Blazing Trails in Unexplored Financial Markets

April 4, 2017 Once upon a time people with health insurance who were treated for medical emergencies, illnesses or chronic health conditions –an illness or accident requiring hospitalization, an appendectomy, or a hip replacement, say – could rest easy. Insurance underwriters like United Health, Wellpoint or Humana would surely handle most, if not all, of a patient’s medical expenses.

Once upon a time people with health insurance who were treated for medical emergencies, illnesses or chronic health conditions –an illness or accident requiring hospitalization, an appendectomy, or a hip replacement, say – could rest easy. Insurance underwriters like United Health, Wellpoint or Humana would surely handle most, if not all, of a patient’s medical expenses.

Today? Not so much. As healthcare becomes ever more pricey, employers are increasingly offering health insurance plans that are less generous and require consumers to pay higher deductibles. Individuals as well are finding that the same goes for them: The only way to afford health insurance is to purchase a plan with a high deductible.

“We’re at a tipping point where the cost of healthcare is outpacing GDP,” says Adam Tibbs, chief executive and co-founder of Parasail Health, a start-up alternative lender in the San Francisco Bay area. “As a result,” he adds, “the only way health insurance can work is either to raise (the cost of) premiums or opt for higher deductibles.”

Statistics confirm Tibbs’s assertion. As of last autumn, according to a September, 2016, survey by Kaiser Family Foundation, the average deductible for workers’ health insurance policies jumped to $1,478, up by more than 12% from $1,318 in 2015. The survey found, moreover, that – for the first time — slightly more than half of all covered workers have deductibles of at least $1,000. At smaller companies, the average deductible is now more than $2,000.

Parasail, a Sausalito-based alternative lender which opened its doors last September, is angling to fill that void. Funded with seed capital raised from four venture capital firms — Healthy Ventures, Montage Ventures, Peter Thiel, and Tiller Partners, reports online data-publisher Crunchbase – Parasail acts as a go-between, connecting the medical practitioners to third-party lenders.

In partnering with doctors, hospitals, and medical clinics, Parasail employs a business model that resembles an auto dealership. After the customers picks out a four-door sedan or a sport utility vehicle, he or she drives it home thanks to a five-year, monthly-payment plan from, say, Capital One.

Similarly, after agreeing to a costly medical procedure, the patient can strike an arrangement with a medical provider’s billing department for on-the-spot financing. Once the deductible is covered, the patient is cleared to glide into the operating room.

Despite being open for less than a year, Tibbs says, Parasail has enlisted as partners some 2,500 medical practitioners with unpaid patient debt of roughly $4 billion. The typical loan averages $6,000. “Our goal,” remarks Parasails marketing vice-president, Dave Matli, “is to create a normal retail experience” so that financing medical debts is as seamless as swiping a credit card.

Meanwhile, industry experts say that Parasail represents a new breed in the financial technology sector. As online alternative lending and the broader fintech industry grow more established, institutional investors and financiers are increasingly wagering bets on companies that promise more than disruptive technologies or cheaper loans.

Increasingly, they are hunting for companies like Parasail that are introducing new products or blazing trails in unexplored markets. “The area that I find most interesting,” says Phin Upham, a venture capitalist and board member at Parasail, is investing in companies that “are developing products that didn’t exist before, serving people who haven’t been served, and playing a unique role incentivizing long-term behaviors.” (Upham, who is a principal at Peter Thiel’s VC firm, emphasizes that he is speaking only for himself.)

Parasail’s fundraising and launch has taken place against a dramatic drop in both global and U.S. fintech financing, according to KPMG’s annual report on the industry, “The Pulse of Fintech.” The accounting firm reports that total funding for fintech companies and deal activity plummeted by more than 50% in the U.S. in 2016 to $12.8 billion from $27 billion the prior year. KPMG attributed much of the drop to “political and regulatory uncertainty, a decline in megadeals, and investor caution.”

Parasail’s fundraising and launch has taken place against a dramatic drop in both global and U.S. fintech financing, according to KPMG’s annual report on the industry, “The Pulse of Fintech.” The accounting firm reports that total funding for fintech companies and deal activity plummeted by more than 50% in the U.S. in 2016 to $12.8 billion from $27 billion the prior year. KPMG attributed much of the drop to “political and regulatory uncertainty, a decline in megadeals, and investor caution.”

The year “2016 brought reality back to the market” after the banner, record-shattering year of 2015, the report noted.

