Payroll Costs Still Exceed Revenues at StreetShares

November 7, 2018 According to the June 30 fiscal year-end earnings report for StreetShares, the veteran-run small business lender, the company’s annual payroll expenses of $4,580,130 exceeded its annual revenue of $3,078,766.

According to the June 30 fiscal year-end earnings report for StreetShares, the veteran-run small business lender, the company’s annual payroll expenses of $4,580,130 exceeded its annual revenue of $3,078,766.

StreetShares, which focuses on lending to veteran-owned small businesses, posted a loss of $6,559,702, more than last year’s loss of $6,193,154. But revenue did increase year over year, from $2,168,067 to $3,078,766.

“Our patient approach means we’re not going to be profitable for a couple more years,” StreetShares CEO Mark Rockefeller told AltFinanceDaily back in January in response to the fact that the company’s losses from 2017 exceeded its revenues by about 4 million. “But it also means we’ll still be here in 50 years.”

The gulf between StreetShares’ losses and revenues is narrower this year, but still considerable. In January 2018, StreetShares completed a $23 million series B funding round led by Rotunda Capital Partners, LLC.

StreetShares offers term loans and business lines of credit from $2,000 to $250,000. This in an increase from last year’s maximum loan amount of $150,000. Loans can be repaid between three months and three years.

Founded in 2013 and based in Reston, VA, StreetShares now employs 46 people, up from 32 last year.

Lendio Surpasses $1 Billion in Originations

October 16, 2018 Lendio announced today that it has facilitated $1 billion in financing to more than 51,000 small businesses across the U.S. since it was founded 2011. It reached the $500 million mark just a little over a year ago in July 2017.

Lendio announced today that it has facilitated $1 billion in financing to more than 51,000 small businesses across the U.S. since it was founded 2011. It reached the $500 million mark just a little over a year ago in July 2017.

“We are a marketplace, not a lender, which means we can help a lot more small business owners,” Lendio co-founder and CEO Brock Blake told AltFinanceDaily. “We can say ‘Yes’ more often because we have more options.”

Brock attributes the company’s recent growth to its marketplace business model, its team and all of its business partners. Lendio works with over 75 lenders on its platform and it also operates a turndown program where participating lenders refer to applications to Lendio that they have declined, but which might be funded by a different lender that Lendio works with.

Lendio also has about 30 franchisees that operate in 50 markers in the U.S. A market could be a single city or a handful of counties, and some franchisees cover multiple markets, according to Blake. Franchisees work with accountants, attorneys and chambers of commerce to inform local business owners about Lendio and ultimately get them to use the Lendio platform when looking for a small business loan.

Lendio has over 150 employees split between its headquarters in the Salt Lake City, Utah area and an office on Long Island.

Prior to co-founding Lendio, Blake created a company called Funding Universe, which connected entrepreneurs to venture capitalists in what he described was like speed dating. But he said that he soon realized that most American businesses need smaller amounts of capital, so he pivoted into small business lending.

“Across 75 lenders and 15 different loan products, it [can be] a challenge to really figure out which business owner fits with which loan product and to help that deal get funded,” Blake said. “But feel like over the last 18 months to 2 years we really have that process down. And now we’re gaining that flywheel effect. We’re continuing to gain more and more momentum. The ceiling is much higher and I’m really excited about the future in front of us.”

Is Your Firm Ready for Machine Learning?

October 15, 2018Artificial intelligence such as machine learning has the potential to dramatically shift the alternative lending and funding landscape. But humans still have a lot to learn about this budding field.

Across the industry, firms are at different points in terms of machine learning adoption. Some firms have begun to implement machine learning within underwriting in an attempt to curb fraud, get more complex insights into risk, make sounder funding decisions and achieve lower loss rates. Others are still in the R&D and planning stage, quietly laying the groundwork for future implementation across multiple areas of their business, including fraud prevention, underwriting, lead generation and collections.

“It’s entirely critical to the success of our business,” says Paul Gu, co-founder and head of product at Upstart, a consumer lending platform that uses machine learning extensively in its operations. “Done right, it completely changes the possibilities in terms of how accurate underwriting and verification are,” he says.

While there’s no absolute right way to implement machine learning within a lender’s or funder’s business, there are many data-related, regulatory and business-specific factors to consider. Because things can go very wrong from a business or regulatory perspective—or both—if machine learning is not implemented properly, firms need to be especially careful. Here are a few pointers that can help lead to a successful machine learning implementation:

Using machine learning, funders can predict better the likelihood of default versus a rule-based model that looks at factors such as the size of the business, the size of the loan and how old the business is, for example, says Eden Amirav, co-founder and chief executive of Lending Express, a firm that relies heavily on AI to match borrowers and funders.

Machine learning takes hundreds and hundreds of parameters into account which you would never look at with a rule-based model and searches for connections. “You can find much more complex insights using these multiple data points. It’s not something a person can do,” Amirav says.

He contends that machine learning will optimize the number of small businesses that will have access to funding because it allows funders to be more precise in their risk analyses. This will open doors for some merchants who were previously turned down based on less precise models, he predicts. To help in this effort, Lending Express recently launched a new dashboard that uses AI-driven technology to help convert business loan candidates that have been previously turned down into viable applicants. The new LendingScore™ algorithm gives businesses detailed information about how they can improve different funding factors to help them unlock new funding opportunities, Amirav says.

Lenders and funders always have to be thinking about what’s next when it comes to artificial intelligence, even if they aren’t quite ready to implement it. While using machine learning for underwriting is currently the primary focus for many firms, there are many other possible use cases for the alternative lenders and funders, according to industry participants.

Lead generation and renewals are two areas that are ripe for machine learning technology, according to Paul Sitruk, chief risk officer and chief technology officer at 6th Avenue Capital, a small business funder. He predicts that it is only a matter of time before firms are using machine learning in these areas and others. “It can be applied to several areas within our existing processes,” he says.

Collection is another area where machine learning could make the process more efficient for firms. Machines can work out, based on real-life patterns, which types of customers might benefit from call reminders and which will be a waste of time for lenders, says Sandeep Bhandari, chief strategy and chief risk officer at Affirm, which uses advanced analytics to make credit decisions.

“There are different business problems that can be solved through machine learning. Lenders sometimes get too fixated on just the approve/decline problem,” he says.

