GOING NATIONAL: How David Gilbert Built One of the Largest Small Business Lenders in the Country

October 17, 2018 When Ty Austin, who owns a florist shop in West Palm Beach, secured a $5,000 loan from National Funding last year, he was happy to have working capital and could build inventory for mini-gardens and landscaping,

When Ty Austin, who owns a florist shop in West Palm Beach, secured a $5,000 loan from National Funding last year, he was happy to have working capital and could build inventory for mini-gardens and landscaping,

The experience, moreover, was surprisingly pleasant. “The guy I worked with was really cool,” Austin says, referring to the sales representative at the San Diego-based financial technology firm. “It turned out that he was getting married and I ended up giving him and his fiancé advice on floral arrangements.”

The borrowing worked out so well that the Floridian, who is 46 and the sole proprietor of Austintatious Designs, re-upped for a second loan of $12,000 to help purchase a commercial van. The van will be used to transport flowers, plants and tools while doubling as a billboard-on-wheels. “It gives me more ‘street cred,’” he jokes.

To register his approval with National Funding, Austin went online to TrustPilot and posted a rave review of the sales rep: “James Johnson Rocks!”

Pam, a Texas wellness coach who provides clients with an array of holistic health therapies, needed extra money to buy an infrared sauna to add to her portfolio of services. But her credit rating was “poor,” she told AltFinanceDaily in an e-mail interview, “from when I changed careers and lost my health and struggled to make my credit card and student loan payments on time.”

Like Austin, Pam — who asks to be identified by her first name —found National Funding through an online search. And she too secured $5,000, although her transaction was structured as a merchant cash advance, rather than a loan. The terms of the MCA require a daily debit from her bank account. She reckons that the total cost of the MCA to be roughly $1,500.

Pam pronounces herself satisfied with the deal and mightily impressed with the way National Funding treated her. The process took about three days — and would have gone even quicker if she’d located her professional licenses sooner. Best of all, she says, the agent at the company tailored the financing to suit her circumstances. “They were great as far as getting my questions answered, even listening to my past situation, which others may not have cared about,” she says.

Pam pronounces herself satisfied with the deal and mightily impressed with the way National Funding treated her. The process took about three days — and would have gone even quicker if she’d located her professional licenses sooner. Best of all, she says, the agent at the company tailored the financing to suit her circumstances. “They were great as far as getting my questions answered, even listening to my past situation, which others may not have cared about,” she says.

“They really wanted to get me an option that they knew I’d be able to repay,” Pam adds. “They said they were in the business of helping small businesses grow rather than putting them in a hard financial situation.”

The positive experiences that Austin and Pam had with National Funding are not isolated instances. Rather, they are representative of clients’ dealings with the company. Witness its online reviews from business borrowers at TrustPilot which go back three years, run for 36 pages, and merit National Funding a 9.4 rating on a scale of 10. That’s a straight-A grade on any report card. Although there’s the occasional naysayer — four percent assert that their experience was “poor” or “bad” (and some negative comments can be blistering) — the weight of the reviews is almost embarrassingly positive.

Typical postings find that National Funding and its agents win kudos for, among other things, being “prompt and professional,” providing service that is “hassle free and about as friendly as you can be,” and even being “accommodating and gracious.” A man named Al McCullough spoke for many when he declared: “My experience was great. Professional and on time. Couldn’t ask for more.”

All of which helps account for why National Funding — its 230 employees working out of a sleek suburban office building guarded by a tall stand of palm trees in San Diego — is a rising star in the world of alternative business lending and financial technology. In 2017, the company raked in $94.5 million in revenues, a 24.8 percent bounce over the $75.7 million recorded a year earlier and nearly fourfold the $26.7 million posted in 2013.

All of which helps account for why National Funding — its 230 employees working out of a sleek suburban office building guarded by a tall stand of palm trees in San Diego — is a rising star in the world of alternative business lending and financial technology. In 2017, the company raked in $94.5 million in revenues, a 24.8 percent bounce over the $75.7 million recorded a year earlier and nearly fourfold the $26.7 million posted in 2013.

In recognition of the company’s three-year growth rate of 142%, Inc. magazine included National Funding in its current list of the country’s 5,000 fastest-growing companies, the lender’s sixth straight appearance on the coveted roster. Since its inception in 1999, National Funding reports that it has originated more than $2 billion in loans to some 35,000 borrowers.

The company’s impressive performance has similarly merited accolades for David Gilbert, the 43-year-old chief executive who started the company on little more than a shoestring and whom employees regularly describe as “visionary.” Among Gilbert’s trophies: Accounting firm Ernst & Young recently presented him with its “Entrepreneur of the Year 2017 Award” for San Diego finance.

At first glance, the San Diego financier doesn’t look too much different from its cohorts. The company proffers unsecured loans of $5,000 to $500,000 to a mélange of small businesses in all 50 states and across multiple industries, including retail stores, auto repair shops, truckers, construction companies, heating-and plumbing contractors, spas and beauty salons, cafes and restaurants, waste management, medical and dental clinics, and insurance agencies.

To qualify for financing, a prospective borrower should have been in business for a year, have at least $100,000 in revenues, and boast a personal credit score of at least 500. While there’s no collateral required for loans, National Funding insists on a personal guarantee. The website reviewer NerdWallet cautions borrowers that this “puts your personal assets and credit at risk if you fail to repay the loan.”

Along with unsecured loans, National Funding offers equipment leasing – usually for heavy trucks and construction equipment – as well as merchant cash advances. The equipment lease is secured by the machinery. As in the case of Pam, the wellness coach cited above, MCAs are debited daily, the money automatically withdrawn from bank accounts.

There are a number of businesses that National Funding disdains, no matter how stellar their credit. “We won’t finance casinos, strip bars, tobacco, or firearms,” Gilbert says. “We’re not going to support industries like that.”

For CEO Gilbert, doing business ethically is a signature feature of the company. Among other things, National Funding presses its salespeople to steer clear of putting people into dodgy loans that are likely to default. “We’re lending capital,” Gilbert says, “and one of our core values is the way we support our customers. Are we placing people with the right product to meet their needs or are we being selfish? The best way to be customer oriented is to get a better understanding of what capital will do for them.”

That corporate ethos, coupled with the company’s remarkable performance, has raised its profile while earning it a measure of esteem among industry peers. “What I do know about National Funding,” says Douglas Rovello, senior managing partner at Fund Simple, a lender and broker in the Tampa area, “is that they have five or six different programs and set their rates high but competitively. They’re known for fitting their products to a client’s needs,” he adds. “And in a business that has its share of bad actors, they have a reputation as a company with a conscience.”

A company with a conscience. Customers come first. And yet National Funding turns heads with its sales production of roughly 1,000 financings a month and triple-digit growth rate. So how do they it? A good place to start is with Gilbert, whose leadership skills, business acumen, and second-to-none work ethic “set the tone,” says Kevin Bryla, the company’s 52-year-old chief marketing officer.

For his part, Gilbert credits his family background and an upbringing in which education and academic achievement were strongly encouraged. The fifth of six children, he’s the only one who opted for a business career. “There are three doctors, two lawyers – and me,” Gilbert says.