Venture capital financing in the U.S., however, did not slip as dramatically as overall funding, sliding some 30% to $4.6 billion from $6 billion in 2015. (Almost overlooked in the report was that corporate investment capital was “the most active in the past seven years,” KPMG’s report notes, representing 18 percent of venture fintech financing.)

Steve Krawciw, a New York-based fintech startup executive asserts that “the business has matured and, yes, there have been defaults, but the business model for fintech has stabilized.” The author of “Real-Time Risk: What Investors Should Know About FinTech, High-Frequency Trading, and Flash Crashes,” Krawciw expects more funding to stream into the industry as new players such as banks, insurance companies, hedge funds and private equity get involved. They’ll “go in a number of different directions,” he reckons, “especially direct lending by hedge funds and private equity firms.”

No figures have yet been released by KPMG for the first quarter of 2017, just ended in March, but fintech industry participants are mightily impressed at news of the $500 million financing for Social Finance Inc. (SoFi). Best known for its refinancing of student loans, the San Francisco firm reported on February 24 that it raised a half-billion dollars in a financing round led by private equity firm Silver Lake Partners. Other investors include SoftBank Group and GPI Capital, bringing SoFi’s total investment to $1.9 billion, the company said in a press release.

SoFi, which plans to use the funds to expand online lending into international markets and devise new financial products, is ambitiously transforming itself into an online financial emporium. Along with a suite of online wares that mimic traditional banking and financial products – savings accounts, life insurance policies and mutual funds – SoFi has also invented new online offerings.

SoFi, which plans to use the funds to expand online lending into international markets and devise new financial products, is ambitiously transforming itself into an online financial emporium. Along with a suite of online wares that mimic traditional banking and financial products – savings accounts, life insurance policies and mutual funds – SoFi has also invented new online offerings.

For example, SoFi formed a partnership with secondary mortgage lender Fannie Mae and, together, the companies are enabling borrowers to refinance both mortgage and student debt. The SoFi financing, says Krawciw, “is not a seminal deal, it’s a sign of what’s coming.”

SoFi may also be providing a road map for fintech companies like Parasail. After building a customer base with health-care loans at 5.88% annual percent rate — compared with credit cards charging interest rates about four times as much – Parasail could be poised to sell additional products to its built-in audience.

Just as SoFi got big on refinancing student loans, Parasail could use healthcare lending as a springboard for future financial endeavors. Its revenues have been growing by 50% month-over-month.

By the first quarter of next year, Tibbs says, the firm will be breaking even.” And at that point, he adds, it expects to roll out a menu of new products too.

In This Online Lender’s Earnings Report, Profits, MCAs and Term Loans

March 22, 2017Limited details were offered when Enova, a publicly traded company, acquired The Business Backer (TBB) in June 2015. For one, the Cincinnati Business Courier had the exclusive, which one might not describe as the typical go-to source for online finance news. But TBB was not typical. Based in Blue Ash, Ohio as opposed to New York City or San Francisco, the company had originally focused on offering merchant cash advances before eventually expanding their suite of solutions to include other products.

According to Enova’s earnings report, TBB had been purchased for $26.4 million with an estimated contingent $5.7 million of that being based on future earn-out opportunities. There was a caveat though. If future operating results exceeded expectations, that contingent amount could increase over time, but not beyond where the total consideration paid for the company exceeded $71 million. As of 2016’s year-end, that contingent amount had increased by $3.3 million.

Enova’s report makes several mentions of their merchant cash advance business or as they call them, receivable purchase agreements (RPAs). For the most part, they obscure the financial metrics of this aspect by lumping it in with installment loans. These installment loans are described as “multi-payment unsecured consumer installment loan products in 17 states in the United States and in the United Kingdom and Brazil” with repayment periods of two to sixty months, so yeah, they’re pretty different.

Their RPA customers, however, “average approximately $1.5 million in annual sales and 10 years of operating history while those who obtain an open line of credit account average approximately $450 thousand in annual sales and 7 years of operating history,” the report says. These lines of credit are primarily offered through a business lending subsidiary called Headway Capital.

While companies like Lending Club and OnDeck grab all the headlines, Enova describes itself as a “leading technology and analytics company focused on providing online financial services.” And in 2016, they extended nearly $2.1 billion in credit to borrowers and had a net income of $34.6 million.