“Most underwriters don’t have enough data to effectively incorporate AI, deep learning, or machine learning tools,” says Taariq Lewis, chief executive of Aquila, a small business funder. He notes that effective research comes from the use of very large datasets that won’t fit in an excel spreadsheet for testing various hypotheses.

Problems, however, can occur when there’s too much complexity in the models and the results become too hard to understand in actionable business terms. For example, firms may use models that analyze seasonal lender performance without understanding the input assumptions, like weather impact, on certain geographies. This may lead to final results that do not make sense or are unexpected, he says.

“There’s a lot of noise in the data. There are spurious correlations. They make meaningful conclusions hard to get and hard to use,” he says.

The more precise firms can be with the data, the more predictive a machine learning model can be, says Bhandari of Affirm. So, for example, instead of looking at credit utilization ratios generally, the model might be more predictive if it includes the utilization rate over recent months in conjunction with debt balance. It’s critical to include as targeted and complete data as possible. “That’s where some of our competitive advantages come in,” Bhandari says.

Underwriters also have to pay particularly close attention that overfitting doesn’t occur. This happens when machines can perfectly predict data in your data set, but they don’t necessarily reflect real world patterns, says Gu of Upstart.

Keeping close tabs on the computer-driven models over time is also important. The model isn’t going to perform the same all along because the competitive environment changes, as do consumer preferences and behaviors. “You have to monitor what’s going well and what’s not going well all the time,” Bhandari says.

Certainly, as AI is integrated into financial services, state and federal regulators that oversee financial services are taking more of an interest. As such, firms dabbling with new technology have to be very careful that any models they are using don’t run afoul of federal Fair Lending Laws or state regulations.

“If you don’t address it early and you have a model that’s treating customers unfairly or differently, it could result in serious consequences,” says Tim Wieher, chief compliance officer and general counsel of CAN Capital, which is in the early stages of determining how to use AI within its business.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

To be sure, regulation around AI is still a very gray area since the technology is so new and it’s constantly evolving. Banking regulators in particular have been looking closely at the issues pertaining to AI such as its possible applications, short-comings, challenges and supervision. Because the waters are so untested, there can be validity in asking for regulatory and compliance advice before moving ahead full steam, some industry watchers say.

Upstart, for example, which uses AI extensively to price credit and automate the borrowing process, wanted buy-in from the Consumer Financial Protection Bureau to help ease the concern of its backers as well as to satisfy its own concerns about the legality of its efforts. So the firm submitted a no-action request to CFPB. The CFPB responded by issuing a no-action letter to Upstart in September 2017, allowing the company to use its model. In return, Upstart shares certain information with the CFPB regarding the loan applications it receives, how it decides which loans to approve, and how it will mitigate risk to consumers, as well as information on how its model expands access to credit for traditionally underserved populations.

The No-Action Letter is in force for three years and Upstart can seek to renew it if it chooses.

Theoretically firms could have a computer underwriting model constantly updating itself without having a human oversee what the model is doing—but it’s a bad idea, industry participants say. “I believe there are companies doing that, and it’s a risky thing to do,” says Scott M. Pearson, a partner with the law firm Ballard Spahr LLP in Los Angeles.

During review of the models—and before implementing them—people should carefully review the models and the output to make sure there’s nothing that causes intrinsic bias, says Kathryn Petralia, co-founder and president of Kabbage, which is one of the front-runners in using machine learning models to understand and predict business performance.

“If you’re not watching the machine, you don’t know how the machine is complying with regulatory requirements,” she says.

Kabbage has teams of data scientists regularly developing models that the company then reviews internally before deploying. The company is also in frequent contact with regulators about its processes. Petralia says it’s very important that firms be able to explain to regulators how their models work. “Machines aren’t very good at explaining things,” she quips.

As a best practice, Pearson of Ballard Spahr says lenders and funders shouldn’t use any machine learning model until it’s been signed off on by compliance. “That strikes a pretty good balance between getting the benefits of AI and making sure it doesn’t create a compliance problem for you,” he says.

While AI has many benefits, industry participants say alternative lenders and funders need to be mindful of how it can be applied practically and effectively within their particular business model.

Craig Focardi, senior analyst with consulting firm Celent in San Francisco, contends that the classic FICO score continues to be the gold standard for credit decisions in the U.S. He warns firms not to get overly distracted trying to find the next best thing.

“Many fintech lenders have immature risk management and operations functions. They’re better off improving those than dabbling in alternative scoring,” he says, noting that data modeling is an entirely separate core competency.

Indeed, Lewis of Aquila cautions underwriters not to view AI as a silver bullet. “AI is just one tool out of many in the lenders’ toolbox, and our industry should use it and respect its limitations,” he says.

The Largest Merchant Cash Advance in History

September 28, 2018 How would you like to be the funder to do a $40 million MCA transaction? According to the Securities & Exchange Commission, a deal of such magnitude was one of the many negligent acts that 1st Global Capital CEO Carl Ruderman did with investor money. Though the SEC refers to the merchant as an auto dealership in California, it’s roughly 9 dealerships with common ownership that collectively gross more than $550 million a year in sales. It’s the deal of a lifetime except that the ISO who brokered it has become the largest unsecured creditor to file a claim in the 1st Global bankruptcy. Records show they are owed approximately $3.9 million in unpaid commissions.

How would you like to be the funder to do a $40 million MCA transaction? According to the Securities & Exchange Commission, a deal of such magnitude was one of the many negligent acts that 1st Global Capital CEO Carl Ruderman did with investor money. Though the SEC refers to the merchant as an auto dealership in California, it’s roughly 9 dealerships with common ownership that collectively gross more than $550 million a year in sales. It’s the deal of a lifetime except that the ISO who brokered it has become the largest unsecured creditor to file a claim in the 1st Global bankruptcy. Records show they are owed approximately $3.9 million in unpaid commissions.

And its performance has not been without challenges, according to emails disclosed in the SEC case.

In April 2018, 1st Global employees discussed what to do about the dealerships’ lingering cash flow problems after becoming aware that the owner intended to either recapitalize the debt or sell the dealerships. The choice by then had come down to either continuing to fund them or to cut their losses, an email says.

“If they were to become insolvent, everyone loses,” wrote the Director of Accounting and Finance.

1st Global continued to fund them. The $40 million (approximate amount) was not disbursed all at once but in increments over the course of a year.

