Tips For More Successful Marketing

April 30, 2018 In marketing, there’s a basic tenet that it takes seven “touches” within 18 months to prod someone into action.

In marketing, there’s a basic tenet that it takes seven “touches” within 18 months to prod someone into action.

Nowadays, with customers exposed to thousands of ads a day and across so many channels, it takes several times that in interactions to generate viable sales leads, according to Samantha Berg, a marketing and strategic partnerships executive with 6th Avenue Capital in New York.

That’s why it’s so important for funders, ISOs, brokers and other alternative funding professionals to have a solid marketing and lead-generation strategy that incorporates multiple channels such as search engine optimization, digital ads, direct mail, email and social media. The challenge, of course, is to find the right balance between being invasive and being top of mind, industry professionals say. Here are a few ways tried and true ways to generate warm leads and potential new business:

DON’T DIS DIRECT MAIL

Many marketers have a negative view about the importance of direct mail to consumers. But consumers may be more interested in this medium than you think. Consider a survey of more than a thousand consumers by Yes Lifecycle Marketing, a provider of email and digital marketing services. According to this study, 56 percent of all consumers say they find direct mail influential when researching a purchase. By contrast, a separate survey by Yes Lifecycle Marketing paints a very different picture of how marketers view direct mail; 78 percent of those polled say they believe direct mail is not influential for any age group.

One good thing about direct mail is that it can be opened at the merchant’s convenience, unlike a phone call which some merchants find annoying, especially since they often get multiple calls a day from numerous funders. With direct mail, even if a business does not need funding immediately, there’s a decent chance the merchant will keep your information on file for future reference, says Glen Faulhaber, vice president of sales at G-Plex Direct Mail Services in Holtsville, N.Y. Sending a follow-up mailing within a week of the first helps you gain additional brand recognition, he says.

One good thing about direct mail is that it can be opened at the merchant’s convenience, unlike a phone call which some merchants find annoying, especially since they often get multiple calls a day from numerous funders. With direct mail, even if a business does not need funding immediately, there’s a decent chance the merchant will keep your information on file for future reference, says Glen Faulhaber, vice president of sales at G-Plex Direct Mail Services in Holtsville, N.Y. Sending a follow-up mailing within a week of the first helps you gain additional brand recognition, he says.

Of course, for direct mail to be successful, certain parameters should be followed. For starters, mailings have to be based off good data; meaning the people or businesses you are sending to have a high likelihood of needing funds. Without worthwhile data, you’re basically throwing money out the window, Faulhaber says.

Timing is also important, he says. With direct mail, Faulhaber says you have about five seconds to get someone’s attention, so your message has to be catchy.

MAKE YOUR WEBSITE SHINE

Trey Markel, a software specialist at CentrexSoftware, a customer relationship management software company in Costa Mesa, Calif., says it’s shocking how many funders don’t use their websites to generate leads. Markel, who consults with B2B lenders and MCA providers on marketing strategies using enterprise software, recommends funders spend time working on their website so that it appeals to all types of visitors: those who want to read relevant articles, those who want to watch webcasts and those who want to listen to podcasts.

The idea is for funders to use their website to provide helpful information to merchants that will, in turn, encourage them to seek funding from you. For instance, you might consider hosting monthly webinars on topics such as how businesses can use loaned money to increase their marketing budget. Another topic merchants may find appealing is how to use credit cards to increase customers. “You give them a solution to a problem, and then you give them the money to go afford that solution,” Markel says.

Many funders know how to close a deal, but they fail to understand that the consultative approach over time will gain them even more business, Markel says. “Becoming a trusted information source in the industry is so much more valuable to customers than just being a funder,” he says. The industry needs “professionals who are going to tell you how to solve a problem.”

GET PERSONAL

Jennie Villano, vice president of business development at Kalamata Advisors LLC, says ISOs looking to build their business should attend networking events where small businesses are present. Sounds simple, but many ISOs don’t take advantage of this, meaning a missed opportunity to connect with “people from every facet” including accountants and other business professionals who can be a good source of referrals.

She also recommends ISOs hire at least one professional who is warm, trusting and engaging to visit merchants at their place of business. She recommends they pick places such as local strip malls which have a sizeable number of merchants. If you saw 20 merchants a day and only two funded with you that amounts to 40 extra deals a month, she points out. “Many ISOs would benefit from an extra 40 deals a month,” she says. On top of that, you have additional touchpoints because each of the merchants you visit may tell other businesses about your services, she says.

USE SOCIAL MEDIA

ISOs should also use social media more often than they do now—and not just to find sales help, Villano recommends. She uses it to target ISOs, but in the course of that, she gets inquiries from small businesses. ISOs should be using social media to find small businesses in need of funds. “I just don’t know why they aren’t using it more. It has tremendous reach,” she says.

To be sure, you don’t have to bombard your connections with posts. Once every other week is a good target. Make sure to include your business name and phone number, but posts shouldn’t be a hard sell. “There are ways to stand out and get your message across without appearing pushy or too sales oriented. The two-minute video ‘Cooking with Kalamata Capital’ that went viral in the industry is an example,” she says.

Also remember there are many social media venues. Sometimes funders focus their efforts on LinkedIn, Facebook and, to a lesser extent, Twitter. But Instagram and Pinterest can also be used to target potential customers. Posting aspirational videos or photos in these venues can help encourage businesses to think about ways to fund the things they might need, says Berg of 6th Avenue Capital.

USE EMAIL MARKETING TO YOUR ADVANTAGE

Some funding professionals say text messaging works well for them, though others prefer email for a host of reasons.

For one thing, it’s a “little less intrusive” than a telephone call or a text, Berg says. Also, with email, there’s ample ability to personalize, and you can run analytics to determine helpful metrics such as open rates and click-through rates, for example. You can compare how these metrics change when you tinker slightly with email subject lines or messages.

“We see email as a very viable channel,” she says.

Another advantage of email is that it helps funders and brokers get around the restrictions imposed by the Telephone Consumer Protection Act (TCPA) that has hampered lead generators’ ability to solicit business owners, says Michael O’Hare, president of Blindbid, a B2B lead generation site.

With email, you can direct the prospect to click on a link, which then triggers a phone call from a sales rep. In an environment when cold-calling can result in a lawsuit, email is a viable alternative, says O’Hare, an outspoken opponent of TCPA restrictions for business-related matters.

A growing number of funders are also using or exploring the use of artificial intelligence to help with lead generation, says Matthew Martin, managing director of Silver Bullet Marketing, a provider of trigger lead data.

One company that’s working in this area is AI Assist. Using Conversica, an AI-powered virtual sales assistant, funders can send automated emails to prospects. The automated sales assistant determines whether the prospect is interested, and if so, it alerts a human sales representative. The automated sales assistant can also gather additional information from a lead, such as the best phone number and best time to call. The entire “dialogue” is available for the human sales rep to review.

“AI is not going to make the sale for you, but it’s going to give you enough information to move forward,” Martin says.

REFINE YOUR LEADS

REFINE YOUR LEADS

To generate leads, funders, ISOs and brokers tend to buy banner ads on Google or send an email blast with a link for interested businesses to click on. The link usually directs businesses to an online form that typically asks for their name, telephone number, email and how much money is being requested.

But it doesn’t generate meaningful information about the business or what type of funding product the business is looking for, says O’Hare of Blindbid. These forms don’t typically include critical information such as whether the person has been in business for less than a year, whether he or she has mounds of debt or what kind of funding the business is seeking.

