Shopify Originated $226.9M in MCAs and Business Loans in Q4, Close to $800M For the Year

February 17, 2021 Shopify released its 2020 fourth-quarter earnings on Wednesday, revealing its financial arm’s latest stats. Shopify Capital originated $226.9 million in merchant cash advances and loans to businesses in the U.S., Canada, and the U.K.

Shopify released its 2020 fourth-quarter earnings on Wednesday, revealing its financial arm’s latest stats. Shopify Capital originated $226.9 million in merchant cash advances and loans to businesses in the U.S., Canada, and the U.K.

That is a posted increase of 96% over the same quarter in 2019 but was down 10% from q3. The full year 2020 originations of $794M were nearly double the $430M in 2019.

“Products like Shopify Capital are increasingly sought out by entrepreneurs and small businesses that face unnecessary barriers to access from traditional banks,” Shopify President Harley Finkelstein said in the quarterly earnings call. “Merchant empathy runs deep at Shopify. When traditional businesses were turned away, for the perceived high risk, we financed a record number of merchants when they needed it most.”

“We also introduced Shopify Capital to Canada and to the U.K. in 2020,” Finkelstein said. “To expand where we could help merchants.”

Shopify Capital still lagged behind rival OnDeck in origination volume, who reported a little over $1B in originations for the year.

Lawsuit Against Former MCC Executives Dismissed

February 12, 2021A lawsuit brought by various investment vehicles of Atalaya Capital Managment LP against former officers and/or senior management of Merchant Cash and Capital (later known as Bizfi), was dismissed on Tuesday.

In the judge’s decision, the Hon. Jennifer Schecter said that “plaintiffs seek to hold defendants, former officers and managers of Merchant Cash & Capital, LLC, liable for money plaintiffs lost by investing in the Company. […] Plaintiffs do not sue the Company for breach of contract; instead, they seek to hold the individual defendants liable for the Company’s deficient underwriting through causes of action for negligent mispresentation and fraud. Those claims fail.”

Bizfi failed in 2017 after a long run of being among the largest and earliest merchant cash advance funders in the US.

The case was in the NY Supreme Court under Index No: 655593/2019

Broker in Early Twenties Builds MCA Business in Less Than Three Years

February 10, 2021 Davron Karimov, a 22-year-old MCA broker, went from $10k in debt to collecting $200k a year in commissions. It took less than three years, and Karimov shared his journey on his personal, sometimes chaotic, yet always informative YouTube channel.

Davron Karimov, a 22-year-old MCA broker, went from $10k in debt to collecting $200k a year in commissions. It took less than three years, and Karimov shared his journey on his personal, sometimes chaotic, yet always informative YouTube channel.

The Staten Island native said he first started at a Long Island City shop and quickly made some early deals, eventually leaving to start his own firm, FunderHunt, and recently opened an office in Miami.

But do the YouTube videos help him make deals? Of course they do, Karimov says, and he not only gets deals through his video platform but he also get questions from other MCA brokers who reach out for help.

“Of course, we get people all the time calling in, people that have questions, people in the industry need help with their merchants,” Karimov says. “I started around 2018, and there was no info on YouTube about business funding, a huge void online. I stepped up and thought I could be the one to supply info.”

Nearly three years later, Karimov has built an expanding business while helping others through the struggles of being a broker and CEO in the MCA world. In the last year alone, the pandemic caused applications to explode, Karimov says.

“It’s been better than ever; I’ve never seen so many applications in March and April; they were just soaring,” Karimov says. “And then I’ve never seen so many applications get denied because of the industry at the time everything was shutting down.”

It was a time to capitalize if your shop was strong enough to survive what Karimov called the “dark ages” for MCA. If you survived, you get to reap the reward of a capital-deprived market, he says.

“The whole crisis took out so many funders that were just not good, they probably were supposed to go out of business a long time ago, but this accelerated it,” Karimov says. “It took out all the bad funders and replaced them with people that are solid, fast, and have everyone’s best interest at heart, from the merchant to whoever the ISO is.”

