MCA Company Files 15 COJs Against a Medical Practice, Dispute Arises Over Alleged Forgery

May 29, 2019 A New Jersey physician was one day going about his usual business, and the next day found himself an unwitting judgment debtor for almost $2,000,000 based on more than a dozen forged Confessions of Judgment (COJs) of which he had no knowledge. That’s the scenario described in papers by the physician’s attorney suing New York-based Itria Ventures, LLC. Itria is a subsidiary of its more well known parent company Biz2Credit.

A New Jersey physician was one day going about his usual business, and the next day found himself an unwitting judgment debtor for almost $2,000,000 based on more than a dozen forged Confessions of Judgment (COJs) of which he had no knowledge. That’s the scenario described in papers by the physician’s attorney suing New York-based Itria Ventures, LLC. Itria is a subsidiary of its more well known parent company Biz2Credit.

In the span of 19 months, Itria funded a medical practice 19 times (an average of once a month), putting the practice on the hook for millions of dollars in purchased receivables. In March 2017, Itria declared one of those agreements to be in default and filed a COJ in the Supreme Court of New York, successfully securing a judgment in the amount of $245,114. Despite this, Itria continued to enter into at least 3 more funding contracts with them after defaulting.

The relationship would sour as Itria attempted to enforce its New York judgment in New Jersey with vigor. According to Court papers filed in Bergen County, Itria sought to have a judgment debtor, a doctor, arrested after he allegedly did not respond to an information subpoena or attend a deposition. In September 2018, a judge denied Itria’s application for an arrest warrant as the parties were reportedly in discussions to resolve.

When those discussions failed, Itria claimed that 14 more of the 19 contracts were also in default as they went ahead and filed 14 new COJs against the medical practice parties in March 2019. All told, Itria’s judgments add up to around $1.9 million. And just as Itria had previously, they began the procedure to enforce them.

But there’s a twist. The COJs and the contracts might have forged signatures for one of the parties.

On April 18th, Itria Ventures was sued by the very same doctor they sought to have arrested.

“Those confessions of judgment appear to bear my signature and have been filed against me but are fraudulent and forgeries because I did not sign them and the signature on them is not mine,” the plaintiff argued. Itria is a co-defendant alongside several entities that make up the medical practice, two notaries, Itria’s attorneys, and the plaintiff’s own brother, who is also a doctor.

Plaintiff’s claims of forgeries are onerous given that notaries were present, but the evidence is compelling given that on several contracts a notary attested that he appeared before her to sign it when there is surprisingly no signature there at all.

“This is a fraud even the most sophisticated lawyers would have trouble spinning in their favor. This fraud is shocking to the conscience,” the plaintiff’s attorney argued.

In instances where plaintiff’s signature is present, plaintiff alleges that his brother forged his signature and that the notaries fraudulently went along with it. In addition to the alarming variations in his signature, the plaintiff’s attorney pointed out an instance where a signature appears to be not only forged but a photocopied forgery.

Accordingly, the plaintiff is seeking to have all the judgments as they pertain to him personally, vacated.

Itria wasn’t convinced the allegations held weight given that it was the first time forgery had been raised in 2 years of communications. Documents filed appear to show there have been discussions to resolve for some time. They separately pressed forward on May 13th to have a Court appoint a post-judgment receiver over the medical practice.

Itria has relayed to AltFinanceDaily that their enforcement efforts have been in compliance with all laws and court rules and that they’ve worked with these debtors in a cooperative fashion to attempt to provide them with the opportunity to resolve their financial difficulties. For example, Itria says they (a) provided these debtors with a reduced/modified payment plan, (b) provided them, for an extended period of time, with a de facto forbearance from enforcement to allow them to ‘catch their breaths,’ and to attempt to resolve their financial difficulties by seeking financing elsewhere or otherwise , and (c) at the debtor’s request, assisted them in attempting to obtain alternate financing for many of their business needs, not just to make Plaintiffs whole.

