History of Merchant Cash Advance

January 24, 2013The History of Merchant Cash Advance

Before it was mainstream, it was kind of mainstream. Merchant Cash Advance (MCA) is not new or even relatively new and it definitely isn’t a byproduct of the 2008-09 financial crisis. In fact, in 2007 some people thought the best days of the industry were already behind it. In an August 2007 issue of the Green Sheet, Dee Karawadra expressed reluctance to write about MCA because he believed the subject was stale.

When a GS Online MLS Forum member suggested I write an article on cash advance, I explained my research and said, “I think that boat has come and gone, and I missed it.”

Dee’s article is an excellent snapshot of the feeling of 2007. Excitement was running wild and bold predictions were being made. A lot of the same questions being asked today were asked and answered back then. Those employed in the industry that do not take the time to read up on MCA history are at a disadvantage. And one thing this industry did a great job of, was chronicling all of the events that unfolded.

The Green Sheet

Prior to 2007, The Green Sheet’s forum was the only source for information. It is still filled with threads going back as far as 2003 on the subject. The discussion seems to begin by one user posing the question:

Who thinks a cash advance program, (a loan) on future credit card volume will help themselves get more deals and their merchants operate better?

March 2003

By 2004, MCA was all the rage. Competition began to nibble at AdvanceMe’s monopoly, a monopoly they were rightfully entitled to because they owned the patent on split-funding. Many chose AdvanceMe anyway simply because they had already established a name for themselves.

You might want to check out AdvanceMe. I think they have a superior product and service as well as more money too … that you will be better served by AdvanceMe than you would by any of the other Cash Advance companies of which their [sic] are not that many.

August 19, 2004

And many weren’t even sure what they were selling exactly. Merchant Cash Advance had not yet even been coined as a term:

quick show of hands as to what title you would place on this product… A) Factoring of receivables B) Cash Advance C) something else… Just for the record – I don’t know what to honestly call it.

August 20, 2004

Those that responded called it an unsecured loan, factoring, merchant funding, and cash advance. Some that weren’t even familiar with the concept appeared completely lost in the conversations. It was common to confuse cash advance as meaning to take a cash advance out on an actual credit card. The need for a universal term was badly needed. An industry couldn’t progress forward if no one even knew what the industry was.

A Way to Build and Strengthen Merchant Account Portfolios

But on the subject of giving money to merchants in exchange for more back, programs offered by AdvanceMe and Rewards Network were compared on the merit of the cost to the customer. Since reps viewed MCA as an acquisition tool to obtain merchant accounts or retain them, commissions and renewals were rarely discussed. They were basically a non-factor and some folks from this era carried this mentality straight into the financial crisis age of MCA. Funders advanced merchants not to make money on advances, but to build their own processing residual portfolios and to sell or lease more POS equipment. The loan, cash advance, merchant funding, or whatever it was of the day was a tool to drive business, not a business itself. Right before and during the financial crisis, funding companies began to streamline their focus and suddenly it became all about funding and nothing else.

The MCA industry has remained in that state for about 5 years and some are starting to think that it’s time to evolve. A poster on DailyFunder.com recently ranted that his company can’t grow unless it diversifies, coincidentally citing that MCA would be better served as an acquisition tool. If this happened, history would repeat itself.

This should be a lesson to the MCA industry which is trying to make a product out of something everyone else views as an acquisition tool. Are we just lenders or diversified businesses? We are the former. As such, prices will never come down, margins can only get slimmer.

1/19/2013

In 2004, when the MCA industry was joined at the hip with payment processing, becoming a dedicated funder was a way to stand out from the crowd. But perhaps now that the market is saturated with dedicated funders, it is getting more difficult to build a presence in the market.

Behold! Merchant Cash Advance!

In May 2005, The Green Sheet was forced to label the product when it published a story about Merchant Cash Advances. We’re not claiming that this article coined the phrase, but it is a good approximation of when it started to be called such. A few sentences in, they actually disclaim their own term.