According to Karimov, 2020 solidified who is a real player in the game. Launching a new office himself, Davron says he enjoys sunny days in Miami while it is twenty degrees in-between blizzards in New York. Though snow wasn’t the reason he moved, but instead the funding environment.

“Everyone has been warm and welcoming [in Miami], the government knows what this is, and that’s what we do. We try to educate them: not a lot of people know here about this; it’s like it’s a secret,” Karimov says. “If you go to New York, it’s like everybody knows, there are so many shops there. But here, it’s kind of rare to see someone that knows what a cash advance is.”

Compared to New York’s increasingly restrictive funding ecosystem, the Florida space is open to growth. That’s exactly the environment Karimov hopes to profit from, expanding his business in any way that will be geared toward helping businesses.

“I’m not a huge fan of diversification,” Karimov says. “I like doing one thing. But we opened up an office in Miami; we’re bringing experienced people in and trying to fund deals as fast as possible. We’re maybe looking to develop into offering a debit card, whatever is in the business’s best interest.”

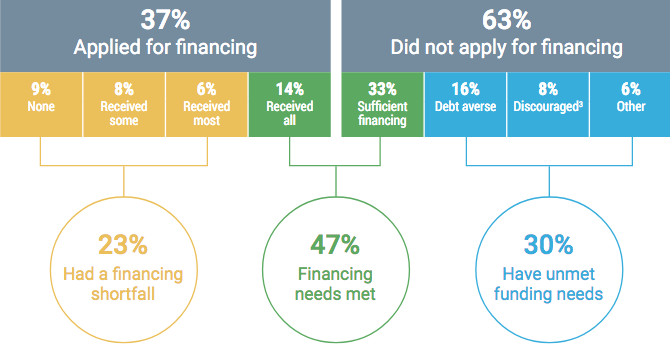

Over Half of Small Businesses Had Unmet Funding Needs

February 8, 2021The Federal Reserve’s analysis of overall funding efforts for all small businesses demonstrates a market of unmet financial needs. In 2020, a total of 47% of firms met their funding needs, while the other half (53%) still needed capital.

23% of firms saw a “financing shortfall.” They were partially approved but still needed more funds. The other 30% have unmet funding needs because they never applied according to the survey- they’re scared of debt, risk-averse, or don’t meet requirements.

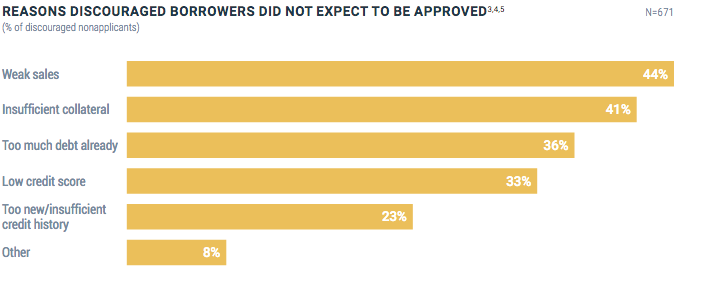

Those that did not apply for funds would have if they were not discouraged by weak sales (44%), insufficient collateral (41%), low credit (33%), and too much debt already (36%).

83% of companies used a bank or small bank as their primary financial service provider, while only 11% said an online lender or fintech was their primary.

Meanwhile, in the funding world, MCAs were only sought by 8% of all funding applicants last year, compared to 89% of firms applying for a loan or line of credit.

Most firms that went for an MCA went with a bank. 85% percent of firms that applied for a loan, credit, or cash advance used a large or small bank. In contrast, only 20% of firms applied to an online lender, falling from 33% since last year.

42% of firms that worked with online lenders or fintech companies were dissatisfied with support during the pandemic. Comparatively, firms that did receive some funding from an online lender were far happier: only 18% were dissatisfied.