The son of a prominent physician, his mother a homemaker and volunteer docent at the nearby Nixon Library for the past 25 years, Gilbert grew up in Yorba Linda. He attributes his keen interest in business to observing how his father, a pathologist, operated his own laboratory, which employed 60 people. “It was the business side of medicine that fascinated me,” he asserts.

The son of a prominent physician, his mother a homemaker and volunteer docent at the nearby Nixon Library for the past 25 years, Gilbert grew up in Yorba Linda. He attributes his keen interest in business to observing how his father, a pathologist, operated his own laboratory, which employed 60 people. “It was the business side of medicine that fascinated me,” he asserts.

Even so, his two closest friends at the University of Southern California — fraternity brothers Marc Newburger and Sean Swerdlow– tell a somewhat different story. They remember Gilbert as someone who found his true calling, his métier, during his college years. Enrolled initially in pre-med courses, he was a diligent student but, his friends assert, manifestly unsuited for a career in medicine.

“Formative,” says Swerdlow, the older of the two fraternity brothers and now a management consultant based in Southern California, “would be a very good word” to characterize that period during which Gilbert abandoned medicine in favor of the world of commerce. In 1997, he earned a bachelor’s degree in business administration “with an emphasis in entrepreneurship.”

But it was fraternity life just as much as the classroom, his friends agree, that shaped him and foreshadowed his future. “It wasn’t ‘Animal House,’” Swerdlow says of Alpha Epsilon Pi. “We boasted the highest GPA (grade point average) on fraternity row.”

Nonetheless, Gilbert took to the social life and camaraderie that the fraternity offered with gusto, and his friendship with the colorful Newburger was especially fateful. A freewheeling entrepreneur today, Newburger takes a measure of credit — Gilbert’s disapproving parents might have preferred the word “blame” — for contributing to his fraternity brother’s metamorphosis. “Dave hated all of his pre-med classes,” Newburger insists. “He had zero stomach for it. He was so much like I was: a natural people person and a born entrepreneur.”

Newburger is the quintessential soldier of fortune. After college, he tried his hand as an actor, supporting himself by playing poker and getting paid to be a contestant on TV game shows including “The Dating Game,” “Card Sharks,” and “3’s A Crowd.” He’s now the co-president and co-inventor of Drop Stop, a patented device that “minds the gap” between a car’s front seat and the console and prevents coins, keys, glasses, and mobile phones from disappearing down that rabbit hole. (Drop Stop really took off after Newburger and his business partner appeared on the television show “Shark Tank” and scored a $300,000 capital injection from celebrity-investor Lori Greiner who took a 30% stake in the company and slapped her name on the brand.)

Back at the frat house, Newburger and Gilbert collaborated on business ventures. The pair once sold T-shirts sporting an off-color message about USC’s archrival, the University of California at Los Angeles. “The (anti-UCLA) message was pure hatred,” Newburger recalls. “But it was just for the day of the football game and it was all in fun.”

At first, sales at the stadium were lackluster. USC students kept trying to bid down the price or importune them to throw in an extra tee. As for the game itself, USC’s chances for victory looked equally unpromising. As time ran out, however, the Trojan quarterback completed a Hail Mary pass and USC won. The two fraternity brothers grabbed the bundle of shirts and sprang into action. “We got to the exit just in time and sold out in a matter of seconds,” Newburger recalls.

Newburger takes credit too for introducing his friend to Las Vegas’ gaming tables. Gilbert, his friend says, immediately demonstrated a knack for counting cards, handling money, and taking risks. “It was typically blackjack,” recalls Swerdlow, who sometimes accompanied them. “We didn’t have much money then. But there were moments when Dave would bet a big pile of chips. He’s willing to make a bet and live with the consequences.”

Sports are another of Gilbert’s enthusiasms. His friends say that, whether he’s returning serve at ping pong or standing over a putt — he plays to an 11 handicap at golf – he wants to win. Remarks Newburger: “He’s competitive to the point that — when he beats you — he wants the Goodyear blimp flying overhead to announce his victory.”

Gilbert, who is married with two children, is legendarily loyal to friends and family. While most members of a college fraternity might keep up with old companions after graduation by exchanging greeting cards and attending college reunions, Gilbert goes the extra mile.

He once footed the bill for Swerdlow to travel with the USC football team to an away game, arranging it so that his fraternity brother could view the action from field-level. After Newburger had a recent health scare (no worries, he’s O.K.), Gilbert rounded up a couple of dozen fraternity brothers and their wives (or companions), and put together a four-day bash in his buddy’s honor. The event was held at Cabo, the Mexican beach resort in Baja California, and Gilbert underwrote a fair amount of the cost. “He shares his success with his friends,” Newburger says, adding: “I don’t know anybody who works harder on friendships.”

He once footed the bill for Swerdlow to travel with the USC football team to an away game, arranging it so that his fraternity brother could view the action from field-level. After Newburger had a recent health scare (no worries, he’s O.K.), Gilbert rounded up a couple of dozen fraternity brothers and their wives (or companions), and put together a four-day bash in his buddy’s honor. The event was held at Cabo, the Mexican beach resort in Baja California, and Gilbert underwrote a fair amount of the cost. “He shares his success with his friends,” Newburger says, adding: “I don’t know anybody who works harder on friendships.”

Many of the personality traits described by friends and colleagues — tenacity and competitiveness, self confidence and leadership — played a key role in the development and success of National Funding, which Gilbert founded just two years out of college with $10,000 borrowed from his uncle, Howard Kaiman, of Omaha.

He’d worked a couple of quick jobs right after college, including a stint at small-business lender Balboa Capital, but he was always destined to be his own boss. Gilbert’s start-up was called Five Point Capital and, at first, it was located in the affluent Chatsworth section of Los Angeles and concentrated on equipment leasing.

“The first two years we were a cold-calling company and then we got into direct mail and saw some success and then we moved to San Diego and started to scale up the company,” Gilbert says. The decampment, he explains, was “for the quality of life, but we also felt we could hire from a better talent pool than L.A. We wanted to set ourselves apart.”

By 2007, Five Point was cranking up operations, revenues shot to $28 million and its headcount totaled 210 employees. “Then the Great Recession hit” in 2008-2009, Gilbert says. The company was forced to furlough 140 employees, two-thirds of its workforce. Yet even as it retrenched, the company managed to branch out. It began making merchant cash advances, Gilbert says, and, also in 2007, it linked up with CAN Capital to do broker financings. “We were pretty well known and they were looking for partners for factoring and leasing,” Gilbert explains.

It took time to recover after the financial crisis. But by 2013 – the year that Gilbert re-branded his company “National Funding” – the company was able to hire back as many as 15% of its laid-off employees (most had found other jobs, in many cases relocating to Silicon Valley, Gilbert reports). By then, the company had secured a $25 million credit facility from Wells Fargo Bank, which allowed it to move up the food chain to “become a balance-sheet lender,” Gilbert says, and offer a wider selection of financing options.

Key to driving the company’s phenomenal growth has been its flood-the-zone marketing and sales strategies. The company spends $16 million annually on marketing using a full panoply of channels and media, both online and offline. These include direct mail and targeted marketing, paid advertising, search-engine optimization or SEO, and sports sponsorships. “We try to build a whole range of marketing mechanisms,” explains marketing chief Bryla, “and when you get the mix right, they all help each other.”