There isn’t even consensus on what to call the product, except that it is most definitely not a loan.

The three word term was not even used in the Green Sheet forums until October 2005, and then not again until March 2006. Soon after, that became the term of choice.

The One and Only MCA Blog

As MCA financing took on a life of its own outside of payment processing, the industry turned to a blog to learn about the unfolding events. From 2007 to 2010, David Goldin, the CEO of AmeriMerchant wrote weekly updates about his firm and experiences. He wrote about his harrowing battle with AdvanceMe. After invalidating their patent, he opened the floodgates for any funder interested in utilizing split-funding. He offered honest opinions and had excellent foresight, forever documenting what it was like for the MCA industry during the financial crisis. Anyone that didn’t get to experience that time firsthand should read it start to finish.

As Goldin’s company grew, he turned his focus to other matters. The North American Merchant Advance Association (NAMAA) was formed on April 29, 2010, a non-profit alliance designed to bring peace and order to an industry that had gone through tremendous turmoil in the last few years. He all but abandoned the blog afterwards.

Free Info for All

Where Goldin left off, I resumed by starting a credit card processing/MCA blog in July 2010 named Merchant Processing Resource (MPR). At that time, I was an MCAer that had toiled away as both the head of an underwriting department and as an account executive. The blog covered a lot of topics and was targeted towards business owners and ISOs simultaneously. I believed there was a vast amount of data that newcomers didn’t have about MCA and set off to share as much as I could without self-promoting a product or service.

By December, my web host (a very simple blog site named Webs.com) informed me that the website was using too much bandwidth for the current package. I upgraded it only to encounter the same problem again 9 months later. The site was forced to transfer to a real host in order to grow and be able to handle the surging stream of visitors. Webs.com’s format was not conducive to transfers and as a result, every article written prior to August 23, 2011 was time-stamped with that very date.

Three History Books

To recap, the Green Sheet and their forums were the places to follow MCA from 2003 to 2007. Goldin’s Blog narrated the story from 2007-2010 and MPR has carried the torch since then. If we go further back, and we believe everyone should, you’ll find that AdvanceMe kind of existed in a world of their own in the late 1990s. In 1999, they funded $9 million. What they were funding annually increased to $200 million by 2006, a time when they had already amassed more than 14,000 clients. These aren’t exactly the humble beginnings of a new industry. These are serious numbers that could arguably support the theory that MCA was already well into the mainstream.

MCA in Black and White

MCA information was publicly available nearly two decades ago via the U.S. patent office. Barbara S. Johnson is listed as the official inventor of split-funding AKA Automated Loan Repayment in documents filed in 1997. There were no forums or bloggers to explain how it worked. There was only this:

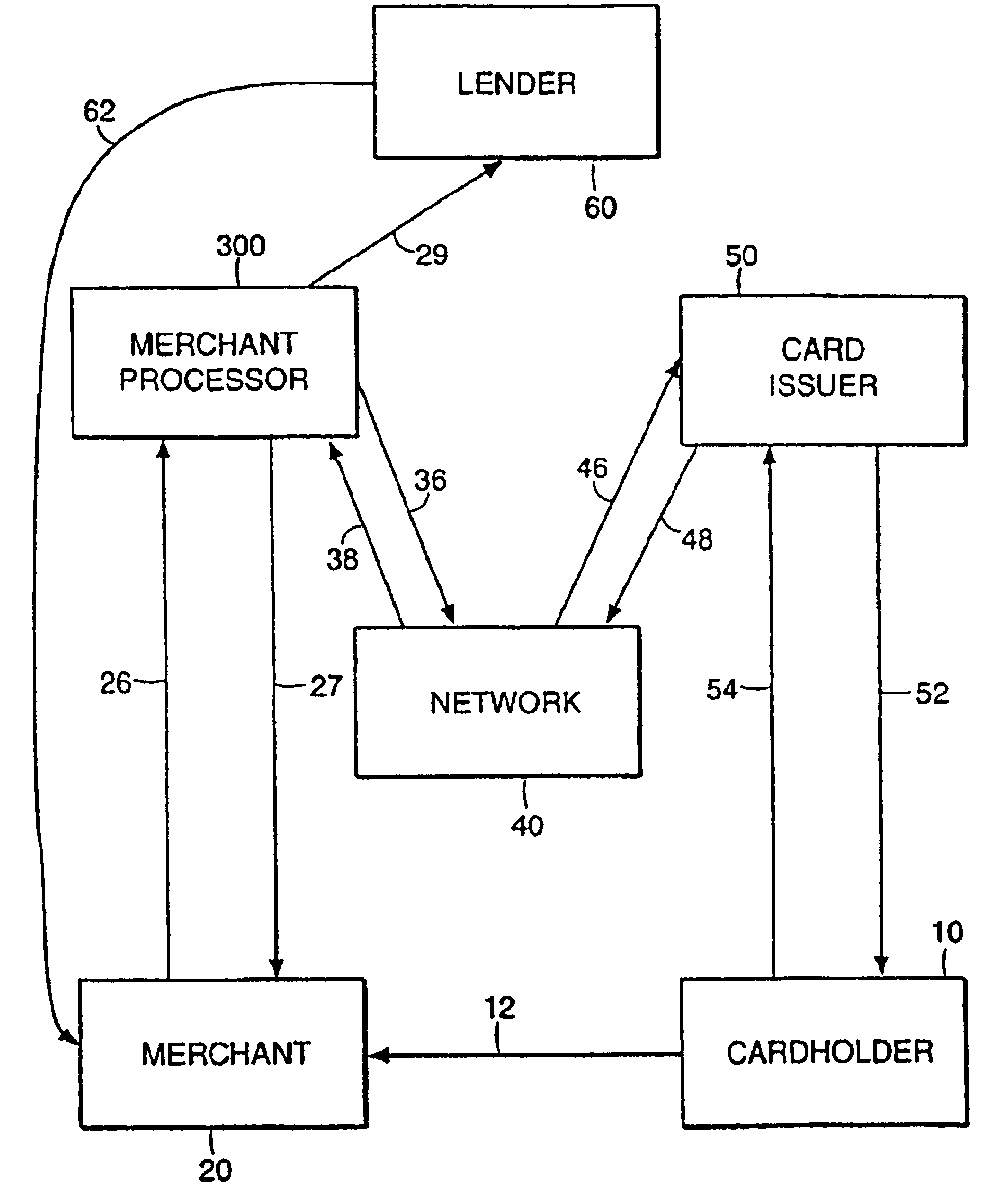

Systems and methods for automated loan repayment involve utilizing consumer payment authorization, clearing, and settlement systems to allow a merchant to reduce an outstanding loan amount. After a customer identifier (e.g., a credit, debit, smart, charge, payment, etc. card account number) is accepted as payment from the customer, information related to the payment is forwarded to a merchant processor. The merchant processor acquires the information related to the payment, processes that information, and forwards at least a portion of the payment to a loan repayment receiver as repayment of at least a portion of the outstanding loan amount owed by the merchant. The loan repayment receiver receives the portion of the payment forwarded by the merchant processor and applies that portion to the outstanding loan amount owed by the merchant to reduce that outstanding loan amount.

The Automated Loan Repayment kicked off an industry that would evolve significantly over the next 15 years and yet a payment processor was already doing this to fund merchants as far back as 1992. Litle & Company didn’t call it MCA. That name didn’t even come about until around 2005, but they were the first MCA funder in the country. The makes MCA more than 20 years old.