Why Funders Are Investing in Real Estate As Their Side Hustle of Choice

January 25, 2021

After five years in finance, Peter Ribeiro decided to strike out on his own and start US Business Funding in 2008, providing equipment leasing and financing for businesses. But when the housing market collapsed four months later, Ribeiro saw a second major business opportunity emerge. Earlier that year, he had purchased a $250,000 home in southern California that appraised for $355,000 at the time he bought it. Within seven months, the home’s value plummeted to $95,000. “I told myself I knew the area really well, so I might as well start buying some properties.”

After five years in finance, Peter Ribeiro decided to strike out on his own and start US Business Funding in 2008, providing equipment leasing and financing for businesses. But when the housing market collapsed four months later, Ribeiro saw a second major business opportunity emerge. Earlier that year, he had purchased a $250,000 home in southern California that appraised for $355,000 at the time he bought it. Within seven months, the home’s value plummeted to $95,000. “I told myself I knew the area really well, so I might as well start buying some properties.”

At that point, Ribeiro’s fledgling company still wasn’t generating much revenue. “I thought, ‘Man, I just can’t get a lot of loans done right now. I only have three or four employees.’ That’s how I got into the real estate industry.” Twelve years later and at the height of a global pandemic, Ribeiro is simultaneously running two thriving ventures —US Business Funding, and a portfolio of hundreds of rental properties he now owns.

At a time when fintech startups and other industry innovators are looking for investors, alternative lending execs like Ribeiro are instead choosing to put their money in real estate to beef up their investment portfolios. Although some execs shy away from talking publicly about their real estate dealings, citing the fact that they don’t want too much exposure, the consensus is that there’s a lot of money to be made in buying, selling and renting property – if you know what you’re doing.

“I think real estate is lucrative because when you look at the history of investments, there are two or three ways to really make money: You can put your money in the stock market, or you can put it in bonds. And the other one guaranteed to go up in value is real estate,” Ribeiro says.

“I think real estate is lucrative because when you look at the history of investments, there are two or three ways to really make money: You can put your money in the stock market, or you can put it in bonds. And the other one guaranteed to go up in value is real estate,” Ribeiro says.

To Ribeiro, real estate offers a few major advantages: It’s a tangible asset. You can leverage it as it appreciates in value. Deductions make it so you pay very little in taxes. And it offers significant cash flow. “It’s the best investment you can make,” he says.

What makes real estate an especially good fit for alternative lending and fintech execs is that they possess the skills, resources and financial literacy to succeed at it.

“Real estate is a long-term gain,” Ribeiro says. “The industry we’re in is a cash-flow cow. People who are doing well are printing money. But what can you do with that money? You can put it in the stock market, but you won’t control much. Then you pay capital gains on it.”

Attorney Paul Rianda, who represents both cash advance clients and real estate investors, says it makes sense that real estate investing appeals to alternative lenders – especially amidst the uncertainty of COVID-19.

Attorney Paul Rianda, who represents both cash advance clients and real estate investors, says it makes sense that real estate investing appeals to alternative lenders – especially amidst the uncertainty of COVID-19.

“If you’re a cash advance guy and COVID happened, then you’re not doing very well,” he says. “If you diversified your assets by doing real estate and cash advance, you’re able to weather these downturns a lot more easily than you would otherwise.”

Rianda has not yet counseled any of his own cash advance clients on real estate matters. But based on his insights from working with both areas, he says real estate would be a logical move for MCA executives, and he’s seen some of his clients in the bankcard industry buy up properties.

“One of my clients had a portfolio of merchants and sold it for a few million, then flipped over to real estate. So it’s a means (to an end),” Rianda says.

‘Snowball effect’

Ribeiro has relied on a simple strategy to steadily build his portfolio of residential properties: Buy. Fix. Leverage. Repeat.

“I feel like the portfolio is doubling every couple of years. It’s just a snowball effect,” he says.

After Ribeiro buys a home, he waits about six months before he has it appraised and fixes it up in the meantime.