Gilbert is a big believer in the benefits of sports marketing, the company’s website featuring the logos of the San Diego Padres (baseball), and Anaheim Ducks and Los Angeles Kings (hockey). Ever the faithful alumnus, Gilbert and his company back USC football as well. During the 2015 2016 college football season, the company paid for naming rights for what became, for one night, the “National Funding Holiday Bowl” at Qualcomm Stadium.

Gilbert is a big believer in the benefits of sports marketing, the company’s website featuring the logos of the San Diego Padres (baseball), and Anaheim Ducks and Los Angeles Kings (hockey). Ever the faithful alumnus, Gilbert and his company back USC football as well. During the 2015 2016 college football season, the company paid for naming rights for what became, for one night, the “National Funding Holiday Bowl” at Qualcomm Stadium.

Janet Fink, department chair at the McCormack School of Sports Management located at the University of Massachusetts-Amherst, told AltFinanceDaily that sponsorship programs can easily cost a million dollars or more. “It’s not cheap,” she says. “When a company sponsors a team, they get a number of benefits. One is that they get to put the team’s logo on their website. The idea is that fans are passionate or have an affinity for the team and that it will rub off on a sponsor.

“Sports enthusiasts,” Fink adds, “often make good customers. When you have enough disposable income to go to these sporting events, you’re probably a good prospect for a loan.”

The sponsorships — which include civic involvement such as offering Holiday Bowl tickets to members of San Diego’s large military contingent as well as to company employees — also build good will in the community and team spirit among the workforce. (National Funding also makes an effort to hire veterans, says Bryla.)

Gilbert believes in the old adage that you have to spend money to make money. The company spends $14 million rewarding its network of outside brokers. Inside the company, high-performing salespeople are compensated with commissions, bonuses and an assortment of rewards, including resort trips.

But sales representatives’ must conform to company guidelines. Justin Thompson, National Funding’s sales chief, explains that the “customer comes first” philosophy is not just a slogan but a core value. “We’re not a factory spitting out widgets,” Thompson says. “We’re here to build relationships and sell a repeatable product. We want that customer to come back to us. Every loan is customized. Six of ten customers who pay off their loans come back for a second financing. Whether your business is dog grooming or you’re an asphalt company,” he adds, “people will do business with people they like and trust.”

Using the software program “customer relationship management” (CRM), National Funding expends a lot of effort gathering data on its business customers and extrapolating the information for use in credit evaluations. But the use of technology only goes so far.

Gilbert reckons that the art of the deal involves about “70 percent algorithm and 30 percent people.” He adds, “You still need the people component to look at credit profiles. The algorithm spits out a recommendation but we still need the human element.”

Gilbert reckons that the art of the deal involves about “70 percent algorithm and 30 percent people.” He adds, “You still need the people component to look at credit profiles. The algorithm spits out a recommendation but we still need the human element.”

If there’s a fly in the National Funding ointment, it’s that the company’s fees can be more expensive than a bank loan.

But borrowers who have been denied loans at a bank or other lender are likely to overlook those costs. Austin, the florist in West Palm Beach, for example, came to National Funding when his bank, North Carolina-based BB&T Bank, gave him the cold shoulder despite the $15,000 in deposits that he averages each month. “I’ve been with them for six years,” he fretted, “and they treated me shabbily.”

Even more grateful was Jimmy Frisco, of Annapolis, who is co-owner with his wife of Lisa’s Luncheonette, a business that includes a food trailer and several cafeterias located in the city’s office buildings. They employ about a dozen people.

Frisco had taken a nasty spill and was laid up for seven months. Health insurance covered the $18,000 in medical costs but he and Lisa fell behind in their bills and needed working capital to pay for food purchases and other business expenses. By the time a flyer from National Funding popped up in his mailbox, he and his wife “had been turned down by several other lenders, including banks,” he says, adding: “Things happen in life and we don’t have the best of credit.”

Getting that loan for $25,000 from National Funding took just three days. Frisco’s health is much improved and business is back to normal. He won’t discuss the terms of the financing, other than to say “it was reasonable.”

He adds: “There were no problems with National Funding, no hassle with the paperwork. They’re great people to work with.”

Capital Stack Hit With Class Action Lawsuit

October 10, 2018A class action lawsuit brought by former employees of Capital Stack, LLC was filed in federal court on Tuesday for damages resulting from alleged labor law violations. David Rubin, Brian Stulman, eProdigy ACH, LLC, and eProdigy Operations, LLC are also among the named defendants. Capital Stack is a merchant cash advance company based in New York.

The 22-page complaint lays out seven claims including failure to pay the minimum wage required by New York Labor Law.

The suit can be downloaded here.

The case is 1:18-cv-09230 in New York Southern District Court.

In Anticipation of Hurricane Florence, Funders Suspend ACH Debits

September 12, 2018McLean, VA-based Breakout Capital is proactively suspending ACH debits for customers based in the counties designated by FEMA’s Major Disaster Declaration, according to an announcement made earlier today. They will be continuing to monitor the situation so that they can respond accordingly.

Gainesville, FL-based Elevate Funding is also pausing debits preemptively, the company says, for active merchants in North Carolina, South Carolina, and Georgia. After the storm, merchants can call in to report their damage or business status, they say. “Being based in Florida, exposed to many storms over the years, allows Elevate to understand how a hurricane’s damage can vary within 50 miles out to a 200 miles. Each case and customer will present different issues over the next week and some out to months.”

Chicago-based Lendr, echoed a similar plan. Company CEO Tim Roach says, “We will suspend payments for the rest of September for any client that is affected by Hurricane Florence. Most clients will come back on a reduced payment schedule for a short period of time. In the past we have provided additional funding for clients in need to help get their business back on track due to these types of natural disasters.”

Ft. Lauderdale-based Fundzio has announced that ACH payments are being suspended for businesses in South Carolina and North Carolina on Monday, Sept 17th through Friday, Sept 21st.

A State of Emergency has already been declared in North Carolina, South Carolina, Virginia, Washington DC, Maryland, and Georgia. It is currently a Category 3 Hurricane.

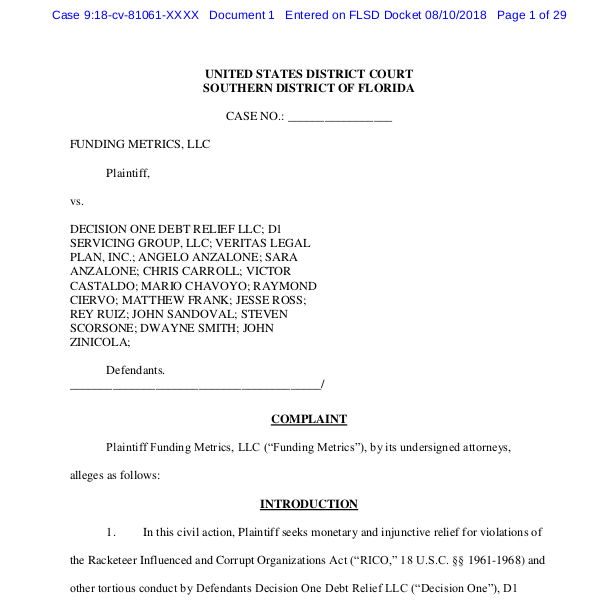

War on Debt Settlement Continues: 16 Defendants Sued in RICO Case

September 6, 2018

Fourteen individuals and two companies (including Decision One Debt Relief) were sued by Funding Metrics in Federal court last month for allegedly “conducting a nationwide illegal debt restructuring scheme through numerous acts of mail and wire fraud.”