On the company’s Q4 earnings call in February, Company CEO David Fisher said, “There currently seems to be a bit of a shakeout occurring in the non-bank small business lending and financing industry. A number of our competitors have either ceased funding or completely shut down over the past several months. From the intelligence we were able to gather, this is largely due to credit issues and their portfolios. As we mentioned last quarter, we have taken a more methodical approach than some to growth for our small business products. And we’re now seeing the benefits of that approach. Recent advantages of our small business book are performing well and the unit economics continue to improve especially as acquisition costs have dropped following the shakeout I just mentioned.”

Enova’s small business financing portfolio only constituted 12% of their loan portfolio at the end of last year. And at $13.70 a share, the company’s current market cap is larger than OnDeck’s.

Patch of Land Hires Chief Investment Product Officer, Matthew Zall, Recognized Capital Markets Expert and Innovator of Lending Products for the Single-Family Home Rental Market

March 5, 2017LOS ANGELES- March 6, 2017 – Patch of Land, a leading online real estate marketplace lender and crowdfunding platform, announces the addition of Matthew Zall as Chief Investment Product Officer as the firm prepares to expand into the single-family rental market with longer term, permanent financing products. The number of non-owner occupied single-family properties in the U.S. including townhomes, condos, and 2-4 unit properties grew to almost 24 million units valued at over $6 trillion in 2016, according to ATTOM Data Solutions.

Zall brings to Patch of Land more than 12 years of real estate and mortgage experience, as well as expertise in financing and product development. He pioneered three of the industry’s first-ever multi-borrower single-family rental securitizations, helping to build Blackstone Group subsidiary, B2R Finance, (now known as Finance of America Holdings, LLC) from start up to a multibillion dollar lender in only a few years. Prior to joining B2R, Matt was a Commercial Real Estate (CRE) trader at J.P. Morgan and Bear Stearns. At Patch of Land, Zall will execute strategies to enable the expansion of the firm’s position as a marketplace lender by offering both accredited and institutional investors additional opportunities to invest in this asset class.

“Patch of Land’s marketplace is designed to meet the lending needs of real estate investors. The addition of Matt enables us to continue the expansion of our marketplace to fully serve the lending needs of more than 10 million Americans who directly invest in single-family residential properties and need consistent, reliable access to capital to fuel their businesses,” said Paul Deitch, Patch of Land’s Chief Executive Officer. “We are excited about adding Matt to our executive team as he is passionate about our mission to leverage technology to improve the borrowing experience for the real estate entrepreneur and at the same time offer investors from both Main Street and Wall Street the opportunity to participate in this attractive asset class.”

About Patch of Land

Since issuing its first real estate loan in October 2013, Patch of Land has been recognized in the financial technology space as a leader in online real estate lending. The company employs its proprietary technology to efficiently fill a void in the real estate finance industry by providing borrowers access to capital for residential and commercial real estate projects. The platform also establishes a marketplace through which qualified individual and institutional investors can participate in private real estate projects with low minimum investments, predictable returns and first-lien secured loans.

More information is available at www.PatchofLand.com or by calling 888-959-1465.

Media Contact: Glen Orr

glenlorr@gmail.com

469.441.3203

I Got Funded, OMG I’m a Merchant!

March 3, 2017 I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced AltFinanceDaily’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, AltFinanceDaily is truly a small business first.

I’ve read the press releases, interviewed the executives, and written the summaries about the latest and greatest innovations in alternative finance. I’m the guy that’s supposed to know how everything in this industry works, but do I REALLY REALLY know? In the last decade, I’ve worn an underwriter hat, an MCA broker hat, a syndicator hat, a lead generator hat and a reporter hat just to name a few. This diverse array of experiences has surely influenced AltFinanceDaily’s success. But even as we publish content about the funders, lenders and other Fintech players in the wider industry, AltFinanceDaily is truly a small business first.

Independently owned, there are no investors in the company to turn to for assistance. And that’s not such a bad thing if you know at all what it can be like to have partners. At the end of last year, we did what hundreds of thousands of small businesses around the country have done, we got funded by a marketplace lender. Through that experience, I found myself wearing a brand new hat, one that says “merchant” on it.

