Meet the Source: How Jared Weitz and United Capital Source became one of the industry’s fastest growing shops

October 23, 2015Jared Weitz came from humble beginnings and nearly settled for a humble fate. But associates say an ordinary, uneventful life wouldn’t have suited him – he works too hard and figures things out too quickly.

Almost ten years ago Weitz, 33, was parking cars to earn money for community college. After finishing at St. Johns University, he almost made plumbing his career. But now he’s CEO of United Capital Source LLC, an alternative-finance brokerage with deal flow of between $9 million and $10 million a month and an annual growth rate of over 65 percent.

Business associates, former bosses and his small cadre of employees all seem to revere Weitz for his honesty and straightforwardness. They consider him a personal friend. They say he continues to grow as a businessman and as a human being while taking pleasure in helping others do the same.

Geographically, Weitz has the good fortune to know where he belongs – the city of New York is in his DNA. “Every time I fly back,” he said, “I’m so happy to land.”

His love affair with the city began in Brooklyn. He was born there and raised in a Brighton Beach apartment in the shadow of Coney Island. When he was 16, the family moved to Oceanside on Long Island.

As the second of six children, Weitz had to come up with the money for college on his own. “My older sister and I had to pay our way,” he said. “Everybody else, my dad was able to cover.” He started school at Nassau Community College, selling cell phones and parking cars at night.

But then came an abrupt change. Once Weitz saved enough money, he transferred to Tulane University in New Orleans to pursue a relationship with a woman who was finishing her studies there. He attended classes part-time, worked as the athletic director at the Jewish Community Center, tended bar in a Mexican restaurant and served summonses for a law firm.

But then came an abrupt change. Once Weitz saved enough money, he transferred to Tulane University in New Orleans to pursue a relationship with a woman who was finishing her studies there. He attended classes part-time, worked as the athletic director at the Jewish Community Center, tended bar in a Mexican restaurant and served summonses for a law firm.

The relationship with the woman fizzled, but Weitz made lasting friendships during his days down south. His old roommate in New Orleans, who now practices law in Atlanta, serves as counsel for United Capital Source.

When Weitz had been in New Orleans for two years, Hurricane Katrina struck. He evacuated to Houston, where he stayed in a Holiday Inn for two weeks before realizing he wouldn’t be able to return to southern Louisiana anytime soon. The magnitude of the devastation was just too great.

Shouldering the duffel bag of belongings he had managed to pack on his back during the evacuation, he returned to New York, enrolled in St. John’s University and began working in sales for Honda Financial Services and parking cars.

Weitz had started school expecting to become a teacher. He had grown up with younger siblings and liked leadership roles, which convinced him teaching would be a good fit.

Still, many of his college jobs had required him to sell. As a bartender, for example, he promoted drink specials. As an athletic director he convinced people to sign up for classes. “Everything that I took to naturally wound up being in the sales, marketing and finance arena,” Weitz observed.

When he was nearly finished at St. John’s, Weitz was parking a car for an acquaintance who offered him a job as a union plumber. Suddenly, he was making $27 an hour and had health benefits. “It was a big breather for me,” Weitz recalled.

He quit his three jobs and labored as a plumber from 7 a.m. to 3 p.m. School started at 3:30 p.m. for him and stretched into the evening. But when he finished his degree, working as a teacher for $35,000 to $40,000 a year no longer seemed attractive.

Besides, his plumbing work didn’t center on toilets. On typical commercial plumbing jobs he did things like install air, medical and gas lines in hospitals. He was reading blueprints and bidding for jobs. A promotion to foreman didn’t seem that far off.

At about the same time, near the end of 2006, a friend, Mike Caronna, landed a job at Bizfi, formerly known as Merchant Cash and Capital (MCC), The company, which had just started and had only a few employees, was looking for underwriters.

As fate would have it, Weitz fell into a conversation with a fellow union plumber, one who had been on the job for 30 years. The older man reminded him that his wages would never climb much higher than they were right now. The veteran plumber then showed the younger man his hands, bent from decades of holding tools. “That got me thinking,” Weitz said.