The suit, which stems from the defendants’ interference with Funding Metrics’ merchant cash advance customers, makes six claims, among them financial damages resulting from state and federal crimes. Per the complaint:

“Defendant Decision One (along with its affiliate/alter ego D1 Servicing) fraudulently presents itself as being able to renegotiate and restructure merchant agreements with Plaintiff and other funding companies. It has established a deceptive business practice of making misleading and often outright false representations to merchants under contract with Plaintiff promising that, with its help, these merchants will save money on those contracts by defaulting on them. Decision One tells merchants that they can safely stop paying cash advance funding companies like Plaintiff; that it will go to work for them promptly; that it can reduce their debt by 60-80% or more; and that they will be provided with a Veritas insurance plan to cover legal expenses arising from their defaults, once cash advance companies exercise their rights under agreements with their merchants, as they inevitably will. Based on these misrepresentations, the merchants default on their contracts with their funders – that is, at Decision One’s direction, they stop paying their funders and instead pay Decision One – although Decision One does not even expect to achieve results for the merchants. The result is a fraud on the merchants and tortious interference with the contracts Plaintiff have with them.”

The suit is just the latest bomb dropped on the exploding debt settlement industry. AltFinanceDaily began covering the controversy surrounding debt settlement in late 2016 after the owner and employees of an upstate New York debt settlement company were arrested for charging merchants to restructure their merchant cash advances and then not actually performing any services. The owner, Sergiy Bezrukov, was charged with money laundering, bank fraud, mail fraud, wire fraud and conspiracy to defraud. Bezrukov has been locked away in jail for almost two years awaiting trial. He is facing a maximum of 30 years. Two of his employees pled guilty, Vanessa Cardona to bank fraud and Dustin Walker to conspiracy to commit bank fraud.

Since then, nearly a dozen major lawsuits have been filed by merchant cash advance companies against other debt settlement companies that are alleged to be carrying out similar schemes. One of those sued companies, NJ-based Corporate Bailout LLC, was featured on the cover of the New York Post last summer for being “the craziest office in America.” Corporate Bailout was sued by both Yellowstone Capital and Everest Business Funding which later resulted in a very public settlement agreement that forced Corporate Bailout to fork over $500,000 to the two MCA companies.

Decision One Debt Relief, sued now by Funding Metrics, was also originally a co-defendant alongside MCA Helpline in a lawsuit filed by Everest Business Funding earlier this year. In February, after determining the two were not related, Everest dropped the claims against Decision One only. The suit against MCA Helpline is still pending.

Around that same time, a representative for Decision One revealed to AltFinanceDaily that the company was on track to be doing more than $100 million a year in business.

Bezrukov, by contrast, who currently resides in a Niagara County New York jail, is accused of having only obtained $1.2 million throughout his entire debt settlement venture’s existence. Although Decision One is not being charged criminally, the private civil suit alleges damages caused by a violation of criminal statutes including RICO.

The Funding Metrics suit against Decision One was filed in the Southern District of Florida under ID# 9:18-cv-81061.

1 Global Capital Files Chapter 11

July 30, 2018

UPDATE: A joint motion filed this morning explained that the companies were forced to file bankruptcy “in order to address a sudden and acute liquidity crisis and to preserve their assets and business operations for the benefit of the individual lenders and all other constituencies. As a result of the investigations commenced by the US Attorney’s Office and Securities and Exchange Commission, with which the Debtors have been and will continue cooperating, the Debtors have ceased their pre-petition effort to raise capital.”

1 Global Capital LLC filed for Chapter 11 on Friday, according to a voluntary petition filed in the Southern District of Florida. The company’s estimated assets and liabilities exceed $100 million while the number of estimated creditors was listed as between 1,000 and 5,000.

A related company, 1 West Capital LLC, also filed for Chapter 11.

Greenberg Traurig, LLP has been retained to assist on the companies’ behalves.

In a joint motion filed this morning, both entities described themselves as “providing direct merchant cash advances to small businesses across the United States.”

Lendio Opens Franchise in Charlotte, NC

March 15, 2018

Today, Lendio announced the opening of its latest franchise in Charlotte, NC. Through the Lendio franchise program, Chris Cronk will help local businesses in the community apply for loans, review their options and secure funding.

The company has a network of over 75 lenders and its funding options include SBA loans, startup loans, equipment loans, commercial real estate loans and more. In the last fiscal year alone, Lendio facilitated more than $300 million in funding, according to the company.

“I’ve worked with numerous companies and witnessed their struggles to find capital,” said Cronk, who was a former investment banker for Bank of America Merrill Lynch where he advised and facilitated financing for companies of all sizes. “Charlotte is a fast-growing market and community. I’m excited to be a part of that growth by helping businesses in every industry find funding.”

Lights, Camera, Crypto-Transaction – How a Lending Journalist Raised Millions to Build Magic Lamps Through the Murky World of Initial Coin Offerings

November 15, 2017

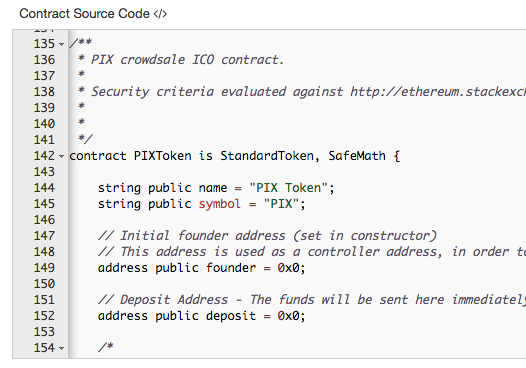

This past July, the winner of the Best Journalist Coverage category at the 2017 LendIt Conference Awards, announced that he would be stepping outside of his journalistic endeavors to raise money for a futuristic lamp company. The product, dubbed Lampix, is described as a lamp with a projector, a camera, specifically placed light-emitting diodes (LEDs), and a cloud-enabled computer. On the company’s “Medium” blog, Lampix promises that the product is “designed to transform any flat horizontal surface into an interactive computer.”

The man behind Lampix, George Popescu (whose Lending Times news site competed against and beat out fellow finalist AltFinanceDaily at the LendIt Awards), makes for an interesting case study in alternative finance. That’s because Lampix shunned traditional capital-raising methods by relying on an Initial Coin Offering (or ICO), an unregulated blockchain-based corporate event which is similar to an initial public offering. Rather than purchasing shares, as is the case in an IPO, investors in an ICO receive digital tokens instead of shares. In August, Lampix raised $14.2 million through its ICO*.