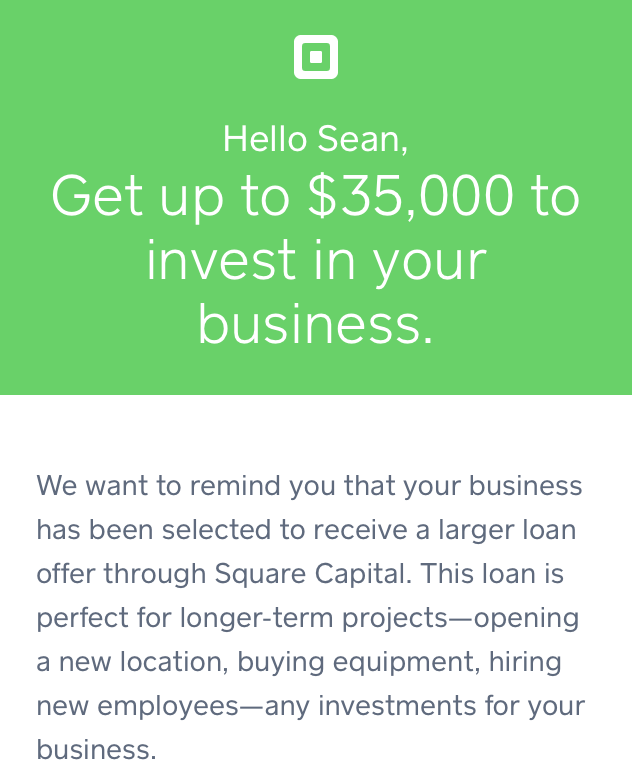

On December 1st, my company received a deposit for $35,000. It was a loan from Square Capital and I didn’t pursue it for a story, but rather to facilitate cash flow at the busiest time of the year. I was moving into a larger office on the same floor of our building and the hustle and bustle of the pre-holiday craze was upon us. The circumstances may come off a bit cliché, simulated even, but there it was at the right time and the right place, an email telling me that my business had been “selected.” If you’ve ever wondered if that kind of marketing works, it must, because a half hour after reading through the materials, I made an educated decision and applied for a loan.

The higher-ups at Square Capital, those above the underwriting department, might have no idea that they even funded us (our legal name is different from our trademark publication name). And I haven’t reached out to them for comment because I didn’t want to turn this into a PR stunt or get them riled up about my account. But if you work at Square and you’re reading this now, you don’t need to hold your breath. Everything seemed to work just as the press releases, ads, and executives claim it does. Phew! That’s good for you, but it was also very good for me.

The most pleasant surprise was that our business got approved for the maximum amount advertised in their email. Here’s how it went down:

11/29/16

1:34 PM

Received email offering a business loan up to $35,000 to repay over 12 months

2:01 PM

Applied for $35,000, which consisted of logging into my Square account and tapping a button

8:02 PM

Got approved for $35,000

11/30/16

Square sent out the funds via ACH

12/1/16

Received full loan deposit in my business bank account

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

All in all, it couldn’t have been any simpler. The deposit was for the full $35,000. And try as you might to hate me for saying this, I never calculated what the APR is. Square explained the cost as a fixed fee, which for me was $3,160. That’s approximately 9% of the principal of which the whole loan and fee would be repaid in equal installments over the next 12 months. To those that work in the industry, I got a 12-month 1.09 deal.

As a small business owner, I calculated whether or not it made sense to pay a set fee for $35,000 over that time period and determined it did. An APR would not have impacted my decision, nor would I really have found it helpful in determining the supposed true cost. The true cost is already there in black and white, the total dollars I agreed to pay.

Two things guided me, speed and economics. I wasn’t motivated to shop around to try and get the absolute best deal, just one that made economic sense with the least amount of work in the shortest amount of time. It sounds ironic to write that, especially as someone who has a bachelor’s in both Accounting and Finance but if you’re someone who works 7 days a week like I do, well maybe you’d understand my thought process. If I was applying for a million bucks, then yes, I’d shop and think on it pretty hard, but in my circumstances, a few thousand dollars in fees is relatively small stakes for the company. Besides, I was using the money proactively, as a positive tool.

I knew my patience for waiting was thin. For example, an experience with one of my banks earlier in the year had already left me rattled. I had asked to extend the limit of a business credit card and I was told that in order to do so, I’d have to visit the bank branch where I had originally signed up for the card (I don’t even live near that branch anymore) and that I would have to bring financial statements with me to present for review. By the way, this was for a limit increase to an amount that was much less than $35,000.

I learned that day that the rumors about (some) banks are true. They wanted me to visit a branch… and bring paperwork… for some kind of unspecified analysis… in 2016. Lo and behold I never showed up, and was more entrenched in my belief than ever before that the world needed to become de-banked and soon.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

My business already processes cards through Square so I’ve got a track record with them. Applying didn’t place any inquiries on my personal credit report nor did anyone at Square ever call me to ask me any questions. I know that most of their competitors conduct what is commonly known as a “merchant interview” prior to full approval or funding, but they didn’t. It wouldn’t have bothered me if they did though since we have a good business and would be using the money for the right reasons.

