to brand itself as. Loan alternative? First choice? Backup plan? Is it for smaller businesses or larger ones? Should it go the way of lending or continue to remain a structured purchase of future card sales? Is industry cohesion really necessary or will increased decentralization lead to greater acceptance of this financial product a whole? Will there come a time when America’s big banks swallow the industry up, buy out the existing portfolios, and add this product to their financing arsenals?

These are tough questions. Merchant Cash Advance is evolving, growing, and no longer moving in one direction. While we contemplate our next step, one thing is for certain, there’s no turning back.

– AltFinanceDaily

www.merchantprocessingresource.com

Merchant Hash Advance

July 16, 2011

Short on capital? Your business may benefit from a Merchant ‘Hash’ Advance. Restaurants, retail stores, and auto repair shops can easily obtain funding, but medical marijuana dispensaries need love too.

A few cannabis related deals have floated around the Merchant Cash Advance (MCA) industry before, but rarely do they close. At best they elicit a few chuckles from underwriters, who will likely make a few juvenile jokes before turning down a viable, serious, and legal business. The store owners walk away frustrated but neither side is to blame.

In states like New York, where many MCA powerhouses reside, marijuana of any kind is illegal. That makes the sale of it for medicinal purposes in states where it’s legal a foreign concept. We spoke to an underwriter of one Long Island, NY based MCA firm who shared this: “I’ve eaten dinner at a restaurant and I’ve bought flowers from a florist. I understand what makes both businesses tick. I’ve never been to, nor met anyone who has been to a medical marijuana dispensary. I don’t really know what the transaction is like, what risks they face, what their profit margins should be. It’s a big unknown. Is it easy for a dispensary to lose their license and suddenly go out of business? Are there laws that prohibit outside financing? Do we need to keep tabs on where they obtained their inventory from? We typically call a restaurant’s vendors prior to funding to ensure they’re in good standing. I would feel a little weird calling up a weed farm for a reference.”

And he’s not the only one that feels that way. Banks do too. Funding aside, evidence shows cannabis related businesses stuggle to fulfill basic needs such as opening a bank account or accepting credit cards. According to a report by creditcards.com, it’s not uncommon for their checking accounts to be closed without warning, sending the business scrambling for help elsewhere.

But the situation isn’t all grim. We interviewed Nick Emerson, the Managing Director of 420 Card Processing in Campbell, CA (420 CP), a firm that’s changing it all. 420 CP not only provides card acceptance services to medical marijuana dispensaries but can also connect them with access to capital.

Using the concept of MCA, 420 CP and their funding partner will provide actual loans based on credit/debit card processing volume It’s a joint partnership. (Sorry couldn’t resist!). And there’s great news. The typical easy criteria that made traditional MCAs so popular still applies. So long as the license to sell medical marijuana can be proven, dispensary owners have the same odds of being approved as a restaurant would.

So the oportunity is there and the target market is bigger than most people think. According to Nick, “Medical marijuana is legal in sixteen states and DC to the best of our knowledge. Those states are: AK, AR, CA, CO, DC, DE, HI, ME, MI, MT, NV, NJ (still pending), NM, OR, RI, VT and WA. Some of these states are in the throes of evaluating how to implement the ballot measures that were passed and they do not all enjoy the same structures.” But once the ground rules are in place, it’s business as usual. “We have faced no problems as our company is dedicated to providing credit card processing services solely to the medical marijuana industry. As you can imagine, our clients love us.”

Add that to the ever growing list that the Mechant Cash Advance concept is being applied to.

- Damaged Credit? Funded!

- Short Time in Business? Funded!

- Restaurants? Funded!

- Retail Stores? Funded!

- Auto Shops? Funded!

- Las Vegas Casinos? Funded!

- E-Bay Stores? Funded!

- Medical Marijuana Dispensaries? Funded!

Short on capital? If you accept electronic payments, someone somewhere is willing to provide cash against those future sales. No matter what you do…

– The Merchant Hash Advance Resource

###

About 420 Card Processing

420 Card Processing was founded by card processing professionals, with decades of combined experience, who are committed to equal access and opportunity for those involved in all aspects of providing medical marijuana to patients in states that have legalized its use. 420 Card Processing provides services to retailers, wholesalers, suppliers of gardening equipment, and physicians. 420 Card Processing is a member of Americans for Safe Access, California NORML and the National Cannabis Industry Association.

For more information on obtaining a merchant account or funding from 420 Card Processing, contact Nick Emerson:

Sales@420cardprocessing.com

(800) 579-1675900 E. Hamilton Ave.

