PayPal Originated ~$2.6B in Funding During 2020

May 10, 2021 PayPal reported originating a total of about $2.6B in capital for U.S. SMBs in 2020, which doesn’t include the more than $2B in PPP loans it arranged.

PayPal reported originating a total of about $2.6B in capital for U.S. SMBs in 2020, which doesn’t include the more than $2B in PPP loans it arranged.

“PayPal delivered record performance in 2020 as businesses of all sizes have digitized in the wake of the pandemic,” Dan Schulman, President and CEO, said.

Exact origination figures are hard to track through the firm’s quarterly reports. The Working Capital product is only mentioned in passing. At the outset of the pandemic, PayPal reported that they helped merchants by “Granting deferral of repayments on business loans and cash advances at no additional cost.”

Throughout the remainder of the year, PayPal was echoing the problems of the industry and slowed down funding as a whole. In the 2021 first quarter call, John Rainey the CFO Global Customer Operations, said that the firm “Tightened underwriting and strong repayment activity contributed to lower balances in our merchant loan portfolio.”

PayPal’s origination volume fell relative to their 2019 estimate.

How Funders Survived PPP and a Year of Covid

May 4, 2021 A year into the pandemic and from the AltFinanceDaily office in Brooklyn, it looks like the world is opening up again.

A year into the pandemic and from the AltFinanceDaily office in Brooklyn, it looks like the world is opening up again.

After a year of Zoom and LinkedIn networking, those in the industry lucky or talented enough to have survived can still complain without restraint about big government lockdowns and misguided legislation. Competing with Uncle Sam’s deep PPP pockets have slowed deals down, and with a new fund opening this week for restaurants, it might be more of the same.

But two funders said that though there is an initial slowdown when a new stimulus is rolled out, the programs have still been vital for business– and if firms kept up with contacts, the business could be booming even after the pandemic.

CEO David Leibowitz of San Diego-based Mulligan Funding said that his firm survived the worst of the shutdown. That was due in no small part to government programs that kept merchants in business.

“People forget where we were sitting in April, May last year, 20 million people filed for unemployment. The segments of the market that we serve in general don’t have more than 30 days of cash on hand at any time,” Leibowitz said. “There’s no chance that our market survives that without the level of government support that they’ve been given.”

Sure, there’s a dampening effect at first, but there wouldn’t be B2B without businesses to fund. Leibowitz said he thinks the macroeconomic effects of printing money will have consequences in the long term, but it’s the lesser of two evils.

Matthew Washington, the well-known CRO of PIRS Capital, has also been vocal about PPP. Like Liebowitz, he said it has its pros and cons, creating a slowdown and demand for capital in one stroke. In his experience, because the stimulus was limited to payroll and rent, merchants were hungry for other products.

“They’re only able to allocate it for certain things, payroll, and hiring people, right,” Washington said. “Our funding allows them to be able to use capital for other opportunities, like buying supplies, buying inventory. Although it’s kind of been somewhat slow, they need to have other working capital needs to be provided for.”

Washington also said some merchants used their PPP funds as low-interest loans, paying off and refinancing advances. PIRS has succeeded through the pandemic due to its relationship-based model.

“It’s all about keeping in touch with your merchants during this time, having a big pulse with the people you do business with,” Washington said. “We’re really a lean and mean company, we kind of have the community bank approach to this space; we’re more relationship-based.”

PIRS had only paused for 60 days and was lucky enough to be set up with recurring merchant partners that turned out to be essential businesses.

“We were very blessed; a lot of our portfolio was operating during the shutdown,” Washington said. “Our portfolio did very well for the circumstance.”

That was how they survived, a lot of good faith and hard work, but pinches of luck as well. Leibowitz said that contrary to popular belief, many good people lost their business during the pandemic. It wasn’t just bad actors and funders with terrible underwriting.