One week before 1st Global filed for bankruptcy, they signed a Binding Letter of Understanding with the dealerships acknowledging that the owner would be selling them. At that time the merchant had unpaid taxes of at least $9 million and had an outstanding receivable balance with 1st Global of $43 million. The Letter said that 1st Global would accept “whatever amount it receives [..] at this point as complete satisfaction” of the current RTR when the business is sold. 1st Global also agreed to forever release the dealerships’ owner personally from all legal claims. It was signed by Carl Ruderman 8 days before he resigned.

The merchant has not returned AltFinanceDaily’s inquiries. The banker named in the Binding Letter as having been exclusively hired to sell the dealerships, told AltFinanceDaily over the phone that he has never heard of 1st Global. 1st Global ceased operations on July 27th. The SEC filed a complaint against Ruderman and the company on August 23rd and an amended complaint on September 26th. The dealership transaction is used as an example of malfeasance in it twice.

New Record

No longer candidates for the largest merchant cash advance in history, two ancient deals that were famous during their eras for their size, ended up in default, and in doing so showed the industry that there was such a thing as too big.

One was a $4 million advance made by Strategic Funding Source in 2011 to a tourist attraction being produced at the Tropicana Hotel in Las Vegas. The Las Vegas Mob Experience, billed as the most technologically advanced interactive presentation of historical artifacts ever devised and set up in a 26,000 square foot total immersion facility, it was predicted to bring in 1.5 million visitors per year. But the deal quickly spiraled out of control, the exhibit shut down, and allegations of fraud were lodged in court. Though the Mob Experience was dubbed the largest merchant cash advance in history, it depends on whether or not you’re counting common ownership of multiple businesses as individual deals or one deal.

Dozens of advances made by Global Swift Funding in 2007 and 2008 to businesses controlled by the same west coast-based restaurateur, led to Global Swift’s demise. When the “restaurant king,” as he was known, filed for bankruptcy across all of his entities, Global Swift had outstanding future receivables with his businesses of approximately $8 million. Dan Chaon, a then representative of Global Swift, told a local newspaper at the time that the restaurateur was “a helluva sales-talk artist… he provided false financial statements, and everyone got caught up in that game.”

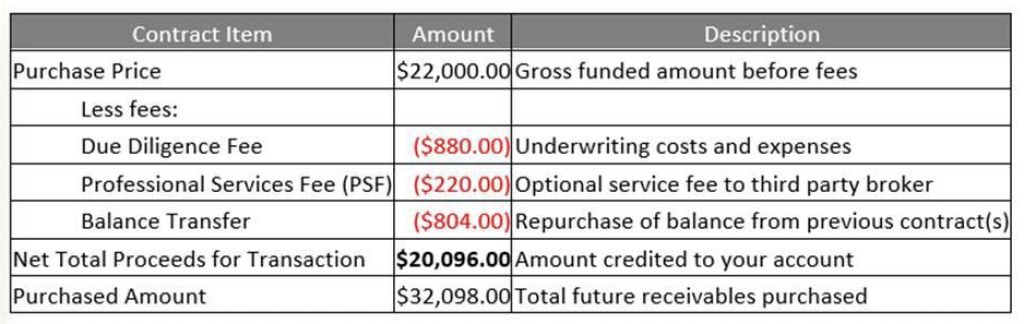

Yellowstone Capital Introduces a Smarter Box In Move Towards Transparency

September 26, 2018Yellowstone Capital CEO Isaac Stern announced a “Smarter Box” through social media channels this morning. The itemized box will be provided to merchants through a post-funding email as part of a company effort to maximize transparency.

According to the announcement:

“[We are] very serious about maximum transparency and disclosure to our funding partners’ great merchant customers. In addition to our new Purchase and Sale Agreement we will be using with each of the funding partners on our platform, we are also implementing a transaction summary email to ensure that all applicable fees, costs, disbursements and hold-backs are clearly understood by all parties. Our new contract will increase disclosure while simplifying the product, while our summary confirmation ensures greater understanding and improved communication between our funding partners and their customers.”

Example of the box:

Based in Jersey City, NJ, Yellowstone Capital has originated more than $2 billion to small businesses since inception.

In Anticipation of Hurricane Florence, Funders Suspend ACH Debits

September 12, 2018McLean, VA-based Breakout Capital is proactively suspending ACH debits for customers based in the counties designated by FEMA’s Major Disaster Declaration, according to an announcement made earlier today. They will be continuing to monitor the situation so that they can respond accordingly.

Gainesville, FL-based Elevate Funding is also pausing debits preemptively, the company says, for active merchants in North Carolina, South Carolina, and Georgia. After the storm, merchants can call in to report their damage or business status, they say. “Being based in Florida, exposed to many storms over the years, allows Elevate to understand how a hurricane’s damage can vary within 50 miles out to a 200 miles. Each case and customer will present different issues over the next week and some out to months.”

Chicago-based Lendr, echoed a similar plan. Company CEO Tim Roach says, “We will suspend payments for the rest of September for any client that is affected by Hurricane Florence. Most clients will come back on a reduced payment schedule for a short period of time. In the past we have provided additional funding for clients in need to help get their business back on track due to these types of natural disasters.”

Ft. Lauderdale-based Fundzio has announced that ACH payments are being suspended for businesses in South Carolina and North Carolina on Monday, Sept 17th through Friday, Sept 21st.

A State of Emergency has already been declared in North Carolina, South Carolina, Virginia, Washington DC, Maryland, and Georgia. It is currently a Category 3 Hurricane.

Grooming The Best Sales Reps

August 22, 2018The best sales reps have a lot in common – they’re smart, honest, likable, well-organized, thick-skinned and hungry for success. They navigate the difficult early days of their careers in the alternative small-business funding community by persevering despite long hours, countless outbound telephone calls and meager commissions.

“Persistency is really, really the key – putting in the time,” says Evan Marmott, CEO of Montreal-based CanaCap and CEO of New York-based CapCall LLC. “It’s not always easy, but you’ve got to stay late, make the phone calls, send the emails and do the follow-ups. It’s a numbers game.”

Being relentless counts not only when pursuing merchants but also when matching merchants with funders, Marmott emphasizes. “If they can’t get an approval one place, they’re going to shop it out until they get approval someplace else so they can monetize everything that comes in,” he says.