One way to get better, more tailored leads is with “lead quizzes” similar to those used by the online insurance industry, he says. Instead of a basic form, potential leads would be directed to fill out a form that has much more pointed questions about the person, the business and the type of funding sought, he explains. Some questions might be, for instance: Is your credit score over 500? Have you been in business for more than a year? And, what type of funding are you seeking? Based on the merchant’s responses, he or she could be directed to a certain funding product or a specific funder, if you’re an ISO working with multiple providers. The funder could also decide to pass on an opportunity based on a merchant’s answers to the lead quiz.

O’Hare says he doesn’t know of MCA providers currently using this type of form, but it’s one of the things he’s working on as a way to generate better leads for his clients. With the basic forms many funders use today, you get a “lot of garbage,” O’Hare says.

Certainly, there are many ways to market and get leads, but industry professionals say one thing is clear: you can’t rely on one avenue alone. According to Markel of CentrexSoftware, too many in the industry put too much faith in raw data that gets plugged into a phone system dialer. The quality of this data isn’t always the best, which means funding professionals are wasting a lot of time, he says. “There are only so many small businesses in the country and an even smaller amount that are fundable,” he says.

Gale Force Twins

April 24, 2018

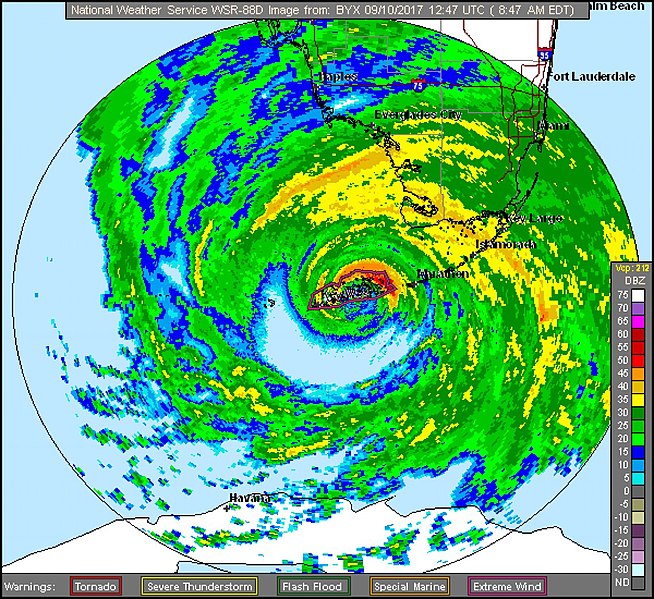

As Hurricane Irma swept through the Caribbean and barreled toward the Florida Keys early last September, Wendy Vila, chief executive, at Unicus Capital evacuated her home in West Palm Beach and decamped to Panama City in the Florida panhandle where “it was just a little bit rainy.”

After safely waiting out Irma, she says, her return south was precarious. The roads were strewn with tree branches and other debris. Fuel was scarce. Many gas stations were either closed or posted signs reading “No Gas.” “Restaurants had run out of food,” Vila adds, “so there was nothing to eat” along the highway.

She returned to West Palm Beach but didn’t stay long. Instead, Vila again drove west, this time across the Florida peninsula to the South Florida city of Naples, not far from where Irma had made landfall. “I went there to volunteer with Samaritan’s Purse for two days,” she says, referring to the Boone, N.C.-based Christian organization that provides humanitarian aid to people in physical need. “Things were a lot worse there than in West Palm Beach,” she reports. “A lot of trees were down, houses were flooded and people had to throw all of their belongings out onto the street.”

Meanwhile, many of the Florida merchants whom Unicus funds were distressed. “If people had no power,” Vila says, “they couldn’t function. A lot of businesses had to close down. For some merchants in the affected areas,” she adds, Unicus extended “a 90-day grace period.”

Vila’s experience with Hurricane Irma – both professionally and personally — is not an isolated one. She is among several business lenders whom AltFinanceDaily interviewed about the storm and its aftermath. This article grew out of AltFinanceDaily’s Florida networking event at the Gale Hotel in South Beach in late January. We went back to many of the attendees as well as to other business-funders in The Sunshine State and sought out their experiences before, during and after the powerful tempest.

At one point, Hurricane Irma was the strongest hurricane ever recorded in the Atlantic by the National Hurricane Center. As Irma took dead aim at Florida, it packed sustained winds exceeding 157 miles per hour, earning it the designation of a Category 5 storm, the highest and most destructive. It slammed into the Florida Keys as a Category 4 hurricane, reached the Gulf of Mexico, and then came ashore a second time on Florida’s west coast at Marco Island, just south of Naples, and began traversing the state as a Category 3 hurricane, gradually losing strength. By the time Irma exited Florida, it had been downgraded to a tropical storm. According to the National Hurricane Center, Irma caused an estimated $50 billion in damage in the U.S., making it the fifth-costliest hurricane to hit the mainland.

Financiers and brokers told personal stories of working with and assisting merchants across Florida who sought to regain their lost footing and keep from going — literally — underwater. In many cases, members of the alternative business financing community said, they were simultaneously assisting troubled merchants while they themselves struggled with Irma-occasioned troubles that ranged from inconvenience to hardship.

“I was ten days without power,” says Manny Columbie, funding manager at Axiom Financial, based in South Miami. Columbie, who lives in the residential Westchester district of Miami, not far from the campus of Florida International University, says that he conducts much of his business from his home. That power loss not only constrained his ability to keep working but posed a life-or-death situation for his family: Columbie’s 90-year-old grandmother, who lives with him and his girlfriend, depends on electrical power to operate her oxygen pump.

Fortunately, he says, he had a backup generator, the use of which alternated between providing power for his grandmother’s oxygen and the family’s refrigerator. Meanwhile, his roof was leaking and there was six inches of rainwater swamping the house — the water gushing into the kitchen through the laundry room, dishwasher and even the oven.

Fortunately, he says, he had a backup generator, the use of which alternated between providing power for his grandmother’s oxygen and the family’s refrigerator. Meanwhile, his roof was leaking and there was six inches of rainwater swamping the house — the water gushing into the kitchen through the laundry room, dishwasher and even the oven.

While Columbie saw instances of tempers growing short in Miami’s September heat, he was nonetheless cheered by the way his community responded. “Neighbors were coming by to see if I needed gasoline for my generator,” Columbie says. “People were firing up food on their outside grills. There was no air-conditioning or cold showers but we cooled off by jumping in a neighbor’s pool. I saw a lot of people coming together.”

At the same time, he was doing what he could to assist merchants who did business with Axiom. Only one – a retail clothing store in Miami – was permanently shuttered. One of his clients, Oscar Pratt, owner of Odessy Party Supplies in Miami Gardens, was grateful for a moratorium on daily payments.

“We’re in the business of selling party accessories for events from births to funerals and everything in-between,” Pratt says. “Baby showers, christenings, birthdays, quinceaneras, ‘Sweet Sixteens,’ graduations, weddings, and all kinds of themed parties like Halloween,” he says. “We sell plates and cups, candy bags, cake-toppers, small favors, pinatas…”

Pratt said he’d called his funders ahead of the storm and “requested some leeway” from payments. Once the storm hit – and for two weeks afterward while there was no electricity – the party-supply business was pretty much on hold. “We had a few days without electricity or phone,” he says. “We couldn’t open the doors and do business because we use computer-generated receipts. Our customer base was down to just about nothing. Without electricity, people weren’t working and they weren’t having parties.”