He asked his friend Caronna to arrange a job interview at MCC. He got an offer and took a 90-day leave from his plumbing job to give the world of finance a try. “After about two weeks, I knew it was for me,” he said of the alternative-finance industry. It was by then the beginning of 2007.

Weitz excelled as an underwriter, and the company CEO, Stephen Sheinbaum, picked him and four others for a sales contest. Sheinbaum gave them some leads and turned them loose. Weitz won the competition but asked his boss to help him gain experience in business development and operations before taking on a sales position.

Sheinbaum was happy to comply. “He is one of the best and the brightest in the space,” he said of Weitz.

So, at age 25, Weitz found himself building a business development department by cultivating relationships with ISOs and persuading them to send business to MCC. “It was amazing,” he said of those days. “That was a big opportunity.”

Weitz learned the mechanics of the business. He found that the right ISO can originate good deals and a bad ISO can ruin deals. He learned the politics of when to talk, when to remain silent and when to let someone vent.

Then Weitz and a good friend at MCC, Anthony Giuliano – who’s now managing partner of Sure Payment Solutions – worked out how they could improve the MCC sales effort. They pitched Sheinbaum on the idea of having a second internal sale force, and that led to the birth of Next Level Funding (NLF), a division of MCC.

Weitz and Giuliano each owned 10 percent of NLF, and MCC owned 80 percent. “I’m 26, about to be 27, and I’m like, ‘You did it, Man,’” Weitz said as he looked back.

After about four months, NLF absorbed MCC’s original sales division. Next, Giuliano and another executive, Paul Giuffrida, decided to leave MCC. Weitz felt torn. He felt an allegiance to Giuliano and respected Giuliano’s knowledge of programming – a subject that was alien to him. Yet Sheinbaum had provided Weitz a series of opportunities.

Weitz stayed at MCC but felt he deserved to become chief sales officer. When that didn’t happen, he sold his shares back to the company at a dramatically reduced price to extricate himself from a non-compete clause and set off to start United Capital Source (UCS).

With a five-figure investment, Weitz and his then partner, started UCS in January of 2011 in a 250-square-foot office in Long Beach, L.I. Weitz invested about 90 percent of the money he had saved while working at MCC.

Jon Baum left NLF with Weitz and became the first UCS employee. Within a week or two, Danielle Rivelli, left NLF to join UCS, and Weitz put the remaining 10 percent of his savings into the business to meet the expanded payroll. Today, Baum and Rivelli are UCS sales managers.

Jon Baum left NLF with Weitz and became the first UCS employee. Within a week or two, Danielle Rivelli, left NLF to join UCS, and Weitz put the remaining 10 percent of his savings into the business to meet the expanded payroll. Today, Baum and Rivelli are UCS sales managers.

The first month UCS was open, it funded $240,000 in deals. “It just felt good to be on my own and start funding deals,” Weitz said. From the beginning of UCS, he won praise from funders for bringing them the right kind of deals with merchants who were likely to repay.

“He really has the pulse of the marketplace and what a lender is looking for,” said Todd Sherer, who handles business development for Entrepreneur Growth Capital. “He doesn’t waste time giving you transactions that don’t fit in your box.”

That’s because doing things right means a lot to Weitz. “He is one of the most straightforward, honest, high-integrity people I have met in the industry,” said Steven Mandis, adjunct associate professor at the Columbia University Business School and chairman of Kalamata Capital LLC.

He’s won the OnDeck seal of approval. “OnDeck has a rigorous and extensive background check process as part of our broker certification process,” said Paul Rosen, OnDeck’s chief sales officer. “Jared Weitz and United Capital have passed our screens and process and are currently active brokers for OnDeck.”

And with time, Weitz has learned patience. He was sometimes short with funders when he started his company but has matured into a pleasant person to deal with, said Heather Francis, CEO of Elevate Funding. “I’ve seen that growth with him,” she said.