“In March, we had customers who, for reasons totally beyond their control, couldn’t pay. And we weren’t sure in March, how long that would go on for, we weren’t sure how bad it would get,” Leibowitz said. “If you’d asked me in March, April, were we going to survive this thing. There’s no way I would have been able to give you a confident answer.”

Some with public securitizations, well-run businesses, dropped out and disappeared. Leibowitz said Mulligan was able to keep every employee on staff and got through the “sh*t show.” In part, it was with help from competitors who specialized in PPP funding that Leibowitz said his firm was still going strong.

“So I think for all of its shortcomings, I have a world of respect for the SBA and the program. I think of Brock and guys at Lendio, I think of the guys at BlueVine and Kabbage, who really have done a truly extraordinary job of distributing that product to our target market,” Leibowitz said. “And I’m sitting here today, unquestionably, enjoying the benefit.”

So PPP helped, despite the slowdowns, in the short term, and Liebowitz said in the long term, the government overspending might get hairy. But with talk about the world opening back up, with bars open down the block for the first time in a year, what does Washington think about the near future?

The world just isn’t going to stop; it’s just evolving with the new temp of what’s going on; I think there’s a lot of positive things on the horizon for our business,” Washington said. “Once the vaccine rates, and everyone’s ‘cured’ how are they not going to open up.”

Gregory J. Nowak, Partner at Troutman Pepper, Has Passed Away

April 13, 2021 Gregory J. Nowak, a partner at Troutman Pepper, passed away suddenly on April 11th at the age of 61.

Gregory J. Nowak, a partner at Troutman Pepper, passed away suddenly on April 11th at the age of 61.

The firm’s website introduced Nowak as a veteran attorney that was “sought after for advice on complex securities law matters, particularly on issues arising out of the Investment Company Act of 1940; the Investment Advisers Act of 1940; federal and state securities laws and regulations; broker dealer, FINRA, CFTC and NFA regulatory matters; and corporate and M&A transactions.”

That perfectly sums up the context in which I first encountered Nowak in 2017 when he spoke at a small event put on by the Alternative Finance Bar Association where I was the only non-lawyer in the entire audience. One might expect a presentation on the finer minutiae of securities law of which he gave, to be a mundane, easily forgotten experience for a financial journalist such as myself, but his energetic delivery and fluid command of the subject matter translated complex securities questions into a folksy debate wherein one could feel confident in resolving the Howey Test over the dinner table just as easily as they could in the courtroom.

In fact, I approached him afterwards to thank him on his presentation and even followed up later over email, asking if I might have the honor to list him as a recommended securities attorney on the AltFinanceDaily website. That was four years ago and as fate would have it, he remained the only recommended attorney that AltFinanceDaily formally listed under the securities category, despite my coming to know very many accomplished and competent attorneys in the same field of law.

Nowak was one of the earliest public voices in the world of merchant cash advance participations and syndication where the securities question was a consideration some weren’t even sure applied as the industry created new products and investing structures at a furious pace.

He spoke at AltFinanceDaily’s first major conference in 2018 on the subject of “Syndication and Raising Capital,” and he continued to generate recognition of the need for securities legal support in the burgeoning industry.

He was a co-author of an article published with a colleague at Pepper Hamilton LLP (now Troutman Pepper) that he had given permission to be reprinted on AltFinanceDaily in December 2018, titled MCA Participations and Securities Law: Recognizing and Managing a Looming Threat. It was read by more than 1,500 people on the AltFinanceDaily website that first day alone.

Nowak was highly sought out on merchant cash advance issues. “Most judges want to see consistency of treatment and that includes your vocabulary,” Nowak said in an interview with AltFinanceDaily in April 2019. “The word ‘loan’ should be banned from their email and Word files.”

Although our relationship was one of professional acquaintances, I often told those seeking advice about MCA syndication that they should “probably call Greg Nowak about that.”