Following the two-week grace period, Pratt says that his funders, which included QuarterSpot, granted a second two-week period of leniency in which Odessy was allowed to make reduced payments. “It was very difficult,” he says. “There was no help from FEMA (Federal Emergency Management Agency) or from our insurance company since we’re on high ground and there were no physical damages, just the electricity.”

He reckoned that Odessy, which boasts annual revenues of $1.2 million, was deprived of roughly $50,000-$60,000 in sales because of Irma. Pratt reports that if his lenders had “played hardball” and demanded that he make his payments, he could have stayed in business thanks to “cash on hand” but it wouldn’t have been easy.

Meantime, his lenders’ forbearance was soon rewarded. By October, business was back to normal and he resumed making payments in full. “As soon as the lights went on,” Pratt says, “the parties started again.”

Similarly, says Paul Boxer, chief marketing officer at Quicksilver Capital in Brooklyn, the ultimate impact of Hurricane Irma on his firm’s funding business was to build trust and cement relationships with clients in South Florida. “We had a full team on board to answer the large number of calls coming in and to assist our merchants with any questions they had,” he says.

Many affected merchants, Boxer reports, were forced to evacuate ahead of the storm. When they returned, it was common for them to discover that their shops and stores sustained flooding damage from the heavy rains and a storm surge. Roofs were blown-off and structures were battered by 100-plus mile-an-hour winds, falling trees, and whipped-up debris. Even businesses that suffered little damage were paralyzed by the loss of electricity, impassable roads, and the absence of customers.

Many affected merchants, Boxer reports, were forced to evacuate ahead of the storm. When they returned, it was common for them to discover that their shops and stores sustained flooding damage from the heavy rains and a storm surge. Roofs were blown-off and structures were battered by 100-plus mile-an-hour winds, falling trees, and whipped-up debris. Even businesses that suffered little damage were paralyzed by the loss of electricity, impassable roads, and the absence of customers.

“Some were down for a few days,” Boxer reports. “Some were down a month to two months. We kept in touch. We were really on top of things with our merchants and asking them what they needed. We even fielded general safety questions and directed them on whom to call with insurance questions and other related business questions. It was good business,” he adds, “because it showed you cared. We were looking to do the right thing by our merchants and they appreciated it.”

Quicksilver typically offered merchants a two-to-three week “reprieve” on payments, Boxer says. For those businesses and entreprenuers whose operations were “completely out of commission” and needed more time, he says, the company suspended payments for as long as two months.

In the end, Quicksilver’s policy of forbearance reaped dividends. It not only built up good will with its customer base but also with the Independent Sales Organizations (ISOs) who’d brokered many of the firm’s Florida deals. “We helped grow that relationship,” Boxer says of the merchant-ISO connection. “They (ISOs) love getting renewals. It’s been a win-win for everybody.”

Doug Rovello, senior managing partner at Fund Simple, Inc., an alternative business lender and broker in Palm Harbor, a beach town just outside Tampa, says the Tampa-St. Petersburg area was spared from severe flooding but “we did experience power outages.” Among his clients, he reports, businesses in the food industry were among the most vulnerable. “I had one restaurant that lost $200,000 in business in the month of September,” he says.

When the electricity went down, grocery stores and bodegas, restaurants, bars, pizzerias, sub shops, delis and luncheonettes suffered outsized losses. Without power, businesses in the food industry were forced to dump spoiled meat, rotting fish, unusable dishes like appetizers and other foodstuffs requiring refrigeration.

When the electricity went down, grocery stores and bodegas, restaurants, bars, pizzerias, sub shops, delis and luncheonettes suffered outsized losses. Without power, businesses in the food industry were forced to dump spoiled meat, rotting fish, unusable dishes like appetizers and other foodstuffs requiring refrigeration.

Rovello reports that the hurricane managed to bollix up the business of one top client, a leading ticket broker in the area with a reputation for obtaining “exclusive” tickets to major events such as A-list rock concerts and featured sporting contests – including the Super Bowl. “He buys tickets in advance and when one big event was canceled he got stuck with $30,000 in tickets that he had to eat,” Rovello says.

Other kinds of businesses that depend on alternative lenders and got hit hard from the loss of power, Rovello observes, were medical clinics, doctors’ offices, pain-management centers, and assisted-living quarters – particularly those south of Sarasota. A number of golf courses also closed down for a couple of weeks, Rovello notes, further impairing the tourism and entertainment economy. “They were not allowed to move any of the damage that was done – poles, trees, et cetera until FEMA got there,” he says.

For some 30 days following Irma’s arrival, Rovello reports that he asked clients to make modest payments – perhaps $100 instead of a $750 monthly payment — “to keep their accounts active.” He also used his connections with FEMA adjusters and interceded with funders on behalf of clients– and even businesses that were not clients – who found themselves in arrears.

While many Floridians were seeking higher ground or hightailing it out of state, Jay Bhatt, who is a senior vice president of marketing at Breakout Capital in McLean, Va., was catching one of the last Jet Blue flights into Orlando to help out his aging parents. They are now in their late 60s and 70s, he reports, and living in a retirement community in Polk County, about ten miles south of Disney World.

Irma was still a Category 1 hurricane with 100 mph winds when it hit Orlando. The electrical grid went down, but Bhatt was able to purchase a generator – the kind designed specifically to provide electricity for oxygen respirators — from Home Depot. During his stay, Bhatt made several car trips in search of fuel, each of which took him probably 35-40 minutes. “We also leveraged some of the neighbors’ sockets,” he says, “but they were so small that the wattage only allowed for the operation of the fridge and a fan.”

Electricity was restored after four or five days. “The fact that it was a retirement community might have been why we got power back so soon while it took two or three weeks for many others,” he reckons.

While Bhatt’s attention was focused on his parents, his employer – which had just offered a blanket hold on payments to its merchant accounts in 11 Texas counties that had been simultaneously inundated and walloped by Hurricane Harvey – now faced the challenge of responding to the second hurricane in two weeks. With Irma, Breakout chose to deal with its customers individually. “We didn’t do an immediate blanket response” as in Texas, Bhatt says, adding: “We were able to contact each one and we only wrote off one small business.”

While Bhatt’s attention was focused on his parents, his employer – which had just offered a blanket hold on payments to its merchant accounts in 11 Texas counties that had been simultaneously inundated and walloped by Hurricane Harvey – now faced the challenge of responding to the second hurricane in two weeks. With Irma, Breakout chose to deal with its customers individually. “We didn’t do an immediate blanket response” as in Texas, Bhatt says, adding: “We were able to contact each one and we only wrote off one small business.”

Rakem Lampkin, senior customer service representative at Pearl Capital, a New York-based alternative funder, says that his firm funds “roughly 175” businesses in South Florida. In addition to those establishments already mentioned as economically reeling because of Irma, such as restaurants, he cited “car dealerships, automotive repair shops and tech companies” as among the hardest hit, especially from the lack of electricity.

Lampkin also noted that many of Pearl’s merchants felt Irma’s wrath when colleges and state schools closed their doors. “Everything from transportation, lunches, sports equipment, even mom-and-pop florists” were slammed, he says, adding: “When the schools shut down, our payments slowed down.”

Pearl provided preferential treatment to merchants on the coast who were granted “a hold on debit payments,” Lampkin says. Even for coastal businesses that remained “structurally sound,” the business owners’ and employees’ “homes were affected, which kept them from getting to work,” he says.

As for businesses situated inland, “We were still sympathetic,” Lampkin says, but after an initial five-day grace-period their discounts were in the range of 66%-75% “so that we could focus our resources toward the people on the coast.”