“It’s all mindset and work ethic,” in sales, according to Joe Camberato, president at Bohemia, N.Y.-based National Business Capital. His company works to create a culture that supports the right mindset by working with a firm called “Delivering Happiness.” Together, they forge to a set of core values based on integrity, innovation, teamwork, empathy, and respect for fellow employees, clients and clients’ businesses.

National Business Capital employees learn to live those ideals by working and playing together on the company volleyball team, through work with local and national charities, and at company mixers and staff picnics, Camberato maintains. “We adapt and change, and we’re committed to helping small businesses grow,” he says of the company culture, “and we have fun while doing all that.”

Likeability helps build relationships with customers, says Justin Thompson, vice president of sales for San Diego-based National Funding. “People will do business with people they like and trust,” says Thompson. “It’s really about establishing a relationship first and then establishing quality discovery.” From there, presentation and execution become paramount, he says.

Methodology can make the difference between success and failure in sales, observes Justin Bakes, co-founder and CEO of Boston-based Forward Financing LLC. “Have a defined process and stick to it,” he advises. A well-organized approach inspires trust among clients, establishes and maintains a great reputation; and fosters understanding of the customers’ needs, wants and business operations that help the rep choose the right financing option and appropriate funder. Using technology to wrangle multiple leads and high volume counts for a lot, too, he says.

It’s all part of the consultative approach to sales, says Jared Weitz, CEO of Great Neck, N.Y.-based United Capital Source. Long ago, sales reps may have succeeded by mimicking carnival barkers, sideshow pitchman and arm-twisting medicine-show peddlers. Thankfully, those days have ended – if they ever really existed. Most of today’s successful salespeople earn clients’ respect by becoming knowledgeable, trusted business consultants, says Weitz.

THE CONSULTATIVE SALE

“Someone calls, and there are two ways of handling a deal, right?” Weitz asks rhetorically. Using one method, a salesperson can say, “We’ll fund you this much at this rate today – are we good?” he says. The other way calls for understanding the client’s business – how long has it been open, does it make more cash deposits or credit card deposits, would it be best-served by an advance, a loan, an equipment lease or a line of credit, how much can it afford in monthly payments?

Establishing how the merchant intends to use the funding plays a crucial role in the consultative sale, Marmott agrees. Objections can arise when a merchant learns that receiving $100,000 this week will require paying back $150,000 in four or five months, he notes. So it’s essential to demonstrate that using the money productively will more than pay for the deal. A trucking company can realize more income if it deploys two more trucks, or a restaurant can increase revenue by placing another bar outside for the summer, he says by way of example.

“A lot of salespeople ask a business owner what they need the money for,” observes Thompson. “The merchant says, ‘Inventory,’ and the rep stops right there. I train my reps at National Funding to go two or three clicks deeper.” Examples abound. When does the merchant need the inventory? From whom do they order it? How long does it take to ship? How long does it take to turn it over? What are the shipping terms?

The consultative approach can require salespeople to pose a lot of open-ended questions that can’t be answered yes or no, according to Thompson. Ideally, the conversation should adhere to the 80-20 rule, with the client talking 80 percent of the time and the sales rep speaking 20 percent, he asserts, adding that “a lot of times it’s reversed in this industry.”

Sometimes, however, salespeople should set aside the time-consuming consultative approach and instead find funding for a merchant as soon as possible. That’s true when the business owner can make an opportune purchase of inventory or when it’s time to acquire a competitor quickly. More often, however, it pays to take the time to understand the merchant’s needs and search out the best type of funding for that particular case, top sales people maintain.

Much of the alternative small-business finance industry has caught on to the importance of the consultative approach to sales as the array of available alternative financial products has grown beyond the industry’s initial offerings of merchant cash advances, according to Weitz. The days of scripted pitches and preplanned rebuttals to objections have ended, he says. Today, management trains reps for success.

THE RIGHT TRAINING

Are top salespeople born that way? “Some people hit the ground running, but sales can be taught – that’s for sure,” Weitz says. “The tougher thing to teach is integrity.” Much of the training process focuses on learning the products to enable a rep to make a consultative sale and shoulder financial responsibility, he maintains.

Believing that some people are born to sell provides a crutch to avoid learning what really works, according to Bakes. Training can teach a smart, motivated person how to succeed, he maintains. They don’t have to be born that way.

However, some people do seem born to exert influence, which can translate into sales prowess, says Thompson. Still, those born with a strong work-ethic can overcome other deficiencies, he notes. The work ethic drives them to “come in every day,” he notes. “They’re organized and disciplined. They follow the National Funding philosophy, and they make a ton of money.”

National Funding trains salespeople to view their craft as being defined by two broad elements – art and science, Thompson continues. The science proves easier to master and includes asking the right questions to learn about the customer and the deal. The hard part, the art of the sale, consists of getting to know the business owner, building a relationship and demonstrating expertise. In one example, that’s based on learning how many trucks are in the fleet, whether they’re long-haul or short haul and whether they use dumpsters versus box trailers, he says.

Beyond those important basics, training should be ongoing because selling techniques change slightly as new products and systems emerge, according to Weitz. “One of the things I like about being a broker is the ability to pivot and add another arrow to your quiver,” he says.

Salespeople at United Capital Source talk sales among themselves almost nonstop, which amounts to daily sales training, Weitz observes. That can take the form of describing a challenge and explaining how to overcome it, he notes. A particularly good idea merits an email to the group to share the new piece of wisdom. It’s a matter of constantly refining the approach.

Training can help sales reps understand the businesses their clients run, according to Marmott. Knowing the margins in a restaurant, for example, can help the salesperson explain that the increase in revenue from an expansion will quickly pay the cost of capital, he notes.

Training should teach new employees how business works because common elements arise in enterprises ranging from dog grooming to asphalt paving, Thompson notes. There’s inventory, marketing, employee expense, payroll taxes, insurance and 401k’s in almost any business. “We teach all that to the reps,” he says. Then after conversations with thousands of merchants, reps have a solid foundation in the workings of businesses.

National Business Capital’s formal two-week classroom training usually lasts three hours a day, focusing on systems, guidelines, product, general business principles and the company’s processes, says Camberato. Teachers include the sales management team, company culture leaders and the managers of IT and Tech, Marketing, Processing, and Human Resources.

National Business Capital’s formal two-week classroom training usually lasts three hours a day, focusing on systems, guidelines, product, general business principles and the company’s processes, says Camberato. Teachers include the sales management team, company culture leaders and the managers of IT and Tech, Marketing, Processing, and Human Resources.