All of those good qualities soon came together to help UCS succeed. Within four months of its launch, the company rented a 1,500-square-foot office in Garden City and hired two more people. Next came a 3,200-square-foot office in Rockville Centre and three more employees.

“The company was growing and gaining traction,” Weitz recalled. “I bought out my original partner.” Since then, Vincent Pappalardo has invested in UCS and become a minority partner.

Meanwhile, the lease was expiring on Long Island, and Weitz felt the time had come to move to Manhattan. That would enable the company to draw employees from throughout the region and not just Long Island.

“We decided to bite the bullet and pay the excess money to move to the city because we believed it would be better for the business,” Weitz said. He added two people and rented a 5,500-square-foot space near Penn Station in the Garment District in September of 2014.

Within three months of making the move to Manhattan, business doubled. “Being in a faster-paced environment caused the business to go through another growth phase,” he said. After nine months in the city, UCS is now taking over a whole 8,500-square-foot floor of the same building.

Within three months of making the move to Manhattan, business doubled. “Being in a faster-paced environment caused the business to go through another growth phase,” he said. After nine months in the city, UCS is now taking over a whole 8,500-square-foot floor of the same building.

UCS remains a small shop in terms of headcount with 21 people, but the company’s funding numbers equal the output of many brokerages five times its size. Twelve of the UCS employees work in sales, with the others engaged mainly in underwriting, operations and customer service.

Less than 2 percent of UCS’s funding volume comes from broker business. “We self-generate all of our business,” Weitz said, declining to elaborate too much on his company’s marketing efforts.

“My salespeople – bar none – are the best in the industry,” he claimed. “Much like the Navy has the SEALS and the Army has the Rangers, there are groups in the industry that can do triple or quadruple what other people do because that’s just the way they are.” His people fund an average of $750,000 per month per person in new business, while his renewals reps fund well into the 7-figure range per person.

UCS salespeople achieve their results because they have detailed knowledge of the industry, Weitz said. The staff’s understanding of alternative finance doesn’t end with sales but also includes underwriting and finance, he noted. “That’s what makes you a very good and knowledgeable sales rep,” he maintained.

His salespeople don’t just tell a client what he or she wants to hear. They take the time to understand the client’s financial situation. “They know how to read a profit and loss statement, a balance sheet and tax returns,” Weitz said.

ARE THE BEST IN THE INDUSTRY”

While 90% of Weitz’s sales team has a college degree, most of the salespeople have come from outside the industry, he said, noting that one was with Sleepy’s, the mattress company. Another was selling memberships at a gym, one worked for a credit card processing company, two were barbers and one had just graduated from college.

UCS doesn’t make double-digit commissions because the company isn’t over-charging merchants, Weitz maintained. The company does not obtain excess funding that a customer can’t afford or increase the factor rate to dangerous levels, he noted.

“You’re not really helping the merchant” by providing too much capital, Weitz asserted. “You’re sucking the blood out of him before he goes away. That’s not why I’m in business.”

A clean record will also prove beneficial when federal regulation comes to the industry, he said. Integrity in the workplace can also spill over into other parts of a person’s life, Weitz believes.

As UCS grew larger and Weitz grew older, he saw his employees rent their first apartments and then buy their first homes. He learned then that he had taken on more responsibility than was apparent to him at first.

As UCS grew larger and Weitz grew older, he saw his employees rent their first apartments and then buy their first homes. He learned then that he had taken on more responsibility than was apparent to him at first.

To accommodate the employees he added a human relations department and commissioned a company handbook. He’s also started marketing, finance, operations and other departments.

He’s lost only four employees because he pays them well, respects their time and doesn’t view their youth as a liability.

Meanwhile, talking daily to merchants and hearing about their heartaches and triumphs has humbled and matured Weitz. Seeing how the merchants’ choices panned out or fell short also shaped him and helped him grow up a little, he said.

Weitz has found time in his 70-hour workweek to meet his future bride. They’re planning to wed next year, and he plans to invite his entire staff. “It wouldn’t feel right without them,” he said.