In “Does Your Merchant Cash Advance Company Pass The Scrutiny Test?“, Nowak explained that funders that decide for business purposes to solicit money from investors, have to be careful not to run afoul of SEC rules. He said that he recommended funders treat these fundraising efforts as if they are issuing securities and follow the rules accordingly. Otherwise they risk being the subject of an enforcement action where the SEC alleges they are raising money using unregulated securities.

“You need to be very careful here because these rules are unforgiving. You can’t ignore them,” Nowak said.

California’s Business Loan & MCA Disclosure Law Is Nearing Finality

April 13, 2021 Nearly three years after California became the first state to pass a business loan and merchant cash advance disclosure law (SB 1235), the actual disclosure rules themselves are finally nearing completion. The public has until April 26th to submit any comments on the amended portions of the proposed rules.

Nearly three years after California became the first state to pass a business loan and merchant cash advance disclosure law (SB 1235), the actual disclosure rules themselves are finally nearing completion. The public has until April 26th to submit any comments on the amended portions of the proposed rules.

The 52-page document is the result of years of negotiations between various parties that all have a stake in its implementation. Among the finer details are the characteristics of the fonts permitted in the disclosures, what column a certain disclosure can be placed in, and the aspect ratio of the columns themselves.

But that’s the easy part. Here’s the hard part, according to a brief published in Manatt’s newsletter yesterday.

“The modified regulations continue to require use of the annual percentage rate (APR) metric, rather than annualized cost of capital (ACC), to disclose the total cost of financing as an annualized rate. This appears to be a final decision, which will make it difficult if not impossible for many commercial finance companies to comply given the significant challenges of calculating APR on products with substantial variance in the amounts and timing of payments or remittances.”

Manatt highlights other issues, including that all the necessary disclosures be provided “whenever a payment amount, rate, or price is quoted based on information provided by the proposed recipient of financing…”

This requirement, the firm says, is not even required under Federal Regulation Z for consumer loans.

“Many companies will not be able to comply with this requirement absent radical changes to their California application and underwriting procedures, as it is common today for companies to have preliminary discussions with applicants about potentially available financing terms before full underwriting has been completed.”

Manatt’s newsletter on the issue can be found here.

Any interested person may submit written comments regarding SB 1235’s modifications by written communication addressed as follows:

Commissioner of Financial Protection and Innovation

Attn: Sandra Sandoval, Regulations Coordinator

300 South Spring Street, 15th Floor

Los Angeles, CA 90013

Written comments may also be sent by electronic mail to regulations@dfpi.ca.gov with a copy to jesse.mattson@dfpi.ca.gov and charles.carriere@dfpi.ca.gov.

The last day to submit comments is April 26, 2021

NY Court Says MCA Agreement is a Factoring Agreement, Not a Loan

March 22, 2021 A New York Supreme Court judge that was presiding over a breach of contract claim (653596/2018) in a merchant cash advance agreement, said he was bound to follow the decision issued in Champion Auto Sales, the landmark appellate ruling in 2018.

A New York Supreme Court judge that was presiding over a breach of contract claim (653596/2018) in a merchant cash advance agreement, said he was bound to follow the decision issued in Champion Auto Sales, the landmark appellate ruling in 2018.

In Principis Capital LLC v Team Van Eyk, Inc. et al, Principis sued the defendants over a breach of contract. Defendants “did not deny the facts underlying the motion or the the amount due,” the judge said, “but asserted instead that the Agreement is not an agreement for the purchase of future receivables; but is instead, a criminally usurious loan, and is therefore void as a matter of public policy.”

This defense actually led to victory for the plaintiff.

The Appellate Division, First Department, in Champion Auto Sales, LLC v Pearl Beta Funding, LLC (159 AD3d 507, 507 [1st Dept], lv denied 31 NY3d 910 [2018]) has considered this issue, involving a merchant agreement substantially similar to the agreement in this matter, and has held that the type of agreement involved in this case is a factoring agreement rather than a usurious loan. This court is bound to follow Champion and, therefore finds that the Agreement is a factoring agreement and not, as defendants assert, a usurious loan. There are, therefore, no genuine triable issues of fact, and plaintiff is entitled to summary judgment on its complaint.