New hires spend much of their time working with mentors for the first six months and a team leader who works with them indefinitely, Camberto continues. The company sometimes hires in groups and sometimes hires individually, he notes.

National Funding provides three eight-hour days of regimented classroom training on the fundamentals to each of the four groups of 12 to 17 hired each year, says Thompson. The classes cover processes, sales strategy, marketing and the lender matrix. Next comes three months of working with a sales manager dedicated to working with the class. After a total of nine to 12 months, management knows which reps will succeed.

Some shops operate on the opener-closer model, with less experienced salespeople qualifying the merchant by asking questions like how long they’re been in business and how much revenue they bring in monthly, Marmott says. If the merchant qualifies, the newer salesperson who’s working as an opener then hands off the call to an experienced closer to complete the deal. Good openers become closers, but opening isn’t easy because it requires lots of calls, he notes.

National Funding doesn’t use the opener-closer approach because the company believes reps should Participate “from cradle to grave,” Thompson says. “They hunt the business down, build the relationship and handle the transaction from A to Z.” East Coast shops often focus on cold calling and use the opener-closer model, while West Coast shops tend to invest more in marketing and reject the opener-closer method, he noted.

But where do these top salespeople come from?

THE RIGHT BACKGROUND

Prospective sales reps who have just finished college should have a grounding in communications or business, Weitz believes. Experience in sales and a familiarity with dealing with merchants helps prepare reps, he notes. Job history doesn’t have to be in the finance industry. Someone who’s sold business services in a Verizon store or worked for a payroll company, for instance, has been dealing with small-business owners and may succeed more quickly than those without that background.

Sales experience in other industries counts, Bakes agrees, especially in businesses that require dealing with a large number of leads. “Organization and process is just as important as being born with the traits of a salesperson,” he opines.

Life experience that breeds a positive attitude can prove vital, says Marmott. That’s especially important in the beginning when a new rep might take home a paltry $300 in the first month. Later, when the rep has a $50,000 month, he or she will see that their optimism wasn’t misplaced, he declares.

GUYS WHO ARE HUNGRY”

“The biggest thing I look for is guys who are hungry,” Marmott maintains. I don’t need somebody with a doctorate or a master’s degree or even a degree,” he says. “I need somebody who is going to put the work in.” Of a roomful of 25 new reps, two or three will succeed and stay on the job, he calculates. “You get to eat what you kill. If you’re not killing anything, you don’t get to eat.”

“We look for potential candidates who come from backgrounds of rejection,” says Thompson. Their previous sales experience has taught them not to take the answer “no” personally. “It’s part of the business and you continue to move on.”

Although most regard the financial services industry as a white-collar pursuit, “it has blue collar written all over it,” Thompson says, referring to the work ethic required for success. But it’s not just the volume of work. Sixty good phone calls generate more business than 300 mediocre calls, he emphasizes.

GETTING UP TO SPEED

Succeeding at sales requires taking the time to form relationships, understand guidelines, become familiar with lenders and acquire a working knowledge of how clients’ businesses operate, Camberato says. How long does it take? “It’s a solid year,” he contends while conceding that most who succeed operate at a fairly high level before then.

Others disagree about what constitutes being up to speed and how much time’s necessary to achieve it. “I’ve seen it take 30 days, and I’ve seen it up to 120 days,” says Weitz. “The hope is that it’s within 60.”

A salesperson should start feeling better after 30 days and should start feeling good after 60 days, Marmott says. Management can usually identify the strong and the week reps within two to three weeks, he says. “You get the lazy ones that drop out, the guys who aren’t making any money, the ones who aren’t putting the effort in,” he says. “The first two weeks are the toughest because you’re learning the product and how to sell it.”

“It depends on the person,” Bakes says of the time needed to begin selling successfully. “It takes time. It is not something that will just happen overnight.” About six months should suffice to become confident as a closer, he estimates.

Even when sales reps hit their stride, some outsell others, Marmott notes, citing the 80-20 rule that 80 percent of the business comes from 20 percent of the salesforce. Outbound sales to merchants who may feel beleaguered by offers of funding requires more effort than when a merchant makes an inbound call to seek funding, he adds.

And even the best salespeople need great marketing and tech support from the their companies, sources agree.

INVESTING IN SALES

A shop just starting out might have a marketing budget as low as $2,500 a month, which won’t do much more than pay for direct mail pieces that might prompt a few potential clients to pick up the phone, Weitz says. With a little more money to spend, a shop can begin buying leads, he notes. “Don’t break the bank before you understand what formula works for you,” he advises.

“The key to sales is marketing,” says Marmott. “You can be the best sales guy but if you don’t have anything qualified to call or follow up with, it’s a waste of time.” Social media doesn’t work as well for business-to-business contact as it does for business-to-consumer marketing, he says. Pay per click and key words have become more expensive and isn’t as cost-effective as it once was, especially for smaller shops, he contends. Mailers can work but require heavy volume and repetition, he says, adding that could mean at least 25,000 pieces and at least three mailings.

Besides allocating marketing dollars, companies can invest in sales by paying new sales staffers a salary instead of forcing them to rely on commissions to eke out subsistence during the tough early days. National Business Capital pays a salary at first and later switches reps to commissions and draw, Camberato says. “An energetic person interested in sales can plug into our platform, get trained and do very well,” he continues. “We believe in you, as long as you believe in us.”

National Funding provides recruits with a salary and commissions so that they have enough income to get by and still reap rewards when they help close a deal, Thompson says.

Investment in technology can help salespeople set priorities, eliminate some of the drudge work in the sale process, measure the sales staff member’s success or lack of success, and provide a consistent experience for customers, notes Bakes. “Because of the way our technology is set up we can hold people accountable,” he adds.

Every salesperson and every shop should organize the workflow by using a lead-management system or customer relationship management tool (CRM) – such as Zoho or Salesforce –instead of operating with just a spreadsheet, Weitz says.

Brokers can invest in sales through syndication, which means putting up some of the funds involved in a deal. Forward Financing favors syndication in some cases because it aligns the salesperson and the funder, thus demonstrating the sales rep’s belief in the validity of the deal and ensuring a willingness to continue servicing that customer, Bakes says.

Some shops offer monthly bonuses for outstanding sales results, but Weitz believes awarding incentives weekly makes more sense. With a monthly cycle, some reps tend to slack off for the first week or so because they believe they can make up for lost time later. With weekly rewards, there’s not much room for downtime, he notes.