To monitor the situation from New York, Lampkin says, the company was able to rely on accounts in the local news media, Google Maps, and other Internet sources. “We evaluated the situation case-by-case and week-by-week,” he says.

Jennifer Legg, a co-owner of Rochelle’s Jewelry & Watch Repair at the Indian River Mall in Vero Beach, is a Pearl-funded merchant who says she shut down the family-run business “for six or seven days” after Irma while the electricity went out. “Trees were down and a lot of people lost food and trailers, but we were not impacted as much as we were supposed to be,” she remarked.

Most of the shop’s business consists of customers stopping in for a new battery or a watch-band. Once they’re in the store, there’s a chance that they’ll purchase something else. But Irma put the kibosh on mall traffic. “A lot of people left the state, so that hurt business,” Legg says.

The store – which records annual sales of about $200,000 — lost probably $10,000 in revenue because of Irma. “It was very hard for that month of September,” Legg says. “Even after the doors opened, it was dead. No money came in for about two weeks.”

Fortunately, though, her capital source “did not take money out for a week,” she says. “If they’d kept taking it out,” she added, “we would have defaulted.”

Wayward Merchants

April 19, 2018

Wayward merchants and outright criminals are continuing to bilk the alternative small-business funding industry out of cash at a dizzying pace. In fact, an estimated 23 percent of the problematic clients that funders reported to an industry database in 2017 appeared to have committed fraud, up from approximately 17 percent in the previous year. That’s according to Scott Williams, managing member of Florida-based Financial Advantage Group LLC, who along with Cody Burgess founded the DataMerch database in 2015. Some 11,000 small businesses now appear in the database because they’ve allegedly failed to honor their commitments to funders, Williams says.

Whether fraudulent or not, defaults remain plentiful enough to keep attorneys busy in funders’ legal departments and at outside law firms funders hire. “I do a lot of collections work on behalf of my cash-advance clients, sending out letters to try to get people to pay,” says Paul Rianda, a California-based attorney. When letters and phone calls don’t succeed, it’s time to file a lawsuit, he says.

Lawsuits become necessary more often than not by the time a funder hires an outside attorney, according to Jamie Polon, a partner at the Great Neck, N.Y.- based law firm of Mavrides Moyal Packman Sadkin LLP and manager of its Creditors’ Rights Group. “Typically, my clients have tried everything to resolve the situation amicably before coming to me,” he observes.

That pursuit of debtors isn’t getting any easier. These days, it’s not just the debtor and the debtor’s attorney that funders and their attorneys must confront. Collections have become more difficult with the recent rise of so-called debt settlement companies that promise to help merchants avoid satisfying their obligations in full, notes Katherine Fisher, who’s a partner in the Maryland office of the law firm of Hudson Cook LLP.

Meanwhile, a consensus among attorneys, consultants and the funders themselves holds that the nature of the fraudulent attacks is changing. On one side of the equation, crooks are hatching increasingly sophisticated schemes to defraud funders, notes Catherine Brennan, who’s also a partner in the Maryland office of Hudson Cook LLP. On the other side, underwriters and software developers are becoming more skilled at detecting and thwarting fraud, she maintains.

Meanwhile, a consensus among attorneys, consultants and the funders themselves holds that the nature of the fraudulent attacks is changing. On one side of the equation, crooks are hatching increasingly sophisticated schemes to defraud funders, notes Catherine Brennan, who’s also a partner in the Maryland office of Hudson Cook LLP. On the other side, underwriters and software developers are becoming more skilled at detecting and thwarting fraud, she maintains.

Digitalization is fueling those changes, says Jeremy Brown, chairman of Bethesda, Md.-based RapidAdvance. “As the business overall becomes more and more automated and moves more online – with less personal contact with merchants – you have to develop different tools to deal with fraud,” he says.

A few years ago, the industry was buzzing about fake bank statements available on craigslist, Brown recalls. Criminals who didn’t even own businesses used the phony statements to borrow against nonexistent bank accounts, and merchants used the fake documents to inflate their numbers.

Altered or invented bank statements remain one of the industry’s biggest challenges, but now they’ve gone digital. About 85 percent of the cases of fraud submitted to the DataMerch database involve falsified bank documents, nearly all of them manipulated digitally, Williams notes.

Merchants alter their statements to overstate their balances, increase the amount of their monthly deposits, erase overdrafts, or hide automatic payments they’re already making on loans or advances, Williams says. Most use software that helps them reformat and tamper with PDF files that begin as legitimate bank statements, he observes.

To combat false statements, alt funders are demanding online access to applicants’ actual bank accounts. Some funders ask for prospective clients’ usernames and passwords to examine bank records, but applicants often consider such requests an invasion of their privacy, sources agree.

That’s why RapidAdvance has joined the ranks of companies that use electronic tools like DecisionLogic, GIACT or Yodlee to verify a bank balance or the owner of the account and perform test ACH transfers – all without needing to persuade anyone to surrender personally identifiable information, Brown says.

Other third-party systems can use an IP address to view the computing device and computer network that a prospective customer is using to apply for credit, Brown says. RapidAdvance has received applications that those tools have traced to known criminal networks. The systems even know when crooks are masking the identity of the networks they’re using to attempt fraud, he observes.

RapidAdvance has also developed its own software to head off fraud. One program developed in-house cross references every customer who’s contacted the company, even those who haven’t taken out a loan or merchant cash advance. “People who want to defraud you will come back with a different business name on the same bank account,” Brown says. “It’s a quick way to see if this is somebody we don’t want to do business with.”

Sometimes businesses use differing federal tax ID numbers to pull off a hoax, according to Williams at DataMerch. That’s why his company’s database lists all of the ID numbers for a business.

All of those electronic safeguards have come into play only recently, Brown maintains. “We didn’t think about any of this five years ago – certainly not 10 years ago,” he says. In those days, funders were satisfied with just an application and a copy of a driver’s license, he remembers.

Since then, some sage advice has been proven true. When RapidAdvance was founded in 2005, the company had a mentor with experience at Capital One, Brown says. One piece of wisdom the company guru imparted was this: “Watch out when the criminals figure out your business model.” That’s when an industry becomes a target of organized fraud.

As that prediction of fraud has become reality, it hasn’t necessarily gotten any easier to pinpoint the percentage of deals proposed with bad intent. That’s because underwriters and electronic aids prevent most fraudulent potential deals from coming to fruition, Brown notes. The company looks at the loss rates for the deals that it funds, not the deals it turns down.

Brown guesses that as many as 10 percent of applications are tainted by fraudulent intention. “It’s meaningful enough that if you miss a couple of accounts with significant dollar amounts,” he says, “then it can have a pretty negative impact on your bottom line.”

Some perpetrators of fraud merely pretend to operate a small business, and funders can discover their scams if there’s time to make site visits, Rianda notes. Other clients begin as genuine entrepreneurs who then run into hard times and want to keep their doors open at all costs, sources agree.

Applicants sometimes provide false landlord information, something that RapidAdvance checks out on larger loans, Brown notes. Underwriters who call to verify the tenant-landlord relationship have to rely upon common sense to ferret out anything “fishy,” he advises.

Applicants sometimes provide false landlord information, something that RapidAdvance checks out on larger loans, Brown notes. Underwriters who call to verify the tenant-landlord relationship have to rely upon common sense to ferret out anything “fishy,” he advises.