“If you go to the bank within the first six months of purchasing it, they’re going to give you the actual market value of whatever you purchased the house for,” he says. “If you wait six months, they’ll reappraise the home and give its true market value, which could be another 40, 50 or 60 percent. And so now you’re going to have a lot more equity in the house, and you’re going to get a lot more money when you leverage that home to go buy the next one.”

Ribeiro says he sees lots of people making the mistake of buying a home, and then going to the bank a week or two later for a loan.

Constantly maintaining a positive cash flow is Ribeiro’s number one rule of real estate investing. “Your best friend is depreciation,” he says.

Constantly maintaining a positive cash flow is Ribeiro’s number one rule of real estate investing. “Your best friend is depreciation,” he says.

Depreciation refers to one of the key tax benefits of real estate. Since owning a rental property is technically a type of business because it generates income, the property is considered a business asset. The IRS allows you to deduct the cost of acquiring that asset – the property – over the span of its useful life. For residential properties, the IRS sets a standard depreciation period of 27.5 years.

So if you buy a $100,000 property with a $20,000 land value, $80,000 of the asset is considered depreciable. Over the course of 27.5 years, you can take an annual deduction of just over $2,900 a year.

The trick, Ribeiro says, is to stick to lower-priced properties with an 80/20 home-to-land value. Most of his properties are single- and multifamily homes between southern California and Las Vegas.

Like Ribeiro, Rianda’s investor clients concentrate on one geographic area to find the best properties. “They look at the area for a long time, understand the area,” he says. “In my neighborhood, three blocks can make a 50 percent difference in the price of a house. You need to focus on a particular geographic area and do a lot of transactions in it.”

Small portfolio, big impact

Real estate investing has provided a way for Jared Weitz to earn more money while being able to focus on his primary job as CEO of New York-based United Capital Source Inc., the company he founded.

Real estate investing has provided a way for Jared Weitz to earn more money while being able to focus on his primary job as CEO of New York-based United Capital Source Inc., the company he founded.

“For me, it’s just a really good second income stream and a way to have a secure return of 4.5% to 6.5% a year,” he says.

Growing up, Weitz got a feel for real estate by watching his uncles invest in multifamily properties. At one point, Weitz’s uncle owned 15 different multifamily homes, and Weitz would help do the maintenance on them.

Eight years ago, Weitz invested in his first two-family home and has fixed and flipped eight properties since then. He currently owns two two-family homes and invests primarily in multifamily homes in Long Island, Brooklyn and Queens. Over the next five years, he plans to pick up at least two more four- or eight-family properties. Working with a small portfolio of residences in his home state has allowed Weitz to have full control over managing his properties and to turn a good profit.

“I think for me, it just offers more liquidity,” he says. “It’s an asset I can sell and liquidate at any time. That’s really important for me.”

Ideally, Weitz would like for his investment to build generational wealth that he can pass down to his son. With many people in the U.S. unable to qualify for mortgages, Weitz sees real estate investing as an opportunity to help the economy by giving renters a place to live and put down roots. “Depending on the neighborhood, you can put yourself in a situation where you have good renters for 20 to 30 years. They want to raise their families and have their kids grow up there,” he says.

Litigation among the pitfalls

Even though Ribeiro has had success with his business model, he cautions that there’s considerable risk involved with real estate.

“I love the industry. It’s a passion. It’s beyond my wildest dreams of the size of the portfolio and how well it performs,” he says. “But don’t think it’s all cupcakes and unicorns. There’s a lot to the madness. That’s why not everyone can replicate the model.”

“Professional litigators” and multiple lawsuits from renters are a major downfall that Ribeiro points to. He sees at least one substantial suit each year and tries to settle outside of court whenever possible.

“Professional litigators” and multiple lawsuits from renters are a major downfall that Ribeiro points to. He sees at least one substantial suit each year and tries to settle outside of court whenever possible.

As an attorney, Rianda says his real estate clients call on him not just for the purchase of the property, but for various issues that occur during the ownership period.