Been There, Done That

We may have closed a chapter in 2012 when it became evident the product had finally graduated from the minor leagues, but there is a forever long story that preceded it. MCA financing existed before some account reps were even born. Sadly some of these kids talk to prospects today without really even knowing what they’re selling. Then again, in 2004 no one knew what the heck they were selling either. There is still technically no formal name especially since split-funding is no longer the standard. If the poster in 2004 posed the same question today about what to label this product as, there would be just as much disagreement. Business cash advance, merchant financing, ach advance, cash flow loan, ach funding, merchant cash advance, unsecured loan, merchant loan. Nobody really agrees and nobody really even does it the same way as everyone else. It’s all MCA to me and I’ll keep reporting on it for as long as it lasts. And as long as it keeps reinventing itself, there will always be a chance to get in early. Those that read up on the past or were there and experienced it firsthand have a major advantage. History repeats itself in MCA.

You know those butterflies you’re getting about 2013? They were felt before in 1998, 2004, and 2007. MCA was kind of mainstream before it was mainstream. 2012 ignited a spark and some of us know what’s going to happen next. As for the rest of you, brace yourselves. It’s going to be more crazy than you can imagine.

– Merchant Processing Resource

../../

Largest Merchant Cash Advance in History Ends in Default

September 27, 2011 Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

While SFS was given high praise from their peers, some began to speculate if transactions that large were practical. After all, the costly financing of a MCA is priced in accordance with the risk of default, not in accordance with big profits for the financier. When your portfolio is in great shape, it can be easy to forget what the pitfalls are. And since the MCA industry paraded the Las Vegas Mob exhibit as the $4 Million deal that changed everything, we’re eerily reminded of the words by Jeff Mitelman, the CEO of AdvanceIt who was quoted two years ago as asking: “How prepared are you to lose $4 million dollars?”

We won’t pretend to know what led to the downfall of the Las Vegas Mob exhibit or why it went south so quickly. SFS could potentially lose 98% of their investment, a hit that will surely change their outlook on doing large deals in the future. The VegasInc article alleges gross mismanagement and fraud, factors that are difficult to foresee in the course of underwriting.

Industry message boards have been abuzz with comments on the default, with some competitors of SFS being accused of kicking a man while he’s down. “you ought to do smart funding, not just showing off your Balls,” one broker fired off at them. SFS has a stellar reputation and is one of the most knowledgeable firms in the MCA space. We have no doubt they inspected the merits of the deal backwards, forwards, and upside down. But nothing is perfect.

The default is expected to attract attention of the news media, leaving many to wonder how this transaction will be interpreted under the public eye. We assert that it will put to rest any criticism the MCA product has ever received about high costs.

Risk vs. Reward

Back in March when the deal was written, an outsider could claim that SFS just had an easy million handed to them. This view clashes with the Risk vs. Reward philosophy that MCA providers hold dear. To the MCA providers, the question was never “how can I make an easy million?” but rather, “how prepared am I to lose $4 Million?”

Any business that can’t get a bank loan, can’t get one for a reason. There’s a measurable value of risk that’s not worth taking. MCA providers fill the gap but compensate to offset defaults. There’s a term for something like this. It’s called a Happy Medium.

Merchant Cash Advance is the happy medium financing option for small businesses. And for the immediate future it is likely to stay within the small business niche. We all know now what can happen when the concept is applied to a multi-million dollar project. The outcome was not so happy and the loss not so medium.

But it will all even out in the end…

– Merchant Processing Resource

An Underwriter in Salesman’s Clothing

April 1, 2009 It was mid-2006 and AdvanceMe was finding it wasn’t so alone in the world anymore. First Funds, Amerimerchant, Merchant Cash and Capital, BFS, among others were abuzz with a business model and a dream. Practically fresh out of college I joined one of the few funding companies as an underwriter. For a kid with little experience in an industry where no one had experience, I was fortunate to have graduated from a great business school. I had held off pursuing a CPA to see where the Merchant Advance wave would take me.

It was mid-2006 and AdvanceMe was finding it wasn’t so alone in the world anymore. First Funds, Amerimerchant, Merchant Cash and Capital, BFS, among others were abuzz with a business model and a dream. Practically fresh out of college I joined one of the few funding companies as an underwriter. For a kid with little experience in an industry where no one had experience, I was fortunate to have graduated from a great business school. I had held off pursuing a CPA to see where the Merchant Advance wave would take me.