Underwriters should ask enough questions in those phone calls to determine whether the supposed landlord really knows the property and the tenant, which could include queries concerning rent per square foot, length of time in business and when the lease terminates, Brown suggests. All of that should match what the applicant has indicated previously.

Lack of a telephone landline may or may not provide a clue that an imposter is posing as a landlord, Brown continues. Be aware of a supposed landlord’s verbal stumbles, realize something’s possibly amiss if a dubious landlord lacks of an online presence, note whether too many calls to the alleged landlord go into voicemail and be suspicious if a phone exchange with a purported landlord simply “feels” residential instead of commercial, he cautions.

Reasonable explanations could exist for any of those concerns, but when in doubt about the validity of a tenant-landlord relationship it pays to request a copy of the lease or other type of verifications, according to Brown. Then there are the cases when the underwriter is talking to the actual landlord, but the applicant has convinced the landlord to lie. It could happen because the landlord might hope to recoup some back rent from a merchant who’s obviously on the verge of closing up shop.

Occasionally, formerly legitimate merchants turn rogue. They take out a loan, immediately withdraw the funds from the bank, stop repaying the loan, close the business and then walk or run away, notes Williams. “We view that as a fraudulent merchant because their mindset all along was qualifying for this loan and not paying it back,” he says.

Collecting on a delinquent account becomes problematic once a business closes its doors, Rianda notes. As long as the merchant remains in business, funders can still hope to collect reduced payments and thus eventually get back most or all of what’s owed, he maintains.

In another scam sometimes merchants whose bank accounts are set up to make automatic transfers to creditors simply change banks to halt the payments, Brown says. That move could either signal desperation or indicate the intent to defraud was there from the start, he says.

Merchants with cash advances that split card revenue could change transaction processors, install an additional card terminal that’s not programmed for the split or offer discounts for paying with cash, but those scams are becoming less prevalent as the industry shifts to ACH, Brown says. Industrywide, only 5 percent to 10 percent of payments are collected through card splits these days, but about 20 percent of RapidAdvance’s payments are made that way.

Merchants occasionally blame their refusal to pay on partners who have absconded with the funds or on spouses who weren’t authorized to apply for a loan or advance, Brown reports. Although that claim might be bogus, such cases do occur, notes Williams of DataMerch. People who own a minority share of a business sometimes manipulate K-1 records to present themselves as majority owners who are empowered to take out a loan, Williams says.

In a phenomenon called “stacking,” merchants take out multiple loans or advances and thus burden themselves with more obligations than they can meet. Whether or not that constitutes fraud remains debatable, Rianda observes. Stacking has increased with greater availability of capital and because some funders purposely pursue such deals, he contends.

Some contracts now contain covenants that bar stacking, notes Brennan of Hudson Cook. As companies come of age in the alt-funding business, they are beginning to employ staff members to detect and guard against practices like stacking, she says.

Moreover, underwriting is improving in general, according to Polon “The vetting is getting better because the industry is getting more mature,” he says. “The underwriting teams have gotten very good at looking at certain data points to see something is wrong with the application – they know when something doesn’t smell right.” They’re better at checking with references, investigating landlords, examining financials and requesting backup documentation, he contends.

Despite more-systematic approaches to foiling the criminal element and protecting against misfortunate merchants, one-of-a-kind attempts at fraud also still drive funders crazy, Brown says. His company found that a merchant once conspired with the broker who brought RapidAdvance the deal. The merchant and the broker set up a dummy business, transferred the funds to it and then withdrew the cash. “The guy came back to us and said, ‘I lost all the money because the broker took it,’” he recounts. “Why is that our problem?” was the RapidAdvance response.

Although such schemes appear rare, some funders are developing methods of auditing their ISOs to prevent problems, notes Brennan. They can search for patterns of irregularities as an early-warning system, she says. It’s also important to terminate relationships with errant brokers and share information about them, she advises, adding that competition has sometimes made funders reluctant to sever ties with brokers.

Although fraud’s clearly a crime, the police rarely choose to involve themselves with it, Brown says. His company has had cases where it lost what it considered large dollar amounts – say $50,000 – and had evidence he felt clearly indicated fraud but the company couldn’t attract the attention of law enforcement, he notes.

Although fraud’s clearly a crime, the police rarely choose to involve themselves with it, Brown says. His company has had cases where it lost what it considered large dollar amounts – say $50,000 – and had evidence he felt clearly indicated fraud but the company couldn’t attract the attention of law enforcement, he notes.

Rianda finds working with law enforcement “hit or miss,” whether it’s a matter of defaulting on loans or committing other crimes. In one of his cases an employee forged invoices to steal $100,000 and the police didn’t care. In another, someone collected $3,000 in credit card refunds and went to jail. If the authorities do intervene, they may seek jail time and sometimes compel crooks to make restitution, he notes.

“Engaging law enforcement is generally not appropriate for collections,” according to Fisher from Hudson Cook. However, notifying police agencies of fraud that occurs at the inception of a deal can sometimes be appropriate, says Fisher’s colleague Brennan, particularly when organized gangs of fraudsters are at work.

At the same time, sheriffs and marshals can help collect judgments, Polon says. He works with attorneys, sheriffs and marshals all over the country to enforce judgments he has obtained in New York State, he says. That can include garnishing wages, levying a bank account or clearing a lien before a debtor can sell or refinance property, he notes.

When Rianda files a lawsuit against an individual or company in default, the defendant fails to appear in court about 90 percent of the time, he says. A court judgment against a delinquent debtor serves as a more effective tool for collections than does a letter an attorney sends before litigation begins, Rianda notes.

But even with a judgment in hand, attorneys and their clients have to pursue the debtor, often in another state and sometimes over a long period of time, Rianda continues. “The good news is that in California a judgment is good for 10 years and renewable for 10,” he adds.

So guarding against fraud comes down to matching wits with criminals across the country and around the world. “It makes it hard to do business, but that’s the reality,” Brown concludes. Still, there’s always hope. To combat fraud, funders should work together, Brennan advises. “It’s an industrywide problem … so the industry as a whole has a collective interest in rooting out fraud.”

Kabbage to Acquire Orchard Platform Markets

April 14, 2018Update 4/26/18: The acquisition is now confirmed

Kabbage is set to acquire Orchard Platform Markets, a provider of lending data and investment advisory services, according to a Bloomberg report yesterday. However, neither company has confirmed this and both companies were unreachable today.

Kabbage is set to acquire Orchard Platform Markets, a provider of lending data and investment advisory services, according to a Bloomberg report yesterday. However, neither company has confirmed this and both companies were unreachable today.

Orchard was founded in 2013 by David Snitkof, Angela Ceresnie, Jonathan Kelfer, Matt Burton and Phil Rosen. Burton and Kelfer both worked previously at Google and Snitkof and Ceresnie worked at Citigroup and American Express. The company has raised nearly $60 million in three rounds, according to Crunchbase, and investors include Spark Capital, Thrive Capital, as well as Vikram Pandit, former CEO of Citigroup and John Mack, former CEO of Morgan Stanley. Indeed, no shabby group.

As this acquisition has not yet been confirmed, the amount Kabbage might be paying for the company is also unknown. According to Orchard’s website, it employs 31 people (including executives) in an office in Manhattan’s Flatiron district, known as a hub for tech startups. The Bloomberg story indicates that co-founders Burton and Snitkof will join Kabbage at its New York office. Founders Ceresnie and Rosen no longer work for Orchard. With headquarters in Atlanta, Kabbage is one of the largest small business lenders in the country and recently launched a new feature of its loan product at LendIt.