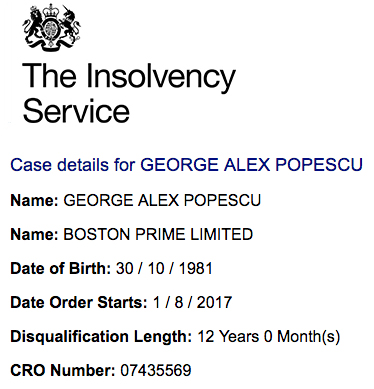

Popescu’s name popped up again a few months after the LendIt award on a regulatory blotter in the UK.

Popescu’s name popped up again a few months after the LendIt award on a regulatory blotter in the UK.

In case details published by the UK’s Insolvency Service on August 1st, the agency announced that Popescu was disqualified from serving as a company director.

Mr Popescu breached his fiduciary duties to act in the best interest of Boston Prime Limited (“Boston Prime”) and/or failed to ensure that both Boston Prime, as the regulated firm, and him individually, as the approved person, complied with the Financial Conduct Authority (“the FCA”) rules and guidance.

$6.2 million was transferred out of the company to a company named FXDD. Boston Prime’s receiver is presently suing FXDD seeking the return of the funds to the company. Proceedings are ongoing. Mr. Popescu is not under investigation and there are no legal proceedings at this time against Mr. Popescu.

It’s an inauspicious beginning for someone financing the “lamp of the future” using an unregulated and controversial strategy. Even so, when its ICO concluded on August 19, Lampix declared its gambit a success after raising $14.2 million through the sale of its digital tokens, which are known as PIX.**

By mid-November, the market value of those digital tokens, which exist on the Ethereum blockchain, had dropped by 50%, causing Lampix investors to suffer losses of $7 million. Unlike shareholders in publicly traded companies, token buyers have few investor protections. It’s not clear they are even considered to be actual investors at all. Buried in the fine print of Lampix’s 85-page “white paper” – a convenient way to avoid the label of prospectus – is a disclaimer. “Buyer should not participate in the [PIX] Token Distribution or purchase [PIX] Tokens for investment purposes. [PIX] Tokens are not designed for investment purposes and should not be considered as a type of investment.”

Additional disclaimers, moreover, declare that the white paper is not a prospectus, that the tokens “are not securities, commodities, swaps on either securities or commodities, or a financial instrument of any kind.”

But the distinction has not deterred people from joining in the frenzy of buying digital tokens like PIX. So much so, TechCrunch reports companies employing this strategy had raised nearly $800 million by means of ICOs in the first half of 2017.

And the SEC is not exactly excited about ICOs. “Fraudsters often use innovations and new technologies to perpetrate fraudulent investment schemes,” a July 29 directive by the SEC states. “Fraudsters may entice investors by touting an ICO investment ‘opportunity’ as a way to get into this cutting-edge space, promising or guaranteeing high investment returns. Investors should always be suspicious of jargon-laden pitches, hard sells, and promises of outsized returns. Also, it is relatively easy for anyone to use blockchain technology to create an ICO that looks impressive, even though it might actually be a scam.”

On September 29, moreover, the SEC brought an enforcement action against REcoin Group, charging Los Angeles businessman Maksim Zaslavskiy and two companies he controls with defrauding investors “in a pair of so-called initial coin offerings (ICOs) purportedly backed by investments in real estate and diamonds,” an SEC press release said.

The SEC alleges that Zaslavskiy and his companies –REcoin Group Foundation and DRC World (also known as Diamond Reserve Club) — have been selling unregistered securities, and that “the digital tokens or coins being peddled don’t really exist.”

Meanwhile, telephone calls and an e-mail to the SEC seeking the federal regulator’s view on Lampix’s ICO drew a terse response from Ryan T. White, a public affairs specialist, who replied that the agency would “decline comment.”

Meanwhile, telephone calls and an e-mail to the SEC seeking the federal regulator’s view on Lampix’s ICO drew a terse response from Ryan T. White, a public affairs specialist, who replied that the agency would “decline comment.”

Deborah Meshulam, a partner in the Washington office of law firm DLA Piper and a former SEC enforcement official, told AltFinanceDaily: “Regarding the lack of equity ownership, Lampix is seeking to establish that the tokens are not securities. Whether the SEC would agree should it decide to look into the offering depends on the facts and circumstances. The SEC staff would look past form to substance to assess whether the sale of the tokens constitutes an investment contract under legal standards. If so, then the SEC would view the Lampix offering as a securities offering. It may be that Lampix (or its lawyers) already vetted the offering with the SEC but I don’t know the answer.”

Popescu tells AltFinanceDaily in an e-mail interview, “We had to respect all securities rules and regulations of course, respect the Howey test and so on. There were no hoops to jump through as we are not trying to avoid anything or prevent anything. We honestly built a token to build a community to help us crowdsource (mine) pictures for all applications among which, Lampix.”

“Each PIX token,” the Lampix website explains, “will be used as a form of payment to picture image miners, voters and app developers or to purchase a Lampix, cloud computing and apps.”

Meshulam also notes that the June, 2017, date of the Lampix white paper pre-dates the SEC’s enforcement activity in this area. She adds, “The statement that ‘token sales or ICOs are not currently regulated by the U.S. Securities and Exchange Commission may be very literal in the sense that there is not a specific regulation, but the SEC has stated that, in the right situation, ICOs are subject to the US federal securities laws.”

Erin Fonte, an attorney in the Austin, Texas, office of Dykema Cox, and the leader of the firm’s regulatory & compliance group, says, “The ICO stuff is so up-in-the-air. The SEC is looking at it closely. But it’s fairly new. And some of them (ICO’s) have been tied to fraud and Ponzi schemes. If a client came to us (seeking advice), we’d want to vet the people behind the offering.”

But what of Lampix, the company that won the Augmented and Virtual Reality category of the South by Southwest (SXSW) Accelerator Pitch Event earlier this year in March – and put a pretty feather in the cap of Popescu?

Popescu’s resume is no doubt impressive. He holds a trio of master’s degrees in various scientific and technological disciplines, including one from Massachusetts Institute of Technology. And he is a serial entrepreneur who lays claim to having founded 10 companies: they include, according to his LinkedIn profile, online lending, a craft beer brewery, an exotic sports car-rental space, a hedge fund, a peer-reviewed scientific journal, and a venture-debt fund.

He’s charmed journalists like Forbes contributor Roger Aitken, who declared: “The founders (of Lampix)…believe that Lampix will impact humans as much as computers or smart phones in the future…Think Tom Cruise in Minority Report. Imagine your room in five years: you will be able to use any surface around you as if it was a computer. The ability to transform any surface into an interactive computer (augmented reality) is going to unleash applications we have not even conceived of.”

The Lampix website hyped its ICO with the aid of an infographic listing “active product inquiries” the company has in its pipeline, the likes of which includes Amazon, Apple, Samsung, Microsoft, Sony, IBM, BMW, Bloomberg, PwC, and the Aspen Institute. With all of these names seemingly lining up, it begs the question: Why did Lampix choose the controversial route of an ICO to raise capital?

But it’s hard to determine the seriousness of these corporate relationships. Florin Mihoc, Lampix’s Strategic Partnerships & Development Advisor, said he could not assist us with confirming any of them, citing the slow and cumbersome bureaucracy of dealing with Fortune 500 companies. He did invite us to try reaching out to some of them on our own, which we did.