Weitz has skipped the Ferrari, Rolls Royce and mansion because he didn’t feel he needed them. But even without those status symbols, it’s clear that Weitz has avoided settling for a humble fate.

As for what comes next, UCS is said to be developing an online marketplace to take their business to the next level, though Weitz declined to provide specific details about how it will work. “We’re on pace to do more than $100 million worth of deals a year,” Weitz said. “And as far as we’ve come, I feel like this is still just the beginning.”

World Business Lenders Acquires Uber Capital, Adds Another Branch

October 2, 2015 Zachary Ramirez, a Branch Manager for NY-based World Business Lenders (WBL) confirmed the company had set up two new branches.

Zachary Ramirez, a Branch Manager for NY-based World Business Lenders (WBL) confirmed the company had set up two new branches.

South Miami-based Uber Capital was acquired and will become a WBL branch. “The founders of Uber Capital, Jessica Fonseca, Tim Fenimore and Tristan Olmedo-Tigertail have joined WBL as Co-Branch Managers,” wrote Ramirez. The company was organized only 8 months ago.

Additionally, WBL has formed a new in-house branch at their 120 W. 45th Street office in Manhattan. “Michael John and his team have joined WBL to establish a new branch designated as the Midtown Branch located at our headquarters location,” Ramirez wrote.

The lender has made scores of small acquisitions this year, particularly merchant cash advance ISOs. As one of the few players in the industry to operate under a multi-branch model, they have no intention of slowing down. “We plan on acquiring many, many more branches in the coming months,” Ramirez posted.

Business Financial Services Rebrands as BFS Capital

September 21, 2015 CORAL SPRINGS, FL, September 21, 2015 – Business Financial Services, Inc., a leading technology-enabled small business financing platform, announced today that it has rebranded as BFS Capital and launched a new website, www.bfscapital.com. As part of this rebranding, the company has also unified its North American business affiliates.

CORAL SPRINGS, FL, September 21, 2015 – Business Financial Services, Inc., a leading technology-enabled small business financing platform, announced today that it has rebranded as BFS Capital and launched a new website, www.bfscapital.com. As part of this rebranding, the company has also unified its North American business affiliates.

A champion of small business, BFS Capital provides flexible, timely solutions for customers without access to traditional financing. The new BFS brand conveys a sustained commitment to empowering the growth and success of these businesses. Today, BFS Capital offers loans and merchant cash advances – up to $2 million – to small businesses across 400 industries in all 50 states, the United Kingdom and Canada through its extensive network of independent sales organizations, as well as its direct sales and online channels.

The rebranding reflects the company’s deep experience serving the diverse financing needs of small businesses, its commitment to innovative products and technology, and its expanded market opportunities. “As we have grown and acquired new partners over the years, we saw the need to unify our businesses under a single brand representative of our rich history and bright future,” said Marc Glazer, CEO and co-founder.

BFS’s affiliates, Entrust Merchant Solutions, GBR Funding and Premium Capital Group, are also known as BFS Capital, which now has more than 275 employees. The former Entrust team has become the BFS direct sales group, led by Ilya Fridman as Senior Vice President. UK affiliate, Boost Capital, will retain its name.

About BFS Capital

BFS Capital champions the long-term growth and prosperity of small businesses by providing timely, flexible financing solutions. BFS’s leading small business financing platform leverages customized underwriting and proprietary algorithms to fund up to $2 million for businesses in all 50 states and Canada, and through its affiliate, Boost Capital, in the United Kingdom. Since 2002, BFS has provided more than $1 billion in total financing to small businesses across more than 400 industries. Headquartered in South Florida with additional offices in New York, California and Georgia, BFS is an accredited BBB company with an A+ rating. For more information, please visit www.bfscapital.com.