Suite 100

Campbell, CA 95008

Merchant Cash Advance Diminished by Growth of Payment Technologies

May 15, 2011

Technology will be the end of us all

When bank lending dried up, Merchant Cash Advance (MCA) providers fulfilled the need to keep America’s small business owners going strong. By withholding a percentage of each credit/debit card sale automatically, there was no need to worry about a client’s ability to make payments. Without the risk of late payers or non-payers, MCA providers singlehandedly eradicated credit score from the underwriting guidelines. Or so they thought.

Only a small percentage of businesses in default actually close their doors. Circumventing the MCA provider’s merchant processor or incentivizing customers to pay with cash are issues that have plagued the industry for years. While this would constitute a clear breach in the sale of one’s future receivables, it’s not always a deliberate act of malice. However, there is a direct correlation between the frequency of breaches and *surprise* declining credit score.

But in the instances without malice, such as if damaged POS equipment prevents the flow of processing, there’s not much a MCA provider can do other than help fix it. These gaps in collection affect the bottom line and lead to upward pressure on costs or tighter restrictions on approval, two outcomes that nobody wants.

And as if there already wasn’t a strain, changes in payment technology are quickly eroding the MCA industry’s turf. The credit/debit card sales of a business aren’t exactly limited to one of these:

Now there are options, lots of them. In today’s world you can accept electronic payments with almost anything, a conundrum for MCA providers aiming to collect a percentage of all of it. And how about those routine PCI compliance upgrades? There are countless businesses with a basement full of old credit card machines that could be plugged back in, put back into service, and freely used to circumvent their financial obligations.

Take this clothing retailer for example. She qualified for an advance of only $5,000 but when it came time to convert the merchant account, the process wasn’t so easy:

Nearly all of the transactions conducted inside the store happen through the touch screen POS. The merchant statements reflect consistent historical sales of nearly $4,800 per month, instilling the belief that the future won’t be much different. But when the customer lines get too long, there’s a backup credit card terminal that they pull out from under the counter that still has an active account with a previous processor. Around the holidays, they dig out the old Tranz model terminals from the basement and use them too. For street fairs and trade shows, they attach their Square to their iPhone and process on the go. And when it comes to their website and Ebay, PayPal is their preferred method of payment.

This doesn’t mean the touch screen POS won’t continue to see $4,800 worth of action per month, but the situation doesn’t inspire a lot of confidence if the goal is to collect a percentage of their credit/debit card sales. What if they occasionally use Square inside the store? What if phone orders are punched into PayPal? These things may happen inadvertently or simply because their customers demand it.

To firmly secure a purchase of future sales, the MCA provider would need to do the following:

- Convert the touch screen POS system (which will very likely come with a fee from the POS reseller)

- Reprogram their backup terminal

- Reprogram all the old terminals collecting dust in the basement

- Force the return of the Square and replace it with their own iPhone processing attachment

- Delete PayPal from the HTML of the business’s website

- Instruct them to stop conducting business on Ebay

- Cancel the PayPal account altogether and replace with an authorize.net virtual interface or something equivalent

That’s a lot of effort for $5,000 but doing anything less is a gamble. That’s another reason why MCAs are more expensive than bank loans. Without set fixed payments, they are extremely vulnerable to economic ups and downs and now the explosion of payment alternatives.

Rather than stay ahead, the industry is becoming more fractured as evident by the rise of new funding sources such as Kabbage, that lends against future PayPal sales. It’s innovative but vulnerable. Kabbage depends on the success and status quo of PayPal for survival, a characteristic that is not likely to carry them far. Similarly, MCA providers are dependent on withholding a percentage of future sales, an uneasy task in a world where the point of sale itself is changing.

Innovation in the MCA space has gone as far as automated bank debits and a lockbox. One depends on the merchant’s use of a single bank account and the other is equally exposed to the issues we’ve discussed.

Which of course begs the question: If electronic payments are becoming more elusive to capture, how can the MCA industry survive? The obvious answer is to transform the product itself into a loan. Secure it against collateral and have the credit bureaus at your disposal. Breaches will become far less likely and electronic payments less elusive when there are actual consequences involved. It’s a dreaded word and one MCA representatives have spent years avoiding, but according to the state of California, it’s probably a loan already anyway.

As MCA providers struggle to keep up with payment alternatives, banks are wondering when we’ll all wake up from the “it’s not a loan” euphoria. If the goal is to provide capital and get more back, reprogramming a terminal isn’t going to cut it. How many free hours can America Online offer to bring people back to their dialup internet service? Technology changed and the age of AOL ended. So too may the age of Merchant Cash Advance…. at least in its current form.

– The Merchant Cash Advance Resource