Alas, the entire process really all just came down to clicking a button online. I kept waiting for the catch, for them to let me down, to come up short of all the promises that the Fintech revolution has made about changing the world, but it never happened. A month later, Square withdrew their first payment from our account. Like I said earlier, I was satisfied with the entire process and it was a big help. Had I been given the option however, I might’ve opted to structure the arrangement differently and sold a portion of our future sales proceeds rather than simply borrow money. Allow me to explain.

It’s entirely possible that the next 12 months of business won’t pan out the way I project. If my sales drop, I still have to make the fixed monthly payment in accordance with my loan terms regardless. Not so when selling future sales since the delivery of those funds to the buyer is entirely tied to actual sales activity. A structure like this, what many consider a merchant cash advance, is actually what Square used to offer up until early 2016.

When the pace of sales slow down, delivery of the sales proceeds slows with it. When the pace of sales increases, so too does the delivery to the buyer. And if I went out of business, well then the buyer would get what they purchased, nothing.

Merchant cash advances are harder to bundle up and securitize though because there are no maturity dates nor is there even a guarantee the buyer will get what they purchased in full. They’re investments with loads of uncertainty built in for the buyer, and that’s probably why Square switched to loans and also probably why the cost of my loan was relatively inexpensive. They’ve minimized the uncertainties.

Nonetheless, the loan I ultimately got, is just fine. In the moment that I needed it, the process couldn’t have been any simpler or any faster. The banks have met their match. I got funded and loved it, now it’s your turn.

In The UK, Regulators Advise Where The Line Between Banks and Non-banks Lies

March 1, 2017Online lenders shouldn’t be borrowing money from other online lenders and using that money to lend, the Financial Conduct Authority in the UK warned on Tuesday. Doing so without regulatory permission, they explained, would constitute accepting deposits and be a criminal offense.

A copy of the official letter signed by Jonathan Davidson, Director of Supervision – Retail and Authorisations, is publicly available.

According to the Financial Times, the warning was prompted after RateSetter asked the government in October 2016 if such activity was acceptable. They had been engaged in such wholesale lending, as it’s called, since 2016 but have since stopped.

Prosper Marketplace Closes Loan Purchase Agreement for up to $5 Billion of Loans with Consortium of Institutional Investors

February 27, 2017SAN FRANCISCO–(BUSINESS WIRE)–Prosper Marketplace, a leading online consumer lending marketplace, today announced that it has closed a deal with a consortium of institutional investors to purchase up to $5 billion worth of loans through the Prosper platform over the next 24 months. The investors in the consortium are affiliates of each of New Residential Investment Corp., Jefferies Group LLC and Third Point LLC, and an entity of which Soros Fund Management LLC serves as principal investment manager. The consortium will also earn an equity stake in the company based on the amount of loans purchased, further aligning the group with Prosper’s future growth and success. Warehouse financing of up to $1 billion will be provided by a syndicate of lenders including Credit Suisse, Deutsche Bank, Goldman Sachs and Morgan Stanley.

“We’re very pleased to be working with this consortium of investors, and believe they will be great long-term partners as we continue to build a large-scale business,” said David Kimball, CEO, Prosper Marketplace. “This deal gives us the funding stability and additional capital markets expertise we need to continue to grow our marketplace and achieve profitability in 2017.”

Prosper has maintained positive momentum since the second half of 2016, with monthly loan originations growing steadily since July. In addition, the Prosper loan portfolio is delivering solid returns to its institutional and individual investors, with an estimated net return of 7.86%<> for January 2017. Prosper continues to diversify its investor base, and is focused on bringing new banks and other institutional investors onto the platform.

Financial Technology Partners (FT Partners) served as strategic advisor to Prosper Marketplace and its Board of Directors on this transaction. DV01 will be the loan data agent to the consortium.

About Prosper Marketplace

Prosper’s mission is to advance financial well-being. The company’s online lending platform connects people who want to borrow money with individuals and institutions that want to invest in consumer credit. Borrowers get access to affordable fixed-rate, fixed-term personal loans, and investors have the opportunity to earn attractive returns via a data-driven underwriting model. To date, over $8 billion in personal loans have been originated through the Prosper platform for debt consolidation and large purchases such as home improvement projects, medical expenses and special occasions.