Whatever form investment takes, it can help build a sterling reputation and a free-flowing “pipeline.”

THE RIGHT REPUTATION

“Reputation is huge,” especially for repeat business and referrals, Marmott says. Once a merchant has received funding, a blizzard of sales call can follow. Treating customers right by maintaining ethical standards and helping them during hard times can guard against defection to a competitor touing low prices, he says.

Reputation requires differentiation, which usually occurs online, by email or over the phone, notes Bakes. Factors that enhance reputation include referrals by satisfied customers and real-world testimonials from actual customers and good ratings on social media sites, he says.

While it’s still uncertain what role social media plays in the industry’s reputation-building efforts, it appears that text messages elicit quick responses if the client has agreed to communicate with the company via that format, Bakes says. He notes that unwanted text messages won’t work. Email messages provide more information than text messages but seem less likely to prompt response, he says.

THE RIGHT GOAL

So, where does the effort to succeed at sales lead? It’s the foundation for building “the pipeline” – the name given to the flow of renewals, referrals and leads that makes every day not just busy, but busy in a productive and profitable way. As a rep’s pipeline takes shape, the cost of acquiring new business also goes down, Marmott says. “It just grows from there,” he says of the successful salesperson’s endeavors at building a pipeline of business. It’s what successful salespeople seek.

The Seven-Minute Loan Shakes Up Washington And The 50 States

August 19, 2018 It takes seven minutes for Kabbage to approve a small-business loan. “The reason there’s so little lag time,” says Sam Taussig, head of global policy at the Atlanta-based financial technology firm, “is that it’s all automated. Our marginal cost for loans is very low,” he explains, “because everything involving the intake of information – your name and address, know-your-customer, anti-money-laundering and anti-terrorism checks, analyzing three years of income statements, cash-flow analysis – is one-hundred-percent automated. There are no people involved unless red flags go off.”

It takes seven minutes for Kabbage to approve a small-business loan. “The reason there’s so little lag time,” says Sam Taussig, head of global policy at the Atlanta-based financial technology firm, “is that it’s all automated. Our marginal cost for loans is very low,” he explains, “because everything involving the intake of information – your name and address, know-your-customer, anti-money-laundering and anti-terrorism checks, analyzing three years of income statements, cash-flow analysis – is one-hundred-percent automated. There are no people involved unless red flags go off.”

One salient testament to Kabbage’s automation: Fully $1 billion of the $5 billion in loans that it has made to 145,000 discrete borrowers since it opened its portals in 2011 were made between 6 p.m. and 6 a.m.

Now compare that hair-trigger response time and 24-hour service for a small business loan of $1,000-$250,000 with what occurs at a typical bank. “Corporate credit underwriting requires 28 separate tasks to arrive at a decision,” William Phelan, president, and co‐founder of PayNet—a top provider of small-business credit data and analysis – testified recently to a Congressional subcommittee. “These 28 tasks involve (among other things): collecting information for the credit application, reviewing the financial information, data entry and calculations, industry analysis, evaluation of borrower capability, capacity (to repay), and valuation of collateral.”

A “time-series analysis,” the Skokie (Ill.)-based executive went on, found that it takes two-to-three weeks – and often as many as eight weeks—to complete the loan approval process. For this “single credit decision,” Phelan added, the services of three bank departments – relationship manager, credit analyst, and credit committee – are required.

The cost of such a labor-intensive operation? PayNet analysts reckoned that banks incur $4,000-$6,000 in underwriting expenses for each credit application. Phelan said, moreover, that credit underwriting typically includes a subsequent loan review, which consumes two days of effort and costs the bank an additional $1,000. “With these costs,” Phelan told lawmakers, “banks are unable to turn a profit unless the loan size exceeds $500,000.”

According to the National Bureau of Economic Research, the country’s very biggest banks — Bank of America, Citigroup, J.P. Morgan Chase, and Wells Fargo—have been the financial institutions most likely to shut down lending to small businesses. “While small business lending declined at all banks beginning in 2008,” NBER’s September, 2017 report announces, “the four largest banks” which the report dubs the ‘Top Four’—“cut back significantly relative to the rest of the banking sector.”

NBER reports further that by 2010—the “trough” of the financial crisis—the annual flow of loan originations from the Top Four stood at just 41% of its 2006 level, which compared with 66% of the pre-crisis level for all other banks. Moreover, small-business lending at the “Top Four” banks remained suppressed for several years afterward, “hovering” at roughly 50% of its pre crisis level through 2014. By contrast, such lending at the rest of the country’s banks eventually bounced back to nearly 80% of the pre-crisis level by 2014.

That pullback—by all banks—continues, says Kenneth Singleton, an economics professor at Stanford University’s Graduate School of Business. Echoing Phelan’s testimony, Singleton told AltFinanceDaily in an interview: “Given the high underwriting costs, banks just chose not to make loans under $250,000,” which are the bread-and-butter of small-business loans. In so doing, he adds, banks “have created a vacuum for fintechs.”

All of which helps explain why Kabbage and other fintechs making small business loans are maintaining a strong growth trajectory. As a Federal Reserve report issued in June notes, the five most prominent fintech lenders to small businesses—OnDeck, Kabbage, Credibly, Square Capital, and PayPal—are on track to grow by an estimated 21.5 percent annually through 2021.

Their outsized growth is just one piece—albeit a major one—of fintech’s larger tapestry. Depending on how you define “financial technology,” there are anywhere from 1,400 to 2,000 fintechs operating in the U.S., experts say. Fintech companies are now engaged in online payments, consumer lending, savings and investment vehicles, insurance, and myriad other forms of financial services.

Fintechs’ advocates—a loose confederacy that includes not only industry practitioners but also investors, analysts, academics, and sympathetic government officials—assert that the U.S. fintech industry is nonetheless being blunted from realizing its full potential. If fintechs were allowed to “do their thing,” (as they said in the sixties) this cohort argues, a supercharged industry would bring “financial inclusion” to “unbanked” and “underbanked” populations in the U.S. By “democratizing access to capital,” as Kabbage’s Taussig puts it, harnessing technology would also re-energize the country’s small businesses, which creates the majority of net new jobs in the U.S., according to the U.S. Small Business Administration.