Here’s one scenario: A property owner has a tenant who isn’t paying rent, so the property owner sues the tenant. But while the lawsuit proceedings are under way, the tenant declares bankruptcy, which puts a stall on further litigation.

“There are people who understand the system and can make it difficult for you to get them out (of the property),” Rianda says, adding that it’s important to have legal counsel readily available. “You need someone who has really done this a lot and knows how the system works to get that person out of the rental property as quickly as possible.”

To minimize liability, Ribeiro has divided his properties into about 10 different business entities – each with a separate umbrella insurance policy.

Rianda sees his own real estate investor clients follow this strategy by grouping multiple homes under the name of an LLC. “If you personally own all these various assets, there’s the potential that if something catastrophic happened at one, it could bleed into all your other properties and potentially put them at risk,” he says.

Dual careers

Ribeiro’s real estate investments and finance company both serve as full-time occupations for him. Some years, he’ll focus more on one area than on the other, depending on market conditions. He spent more time on real estate between 2008 and 2013; then his business needs flip-flopped when real estate prices started going back up. This past year, he’s directed more attention to the finance company because of COVID, which necessitated some operational changes and a need to help clients who had been trying to get PPP loans. But he’s also started investing in commercial real estate, which has taken a hit because of companies forgoing office space to save overhead costs while employees work remotely.

Ribeiro expects to start seeing more mortgage defaults on lower-level homes in 2021 and 2022, after forbearance periods are over. And he’s been leveraging his assets to start buying more properties around the second quarter of the new year. “I think it will be a good time to start buying heavy again,” he says.

An attractive investment vehicle

With the pandemic weakening business portfolios, secondary investment options might sound like just what the doctor ordered.

When COVID first hit, some of Rianda’s clients started pursuing other investments like personal protective equipment (PPE). Most of his cash advance clients closed up shop for a few months.

When COVID first hit, some of Rianda’s clients started pursuing other investments like personal protective equipment (PPE). Most of his cash advance clients closed up shop for a few months.

“As time goes on, I’m starting to see my clients go back into their lending,” Rianda says.

Even as clients start to recoup their business, Rianda sees the wisdom in other investments and says cash advance executives are well suited for real estate. “It’s just a way that people who have been successful and spin off a lot of cash for their businesses see as a safe way to diversify their income,” Rianda says. “It’s something I find that people who are doing well in their business do, regardless of what business they’re in. So cash advance guys are just following the things people have done for years.”

Ribeiro cautions that people who get into real estate should look at it as a 10-year investment minimum, and not just a two- or three-month stint.

“It’s not a lottery ticket, and it’s not an overnight race,” Ribeiro says. “This is a long-term gain. But it’s a very lucrative gain from a cash-flow perspective and a tax perspective. I don’t think there’s a more attractive vehicle than real estate.”

Par Funding, Receiver Continue to Spar Over Its MCA Business

December 18, 2020 “From inception through 2019, [Par Funding] incurred a cash loss from operations of $136.2 million.”

“From inception through 2019, [Par Funding] incurred a cash loss from operations of $136.2 million.”

That’s the conclusion reached by Bradley D. Sharp, CEO of Development Specialists Inc (DSI), the financial advisor to the Receiver appointed in the Par SEC case.

Par has scoffed at the Receiver’s analysis of its business. “We do not necessarily begrudge attorneys, whose skill sets are often in other areas, a potential inability to understand the math that often makes for a strong and profitable financial model,” Par’s lawyers wrote in an October court filing. “There is a reason that smart, mathematically inclined people are typically hired by banks, hedge funds and financial services firms. But the Receiver and his counsel’s inability to understand Par’s business has led to all manner of baseless accusations that are easily answered in the very documents they possess but do not understand…”

Par says it was profitable and walks the Court throught its mathematical process. Sharp says Par’s assessment “is misleading and does not reflect actual operations at the company.”