On May 29th, the judge ordered a preliminary injunction enjoining Itria from enforcing the 15 judgments against the plaintiff only and any other judgments “purportedly executed by plaintiff.” The catch is that the plaintiff must post a $1.3 million bond by June 7th. If it’s ultimately determined that the injunction was not warranted, the plaintiff will be responsible for all of Itria’s costs and damages related to the injunction. Itria is not enjoined, however, from enforcing the judgments against any of the plaintiff’s co-defendants.

The case is listed under Index Number 154067/2019 in The New York County Supreme Court.

Does The Borrower Even Exist? Image Algorithms, Site Inspectors Spot The Fakers

May 24, 2019 Their product research lab was the real deal. That’s what a business seeking capital hoped to convince a lender of when they snapped a photo of a $450,000 microscope and sent it over to underwriting along with two dozen other photos of their warehouse.

Their product research lab was the real deal. That’s what a business seeking capital hoped to convince a lender of when they snapped a photo of a $450,000 microscope and sent it over to underwriting along with two dozen other photos of their warehouse.

Most of the pictures were genuine, but the microscope was not. Truepic, a virtual site inspection and photo verification company that the lender had relied on, algorithmically determined that the microscope was actually a photo of a photo, one that had been grabbed off the web.

If they had just emailed these photos directly to the lender, the loan would’ve been issued, but this image analyzing technology changed everything.

Truepic founder and COO Craig Stack said that they were able to identify the false ones because of software they have that can detect when a photo is being taken of a two-dimensional image. Truepic didn’t just obtain the photos, they were taken in real time using their mobile photo-taking app. In addition to detecting only two dimensions, Truepic also found the real photos online through a reverse-image search to show where the photos came from.

Photo verification isn’t brand new. Nationwide Management Services has been providing these very same services to their customers since 2015, according to its CEO John Marsh. Marsh started his company in 2005 and originally provided traditional on-site inspections with certified field agents taking pictures.

“You can’t tell the difference,” Marsh said of photos taken by a field agent, compared to those taken virtually by the owner of the store or office. In the virtual one, the merchant receives a text and clicks on a link that essentially turns the merchant’s phone into a live video feed for the lender.

Commonly, the lender wants to see, among other things, the company’s signage, credit card machine and merchant’s driver’s license. Using GPS technology, Nationwide Management Services can tell exactly where the merchant is, so they can’t be taking photos – in real time – of a different store.

Marsh still offers on-site inspection for clients, but mostly as discreet, unannounced visits to check up on a merchant that is having a hard time making payments. Sometimes a field agent will find that a direct competitor moved in across the street or the neighborhood is declining and there are a number of vacant stores, Marsh said.

Marsh still offers on-site inspection for clients, but mostly as discreet, unannounced visits to check up on a merchant that is having a hard time making payments. Sometimes a field agent will find that a direct competitor moved in across the street or the neighborhood is declining and there are a number of vacant stores, Marsh said.

Marsh’s virtual video verification product is instantaneous, allowing the lender to see the merchant’s space – and face – in real time, virtually eliminating misrepresentation of the merchant’s store. Stack said that Truepic also has a video verification product that they will be releasing in less than three weeks.

Marsh said that would-be merchant fraudsters get scared as soon as they hear about a real time virtual inspection.

“When we reach out to them for the virtual inspection, they go dark,” Marsh said.

Most of the deception Marsh has encountered is of merchants giving a P.O. Box address as the address of their “physical store.”

Gayle Juhl, President and CEO of Metro Inspections, said that one of her field agents found a merchant with a far more unusual distortion of its company address. The field agent went to the address of the merchant only to find a 1970s bright blue Volvo station wagon with a sign on it, parked in front of the address listed, which belonged to a completely different store.

The man seeking funding, who came out of the car-turned-store, was apparently confrontational, according to the field agent’s report.

Juhl said that she will coordinate a virtual inspection upon request, but that her company primarily does onsite inspections.

“You can’t replace a handshake and an eye-to-eye to see what’s really going on,” Juhl said.