Prosper launched in 2006 and is headquartered in San Francisco. The lending platform is owned by Prosper Funding LLC, a subsidiary of Prosper Marketplace. Loans originated through the Prosper marketplace are made by WebBank, member FDIC. Visit www.prosper.com and follow @Prosperloans to learn more. Prosper notes offered by Prospectus.

1 Estimated return on January 2017 production is 7.86% according to the Prosper Performance Update: January 2017

Contacts

Prosper Marketplace:

Sarah Cain, 415-593-5474

scain@prosper.com

The Road To Training The Best Sales Reps

February 26, 2017

Alternative-finance industry executives tend to agree on at least two basic rules for building a successful sales team: Hire people who know how to sell and never stop training them. Following the second rule requires knowledge and perseverance. The first one takes a leap of faith.

To obey Rule No. 1, companies have to find ways of determining who possesses that elusive quality known as salesmanship, even among inexperienced job candidates. To that end, most firms make an educated guess based on experience, intuition, common sense, high hopes and the good graces of Lady Luck.

“We look at personality traits,” says Zach Ramirez, a World Business Lenders vice president and manager of the company’s Costa Mesa, Calif., branch. “We’re looking for an outstanding person – the highest-caliber person we can find. They should be hard-working and competitive. You can underline ‘competitive.’ They should have a fire inside them.”

“We want someone who’s hungry for money and is going to be a go-getter, says Chad Otar, CEO and executive funding manager at Excel Capital Management Inc. “It’s a feeling that you get when you talk to them. You can tell when a person is going to sit back and not do anything.” In addition, good candidates aren’t intimidated by the challenge of learning how the industry works, he notes.

“It’s really about how you connect with someone,” according to Amanda Kingsley, who owns Options Capital and also works as a sales training consultant. “Even over the phone, you need to treat people with understanding. You need to inspire the trust that you could provide the advisory help they need.” Small details, like remembering a potential client’s daughter just got married, mean a lot, she says.

“It’s really about how you connect with someone,” according to Amanda Kingsley, who owns Options Capital and also works as a sales training consultant. “Even over the phone, you need to treat people with understanding. You need to inspire the trust that you could provide the advisory help they need.” Small details, like remembering a potential client’s daughter just got married, mean a lot, she says.

“It comes down to drive and personality,” says John Celifarco, sales manager at Sure Funding Solutions. He finds there’s not much room for the thin-skinned and it takes a certain kind of person to succeed. “When you find the right people, it usually clicks pretty quick,” he says. “For the people who don’t work out, it usually falls apart pretty quick.”

“I look for strong personalities,” says Isaac Stern, CEO of Yellowstone Capital. “I don’t believe you can necessarily teach someone to sell,” he asserts. “This isn’t an easy sell, so you have to have a Type A personality. They’re on the phone and they’re confident whether they know the product or not in the beginning.” The interview process can “weed out” candidates who aren’t going to find success, he says.

Don’t expect someone with a background in outside sales to find happiness spending eight hours a day on the phone as an inside salesperson, warns Stephen Halasnik, managing partner at Financing Solutions. As a direct financing company, his firm hires salespeople different from those an ISO or broker employs, he says. His company expects salespeople to act as consultants who are knowledgeable about finance and empathetic to small-business owners.

Nearly every company prefers candidates with selling experience, possibly in telemarketing. Some seek reps with a background in selling financial services, but others prefer prospective employees who are new to the industry. “I don’t want to hire someone else’s problem child,” Stern asserts. “I’d like them to learn the way we do things from start

to finish.”

“Different offices have different cultures, so someone who has worked well in one office might not work well in another,” Celifarco says. People hired from other companies may bring bad habits, he says. They may approach the job in a variety of ways they’ve learned elsewhere and thus prevent the company from presenting a consistent face to the public, he says. “Every company has an identity,” he contends.

“Different offices have different cultures, so someone who has worked well in one office might not work well in another,” Celifarco says. People hired from other companies may bring bad habits, he says. They may approach the job in a variety of ways they’ve learned elsewhere and thus prevent the company from presenting a consistent face to the public, he says. “Every company has an identity,” he contends.

Applicants without a sales background sometimes rise to the occasion and succeed, says Ramirez. In fact, one of his top sales managers joined the company with no sales experience. Former entrepreneurs, even those without a sales background, often have a lot in common with other small-business owners and that helps them do well, he notes.