Sharp alludes to Ponzi-like characteristics but refrains from using that term. “From inception through 2019, [Par] paid $231 million to investors, consisting of principal repayments totaling $135.6 million and interest payments totaling $95.4 million. [Par] could not have made these principal and interest payments to the investors without additional funds from the investors.”

Par explained that the key to its business is in the compounding:

“The merchant funding model is profitable because merchant funding returns are reinvested, either in a new or different merchant, or in an existing merchant with adequate receivables as a consolidation, or as a refinance of a merchant which may already have MCA funding from another provider. And the reinvestment begins on the merchant funding returns which commence immediately and occur daily. In very simple form, the math works as follows. Assuming $10,000 is funded to a merchant pursuant to a funding agreement providing for a funding return of $13,000 over the course of 100 daily ACH withdrawals, the agreement would provide for repayment to begin immediately with daily payments of $130. As those monies are returned, portions are used to pay operating expenses, but most of the monies are re-invested to fund other merchants. Mathematically, this means that the original $10,000 is being used to fund more than one merchant. Over the life of a single $10,000 funding, that same $10,000 can be used to fund multiple merchants, all of whom are paying funding fees in excess of the principal amount received. Thus, the original $10,000, at a 1.30 factor rate, generates $13,000 on the first merchant cash advance (MCA). Those funds are reinvested and generate $16,900 on the second MCA, and $21,970 by the third MCA – an increase of $11,970 over and above the initial $10,000. And that can happen within a year. This is the powerful compounding effect of the financial model.

That is the simplest version of the model. In practice, the model is far more sophisticated than that because the leveraging to new merchants of the MCA returns begins as soon as the MCA payments come in.”

Par additionally said:

“At the conference on October 8, 2020, the Receiver’s counsel told this Court, and many investors, that out of $1.5 million received per day from merchants prior to July 28, 2020, $1.2 million was used for new MCA funding. Thus, according to the Receiver’s counsel, only $300,000 constituted net collections, about 20%. The Receiver’s counsel appears to be suggesting that the company is not holding on to receivables but, instead, is refunding the same merchants 80% of receipts. This proposition is wrong and its assertion shows that the Receiver and his counsel do not understand the MCA business.”

One could assess that a large element of this case consists of the Receiver being like, ha! well look at this! and Par responding, well, yes, that is actually how our business works.

In fact, that is precisely the angle Par took in defending its use of funding new deals with money collected from deals previously funded.

“First, the numbers show that collections are used to fund new MCA deals,” Par’s attorneys wrote. “This may come as a total surprise to the Receiver and his counsel, but funding merchants is the business of Par. That is like criticizing Ford Motor Corp. for using its car sales income to build and sell more cars.”

Both sides agree that Par advanced over $1 billion to small businesses but Sharp says that “reloads” distorted the numbers.

“Use of reloads escalates the obligations of the merchant as each reload adds an additional ‘factor’ along with any new funds advanced,” Sharp wrote. “In [one example the reloaded funds are] subject to the factor twice; once when the funds were originally sent and again when they are included in the reload advance. The use of reloads also significantly distorts the calculation of loss rates as the advances are simply refinanced without becoming a loss.”

Sharp concludes that the true end result for Par is a much higher default rate than it lets on to.

And then there’s this

Sharp has repeatedly brought attention to a list of merchants with unusual payment and funding activity. Par countered by saying there are good explanations for each.

Amongst all of this is that company insiders are alleged to have received tens of millions in payments from Par and the Receiver is confident, in part due to DSI’s report, that Par was majorly unprofitable.

“Based on our review to date, it is apparent that [Par] would not have been able to continue to provide payments to investors, or to continue to operate, without additional funds from investors,” Sharp wrote in a December 13th report.

This case is not the first rodeo for Sharp and DSI in the merchant cash advance business. They were also assigned to manage the 1 Global Capital case.

The case is ongoing. The Court recently approved a motion to expand the Receivership estate.