Bloomberg is one of the few acknowledging a relationship with Popescu’s company. Chaim Haas, head of innovative communication at Bloomberg, told AltFinanceDaily that the New York-based media and financial communications company “collaborated” with Lampix. Bloomberg, he says, “has used Lampix hardware in its fellowship program (Bloomberg AR Fellows) as a prototype for augmented reality applications.” But Haas declined to elaborate on whether Bloomberg’s relationship with Lampix was more than an experimental one.

Edward Caldwell, director of public relations for East Coast markets and sectors at Pricewaterhouse Coopers, the Big Four accounting firm, declined to comment about Lampix. “We can’t discuss individual companies, clients or engagements,” he reports.

Douglas Farrar, senior manager for communications and public affairs at the Aspen Institute, told AltFinanceDaily that he could find no business relationship between Aspen and Lampix. “I have gone down quite a few rabbit holes here,” he said in an e-mail, “But I’m coming up empty.”

When Popescu was directly confronted about this, he wrote, “The companies would only figure [in the infographic] if they actually themselves reached out to us and we exchanged emails with somebody from that entity. Most of these entities have many people and most of the companies’ people will have no idea [that] somebody else in the company is talking to us.”

Telephone calls and e-mail requests for comment to Microsoft were not returned.

A spokesperson using BMW of USA’s official twitter account, however, responded to an inquiry by saying they were a customer of Lampix, “but only for office usage.”

Meanwhile, George Popescu has been on the sales trail. A case in point was his October 5, Youtube interview conducted by Ian Balina, a self-described influential investor in blockchain technology and cryptocurrency – and someone with a reputation as an industry promoter and evangelist. (Balina caters to the get-rich quick crowd and publishes how-to guides trumpeting promises like “How ICOs can make you a millionaire in 3 years” and “make millions with bitcoin.”)

Meanwhile, George Popescu has been on the sales trail. A case in point was his October 5, Youtube interview conducted by Ian Balina, a self-described influential investor in blockchain technology and cryptocurrency – and someone with a reputation as an industry promoter and evangelist. (Balina caters to the get-rich quick crowd and publishes how-to guides trumpeting promises like “How ICOs can make you a millionaire in 3 years” and “make millions with bitcoin.”)

Balina asked Popescu the softball question, could he show viewers a demonstration of the product? Popescu admitted he wasn’t prepared to do that and when he attempted to set one up on the fly, it didn’t work. The incident is notable because Lampix has been promoting the video through its social media network.

Popescu corroborates a number of details about the ICO, however. He confirmed the ICO price of a PIX token to be 12 cents, the US dollar price people had to pay per token. Cryptocurrency exchanges, where token speculators can buy and sell tokens online, show the trading value of a PIX token currently hovering around 6 cents, which translates into roughly a 50% loss in value.

Investors feeling hurt by such a loss can’t contest the purchase of PIX tokens with their credit card issuers. That’s because of a requirement that token sales had to be purchased with ether (ETH), the currency of the Ethereum blockchain. While ether is arguably similar to Bitcoin, it operates on an entirely different blockchain.

To participate in the ICO, in a Youtube video, Lampix also explained to purchasers, for example, how they could first buy ether with dollars through an online exchange known as Coinbase** before forwarding the ether to a digital wallet. Next, investors were instructed to send the ether from the digital wallet to a specially designated PIX address. An automated “smart contract” would then release the appropriate amount of tokens to the buyers’ digital wallets 31 days after the ICO was consummated.

It’s a byzantine procedure. And for investors – especially for those who are not exactly tech-savvy – the rigmarole makes it nearly impossible for them to recover their money should they feel buyer’s remorse. Neither the video nor the Lampix white paper mentions any buyer restrictions. Indeed, Lampix’s white paper specifies that “anyone” in the global market can participate. That means that an investor could theoretically be underage or a citizen of Iran or North Korea. (When asked what steps Lampix took with regards to KYC/AML, Popescu said, we “implemented the standard ones with partners specialized in it.”) Investors could even be citizens of the UK where Popescu is banned from being a company director.

And global they are. AltFinanceDaily interviewed Rudy (whose last name we are withholding), a graduate student who lives in Singapore that says he bought approximately $2,200 worth of PIX tokens during the ICO. The drop in value has gotten him so frustrated that he’s contacted securities regulators in the United States to investigate Lampix. Despite the caveat in the white paper that tokens are not an investment and should not be used for investment purposes, Rudy said he considered himself to be an “investor” and that his reason for buying the tokens was to sell them in the future for a profit.

Popescu, who wasn’t asked about Rudy’s experience specifically, told AltFinanceDaily that Lampix is not selling PIX tokens as an investment but rather to primarily build a community. “What people do with the tokens is their choice and we cannot prevent them,” he asserted.

English is not his first language but Rudy said, “I think that [the] SEC should regulate ICOs in the USA. There are no rules currently, teams can promise anything before the ICO and forget everything after the ICO. Things have to change, there should be legal pressure on crypto teams.”

Rudy added that he was “so enchanted” by Lampix’s ideas that he had promised himself not to sell the tokens for at least two years even if they were losing value. He conceded that he was not a tech expert. But, he says, the award at the SXSW competition was an important milepost to him.

AltFinanceDaily found 700 more people interested in Lampix on the company’s official Telegram channel. The chat history since September 20, which we were able to obtain, has been dominated by talk of the PIX token’s trading value. Those bemoaning the low price regularly use the term “investors” to describe themselves – never mind that the white paper specifies that PIX tokens are not supposed to be an investment or to be used for investment purposes.

The chat’s administrator, who uses the nickname Chester, identifies himself as a “community manager” at Lampix. At one point he too refers to PIX holders as investors. “Hey guys,” he wrote in the channel on October 1, “Lampix is a company, not a single person, we don’t do things that quick, but pretty quick and we try not to confuse our investors by telling you unconfirmed news. Be patient, things will be just fine.”

Laura Toma, another community manager for Lampix, responded to complaints about the depressed price in the channel by saying, “The issue is that people want to get rich in a month.”

Indeed, investors hound not only the community managers, but also Popescu himself, who frequently joins in on the chat and fields questions about the trading price of PIX. “You should care more about the company revenue, clients, users.” Popescu replied to one user.

“Are you serious?” a user calling himself Dante fired back. “We are investors, and we care about the return on investment.” Another user with rough English tells Popescu, “As you know, most people come to ICOs for short-term profit. We cannot deny it.”

“Are you serious?” a user calling himself Dante fired back. “We are investors, and we care about the return on investment.” Another user with rough English tells Popescu, “As you know, most people come to ICOs for short-term profit. We cannot deny it.”

Others keep the faith. “PIX will be the real Aladdin’s magic lamp,” writes one user. Another hyperbolically predicts the price will “fly out of the earth, fly to the moon, and finally fly out of the galaxy.”

There is very little discussion about the use of the product itself while numerous inquiries are written in Mandarin. “Lampix has a lot of Chinese investors,” writes one. Other users self-identified as citizens of Russia, Romania, and France. Meanwhile, Toma writes, “Yes, there are investors from USA as well.”