This may be true, but Marsh said that it can take 24 to 48 hours to collect photos for his onsite inspections whereas it can take as little as four minutes with his virtual video or virtual photo services. (This depends on how many images the lender is looking to capture.) Granted, Juhl said that Metro Inspections’ on-site inspections can be collected and delivered on the same day it was requested, given that the request comes early enough in the day.

Stack, who has only been servicing the online lending industry for about five months, says that he has gotten financial services clients who are very excited about the speed of virtual inspections and the fact that they are far less invasive for the merchant. Rather than have a stranger come in to take pictures – raising questions among employees and customers – the business owner can discreetly photograph their space at their convenience. Stack’s company has never offered onsite inspections and says he never will.

“Our camera doesn’t lie,” he said.

Canada’s Alternative Financing Market Is Taking Off

May 20, 2019

Canadians have been slow out of the gate when it comes to mass adoption of alternative financing, but times are changing, presenting opportunities and challenges for those who focus on this growing market.

Historically, the Canadian credit market has traditionally been dominated by a few main banks; consumers or businesses that weren’t approved for funding through them didn’t have a multitude of options. The door, however, is starting to unlock, as awareness increases about financing alternatives and speed and convenience become more important, especially to younger Canadians.

Indeed, the Canada alternative finance market experienced considerable growth in 2017—the latest period for which data is available. Market volume reached $867.6 million, up 159 percent from $334.5 million in 2016, according to a report by the Cambridge Centre for Alternative Finance and the Ivey Business School at Western University. Balance sheet business lending makes up the largest proportion of Canadian alternative finance, accounting for 57 percent of the market; overall, this model grew 378 percent to $494 million in 2017, according to the report.

Industry participants say the growth trajectory in Canada is continuing. It’s being driven by a number of factors, including tightening credit standards by banks, growing market demand for quick and easy funding and broader awareness of alternative financing products.

To meet this growing demand, new alternative financing companies are coming to the market all the time, says Vlad Sherbatov, president and co-founder of Smarter Loans, which works with about three dozen of Canada’s top financing companies. He predicts that over time more players will enter the market—from within Canada and also from the U.S.—and that product types will continue to grow as demand and understanding of the benefits of alternative finance become more well-known. Notably, 42 percent of firms that reported volumes in Canada were primarily headquartered in the U.S., according to the Cambridge report.

To meet this growing demand, new alternative financing companies are coming to the market all the time, says Vlad Sherbatov, president and co-founder of Smarter Loans, which works with about three dozen of Canada’s top financing companies. He predicts that over time more players will enter the market—from within Canada and also from the U.S.—and that product types will continue to grow as demand and understanding of the benefits of alternative finance become more well-known. Notably, 42 percent of firms that reported volumes in Canada were primarily headquartered in the U.S., according to the Cambridge report.

To be sure, the Canadian market is much smaller than the U.S. and alternative finance isn’t ever expected to overtake it in size or scope. That’s because while the country is huge from a geographic standpoint, it’s not as densely populated as the U.S., and businesses are clustered primarily in a few key regions.

To put things in perspective, Canada has an estimated population of around 37 million compared with the U.S.’s roughly 327 million. On the business front, Canada is similar to California in terms of the size and scope of its small business market, estimates Paul Pitcher, managing partner at SharpShooter, a Toronto-based funder, who also operates First Down Funding in Annapolis, Md.

Nonetheless, alternative lenders and funders in Canada are becoming more of a force to be reckoned with by a number of measures. Indeed, a majority of Canadians now look to online lenders as a viable alternative to traditional financial institutions, according to the 2018 State of Alternative Lending in Canada, a study conducted by online comparison service Smarter Loans.

Of the 1,160 Canadians surveyed about the loan products they have recently received, only 29 percent sought funding from a traditional financial institution, such as a bank, the study found. At the same time, interest in alternative loans has been on an upward trajectory since 2013. Twenty-four percent of respondents indicated they sought their first loan with an alternative lender in 2018. Overall, nearly 54 percent of respondents submitted their first application with a non-traditional lender within the past three years, according to the report.