Case closed.

Steve Denis, SBFA on Why Maryland MCA Bill Failed

March 22, 2021 “In a lot of these places, a lot of the bills are well intended, believe it or not,” Steve Denis, executive director of the Small Business Finance Association, said. “Legislators just don’t understand enough about our industry to understand the nuances. We’ve worked really hard educating policymakers in Maryland, and frankly, they now understand our industry better.”

“In a lot of these places, a lot of the bills are well intended, believe it or not,” Steve Denis, executive director of the Small Business Finance Association, said. “Legislators just don’t understand enough about our industry to understand the nuances. We’ve worked really hard educating policymakers in Maryland, and frankly, they now understand our industry better.”

Denis was referring to the nearly unanimous canning of Maryland’s MCA “Prohibition” bill last week. The bill failed to get enough support to leave the committee, blocked by a 19 to 3 vote against bringing the law out to the House floor. Denis, a proponent of the MCA and alt financing industry for years, said it was due to legislators understanding the need for capital “out there during the pandemic” and how harmful an APR cap could be for both business owners and the broker industry.

The law was originally proposed last year before covid shutdowns, but that also failed to make it to the floor. It now appears to be an annual event.

“Our goal as an organization is to make sure that small businesses have access to all different types of financial products and that we believe that small businesses are in the best position to make good decisions for their businesses,” Denis said. “The bill in Maryland narrowly targeted MCA products, and as you know and a lot of folks in the industry know, that sometimes MCA is in the best interest of the business, there’s a lot of benefits to an MCA.”

Denis punctuated his statement with the mantra- we were not out of the woods yet. An APR disclosure bill was just introduced in the Connecticut State Senate last month, modeled off the New York APR bill set to go into effect this year. Denis was hopeful the legislators could learn from speaking to industry interests and change their course like in Maryland.

“We are engaged, I think we’re in a good spot. With any of these bills, Maryland, Connecticut, I caution you know we’re not out of the woods yet,” Denis said. “We still want to work really closely with policymakers. We’re for meaningful disclosure, we think there needs to be some guardrails on our industry, but I think that the most important thing we can do is continue to educate folks in states.”

Forward Financing Reaches $1 Billion in Funding to Underserved Small Business

March 1, 2021Boston-based Fintech Company Expands Main Street’s Access to Capital During Pandemic, Achieves Major Growth Milestone

Boston, Mass., March 1, 2021 – Forward Financing, a financial technology company that provides flexible revenue-based financing to small businesses, today announced that they have provided $1 billion in funding since their inception in 2012. The majority of this funding has gone to underserved small businesses nationwide; those that are unable to obtain financing through traditional sources like banks or the Small Business Administration.

“Nine years ago, we started this company upon the realization that so many small businesses lacked access to working capital,” said Forward Financing co-founder and CEO Justin Bakes. “As we look ahead to our next $1 billion milestone, we will continue to focus on providing best-in-class customer service and on helping our small business customers reach their full potential, no matter what challenges may arise.”

The COVID-19 pandemic has severely impacted the U.S. economy and many small businesses have needed additional financial resources to get by. Despite over $600 billion in loans provided through the Payroll Protection Program, this alone has been insufficient in fulfilling the need for capital. As a result, many small business owners have turned to funders like Forward Financing for support.

Forward Financing is uniquely suited to help small businesses during this economic downturn because it offers financing that is based on revenue, and is not a loan. Therefore, small business customers who may be experiencing a revenue slowdown can reduce their payments proportionately.

“Forward Financing has helped me grow my business and take advantage of opportunities,” a retail business owner recently said. “Their service has been excellent and when COVID hit, they easily and efficiently helped me adjust my payment schedule so I remained current and my business was not interrupted. I will use them again and again in the future!”