Contact

Abby Trexler, Peppercomm

bfs@peppercomm.com

Expansion Capital Group Crosses $50 Million Milestone

August 27, 2015 Move over New York and Silicon Valley, Expansion Capital Group (ECG), a young Sioux Falls, South Dakota-based business lender is quickly rising up the ranks. Founded just two years ago, a company representative has confirmed to AltFinanceDaily that they’ve already funded more than $50 million to small businesses nationwide.

Move over New York and Silicon Valley, Expansion Capital Group (ECG), a young Sioux Falls, South Dakota-based business lender is quickly rising up the ranks. Founded just two years ago, a company representative has confirmed to AltFinanceDaily that they’ve already funded more than $50 million to small businesses nationwide.

While South Dakota might be better known as the home state of Mount Rushmore, they have made a name for themselves in an industry largely centered around New York, California, and South Florida.

Jay Larson, ECG’s COO, shared with AltFinanceDaily, “We are definitely excited to cross the $50 million deployment milestone. First and foremost, we’d like to thank all of our industry partners for all their help and support in getting us here. Second, this is only the beginning of ECG’s journey [and] as such we’re looking forward to reaching the $100M milestone in a much shorter period of time.”

On the industry leaderboard, ECG is not that far behind competitors that have been in the industry for much longer. Credibly, for example, has reportedly funded more than $140 million since inception but that’s spread out over a period of more than four years.

Merchant Cash and Capital Hits a Billion Dollars

March 18, 2015I was there. In August 2006, a little startup in College Point, Queens hired its third and fourth employees. One of them was me. The company’s CEO Steve Sheinbaum hired us to be underwriters of a financial product that at that point didn’t really have a name. It would later become referred to as a merchant cash advance.

The company grew fast, almost too fast. By December of 2006, half of the company was working out of temporary offices in the Empire State Building. And when that no longer made sense, we leased a floor at 450 Park Avenue South in mid-2007 where Merchant Cash and Capital still has its headquarters today.

Fast forward to 2008, I was the most senior risk manager of the firm. As the Director of Underwriting, my direct reports were two underwriting managers. Below them were three or four team leaders. And below them were entry-level underwriters and their administrative assistants. I oversaw what was arguably the most important department leading up to the financial crisis. I really believe the hard work of all the underwriters and the seriousness of which they took their job is a huge contributing factor to why MCC survived when many of their competitors did not.

It is great to see them hit the milestone of $1 billion in funding. Congratulations.

The End of an Era

September 19, 2012It’s the end of an era. Sound ominous for a blog that reports on the Merchant Cash Advance (MCA) industry? It shouldn’t. In the last 10 years, MCA firms played in the minor leagues. No one was really paying attention to them and truthfully, a lot of critics didn’t think this business model would still be around. But today it still stands, funders are still funding, and this blog is practically struggling to keep up with the incredible amount of action that is taking place. Coincidentally, 2012 marks the end of the Mayan Calendar. Yes, it’s the end of an era.

MCA Goes From 0 to 60

There were a few big firms in the Mid-2000s (RapidAdvance, Merchant Cash and Capital, Strategic Funding Source, AdvanceMe, etc.) and they’ve all experienced modest success. It was “modest” in the sense that it is nothing compared to today’s standards. The level of play is changing. Wining and dining an Independent Sales Office (ISO) that could bring in $300,000 a month in deal flow used to be all the rage. 300k for one company was 300k less for a competitor. An extra point of commission here or a freebie approval there was enough to make you the big dog in town, at least for awhile. Despite all the supposed innovation and growth, the talent pool remained the same. Lead generators became agents, agents became ISOs, ISOs became syndication partners, syndication partners became funders, and funders became technology companies that were basically clearing houses for groups of funders. If the industry was Sally, Joe, and Tom in 2005, it was still Sally, Joe, and Tom in early 2011, just with new company names or titles. Then everything changed…

Money poured in:

Merchant Cash and Capital Announces $25 Million in new financing 10/4/11

Snap Advances raises $3 Million from TAB bank 11/21/11

Capital Access Network raises $30 Million 2/7/12

RapidAdvance Receives new financing facility through Wells Fargo 4/2/12

1st Merchant Funding | $5 Million re-discount line of credit from TAB bank 6/12

Strategic Funding Source secures $27 million 6/27/12

On Deck Capital raises $100 Million 8/23/12

Kabbage raises $30 Million 9/17/12

Industry insiders loosely redefined what a Merchant Cash Advance was:

Merchant Cash Advance Redefined Merchant Processing Resource 3/25/12

Big companies entered the market:

American Express Announces Their Own Merchant Cash Advance Program 9/22/11

PayPal Pilots Merchant Cash Advance Program in the U.K. 7/13/12

Some funders became licensed lenders in major states such as California:

A New Chapter Opens for Merchant Cash Advance The Green Sheet 6/25/12

Search the California licensed lender registry

New products formed:

FundersCloud creates platform to raise capital and find syndicate partners faster 8/29/12

A charity announces a new way to make subsidized business loans using the split-funding method 9/6/12

These barely scratch the surface of industry events. What used to be a competition to score the local neighborhood ISO has morphed into a race to be the first to partner up with Facebook, twitter, Groupon, and Square. Anyone not moving full speed ahead to integrate technology and social media will be gone in the next 24 months.

May 18, 2012 was the first time we noticed and commented on what was happening. In How The Facebook IPO Affects the Merchant Cash Advance Industry, venture capitalists and Silicon Valley had finally found MCA and there’s no hiding from them. Now it seems all of our far-fetched predictions are not only coming true, they’re happening moments after we predict them. In our last article we instructed everyone to keep their eyes on Kabbage. Six days later they announced they had raised $30 million in new financing and would be expanding overseas. For a company that makes wild claims about the correlation of facebook fans with account performance, all while humorously being named after a boring vegetable, they sure seem perfectly able to threaten the status quo. Nobody dared touch Ebay or Amazon businesses until they came around.

Price

On the cost basis front, the middle ground is eroding even further. We first discussed this phenomenon on April 25, 2011 in The Fork in the Merchant Cash Advance Road. In it, we explained that the combination of competition and defaults were placing downward pressure and upward pressure on price at the same time. Today, there is surging demand for “starter deals” at 1.49 factors that are payable over 3 months at the same time that more and more new lenders are offering 1 year loans at 10%. The low rate, 12-18 month term deals are nothing new. A few funders tried them in the past and most suffered irrecoverable consequences. This is history that the new players didn’t witness.

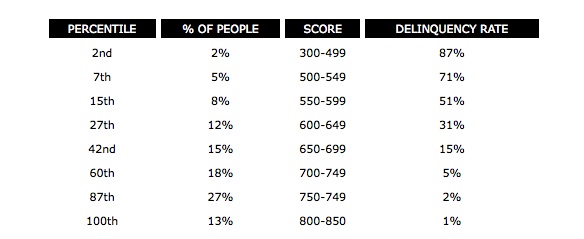

Some outsiders view the MCA industry as a bunch of Wall Street guys that got fat, happy, and disincentivized to lower costs. On the contrary, one only needs to take a single look at this chart to realize that undercutting the entire market isn’t so genius after all. How can a funder survive with extremely low margins when 15% – 71% of their target market is likely to experience problems repaying their loans? These aren’t our stats, these are FICO’s:

Veteran industry insiders know this and acknowledge that the coming tide of low rate financing is a bubble that has burst before. On the DailyFunder, a few folks have offered this insight:

The mca/unsecured loan biz is very risky. It’s all fun and games till deals start going south. My guess is they either adjust rates to match defaults or go out of business. I know first hand that this is not a get rich quick business. It may look like it is from the outside but once you are inside you see the world differently pretty quickly.

[these new low rate deals are] just like On Deck did. When they first came out, they offered 12 month 1.09’s. Then it dropped to 6 month 1.12’s, then 1.18’s. Now you see 1.25’s to 1.35’s offered by them

Governance

On the other side of the cost war is potential federal regulation. At least one D.C. consulting firm is prodding the leaders of the MCA industry to take a proactive approach on self-governance. According to Magnolia Strategic Partners, MCA is on the radar of regulators and members of congress, especially in light of the Dodd-Frank Wall Street Reform and Consumer Protection Act. The new MCA playing field has invited media attention, and not all of it is positive.