CFPB Initially Proposed to Exclude MCAs, Factoring, and Equipment Leasing From Section 1071

December 17, 2020 After ten years of debate over when and how to roll out the CFPB’s mandate to collect data from small business lenders, the Bureau has initially proposed to exclude merchant cash advance providers, factors, and equipment leasing companies from the requirement, according to a recently published report.

After ten years of debate over when and how to roll out the CFPB’s mandate to collect data from small business lenders, the Bureau has initially proposed to exclude merchant cash advance providers, factors, and equipment leasing companies from the requirement, according to a recently published report.

The decision is not final. A panel of Small Entity Representatives (SERS) that consulted with the CFPB on the proposed rollout recommended that the “Bureau continue to explore the extent to which covering MCAs or other products, such as factoring, would further the statutory purposes of Section 1071, along with the benefits and costs of covering such products.”

The SERS included individuals from:

- AP Equipment Financing

- Artisans’ Bank

- Bippus State Bank

- CDC Small Business Finance

- City First Bank

- Floorplan Xpress LLC

- Fundation Group LLC

- Funding Circle

- Greenbox Capital

- Hope Credit Union

- InRoads Credit Union

- Kore Capital Corporation

- Lakota Funds

- MariSol Federal Credit Union

- Opportunity Fund

- Reading Co-Operative bank

- River City Federal Credit Union

- Security First Bank of North Dakota

- UT Federal Credit Union

- Virginia Community Capital

The panel discussed many issues including how elements of Section 1071 could inadvertently embarrass or deter borrowers from applying for business loans. That would run counter to the spirit of the law which aims to measure if there are disparities in the small business loan market for both women-owned and minority-owned businesses.

One potential snag that could complicate this endeavor is that the concept of gender has evolved since Dodd-Frank was passed in 2010. “One SER stated that the Bureau should consider revisiting the use of male and female as categories for sex because gender is not binary,” the CFPB report says.

But in any case, there was broad support for the applicants to self-report their own sex, race, and ethnicity, rather than to force loan underwriters to try and make those determinations on their own. The ironic twist, however, according to one SER, is that when applicants are asked to self-report this information on a business loan application, a high percentage refuse to answer the questions at all.

The CFPB will eventually roll the law out in some final fashion regardless. The full report can be viewed here.

Immigrating From Cuba With “Nothing in my pockets,” to a CEO Funding $12 Million a Month

December 15, 2020 “Work hard, don’t ask questions, and good things will happen to you,” Frank Ebanks described his keys to success in the MCA world. “Being Positive, working hard, and keeping my eyes open: If I hadn’t been looking for opportunities at 2 am in the morning on Craigslist, I would have never known about this industry, but it’s huge, it’s such a big industry.”

“Work hard, don’t ask questions, and good things will happen to you,” Frank Ebanks described his keys to success in the MCA world. “Being Positive, working hard, and keeping my eyes open: If I hadn’t been looking for opportunities at 2 am in the morning on Craigslist, I would have never known about this industry, but it’s huge, it’s such a big industry.”

Ebanks started what would become Spartan Capital shortly after seeing an ad calling for startup investors in an industry Ebanks had never heard of, called Merchant Cash Advance.

It was around 2016. Ebanks was up late in the NYU university library, putting himself through an MBA while working as a reactor operator at the Indian Point nuclear power plant in Westchester.

Despite the job security Ebanks enjoyed, he said he wasn’t happy with his career, wasn’t getting the satisfaction he wanted. He had already made it a long way— starting before the millennium as a Cuban immigrant, immigrating to the Dominican Republic in 1998 and then Florida in 2002 with empty pockets. Shortly after arriving, Ebanks enlisted.

“I spent some time in the army; I wanted to put in some time,” Ebanks said. “I said: ‘I’m a new immigrant, what’s the best thing that I could do to reward these opportunities?’ To serve in the army, give the country a couple years, and payback in advance for this opportunity that I knew I was going to have.”

Ebanks said he learned early on to take every opportunity seriously. He served for two years and then became an engineer and contractor for the army, working on the Patriot Missile defense system. He went through college at NJIT, graduating in 2009, and following in his father’s footsteps to become an electrical engineer.