Despite the big name investors Orchard had when it started, some suspect the company may have lost momentum. AltFinanceDaily called a number of leaders in the alternative lending space and none were willing to comment until the acquisition was made certain.

How One CEO Unified Two Companies with Different Cultures on Different Coasts

March 21, 2018 Company mergers, like marriages, have their pros and cons. Some are more successful than others and many say it’s unwise to rush into one. This is certainly the approach Adam Stettner adopted when he, as CEO of San Diego, CA-based Reliant Funding, oversaw the merger of his company with Merchants Capital Access, based in Melville, NY on Long Island.

Company mergers, like marriages, have their pros and cons. Some are more successful than others and many say it’s unwise to rush into one. This is certainly the approach Adam Stettner adopted when he, as CEO of San Diego, CA-based Reliant Funding, oversaw the merger of his company with Merchants Capital Access, based in Melville, NY on Long Island.

At the time of the merger in April 2015, Merchants Capital Access was an MCA funder. According to Stettner, they were what he considered a “back end” as they didn’t do marketing or sales. They did underwriting and funding, but they did not originate any new business.

Reliant Funding, which Stettner led, did almost the inverse. While it did some cursory underwriting, it mostly marketed and sold funding to small businesses. It would also package small business merchants and place them for appropriate funding. But they did not fund directly. So, it seems, these two companies made for a perfect marriage. They completed each other. But not so fast.

Even though Stettner had considerable experience working as a direct lender in the student loan business prior to taking the helm at Reliant Funding in 2008, he didn’t feel ready to dive into funding a different type of client. (Stettner said he originated and held on his balance sheet $15 billion in student loans at National Lending Associates, a San Diego company he co-founded.)

“I felt like it was easy for somebody to come into the [merchant advance] space and start writing checks and funding businesses,” Stettner said. “It’s hard to figure out how to get that money back. So instead of jumping in with both feet, I thought it would be wise to really understand our target demographic, our end user, the small business owner.”

So while the technical merger of Reliant Funding and Merchants Capital Access happened in April 2015, the newly enlarged entity operated as two distinct brands until September 2017.

During this period, Stettner said, “we were studying everybody’s credit models and the best way to approach American small business owners, the best way to fund them, the best way to service them, and ultimately, the best way to renew them.”

This roughly two year period between the time of the actual merger and the official fusion of the two companies, now simply called Reliant Funding, was not just for Stettner to learn about funding small businesses. A lot more needed to happen to sync together a southern California company and a New York City-area company, each with different corporate cultures, attitudes and ways of getting work done.

“Getting 150 people with different views on work, culture, approach and strategy wasn’t easy,” Stettner said. “But it was definitely worthwhile and it was a lot of fun. There were times, of course, when it was frustrating as well.”

The stereotype of southern California being more laid back doesn’t hold up, according to Stettner, who grew up in New York and has worked in southern California for 14 years.

“While the environment may be laid back in appearance, the effort that’s put forth and the intensity that exists in the southern California office is no less than what you see out from our New York office,” Stettner said. “Both work incredibly hard and have great attitudes.”

However, he did say that the original culture in the New York office (formerly the Merchants Capital Access office) was much more centered around management decisions and Stettner made a point of bringing a culture of empowerment to that office.

What does that look like exactly?

“We talk [with employees] not only about the top line numbers, but also the bottom line numbers with the idea of empowering everyone,” Stettner said. “It’s important to me that everybody knows the why behind what we do. If people understand why we do something, it’s easier for them to get behind it, and they’re better equipped to offer an opinion that can help get us there faster.”

Now as Reliant Funding, Stettner said that the company is fully integrated under the one brand with unified systems and technology. The company is a funder with a sales team focused on direct origination. It also continues to grow what Stettner calls the wholesale channel or broker channel.

Lendio Opens Franchise in Charlotte, NC

March 15, 2018

Today, Lendio announced the opening of its latest franchise in Charlotte, NC. Through the Lendio franchise program, Chris Cronk will help local businesses in the community apply for loans, review their options and secure funding.

The company has a network of over 75 lenders and its funding options include SBA loans, startup loans, equipment loans, commercial real estate loans and more. In the last fiscal year alone, Lendio facilitated more than $300 million in funding, according to the company.

“I’ve worked with numerous companies and witnessed their struggles to find capital,” said Cronk, who was a former investment banker for Bank of America Merrill Lynch where he advised and facilitated financing for companies of all sizes. “Charlotte is a fast-growing market and community. I’m excited to be a part of that growth by helping businesses in every industry find funding.”

Mad Over Madden

March 15, 2018 In a dispute that reflects the nation’s rigid political polarization, a piece of legislation pending before Congress either corrects a judicial error or condones “predatory lending.” It depends upon whom one asks. Either way, the proposed law could affect the alternative small-business funding industry indirectly in the short run and directly in the long term by addressing the interest rates non-banks charge when they take over bank loans.

In a dispute that reflects the nation’s rigid political polarization, a piece of legislation pending before Congress either corrects a judicial error or condones “predatory lending.” It depends upon whom one asks. Either way, the proposed law could affect the alternative small-business funding industry indirectly in the short run and directly in the long term by addressing the interest rates non-banks charge when they take over bank loans.

The easiest way to understand the controversy may be to trace it back to a ruling in 2015 by the United States Court of Appeals for the Second Circuit in New York. The case of Madden v. Midland Funding LLC started as claim by a consumer who was challenging the collection of a debt by a debt buyer, says Catherine Brennan, a partner in the law firm Hudson Cook LLP.

“Debt buyers like Midland are sued on a regular basis,” Brennan notes. “That’s a common occurrence.” What’s uncommon is that the appellate court affirmed the idea that the loan debt that Midland sought to collect from Madden became usurious when Midland bought it. The court ruled that because Midland wasn’t a bank it was not entitled to charge the interest the bank was allowed to charge, she maintains.

Under the ruling, non-banks that buy loans can’t necessarily continue to collect the interest rates banks charged because non-banks are generally subject to the limits of the borrower’s state, according to the Republican Policy Committee, an advisory group established by members of the House of Representatives in 1949. Banks can charge the highest rate allowed in the state where they are chartered, which could be much higher than allowed in the borrower’s state.

“So it undermines the concept that you determine the validity of a loan at the time the loan is made,” Brennan says of the decision in the Madden case. The “valid-when-made” doctrine – a long-established principle of usury law – states that if a loan is not usurious when made it does not become usurious when taken over by a third party, published reports say. In 2016, the U.S. Supreme Court declined to hear the Madden case, which in effect upheld the appellate court ruling.

In response, both houses of Congress are considering bills that would ensure that the interest rate on a loan originated by a bank remains valid if the loan is sold, assigned or transferred to a non-bank third party, the Republican Policy Committee says.

On Feb. 14, 2018, the House passed its version of the proposal, H.R. 3299, the Protecting Consumers’ Access to Credit Act of 2017, or the “Madden fix,” as it’s known colloquially. The vote was 245 to 171, mostly along party lines with 16 Democrats joining 229 Republicans to vote in favor. The Senate version, S. 1642, had not reached a vote by press time.

“It’s not a revolutionary concept,” Brennan says of the proposed law. “It had been understood prior to Madden that you determine usury at the time the loan is originated, and that should be restored.”

As the alternative small-business funding industry continues to mature it could benefit from the legislation, Brennan predicts. In the future, alt funders may begin to buy or sell more debt, which would make it subject to the state caps if the legislation fails to pass, she says.