The North American Merchant Advance Association is the only organization for industry cooperation but their ability to dictate policies and standards is weak. They receive very little press and their website has been down for weeks. Many argue that they have been effective in minimizing defaults by sharing data on fraudsters. While this does stand to serve the community, it is but a footnote in their orignal intended purpose.

New Barriers to Entry

For the first time ever, potential resellers are facing barriers to entry. Becoming an ISO has long been as simple as owning a phone and purchasing a list of businesses that have used MCA financing before. Today, it’s not that easy. These lists have been sold literally hundreds of times over and called tens of thousands of times over. Pay-Per-Click marketing is dominated by the million and billion dollar firms with money to burn. If John Doe ISO wants to advertise on Google, he better be prepared to compete with the likes of American Express and Wells Fargo. Good luck! Putting skin in the game has also become more of a prerequisite for ISOs to succeed. Funders want to know if a sales agent would put his or her own money into a deal… and then actually commit them to doing just that. The odds are becoming stacked against the undercapitalized and it isn’t likely to change.

In 2009, the most prevalent pitch used by sales agents was to inform prospects that they themselves were “a direct lender” and that anyone else the prospect might be talking to was a broker. “Cut out the middleman and go direct with us,” they’d convincingly argue. This line became less effective when prospects heard this from all five agents they spoke to. Name dropping strategic partnerships will be the new way to build credibility. “We’re partnered with Facebook, twitter, Groupon, and Square,” a sales agent will soon be saying. “Can our competitors make the same claims? Go with us.”

See You On the Other Side

See You On the Other Side

2013 will kick off a single elimination tournament. Funders that didn’t realize 2012 was the end of an era will begin to fade. 2014 will eliminate the weaker firms that remain and by 2015, Merchant Cash Advance will no longer be a term that anyone uses. Big banks and billion dollar technology companies will go on to rebrand all that which the funding warriors of the last decade have worked so hard to establish. MCA will simply assimilate into other financial products. The metaphorical Sally, Joe, and Tom will probably still be in the business, but be working for companies like Capital One, Wells Fargo, and American Express. And as for us…well… we’re going to need something else to talk about. But we’ll keep you posted until that day. 🙂

– Merchant Processing Resource

../../

Largest Merchant Cash Advance in History Ends in Default

September 27, 2011 Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

While SFS was given high praise from their peers, some began to speculate if transactions that large were practical. After all, the costly financing of a MCA is priced in accordance with the risk of default, not in accordance with big profits for the financier. When your portfolio is in great shape, it can be easy to forget what the pitfalls are. And since the MCA industry paraded the Las Vegas Mob exhibit as the $4 Million deal that changed everything, we’re eerily reminded of the words by Jeff Mitelman, the CEO of AdvanceIt who was quoted two years ago as asking: “How prepared are you to lose $4 million dollars?”

We won’t pretend to know what led to the downfall of the Las Vegas Mob exhibit or why it went south so quickly. SFS could potentially lose 98% of their investment, a hit that will surely change their outlook on doing large deals in the future. The VegasInc article alleges gross mismanagement and fraud, factors that are difficult to foresee in the course of underwriting.

Industry message boards have been abuzz with comments on the default, with some competitors of SFS being accused of kicking a man while he’s down. “you ought to do smart funding, not just showing off your Balls,” one broker fired off at them. SFS has a stellar reputation and is one of the most knowledgeable firms in the MCA space. We have no doubt they inspected the merits of the deal backwards, forwards, and upside down. But nothing is perfect.

The default is expected to attract attention of the news media, leaving many to wonder how this transaction will be interpreted under the public eye. We assert that it will put to rest any criticism the MCA product has ever received about high costs.