After working with South Jerseys PSE&G, Ebanks took the opportunity to work full time shifts at the the nuclear power plant, and by 2016 he was pursuing an MBA and looking for ways to grow what he called “my empire.” Used to investing in small businesses already, discovering MCA fit right within his world.

“I’ve always been active, throughout my professional career I had businesses in real estate, I owned several businesses such as laundromats, a lot of retail cell phone stores and things like that,” Ebanks said. “So at one or two am in the morning, I’m working on how to build my empire. I was on Craigslist looking for opportunities, seeing what’s out there, and somebody wanted an investment, to partner up and start a company in a new industry.”

He took a meeting and learned a ton. Although he did not end up going into business with that person, he was hooked on the concept.

“I looked at that ad, and $10,000 later, we had a company,” Ebanks said.

He learned what he needed and ended up opening his own MCA business shortly after in New Jersey, finding he loved setting up syndicated MCA deals.

He learned what he needed and ended up opening his own MCA business shortly after in New Jersey, finding he loved setting up syndicated MCA deals.

“I did some research, opened an office in New Jersey, secured a manager to run the operation, and we started brokering deals and learning about syndication.”

He worked with SFS Capital, now called Kapitus. He fell in love with the immediate gratification feedback of making deals, seeing returns on account receivables, and watching renewals come in. The business grew, but things were not always a straight climb to success.

“There was a point where things were not going well and I had to start a new company, find new parters and investors with a funding direct-only focus, and moved into my basement- my wife was unhappy with that. I started hiring people, processors, underwriters, and ISO managers in my basement,” Ebanks said. “At one point, she said, ‘Okay, this is enough. Ten strangers are coming into my house every day, you’ve got to get an office,’ so we secured an office in New York. And that’s when things took off in 2017.”

At that point, Ebanks had shifted his business model from securing deals to funding them all his own, using capital he raised. Ebanks said that being a broker partnered with Kapitus was great, but he wanted to grow and run his business entirely. The best way to do that was through ISO management, Ebanks said. Ebanks let the direct sales team phase out and he hired ISO managers, learning the ISO business as he went.

“So fast forward now: We have over five ISO managers, and we’re funding about $12 million a month,” Ebanks said. “It’s been a phenomenal journey and the most rewarding thing I’ve ever done in my life; I’m not shy to share how exciting every day is to me, and how other than my family and my kids and God, this is the most important thing my life.”

For brokers looking to get started in the industry, Ebanks has this advice to share: Don’t settle.

“Don’t settle, look for growth, and invest your money,” Ebanks said. “I always invested everything I could, 95%, every penny on the business. It matters especially at the beginning, the more you invest, don’t let it sit.”

That investment should go toward your business, your staff, and hiring. Ebanks said the more you invest, the bigger the bag, the more your firm would grow, and your employees will grow with you. Helping employees will mean they will eventually leave, but in Ebanks’ experience treating employees right creates partners.

“Some of them now are partners, and the employee-employer relationship is always more partnership,” Ebanks said. “Some of them own their own companies now, and we help each other out. If they have a big deal, they say: ‘Frank do you want to take $50,000 out of this deal?’ I say yea I trust you. I’ve known you for years.”

Now that he’s on track to grow with recurring customers, seeing some merchants come back to renew twenty times since 2016, Ebanks sees a possible bright future for Spartan Capital: becoming a chartered online bank.

“It is an alternative lending space but to offer the best products to people,” Ebanks said. “I think at the end of the day, and we need all the resources we can get, the next chapter is to apply and secure an online bank charter, it’s the future of the fintech industry.

“Why do people like doing business with us versus a bank? Some of them can do business with banks, but they choose to use us because they have direct access to us after 6 pm, they could call us Saturday, they can call us on a Sunday,” Ebanks said. “A great relationship that they can never get from a bank. I want to bring what we do in MCA to the banking industry to serve people that want banking products, but I want to give them that MCA experience.”