The proposed law would also benefit partnerships in which banks refer prospective borrowers to alternative funders because it would eliminate uncertainty and would thus improve the stability of the asset, Brennan continues. “I would think anyone in the commercial lending space would want to see the Madden bill pass,” she contends.

Stephen Denis, executive director of the Small Business Finance Association, a trade group for alt funders, agrees. While most of the SBFA’s members don’t work with bank partners, the trade group has supported the lobbying efforts of other associations and coalitions representing financial services companies directly affected, he says. “We are concerned on behalf of the broader industry because we all work closely together and everyone has the same goal of making sure that we’re providing capital to small businesses,” he maintains.

That goal of keeping funds available to entrepreneurs also motivates the sponsor of H.R. 3299, Rep. Patrick McHenry, R-N.C., who’s chief deputy whip of the House and vice chair of the House Financial Services Committee. His interest in crowdfunding, capital formation and disruptive finance is fueled by events he experienced in his childhood, when his father attempted to operate a small business but struggled to find financing, according to the Congressman’s website.

Although H.R. 3299 passed in the House with mostly Republican votes, it attracted bipartisan co-sponsors in that chamber. They are Rep. Gregory Meeks, D-N.Y.; Rep. Gwen Moore, D-Wis., and Rep. Trey Hollingsworth, R-Ind. The Senate version of the legislation is sponsored by Sen. Mark R. Warner, D- Va.

Although H.R. 3299 passed in the House with mostly Republican votes, it attracted bipartisan co-sponsors in that chamber. They are Rep. Gregory Meeks, D-N.Y.; Rep. Gwen Moore, D-Wis., and Rep. Trey Hollingsworth, R-Ind. The Senate version of the legislation is sponsored by Sen. Mark R. Warner, D- Va.

But opponents of the proposed law aren’t feeling particularly bipartisan and argue vehemently against it, Brennan contends. “There’s been a lot of misinformation put out there by consumer advocates saying this would somehow embolden payday lending in all 50 states,” she says. “It’s simply not true.”

Payday lenders aren’t banks, so the proposed legislation would not apply to them and thus would not enable them to avoid interest caps imposed by borrowers’ states, Brennan notes, adding that some states don’t even allow payday consumer lending.

Consumer advocates are spreading propaganda because they oppose interest rates they consider high, Brennan continues. Advocates are incorrectly conflating payday lending with marketplace lending, she maintains.

The latter is defined as partnerships where non-banks sometimes work with banks to operate nationwide platforms, mostly online and sometimes peer-to-peer, she says, noting that examples include LendingClub and Prosper.

There’s no evidence marketplace lenders would astronomically increase their interest rates if the president signs into law a bill that resembles those now before Congress, Brennan says. It wasn’t happening before Madden, she notes, and banks involved in those partnerships operate under strict guidance of the Federal Deposit Insurance Corp. (FDIC) or the Office of the Comptroller of the currency, depending upon their charters.

But consumer advocates haven taken to the warpath, Brennan reports. Opponents of the legislation call partnerships between banks and non-bank lenders by the derogatory term “rent-a-bank schemes.” But it’s lawful to create such relationships because the FDIC oversees them, she asserts.

Just the same, the House is considering H.R. 4439, a bill to ensure that in a bank partnership with a non-bank, the bank remains the “true lender” and can set the interest rate, Brennan notes. If the bill becomes law, it would clear up the conflict that has arisen in inconsistent case law, some of which has defined the non-bank as the true lender, she says.

Meanwhile, opponents of H.R. 3299 and S. 1642 have written a letter to members of Congress, urging them to vote against the bills. The letter, drafted by the Center for Responsible Lending (CRL) and the National Consumer Law Center (NCLC), was signed by 152 local, state, regional and national organizations. Most of the signers belong to a coalition called Stop the Debt Trap, says Cheye-Ann Corona, CRL senior policy associate.

The bills create a loophole that enables predatory lenders to sidestep state interest rate caps, Corona maintains. That’s because non-banks are actually originating the loans when they work in tandem with banks, she says. The non-banks are using banks as a shield against state laws because banks are regulated by the federal government. If the legislation passes, non-banks would not have to observe state caps and could charge triple-digit interest rates, she contends.

“This bill is trying to address the issue of fintech companies, but there is nothing innovative about usury,” Corona says. “They are just repackaging products that we’ve seen before. A loan is a loan. These lenders don’t need this bill if they are obeying state interest-rate caps.”

The lenders disagree. In fact, a trade group formed by OnDeck, Kabbage and Breakout Capital calls itself the Innovative Lending Platform Association, according to a report in the Los Angeles Times. The article cites the need for small-business capital but questions whether the loans are marketed fairly.

Innovative or not, lenders offering credit with higher interest rates could condemn consumers to a nightmare of debt, according to the letter from the CRL and NCLC to Capitol Hill. “Unaffordable loans have devastating consequences for borrowers – trapping them in a cycle of unaffordable payments and leading to harms such as greater delinquency on other bills,” the letter says.

However, alt funders say their savvy small-business customers understand finance and thus don’t need much government protection from high interest rates. But the CRL doesn’t adhere to that philosophy, Corona counters. “Small businesses are at risk with predatory lending practices,” she says, maintaining that some alt funders charge interest rates of 99 percent.

Small-business owners plunged themselves into hot water by borrowing too much in anecdotal examples provided by Matthew Kravitz, CRL communications manager. In one example, an entrepreneur found himself automatically paying back $331 every day. He overestimated his future income and now says he feels like hiding under the covers every morning.

Corona also dismisses the idea that high risk calls for high interest rates to compensate for high default rates. When interest rates rise to a level that borrowers can’t handle, no one wins, she maintains.

The right to charge higher interest rates could also encourage lenders to loosen their underwriting criteria, Corona warns. That could result in shortcuts reminiscent to the practices that gave rise to the foreclosure crisis and the Great Recession, she says, adding that, “we don’t want to see that happen again.”

The Madden Decision, Three Years Later

February 18, 2018

At first, reversing the 2015 Madden v. Midland Funding court decision, which continues to vex the country’s financial system and which is having a negative impact on the financial technology industry, seemed like a fairly reasonable expectation.

The controversial ruling by the Second Circuit Court of Appeals in New York, which also covers the states of Connecticut and Vermont, had humble roots. Saliha Madden, a New Yorker, had contracted for a credit card offered by Bank of America that charged a 27% interest rate, which was both allowable under Delaware law and in force in her home state.

But when Madden defaulted on her payments and the debt was eventually transferred to Midland Funding, one of the country’s largest purchasers of unpaid debts, she sued on behalf of herself and others. Madden’s claim under the Fair Debt Collection Practices Act was that the debt was illegal for two reasons: the 27% interest rate was in violation of New York State’s 16% civil usury rate and 25% criminal usury rate; and Midland, a debt-collection agency, did not have the same rights as a bank to override New York’s state usury laws.

In 2013, Madden lost at the district court level but, two years later, she won on appeal. Extension of the National Bank Act’s usury-rate preemption to third party debt-buyers like Midland, the Second Circuit Court ruled, would be an “overly broad” interpretation of the statute.

For the banking industry, the Madden decision – which after all involved the Bank of America — meant that they would be constrained from selling off their debt to non-bank second parties in just three states. But for the financial technology industry, says Todd Baker, a senior fellow Harvard’s Kennedy School of Government and a principal at Broadmoor Consulting, it was especially troubling.