Despite the losses that investors have so far experienced with Lampix, among other concerns, Popescu isn’t limiting himself to just one ICO. According to his online statements, Popescu is connected as an “advisor” to another company engaged in an ICO. AirFox, a Boston-based start-up launched by two Google alumni, provides free data to mobile phone users in return for eyeballing advertising. In early October, Airfox’s ICO raised $15 million. But a month later its AIR tokens, which sold for two cents apiece during the ICO, had lost 75% of their trading value. That means investors in AIR, the company’s ICO ticker symbol (which is becoming an increasingly ironic moniker) have seen more than $11 million go up in smoke almost overnight.

Popescu says in their defense, “The AIR tokens are meant to solve a real problem, of remunerating people who watch ads in exchange of getting more data and minutes on their mobile phone. The ecosystem is still being worked upon, the product is not live. Once the ecosystem is live we will see what really happens. Until then the token is mostly being handled by speculators. The price can therefore vary widely and it doesn’t reflect their true value.”

Even as Lampix and AirFox have been racking up massive losses for investors, Popescu announced on November 5 in a LinkedIn post that he would be involved in five more ICOs.

Among them is DropDeck Technologies, at which Popescu is listed as the chair of the advisor board; its ICO is scheduled for November 21. Another company, Factury, for which he is listed as an advisor, is initiating its ICO on December 15.

He’s an ambitious man.

And his ICO familiarity hasn’t escaped the scrutiny of PIX investors. “I find it strange that you are directing 5 other ICOs,” writes one user in the Telegram chat on November 4. “To make Lampix big, this will require a CEO [who is working] full time working on the project.”

Popescu responds personally. “I am working full time on the project but people have asked me to advise on their ICOs and this grows Lampix’s notoriety a lot in the crypto space,” he writes. He offered further assurances that he wouldn’t be advising those companies’ projects beyond their ICOs.

In an email to AltFinanceDaily, he writes, “I run right now Lending Times, Lampix and Block X Bank only. The ICOs are just customers of Block X Bank. I have built about a dozen companies in 9 years, sold a few, closed a few. Each company has a team to help me, I am not doing this alone. For the ICOs I am more or less involved as an advisor / helping them project-manage their ICOs. How to run 3 companies? It’s about being effective, organized, delegating, partnering and being productive. Oh and I don’t watch TV, so maybe I have a few more hours per day than the average person. I do work long hours.”

Block X Bank, through which Popescu extends his efforts toward other ICOs, is described on the company website as “a boutique investment consulting company specializing in connecting blockchain projects with funding.”

In all of these ICOs, money is seemingly being created out of thin air. A consultant who was hired by AltFinanceDaily to help analyze the technical aspects of both ICOs and smart contracts determined that Lampix raised much more than just the $14.2 million in token sales. In addition to the 114 million PIX tokens sold to investors, our consultant explained, the company also issued 220 million tokens to itself. At the ICO price of 12 cents apiece, those tokens would theoretically be worth $26.4 million – a huge piece of the total ICO pie that Lampix could sell on cryptocurrency exchanges if it wanted to rake in even more money.

There’s a kicker too. At scheduled intervals over the next four years, the smart contract that made PIX tokens possible in the first place is slated to automatically create – and allocate – 330 million new tokens to Lampix. Thus, when Lampix raised $14.2 million in August, the company reserved $66 million worth of PIX tokens for their corporate use.

Popescu said in his e-mail to AltFinanceDaily that these company tokens are for “corporate usage like employee incentives, M&A, other company investments…etc.”

It’s a mind-boggling sum of money for the development of a futuristic lamp whose followers mostly seem to reside on internet chats like Telegram, reddit, and bitcointalk.org.

And this has occurred despite the company’s withholding any information regarding Popescu’s status in the UK. Balina, who interviewed Popescu on Youtube, told AltFinanceDaily he wished he had known about his disqualification in the UK. “This is definitely a big issue and I wish I would have known about it so that either my audience or I could have asked him this directly on the live stream,” he said.

AltFinanceDaily asked Paul Savchuk, Co-founder, CEO, and Chief Product Officer at Cryptocurrency Capital LLC, a US-based hedge fund that only invests in utility tokens as commodities, if Popescu’s ban in the UK would have been relevant information in the Lampix ICO. “Yes, that might be a red flag for us in some cases and require us to perform additional research,” he wrote in an emailed response. “We look at management very seriously – especially since a lot of projects are treated like startups and management is a key component to whether or not many of these ICOs can make it. We try to find such events and spot red flags whenever we conduct our due diligence research on ICOs. The reason: each project has something that needs to be improved. ‘Red flag’ – sometimes conversely can lead to a great opportunity when other market participants ignored it or were too skeptical.”

Mr. Savchuk further said, “Lampix is a perfect example of a coin that on the surface looks very promising, but when you dig a little deeper, you do find red flags that can dampen the excitement for this investment.”

And yet Savchuk spoke rather positively of the Lampix product after reading their white paper. “We believe the project is looking to change the current AR/VR tech industry,” he said, referring to augmented reality/virtual reality. “The project is promising for two reasons. First, they have multiple companies in their pipeline. Second, they have a legitimate product which they will manufacture and sell. They are one of the few blockchain products to offer a tangible product with the ability to disrupt the market.”

“Third,” he went on, “most companies have gaps in building a strong structure at the outset of their existence. Some have bugs in initial code that cause breaches in cybersecurity. Others release product with a low level of usability – the ones who are aware of such problems have a greater chance of success. We would prefer to see publicly known strengths and weaknesses of such companies. Management has to be transparent about their team and product no matter what. Whenever possible, we want to be in touch with the management team.”

“Third,” he went on, “most companies have gaps in building a strong structure at the outset of their existence. Some have bugs in initial code that cause breaches in cybersecurity. Others release product with a low level of usability – the ones who are aware of such problems have a greater chance of success. We would prefer to see publicly known strengths and weaknesses of such companies. Management has to be transparent about their team and product no matter what. Whenever possible, we want to be in touch with the management team.”

With regard to the price drop, Savchuk said, “This is a danger for all purchasers of ICOs. Sometimes it’s caused by token purchasers (swayed by) fear and greed and (hoping for) easy money and fast money. I doubt somebody sold Apple Inc.’s stock right after its IPO. It is also very difficult to restrict exchanges from allowing massive pump and dumps. That’s not even mentioning the difficulty of measuring the value of tokens,” Savchuk concluded. “Consequently, such projects are struggling with low credibility. However, it also creates a possibility for those who believe in the idea and product on a long-term run.”

Popescu downplays the significance of the UK issue. The root of the debacle, he says, is the result of Boston Prime – the company he previously ran – being forced into bankruptcy by the actions of a company he is now suing called FXDD. “FXDD bought the companies and then bankrupted them and that’s why Boston Prime [went bankrupt],” he writes. “Myself personally and each company separately are suing FXDD for this. UK has archaic laws where if you are a director of a bankrupted company you get disqualified from being a director again for a time. Attorneys charge about 40,000 GBP to defend this automatic case and I weighed the pros and cons and decided to ignore it as I have no plans to be a director in the UK for time being.”