But standing in the way of both innovation and more robust economic growth, this cohort asserts, is a breathtakingly complex—and restrictive—regulatory system that dates back to the Civil War. “I do think we’re victims of our own success in that we’ve got a pretty good financial system and a pretty good regulatory structure where most people can make payments and the vast majority of people can get credit.” says Jo Ann Barefoot, chief executive at Barefoot Innovation Group in Washington, D.C. and a former senior fellow at Harvard’s Kennedy School. But because of that “there’s been more inertia and slower adoption of new technology,” she adds. “People in the U.S. are still going to bank branches more than people in the rest of the world.”

Barefoot adds: “There are five agencies directly overseeing financial services at the Federal level and another two dozen federal agencies” providing some measure of additional, if not duplicative oversight, over financial services. “But there’s no fintech licensing at the national level,” she says. And because each state also has a bank regulator, she notes, “if you’re a fintech innovator, you have to go state by state and spend millions of dollars and take years” to comply with a spool of red tape pertaining to nonbanks.

At the federal level, the current system— which includes the Federal Reserve, Office of the Comptroller of the Currency (OCC), and the Federal Deposit Insurance Corporation (FDIC)—developed over time in a piecemeal fashion, largely through legislative responses to economic panics, shocks and emergencies. “For historical reasons,” Barefoot remarks, “we have a lot of agencies” regulating financial services.

For exhibit A, look no further than the Consumer Financial Protection Bureau created amidst the shambles of the 2008-2009 financial crisis by the 2010 Dodd-Frank Act. Built ostensibly to preserve safety and soundness, the agencies have constructed a moat around the banking system.

Karen Shaw Petrou, managing partner at Federal Financial Analytics, a Washington, D.C. consultancy, is a banking policy expert who frequently provides testimony to Congress and regulatory agencies. She wrote recently that the country’s banking sector has been protected from the kind of technological disruption that has upended a whole bevy of industries.

“The only reason Amazon and its ilk may not do to banking, brokers and insurers what they did to retailers—and are about to do to grocers and pharmacies,” she observed recently in a blog—“is the regulatory structure of each of these businesses. If and how it changes are the most critical strategic factors now facing finance.”

Cornelius Hurley, a Boston University law professor and executive director of the Online Lending Policy Institute, is especially critical of the 50-state, dual banking system. State bank regulators oversee 75 percent of the country’s banks and are the primary regulators of nonbank financial technology companies. “The U.S. is falling behind other countries that are much less balkanized,” Hurley says. “Our federal system of government has served us well in many areas in our becoming a leading civil society. It’s given us NOW (Negotiable Order of Withdrawal) accounts, money-market accounts, automatic teller machines, and interstate banking. But now it’s outlived its usefulness and has become an impediment.”

Take Kabbage, which actually avoids a lot of regulatory rigmarole by virtue of its partnership with Celtic Bank, a Utah-chartered industrial bank. The association with a regulated state bank essentially provides Kabbage with a passport to conduct business across state lines. Nonetheless, Kabbage has multiple, incessant, and confusing dealings with its bank overseers in the 50 states.

“Where the states get involved,” says Taussig, “is on brokering, solicitation, disclosure and privacy. We run into varying degrees of state legislative issues that make it hard to do business. Right now we’re plagued by what’s been happening with national technology actors on cybersecurity breaches and breach disclosures. We are required to notify customers. But some states require that we do it in as few as 36 hours, and in others it’s a couple of months. We’ve lobbied for a national breach law of four days,” he adds, which would “make it easier for everyone operating across the country.”

Then there’s the meaning of “What is a broker?’” says Taussig, who as a regulatory compliance expert at Kabbage sees his role as something of an emissary and educator to regulators and politicians, the news media, and the public. “The definitions haven’t been updated since the 1950s and now we have wildly different interpretations of brokering and solicitation,” he says. “The landscape has changed with e-commerce and each state has a different perspective of what’s kosher on the Internet.”

Washington State is a good example. It’s one of a handful of jurisdictions in which regulators confine nonbank fintechs to making consumer loans. In a kabuki dance, fintech companies apply for a consumer-lending license and then ask for a special dispensation to do small-business lending.

And let’s not forget New Mexico, Nevada and Vermont where a physical “brick-and-mortar” presence is required for a lender to do business. Digital companies, Taussig says, would have to seek a waiver from regulators in those states. “Many companies spend a lot of money on billable hours for local lawyers to comply with policies and procedures,” Taussig reports, “and it doesn’t serve to protect customers. It’s really just revenue extraction.”

All such restraints put fintechs at a disadvantage to traditional financial institutions, which by virtue of a bank charter, enjoy laws guaranteeing parity between state-chartered and federally chartered national banks. The banks are therefore able to traverse state lines seamlessly to take deposits, make loans, and engage in other lines of business. In addition, fintechs’ cost of funds is far higher than banks, which pay depositors a meager interest rate. And banks have access to the Fed discount window, while their depositors’ savings and checking accounts are insured up to $200,000.

The result is a higher cost of funds for fintechs, which principally depend on venture capital, private equity, securitization and debt financing as well as retained earnings. And that translates into steeper charges for small business borrowers. A fintech customer can easily pay an interest rate on a loan or line of credit that’s three to four times higher than, say, a bank loan backed by the U.S. Small Business Administration.

Kabbage, for example, reports that its average loan of roughly $10,000 typically carries an interest rate of 35%-36%. It’s credits are, of course, riskier than the banks’. The company does not report figures on loans denied, Taussig told AltFinanceDaily, but Stanford’s Singleton says that the fintech industry’s denial rate is roughly 50 percent for small business loans. “Fintechs have higher costs of capital and they’re also facing moderate default rates,” notes Singleton. “They’re not enormous, but fintechs are dealing with a different segment. Small businesses have much more variability in cash flows, so lending could be riskier than larger, established companies.”

Even so, venture capitalists continue to pour money into fintech start-ups. “I’ve gone to several conferences,” Singleton says, “and everywhere I turn I’m meeting people from a new fintech company. One of the striking things about this space,” he adds, “is that there are lot of aspiring start-ups attacking very specific, very narrow issues. Not all will survive, but someone will probably acquire them.”

Even so, venture capitalists continue to pour money into fintech start-ups. “I’ve gone to several conferences,” Singleton says, “and everywhere I turn I’m meeting people from a new fintech company. One of the striking things about this space,” he adds, “is that there are lot of aspiring start-ups attacking very specific, very narrow issues. Not all will survive, but someone will probably acquire them.”