“The ability to ‘export’ interest rates is critical to the current securitization market and to the practice that some banks have embraced as lenders of record for fintechs that want to operate in all 50 states,” Baker told AltFinanceDaily in an e-mail interview.

A 2016 study by a trio of law professors at Columbia, Stanford and Fordham found other consequences of Madden. They determined that “hundreds of loans (were) issued to borrowers with FICO scores below 640 in Connecticut and New York in the first half of 2015, but no such loans after July 2015.” In another finding, they reported: “Not only did lenders make smaller loans in these states post-Madden, but they also declined to issue loans to the higher-risk borrowers most likely to borrow above usury rates.”

With only three states observing the “Madden Rule,” the general assumption in business, financial and legal circles was that the Supreme Court would likely overturn Madden and harmonize the law. Brightening prospects for a Madden reversal by the Supremes: not only were all segments of the powerful financial industry behind that effort but the Obama Administration’s Solicitor General supported the anti-Madden petitioners (but complicating matters, the SG recommended against the High Court’s hearing the case until it was fully resolved in lower courts).

Despite all the heavyweight backing, however, the High Court announced in June, 2016, that it would decline to hear Madden.

That decision was especially disheartening for members of the financial technology community. “The Supreme Court has upheld the doctrine of ‘valid when made’ for a long time,” a glum Scott Stewart, chief executive of the Innovative Lending Platform Association – a Washington, D.C.-based trade group representing small-business lenders including Kabbbage, OnDeck, and CAN Capital — told AltFinanceDaily.

Even so, the setback was not regarded as fatal. Congress appeared poised to ride to the lending industry’s rescue. Indeed, there was rare bipartisan support on Capitol Hill for the Protecting Consumers’ Access to Credit Act of 2017 — better known as the “Madden fix.”

Introduced in the House by Patrick McHenry, a North Carolina Republican, and in the Senate by Mark Warner, Democrat of Virginia, the proposed legislation would add the following language to the National Bank Act. “A loan that is valid when made as to its maximum rate of interest…shall remain valid with respect to such rate regardless of whether the loan is subsequently sold, assigned, or otherwise transferred to a third party, and may be enforced by such third party notwithstanding any State law to the contrary.”

Just before Thanksgiving, the House Financial Services Committee approved the Madden fix by 42-17, with nine Democrats joining the Republican majority, including some members of the Congressional Black Caucus. Notes ILPA’s Stewart: “We were seeing broad-based support.”

But the optimism has been short-lived. The Madden fix was not included in a package of financial legislation recently approved by the Senate Banking Committee, headed by Sen. Mike Crapo, Republican of Idaho. Moreover, observes Stewart: “Senator Warner appears to have gotten cold feet.”

What happened? Last fall, a coast-to-coast alliance of 202 consumer groups and community organizations came out squarely against the McHenry-Warner bill. Denouncing the bill in a strongly worded public letter, the groups — ranging from grassroots councils like the West Virginia Citizen Action Group and the Indiana Institute for Working Families to Washington fixtures like Consumer Action and Consumer Federation of America – declared: “Reversing the Second Circuit’s decision, as this bill seeks to do, would make it easier for payday lenders, debt buyers, online lenders, fintech companies, and other companies to use ‘rent-a-bank’ arrangements to charge high rates on loans.”

The letter also charged that, if enacted, the McHenry-Warner bill “could open the floodgates to a wide range of predatory actors to make loans at 300% annual interest or higher.” And the group’s letter asserted that “the bill is a massive attack on state consumer protection laws.”

Lauren Saunders, an attorney with the National Consumer Law Center in Washington, a signatory to the letter and spokesperson for the alliance, told AltFinanceDaily that “our main concern is that interest-rate caps are the No. 1 protection against predatory lending and, for the most part, they only exist at the state level.”

But in their study on Madden, the Stanford-Columbia-Fordham legal scholars report that the strength of state usury laws has largely been sapped since the 1970s. “Despite their pervasiveness,” write law professors Colleen Honigsberg, Robert J. Jackson, Jr., and Richard Squire, “usury laws have very little effect on modern American lending markets. The reason is that federal law preempts state usury limits, rendering these caps inoperable for most loans.”

While the battle over the Madden fix has all the earmarks of a classic consumers-versus-industry kerfuffle, the fintechs and their allies are making the argument that they are being unfairly lumped in with payday lenders. “Online lending, generally at interest rates below 36%, is a far cry from predatory lending at rates in the hundreds of percent that use observable rent-a-charter techniques and that result in debt-traps for borrowers,” insists Cornelius Hurley, a Boston University law professor and executive director of the Online Lending Policy Institute. Because of fintechs, he adds: “A lot of people who wouldn’t otherwise qualify in the existing system are getting credit.”

A 2016 Philadelphia Federal Reserve Bank study reports that traditional sources of funding for small businesses are gradually exiting that market. In 1997, small banks under $1 billion in assets –which are “the traditional go-to source of small business credit,” Fed researchers note — had 14 percent of their assets in small business loans. By 2016, that figure had dipped to about 11 percent.

The Joint Small Business Credit Survey Report conducted by the Federal Reserve in 2015 determined that the inability to gain access to credit “has been an important obstacle for smaller, younger, less profitable, and minority-owned businesses.” It looked at credit applications from very small businesses that depend on contractors — not employees – and discovered that only 29 percent of applicants received the full amount of their requested loan while 30 percent received only partial funding. The borrowers who “were not fully funded through the traditional channel have increasingly turned to online alternative lenders,” the Fed study reported.

The ILPA’s Stewart gives this example: A woman who owns a two-person hair-braiding shop in St. Louis and wants to borrow $20,000 to expand but has “a terrible credit score of 640 because she’s had cancer in the family,” will find the odds stacked against when seeking a loan from a traditional financial institution.

But a fintech lender like Kabbage or CAN Capital will not only make the loan, but often deliver the money in just a few days, compared with the weeks or even months of delivery time taken by a typical bank. “She’ll pay 40% APR or $2,100 (in interest) over six months,” Steward explains. “She’s saying, ‘I’ll make that bet on myself’ and add two additional chairs, which will give her $40,000-$50,000 or more in new revenues.”

In yet another analysis by the Philadelphia Fed published in 2017, researchers concluded that one prominent financial technology platform “played a role in filling the credit gap” for consumer loans. In examining data supplied by Lending Club, the researchers reported that, save for the first few years of its existence, the fintech’s “activities have been mainly in the areas in which there has been a decline in bank branches….More than 75 percent of newly originated loans in 2014 and 2015 were in the areas where bank branches declined in the local market.”

Meanwhile, there is palpable fear in the fintech world that, without a Madden fix, their business model is vulnerable. Those worries were exacerbated last year when the attorney general of Colorado cited Madden in alleging violations of Colorado’s Uniform Consumer Credit Code in separate complaints against Marlette Funding LLC and Avant of Colorado LLC. According to an analysis by Pepper Hamilton, a Philadelphia-headquartered law firm, “the respective complaints filed against Marlette and Avant allege facts that are clearly distinguishable from the facts considered by the Second Circuit in Madden.

“Yet those differences did not prevent the Colorado attorney general from citing Madden for the broad-based proposition that a non-bank that receives the assignment of a loan from a bank can never rely on federal preemption of state usury laws ‘because banks cannot validly assign such rights to non-banks.’”

Should the Federal court accept the reasoning of Madden, Pepper Hamilton’s analysis declares, such a ruling “could have severe adverse consequences for the marketplace and the online lending industry and for the banking industry generally….”