Investors unhappy with underperforming ICOs may be willing to challenge their legality. On October 25, for example, a class action lawsuit was filed against Tezos, a computer networking project that raised $232 million in one of the largest ICOs ever. In a complaint, the lead plaintiff alleges that, among other things, Tezos unlawfully engaged in the unregistered offer and sale of securities and fraud in the offer or sale of securities. “In July 2017, Defendants conducted an ICO in which they sold 607,489,040.89 tokens (dubbed ‘Tezzies’ or ‘XTZ’) in exchange for digital currency worth approximately $232 million at the time,” the complaint reads. The plaintiff, who purchased 5,000 Tezzies, feels he was misled about the company and the offering.

Internal squabbling at Tezos which has delayed the release of its product and the sheer amount of money at stake have put the company on the map with the mainstream media and business press. The New York Times, Wall Street Journal, and Fortune as well as news services Reuters and Bloomberg have all covered the allegations of fraud.

The day before the class action lawsuit was filed, moreover, a AltFinanceDaily reporter attended an explosive session at Money2020 in Las Vegas that saw Tezos co-founders, Arthur and Kathleen Breitman, attempting to give a status report of the company. A crowd that had gathered outside prior to the doors opening had attendees speculating whether the Breitmans “would actually show their faces” in the midst of all the drama.

To date, no lawsuits have been filed against Lampix despite the drop in the token’s value.

At a cryptocurrency/ICO meetup in NYC in October, a AltFinanceDaily reporter met with executives at one company preparing an ICO who said they would not allow American investors to participate because of securities-enforcement fears. Pressure is mounting in the Far East as well. Citing their illegality, Chinese regulators in September issued a blanket cease-and-desist order on all ICOs in their country. What that means for Lampix’s Chinese investors bears watching.

Popescu says that Lampix supports regulation in China. “Of course, all Chinese people have to follow Chinese regulation,” he writes.

Meanwhile, on the product front, Popescu says that right now a Lampix lamp can be purchased for $10,000, a tidy sum because they must be hand-made. “We plan to improve the manufacturing costs and then we’re planning to do a kickstarter early next year for around $500 [per] Lampix,” Popescu told AltFinanceDaily in his e-mail interview.

But for investors, it always comes back to the trading value of PIX. On October 25, one investor asks Popescu if the company will buy back its own PIX tokens at the ICO price to pump up their market price. “If you want a pump and dump please go to other companies,” Popescu responds. “We are here for 5-10 years to build a $100 billion dollar company and compete with Apple.”

And it all began with an ICO.

“ICOs also help with bootstrapping the user base – breaking the chicken and egg problem,” Popescu also explains in his e-mail to AltFinanceDaily. “In addition, given that Lampix is looking to crowdsource images, we prefer many different people hold PIX tokens rather than 2-3 VC funds. And last but not least I think tokens are better rewards for the community (liquid, mark to market, etc.) than illiquid instruments.”

Not everyone agrees that PIX is the most liquid instrument to grow the community. US Dollars come to mind, for example. “Let’s say I’m a customer,” one investor poses to Chester, a Lampix community manager. “I want to use the cloud computing service but then I see I have to pay with PIX. I have no experience in crypto and have no idea how to do that. I just want to use your service fast and don’t want to buy PIX coins first before I can make use of it. Will there be a fiat option?”

Chester is awed by the idea. “Well, you are so professional,” he writes. “Man, you are good. You are good, the question you threw just hit the spot seriously. I guess there is always something Lampix needs to figure out and choose the best solution. Technically speaking they are jolly good at this point, but it doesn’t mean it’s perfect.”

Chester, who assures him that he isn’t being sarcastic, goes on to refer to the investor who asked that fairly elementary question as a “big shark” that is “born to bite.”

It remains to be seen if the PIX “user base” shares the same philosophy as Lampix. Ian Balina, who interviewed Popescu on Youtube, separately asked his social media followers: “What’s the first thing you’re going to do once you hit your goals in cryptos?”

It remains to be seen if the PIX “user base” shares the same philosophy as Lampix. Ian Balina, who interviewed Popescu on Youtube, separately asked his social media followers: “What’s the first thing you’re going to do once you hit your goals in cryptos?”

The responses fly in:

“Buying my Lambo”

“Travel to Paris”

“Buy an island”

“Buy my mum her dream home”

“Quit my job and start up something for me”

“Pay off mortgage and be financially free”

“Buy house in Miami, buy Lambo, enjoy life”

“Retire”

“Easy. Buy more crypto”

Meanwhile on Telegram, where investors continue to engage Lampix management on a daily basis, Dante offers a sobering reminder of what they’ve bought into, “We don’t have equity, we only have tokens,” he writes. “And we are taking a big risk.”

* The amount of tokens sold multiplied by the 12 cent ICO price doesn’t exactly match the dollar amount Lampix says they had raised. That’s because Lampix not only issued bonus tokens to buyers at each stage of their ICO but also because the market value of ether, which users had to convert to from dollars to buy PIX, had fluctuated when they reported how much they raised. Like Bitcoin, the value of ether is volatile.

** The smart contract Lampix wrote to launch Lampix’s tokens into existence specifically named them PIX tokens and dubbed their publicly identifiable symbol to be PIX.

*** Coinbase is a respected digital currency wallet platform based in San Francisco.

BFS Capital Appoints Michael Marrache as CEO

August 17, 2017Coral Springs, Fla.—August 17, 2017—BFS Capital Inc., a leading small business financing company, announced that it has appointed Michael Marrache as Chief Executive Officer to succeed outgoing CEO and co-founder Marc Glazer. Named President in September 2016, Marrache previously served for more than three years as the company’s Chief Operating Officer. He also will join the company’s Board of Directors. Marc Glazer will continue to serve as Chairman of the BFS Capital Board.

“Michael has been invaluable in enhancing operations and driving sales. As CEO, he will lead our strategic direction both domestically and internationally, and spearhead initiatives that will continue to improve our loan portfolio metrics and strengthen our reputation among customers and partners as a premier small business lending organization,” said Glazer.

Over recent months, Marrache has built a management team that will execute on a long-term strategic plan to guide the company’s future and reach new milestones in the areas of origination, ISO partnerships and customer experience.

“I began work with BFS Capital nearly four years ago because I thought the company had enormous potential, and I’m even more certain of this today. I’m honored to have been asked by Marc and the Board to lead the company’s next phase of growth,” said Marrache.

“Our business has experienced great momentum over the last year and we’re setting a course for continued growth and leadership. We have a strong, committed management team and together, along with our employees, we’re primed to execute on our priorities, including upgrading the customer experience, investing in our product offerings and leveraging our data science to drive insights for our customers and partners,” Marrache added.

In April, BFS Capital reached a milestone of $1.5 billion in financing—a 50% increase over the $1 billion the company generated from inception through July 2015, led by loan portfolio growth in both new and repeat customers.

About BFS Capital

BFS Capital champions the long-term growth and prosperity of small businesses by providing timely, flexible financing solutions. BFS Capital’s leading small business financing platform leverages customized underwriting and proprietary algorithms to fund businesses in all 50 states and Canada, and through its affiliate, Boost Capital, in the United Kingdom. Since 2002, BFS Capital has provided more than $1.5 billion in total financing to more than 18,000 small businesses across more than 400 industries. Headquartered in South Florida with offices in New York, California and the United Kingdom, BFS Capital is an accredited BBB company with an A+ rating. To learn more, please visit: www.bfscapital.com.