Excel Capital Management seeks salespeople with differing backgrounds for two different types of roles in its sales force, says Otar. Openers work on salary and should have phone sales experience so they’re comfortable on the telephone. Closers, who work for commissions, should have experience at selling financial services products or something closely

related, such as stocks or mortgages, he says.

While good hiring practices bring good employees into the company, they also guard against inviting bad ones into the fold. World Business Lenders uses several third-party companies to perform background checks and pre-employment screening, but most often calls upon ADP, says Alex Gemici, the company’s chief revenue officer. ADP performs evaluations that comply with the laws of the states where the employees are located, he says.

Eliminating unsavory candidates carries special significance in the alternative-finance business, notes Ramirez. “It’s critically important that they have no background issues,” he says. “In this industry there a lot of bad apples out there. It’s important that they don’t infiltrate our organization.”

“It’s very difficult to find loyal guys,” Otar laments. “They come in and utilize all your systems and then you catch them stealing.” In other words, they pass deals along to other companies. Otar has caught three of his closers doing exactly that. “You’ve got to be very careful,” he warns, adding that it’s difficult to spot bad actors because they’re skilled at selling themselves.

Once a company chooses the best candidates, the training can begin. New salespeople always start on Mondays at World Business Lenders, and the company’s corporate headquarters conducts sales training nationwide that day, says Gemici. The full day of instruction originates at headquarters, and new hires at branch locations participate on Skype. Subjects include the industry in general, specific company products and sales tips.

On Tuesdays, the World Business Lenders branches take over the training for a day or more, Gemici notes. That instruction, which lasts as long as the branches decide, can include having the new employees “shadow” more-experienced workers and having crack salespeople listen in on the phone calls of the new staffers as they make their pitches.

In the World Business Lenders office in California, Ramirez continues the training every day of a new employee’s first two weeks on the job. Tuesday and Wednesday of the first week, he spends the full eight-hour day with them. After that, he sets aside at least two or three hours of instruction each day. “I want to err on the side of over-training,” he explains.

From there, education continues as long as employees work for the company, Ramirez says. That can include spot training that he institutes anytime he sees a problem or an opportunity for improvement. Ongoing training also helps salespeople keep up with changes that occur in the industry, he notes.

The sales staff in the California office of World Business Lenders also assembles in a conference room for regular sales meetings. Ramirez picks a rep who’s outstanding at some aspect of the job to deliver a short lecture on the subject at those meetings. A star at prospecting, for example, could explain tricks of that part of the trade and then field questions on the subject. “That way, everybody can learn what everybody else knows,” he says.

For ongoing training at Financing Solutions, Halasnik calls his staff into a “huddle” for 10 minutes every day. They review what deals are pending so that salespeople know what management is seeking and can use that knowledge when they’re gathering data from customers. “We’re looking for reasons to give someone financing that doesn’t fit the cookie cutter approach a bank would use,” he notes. The team also use the huddle to share information about the industry.

At Sure Funding Solutions the sales staff meets every couple of weeks for ongoing training. They talk about some aspect of the sales process, such as opening, closing, dealing with banks, what’s working and what’s not working, says Celifarco. “I’ve been in this business since ’08, and I’m still learning new things,” he notes, adding that changing one phrase in a pitch could get better results.

Ongoing training at Excel hinges on monitoring phone calls to ensure openers are asking the appropriate questions to qualify leads and that closers are working effectively, Otar emphasizes. “It’s a never-ending process to learn what to say at the right time,” he says of his company’s training policies. Salespeople who have mastered the basics can bring their own personalities into their presentations to avoid sounding as though they’re reading from a script and thus foster an organic conversation, he notes. “That’s perfect – it’s golden,” he exclaims.

Kingsley agrees. “Don’t be too ‘salesy,’” she counsels. “That’s the best sales advice I can give.” Nobody enjoys receiving a telemarketing call, she reminds her trainees. Larger companies probably won’t heed that tip because they’re focused on volume, but smaller companies can avoid the “salesy” trap, she says.

Training should also teach originators to avoid industry jargon on their calls because prospects simply may not know the lingo, Kingsley cautions. Closers should learn from their training that knowledge of the customer’s industry can help build a relationship, she says. And knowing the customer’s industry also helps salespeople convey a deeper understanding of creditworthiness to underwriters, she maintains.

Financing Solutions trains salespeople to reveal information to clients through a string of questions instead of merely throwing out statements about the company’s products, Halasnik says. The questions can include how the customer’s business works and how he’ll use the money. That can allow the client to sell himself, and it can help the salesperson explain the client’s situation to the underwriters, he says.