Risk vs. Reward

Back in March when the deal was written, an outsider could claim that SFS just had an easy million handed to them. This view clashes with the Risk vs. Reward philosophy that MCA providers hold dear. To the MCA providers, the question was never “how can I make an easy million?” but rather, “how prepared am I to lose $4 Million?”

Any business that can’t get a bank loan, can’t get one for a reason. There’s a measurable value of risk that’s not worth taking. MCA providers fill the gap but compensate to offset defaults. There’s a term for something like this. It’s called a Happy Medium.

Merchant Cash Advance is the happy medium financing option for small businesses. And for the immediate future it is likely to stay within the small business niche. We all know now what can happen when the concept is applied to a multi-million dollar project. The outcome was not so happy and the loss not so medium.

But it will all even out in the end…

– Merchant Processing Resource

Small Business Finance Industry Mulls Crypto, NFTs

September 16, 2021 As the crypto craze roars on, NFTs are starting to stake a claim in the finance world as a legitimate option for those looking to invest or stash money in a virtual space. The sports world recently took their swing at NFTs, and here at AltFinanceDaily we minted NFTs of our own early this week. It seems that NFTs have sparked the interest of the media, athletes, and art enthusiasts— but in small business finance, the conversation is only in the early stages.

As the crypto craze roars on, NFTs are starting to stake a claim in the finance world as a legitimate option for those looking to invest or stash money in a virtual space. The sports world recently took their swing at NFTs, and here at AltFinanceDaily we minted NFTs of our own early this week. It seems that NFTs have sparked the interest of the media, athletes, and art enthusiasts— but in small business finance, the conversation is only in the early stages.

“I think of it more not so much as a currency, but from what I’ve been reading, more of an investment vehicle,” said Noah Grayson, President of South End Capital, when asked what he thinks an NFT represents. “It’s a way for people to put tangible items in a digital format to get ownership from.”

Grayson says those in his industry have brought up the topic around the office, but it hasn’t made its way into any type of business practices yet. “It’s tough to see how [NFTs] would affect the lending industry at this time, cryptocurrency is something a little more probable in the long term.”

Grayson stressed how difficult small business lending can already be with dollars, and it seems as though the industry just isn’t ready to start conducting business in other types of currencies. “When you consider that many small business owners have no credit score and a large portion of those still pay for things in cash, I think it’s going to be a long time before the industry as a whole considers [crypto] an option to make loans with or compensate partners [with] as a whole,” he said.

“I’d describe it as a digital asset that can be purchased, owned, and used by an individual, giving that individual exclusive rights to the asset,” said James Webster, CEO and founder of ROK Financial when asked how he would define an NFT. “Like any other asset, the price can go up or down over time.”

Although his company has never created an NFT themselves, Webster won’t eliminate the possibility for one in the future. With the interest of the industry and his employees being focused around crypto as of late, Webster can’t keep the crypto and NFT talk out of the office.

“We have a [clever] and nimble-minded staff at ROK. NFTs and crypto like other tradable assets are always being discussed and invested in here,” said Webster. “The team has been buying crypto for years now and I don’t see that slowing down any time soon.”

“We have a [clever] and nimble-minded staff at ROK. NFTs and crypto like other tradable assets are always being discussed and invested in here,” said Webster. “The team has been buying crypto for years now and I don’t see that slowing down any time soon.”

Webster believes it’ll inevitably make its way into the business with positive effects. “I see it streamlining, as well as making lending and banking for that matter more efficient over time,” he said.

At Velocity Capital Group, crypto has already seeped into the business. The company began offering commission payments to brokers this past August with an immediate positive reception. Velocity Capital Group CEO Jay Avigdor attributes “speed” as the primary use-case of crypto in his business.

“The feedback has been fantastic!” Avigdor said.

With crypto on the minds of fintech gurus everywhere, it’s evident its interest comes from the ability to put the technology in practice. Until these types of things can be borrowed, used to buy goods, or seen as a means of collateral at a mainstream level, the small business finance community will continue to eye their development and evolve if necessary.