After my first week, I was hooked. Merchant processing, purchasing future receivables, private investors, and millions of dollars being pumped into small businesses were all part of an average day. After a month, I had complete sign-off ability to approve an account and wire funds out. “Fascinating,” I thought.

“3 Merchant processing statements and a signed contract.” This was the industry wide standard documentation at the time. If one Cash Provider wanted more documentation than that, the ISOs could divert their business to another Cash Provider in defiance. Cash Providers spent a lot of time courting and tending to the needs of their ISOs. It was truly a day when salesmen ran the Merchant Advance world.

I remember visiting giant telemarketing centers with 50-100 people spreading the word about the Merchant Advance to thousands of people a day. At one in particular, there was a legendary ex-stock broker at the front of the room rallying the troops on a megaphone. “Sell! Sell! Sell!” The Team Captains had their names up on giant marker board with their stats for the month. Combined, they were at $2 Million in sales so far.

After I had done my “courting” and “tending” to the brass of these sales warriors, I saw a 21-year old salesman being written a check for $20,000 for a sales benchmark he had just hit. Rumor had it that he was a pizza delivery guy living out of his car just 6 weeks before. I wondered how people were making THAT much money. It was hard not to be caught up in the commotion and excitement. Nobody knew when the growth of this product would stop exploding. It wasn’t long after that when one of my fellow underwriters resigned to get in the action. I didn’t blame him, but it just wasn’t for me. I was an analytical type guy, not the sales type.

I spent my days of 2007 learning and dealing with the fact that small businesses were taking Advances simultaneously, huge commissions were paid for deals that were defaulting, 10% Closing fees were being charged, and new terminals were being sent to merchants that provided them with the opportunity to divert sales away from the Cash Providers.

This was all happening while ISOs/Providers were quadrupling their staff to deal with the surge in applications. Too much was happening at once. There were situations where Cash Providers became so overburdened and technologically unprepared, that it would take weeks just to determine what a merchant owed on their Advance. That’s not a good position to be in.

In all the madness, our team of underwriters were ahead of the game. There were alarming trends that spelled disaster. We believed the sales model had gone awry. It was $10,000 for $13,500 for our company, a profit of $3,500. It was 10% Commission + 10% closing cost + increased merchant processing rates + terminal leases, a profit of $2,000+ for the sales company. That was way too much for having no liability. There was no way these additional fees could be tacked on to what could already be considered our expensive product.

I eventually became Manager of the entire underwriting department on my platform of conservative underwriting. Boy, was I unpopular. I found myself butting heads with salesmen all day. I lobbied for more documentation and the elimination of closing costs.

What I especially subconsciously disliked, was that some Advance salesmen my age were earning 4x more than I was annually and I considered myself to be earning a hefty sum. They would debate constantly about declines and make excuses for required paperwork their merchants couldn’t produce. It was a rule that no matter how terrible the submitted application and paperwork looked, a full workup and discussion of the deal with the salesman would be had. For certain submissions, this just didn’t seem to make sense. To the salesman who worked hard for the application, it meant the world to him.

Some of us thought their over-ambitious tactics and need for closing costs were the result of greed. “A bunch of fat cat brokers”, some of us would think. Sure, there were the guys out there making $30,000 in a month, but a lot of the day-to-day calls were from guys only making 1.5% on the Advance amount, only a portion of the closing cost, and had no idea what bankcard residuals were.

It didn’t faze me when a salesman pleaded that he had been pitching a particular merchant for over 3 months and the excuse for why his May processing statement was missing. “No statement, no funding,” I asserted. Rules were rules and I would not put up with someone trying to circumvent them. The merchant probably would’ve been just fine too.

Our underwriting group took a lot of heat from the Execs at our company. Conservative underwriting jeopardized demand. It was a terrible cost-benefit debacle that we faced day in and day out. Sounds similar to the mortgage broker/ bank dilemma eh?