Salespeople should learn to present themselves as professionals and avoid sounding like used car dealers, Halasnik maintains. “They have to understand business,” he notes, adding that training must convey that sensibility because “they don’t really come in that way.” In fact, he maintains that financing Solutions has to persevere in continuing to help the sales staff understand how small-business owners think.

Even though training never ends, it eventually pays off, Halasnik contends. He looks forward to the time – possibly in six months or so – when the roles reverse because his salespeople are picking up so much information that they’re training him. The fact that sales reps are making contact with customers keeps them in touch with the pulse of the industry, he notes.

But problems can arise even with the most persistent training efforts, so it’s also vital to begin the process with employees who are trainable, Kingsley suggests. “Some people listen to you, but then they don’t act on the advice,” she maintains. Others don’t want to expend the effort necessary to research their customers’ industries. “If you’re going to make $10,000 off of a sale, put in the work for it,” she admonishes.

Some companies are hiring lots of salespeople and putting them to work quickly as part an effort to achieve sheer volume, Kingsley says. Instead, she recommends training a smaller number of reps to conduct themselves in a transparent manner that promotes repeat business.

World Business Lenders allows for a 90-day period to determine whether a new salesperson and the company are a good fit, says Gemici. Turnover occurs during that period, often because the company is growing so quickly that it’s necessary to take on a few inexperienced employees, he says. For salespeople who complete the 90 days, the success rate is high, he notes.

World Business Lenders allows for a 90-day period to determine whether a new salesperson and the company are a good fit, says Gemici. Turnover occurs during that period, often because the company is growing so quickly that it’s necessary to take on a few inexperienced employees, he says. For salespeople who complete the 90 days, the success rate is high, he notes.

“We like to say six weeks,” Otar says of his company’s probationary period. By then, a closer should be making four to seven deals a week, he suggests, noting that openers should generate 15 to 25 leads weekly and five to seven should be getting funded.

Salespeople can require four months to really catch onto their jobs, according to Halasnik. He finds that he can gauge their progress by the quality of the questions they ask, not by what they say. As they learn the business, their questions improve, he notes.

The effort required to find and train salespeople can tempt some companies to steal good employees from their competitors, but the problem’s no more severe in the alternative-finance industry than in other businesses, according to Ramirez. “I never intentionally poach someone else’s employees, although people have tried to recruit mine,” he says. “Most of these people are clients. These competitors of ours send deals to us so I don’t want to do anything to jeopardize that relationship nor do I think that’s a good business tactic.”

So where are those prospective employees hiding? World Business Lenders employs a full-time in-house recruiter to ferret them out. Excel finds candidates on industry blogs or through general employment websites. Kingsley urges companies to contact colleges to seek out finance majors. Stern says he puts up a post and receives “tons of resumes.”

Wherever the employees come from, one of the keys to their success lies in understanding the customer’s business, Halasnik maintains. “If you only think of your business as money, it could be a little bit boring,” he says. “If you think about who the clients are and how they got there and who their customers are, that’s the fun part of the job.”

Lending Club Reveals Q4 Figures, $146 Million Loss for the Year

February 15, 2017

The year that shook the industry ended six weeks ago but the total damage wrought is just now coming out. Lending Club lost $146 million in 2016, $32 million of which can be attributed to Q4. But it didn’t end all that badly according to CEO Scott Sanborn.

On the earnings call he said, “our attention was focused on rebalancing our funding mix, a key step to bolster our resiliency and enable a return to growth. We set a target to help our bank partners close out their rigorous diligence, so that they could return to scale. I’m pleased to say that our efforts have paid off as not only are all of our key bank investors back buying on the platform, but we’ve also welcomed multiple new bank partners over the last few months.”

And so they’re feeling quite optimistic. “It’s an exciting time for Lending Club and I look forward to beginning the next phase of our growth,” Sanborn concluded before turning the call over to new CFO Tom Casey.

Casey went on to predict that the company would lose another $69 million to $84 million in 2017, with nearly half of that expected to be generated in the first quarter of this year.

In brighter news, the company celebrated the 10th year anniversary of their first loan and surpassed more than $25 billion in loans since inception. With close to 2 million customers-to-date, that would mean that nearly 1% of the adult population in the US has had a Lending Club loan.

Less than 10% of their loan volume is comprised of education and patient finance loans, small business loans, and small business lines of credit, according to their report.