Over the past six months, Forward Financing has grown daily funding volume at an average rate of 17% per month as they continue to help small businesses navigate the pandemic economy. In order to help meet rapidly growing demand, they are currently expanding headcount in Boston by 20%.

About Forward Financing

Forward Financing is a Boston-based financial technology company that provides fast, flexible working capital to small businesses nationwide. Their dedicated account representatives and advanced proprietary technology help customers spend less time finding capital and more time growing their business. With a simple, secure online application, business owners can trust that Forward Financing works to get them approvals within minutes, funding within hours, and personalized support when they need it most.

Since 2012, Forward Financing has expanded Main Street’s access to capital by providing over $1 billion in funding to nearly 30,000 small businesses. The company is rated A+ by the Better Business Bureau and ‘Excellent / 4.9 stars’ on Trustpilot.com. Forward Financing was named a Best Place To Work by both

the Boston Business Journal and Built In Boston, and has been named by both Inc. Magazine and the Boston Business Journal as one of Massachusetts’ fastest-growing companies each year since 2017. Forward Financing is committed to helping more small business owners succeed and achieve their full potential. To learn more, visit www.forwardfinancing.com.

Media Contact

Lauren Groccia

lmelaugh@forwardfinancing.com

508-314-3574

###

LoanMe, Liberty Tax Merger to Take on Intuit, Enova

February 22, 2021NextPoint Financial will combine LoanMe’s business, consumer, and mortgage lending with Liberty Tax’s tax preparation business, according to merger announced on Monday. Liberty’s “2,700+ locations in the US and Canada” will become consumer and SMB loan shops.

The new firm will also offer Merchant Cash Advances; LoanMe launched MCA funding in January and expects to fund $15 million in MCAs in 2021. Based on the acquisition prospectus, NextPoint will be a tax readiness firm, with the added suite of financial products as a value and growth builder.

Ramping up consumer, installment, and MCA lending, paired with the third-largest tax-prep business in the U.S, NextPoint expects to compete directly with Intuit, H&R Block, Enova, and Elevate.

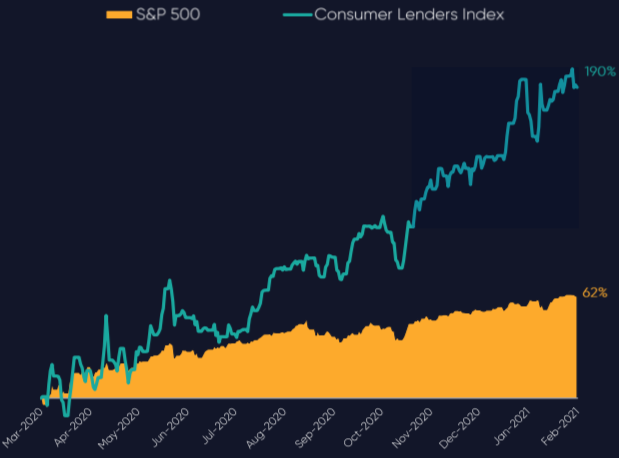

Fintech firms are setting themselves apart from the competition as one-stop shops for everything a business needs, including MCA products. Why branch into financial services now? NextPoint found that this year alt lenders have outperformed the S&P500 three times over.

“We are a one-stop financial services destination empowering hardworking and credit-challenged consumers and small businesses,” the investor presentation reads. “To get to the next point in their financial futures.”

Intuit offers a variety of financial products, like business loans through Quickbooks Capital, alongside their popular, 60%+ market share of tax prep software. H&R began offering small $1,000 lines of credit this year, but not much more.

The team leading the new company, NextPoint Financial, will feature execs like Brent Turner as CEO, Mike Piper CFO, both keeping their previous Liberty Tax positions. Jonathan Williams, former president and founding shareholder of LoanMe, will become president of lending.