Contrast that to the world of banking. Many banks are wholeheartedly embracing technology by collaborating with fintechs, acquiring start-ups with promising technology, or developing in-house solutions. Among the most impressive are super-regionals Fifth Third Bank ($142.2 billion), Regions Financial Corp. ($123.5 billion), and BBVA Compass ($69.6 billion), notes Miami-based bank consultant Charles Wendel. But many banks are content to cater to familiar customers and remain complacent. One result is that there’s been a steady diminution in the number of U.S. banks.

Over the past ten years, fully one-third of the country’s banks were swallowed whole in an acquisition, disappeared in a merger, failed, or otherwise closed their doors. There were 5,670 federally insured banks at the end of 2017, according to the Federal Deposit Insurance Corp., a 2,863-bank, 33.5% decrease from the 8,533 commercial banks operating in the U.S. in 2007.

It does appear that, to paraphrase an old expression, many banks “are going out of style.” In recent years there have been more banking industry deaths than births. Sixty-three banks have failed since 2013 through June while only 14 de novo banks have been launched. In Texas, which is known for having the most banks of any state in the country, only one newly minted bank debuted since 2009. (The Bank of Austin is the new kid on the Texas block, opening in a city known as a hotbed of technology with its “Silicon Hills.”)

One reason there’s so little enthusiasm among venture capitalists and other financial backers for investing in de novo banks is that regulators are known to be austere. “If you’re a company in the U.S.,” says Matt Burton, a founder of data analytics firm Orchard Platform Markets (which was recently acquired by Kabbage), “and you tell regulators that you want to grow by 100 percent a year – which is the scale you must grow at to get venture-capital funding – regulators will freak out. Bank regulators are very, very strict. That’s why you never hear about new banks achieving any sort of scale.”

But while bank regulators “are moving sluggishly compared to the rest of the world” in adapting to the fintech revolution, says Singleton, there are numerous signs that the status quo may be in for a surprising jolt. The Treasury Department is about to issue (possibly by the time this story is published) a major report recommending an across-the-board overhaul in the regulatory stance toward all nonbank financials, including fintechs. According to a report in The American Banker, Craig Phillips, counselor to Treasury Secretary Steven Mnuchin, told a trade group that the report would address regulatory shortcomings and especially “regulatory asymmetries” between fintech firms and regulated financial institutions.

Christopher Cole, senior regulatory counsel at the Independent Community Bankers Association—a Washington, D.C. trade association representing the country’s Main Street bankers—told AltFinanceDaily that, among other things, the Treasury report would likely recommend “regulatory sandboxes.” (A regulatory sandbox allows businesses to experiment with innovative products, services, and business models in the marketplace, usually for a specified period of time.)

That’s an idea that fintech proponents have been drumming enthusiastically since it was pioneered in the U.K. a few years ago, and it’s something that the independent bankers’ lobby, whose member banks are among the most threatened by fintech small-business lenders, says it too can support. Treasury’s Phillips “has said in the past that he’d like to see a level playing field,” the ICBA’s Cole says. “So if (regulators) are going to allow a sandbox, any company could be involved, including a community bank. We agree with him, of course, because we’d like to take advantage of that.”

In March, 2018, Arizona became the first state to establish a regulatory sandbox when the governor signed a law directing that state’s attorney general (and not the state’s banking regulator) to oversee the program. The agency will begin taking applications in August with approval in 90 days, says Paul Watkins, civil litigation chief in the AG’s office. Watkins told AltFinanceDaily that he’s been most surprised so far by “the degree of enthusiasm” from overseas companies. With the advent of the sandbox, he adds, “Landlocked Arizona has become a port state.”

The OCC, which is part of the Treasury Department, may also revive its plan to issue a national bank charter to fintechs, sources say (EDITOR’S NOTE: This had not yet been implemented before this story went to print. The OCC is now accepting such applications) – a hugely controversial proposal that was put on ice last year (and some thought left for dead) when former Commissioner Thomas J. Curry’s tenure ended last spring. At his departure, the fintech bank charter faced a lawsuit filed by both the New York State Banking Department and the Conference of State Bank Supervisors. (Since then, the lawsuit was tossed out by the courts on the ground that the case was not “ripe” – that is, it was too soon for plaintiffs to show injury).

The OCC, which is part of the Treasury Department, may also revive its plan to issue a national bank charter to fintechs, sources say (EDITOR’S NOTE: This had not yet been implemented before this story went to print. The OCC is now accepting such applications) – a hugely controversial proposal that was put on ice last year (and some thought left for dead) when former Commissioner Thomas J. Curry’s tenure ended last spring. At his departure, the fintech bank charter faced a lawsuit filed by both the New York State Banking Department and the Conference of State Bank Supervisors. (Since then, the lawsuit was tossed out by the courts on the ground that the case was not “ripe” – that is, it was too soon for plaintiffs to show injury).

Taussig, the regulatory expert at Kabbage, reports that the Comptroller of the Currency, Robert J. Otting, has promised “a thumbs-up or thumbs-down” decision by the end of July or early August on issuing fintechs a national bank charter. He counts himself as “hopeful” that OCC’s decision will see both of the regulator’s thumbs pointing north.

The Conference of State Bank Supervisors, meanwhile, has extended an olive branch to the fintech community in the form of “Vision 2020.” CSBS touts the program as “an initiative to modernize state regulation of non-bank financial companies.” As part of Vision 2020, CSBS formed a 21-member “Fintech Industry Advisory Panel” with a recognizable roster of industry stalwarts: small business lenders Kabbage and OnDeck Capital are on board, as are consumer lenders like Funding Circle, LendUp and SoFi Lending Corp. The panel also boasts such heavyweights in payments as Amazon and Microsoft.

Working closely with the fintech industry is a “key component” of Vision 2020, Margaret Liu, deputy general counsel at CSBS, told AltFinanceDaily in a recent telephone interview. CSBS and the fintech industry are “having a dialogue,” she says, “and we’re asking industry to work together (with us) and bring us a handful of top recommendations on what states can do to improve regulation of nonbanks in licensing, regulations, and examinations.

“We want to know,” she added, ‘What the main friction points are so that we can find a path forward. We want to hear their concerns and talk about pain points. We want them to know the states are not deaf and blind to their concerns.”