FAST FORWARD……

It was late Summer, 2008. Our company was stable and in good hands. I basked in our accomplishment. Some of our competitors hadn’t been so lucky. Like the friend of mine who left before me over a year before, I wanted in on the action. I resigned and became a salesman.

I never wanted to manage an ISO, I wanted to be a salesman on the front lines. I wanted the ringing phones, the commotion, the marker boards with stats, the glory, the $20,000 checks.

I became an Advance salesman at the worst time in history. Fast Capital had long gone, Merit left the arena, and some of the good ‘ol boys had changed to renewals only. Submitted applications were responded to by computer programs saying my deal was ‘automatically declined due to something or other” and would not even be reviewed. “How could my deal not get reviewed? I spent 30 days pitching this merchant only to find out he wasn’t even worthy of review?” My subsequent calls were met by agitated voices at Cash Providers who couldn’t comprehend why I wanted to know the status only 2 days after I submitted the application.

I shrugged it off in the beginning. In fact I found myself not even submitting a large chunk of the applications I generated because they didn’t look like approval material. That was the underwriter in me. I learned it to be a harmful habit.

It was 10 straight declined deals later that I found myself wondering if I should submit everything I get just to make something happen. I extended the streak to 15 declines and my subsequent phone calls to Cash Providers were met with cold responses about Policy, Policy, Policy. “No Statement, No funding,” I was told. My argument that my merchant could not provide his November merchant statement went unheard. They could not understand why I was trying to circumvent rules. I wasn’t. The streak was extended to 20 declined deals. “Under 500 FICO, too many NSFs, landlord reference insufficient, volume under $5,000, etc.” Some would suggest certain marketing campaigns produce low quality merchants. Maybe, maybe not.

The streak was extended to 25 declined deals and a merchant I had been pitching for literally 4 months was finally giving me a shot. The sweat, the stress, and the dwindling commission paychecks led to the addition of a 2% closing cost on the deal. The merchant ok’d it and signed my form. My stats on the marker board were pathetic and I was far from glory. What happened next is ironic.

The Cash Provider got wind of the closing cost and called our office. Something was said about greed and overburdening their merchant. A warning was issued and they were going to watch my submissions more closely. 25 straight declined submissions done via a computer program e-mailing me a notice of decline with no human discussion, 4 months of sweat in closing a deal, and only a quarter of that 2% closing cost actually going into my pocket. That’s pre-tax by the way. Now I’m on their watch list.

I’ve got to appreciate the irony of it all. I understand where the Cash Providers are coming from. I’ve seen it through their eyes. The power is back in the Cash Providers hands but it has become too much so.

With restrictions so tight, our collective target merchant has relatively good credit, money in the bank, current with all their vendors and rent, consistent processing, sufficient gross sales, and be able to submit a large amount of paperwork. These merchants are harder to come by and many of the amateur salesmen will not be able to close someone like that. Ironically, I personally obtained a credit card last week with 0% APR for 12 months with a $20,000 limit. I submitted no documents and spoke to no one. All I did was fill in my info online.

Cash Providers charge an $8,000 fee for $20,000 and we all know the hoops the applicants have to jump through to get there. Interesting. Makes me think 1.40 factor rates will not last forever regardless of any credit crisis.

The Cash Providers that brag, “We have ISOs that submit 10 deals a month and get 10 approvals” should realize they surely generated way more applications than that. They just sent the ones they knew you would approve. Marketing and overhead costs were incurred on all of them.

Many are shouting that only the strong will survive in this new world order of Merchant Advances. I think lending will free up again one day and all the Cash Providers that think providing ISO support means having a computer program spit out automated response e-mails and a toll free number that no one of decision making capacity answers will find themselves alone. There should be a bit more “courting” and “tending” to the ISO’s needs. They need you badly right now and you can’t live without them.

Perhaps I’m just ahead of the game again. Maybe I should apply for an underwriting job.