Like in the U.S., there’s a mix of alternative financing companies in Canada. A number of companies offer factoring and invoicing and payday loans. But there’s a growing number focused on consumer and business lending as well as merchant cash advance.

Some major players in the Canadian alternative lending or funding landscape include Fairstone Financial (formerly CitiFinancial Canada), an established non-bank lender that recently began offering online personal loans in select provinces; Lendified, an online small business lender; Thinking Capital, an online small business lender and funder; easyfinancial, the business arm of alternative financial company goeasy Ltd. that focuses on lending to non-prime consumers; OnDeck, which offers small business financing loans and lines of credit; and Progressa, which provides consolidation loans to consumers.

By comparison, the merchant cash advance space has fewer players; it is primarily dominated by Thinking Capital and less than a dozen smaller companies, although momentum in the space is increasing, industry participants say.

“The U.S. got there 10 years ago, we’re still catching up,” says Avi Bernstein, chief executive and co-founder of 2M7 Financial Solutions, a Toronto-based merchant cash advance company.

OPPORTUNITIES ABOUND

In terms of opportunities, Canada has a population that is very used to dealing with major banks and who are actively looking for alternative solutions that are faster and more convenient, says Sherbatov of Smarter Loans. This is especially true for the younger population, which is more tech-savvy and prefers to deal with finances on the go, he says.

Because the alternative financing landscape is not as developed in Canada, new and innovative products can really make a significant impact and capture market share. “We think this is one of the key reasons why there’s been such an influx of international companies, from the U.S. and U.K. for example, that are looking to enter the Canadian market,” he says.

Just recently, for example, Funding Circle announced it would establish operations in Canada during the second half of 2019. “Canada’s stable, growing economy coupled with good access to credit data and progressive regulatory environment made it the obvious choice,” said Tom Eilon, managing director of Funding Circle Canada, in a March press release announcing the expansion. “The most important factor [in coming to Canada] though was the clear need for additional funding options among Canadian SMEs,” he said.

OnDeck, meanwhile, recently solidified its existing business in Canada through the purchase of Evolocity Financial Group, a Montreal-based small business funder. The combined firm represents a significantly expanded Canadian footprint for both companies. OnDeck began doing business in Canada in 2014 and has originated more than CAD$200 million in online small business loans there since entering the market. For its part, Evolocity has provided over CAD$240 million of financing to Canadian small businesses since 2010.

“There is an enormous need among underserved Canadian small businesses to access capital quickly and easily online, supported by trusted and knowledgeable customer service experts,” Noah Breslow, OnDeck’s chairman and chief executive, said in a December 2018 press release announcing the firms’ nuptials.

There are also a number of home grown Canadian companies that are benefiting from the growth in the alternative financing market.

2M7 Financial Solutions, which focuses on merchant cash advances, is one of these companies. It was founded in 2008 to meet the growing credit needs within the small and medium-sized business market at a time when businesses were having trouble in this regard.

But only in the past few years has MCA in Canada really started picking up to the point where Bernstein, the chief executive, says the company now receives applications from about 200 to 300 companies a month, which represents more than 50 percent growth from last year.

“We’re seeing more quality businesses, more quality merchants applying and the average funding size has gone up as well,” he says.

NAVIGATING THROUGH CHALLENGES

Despite heightened growth possibilities, there are also significant headwinds facing companies that are seeking to crack the Canadian alternative financing market. For various reasons, some companies have even chosen to pull back or out of Canada and focus their efforts elsewhere. Avant, for example, which offers personal loans in the U.S., is no longer accepting new loan applications in Canada at this time, according to its website. Capify also recently exited the Canadian business it entered in 2007, even as it continues to bulk up in the U.K. and Australia.

One of the challenges alternative lenders face in Canada is distrust of change. Since Canadians are so used to dealing with only a few major financial institutions to handle all their finances, they are skeptical to change this behavior, especially when the customer experience shifts from physical branches to online apps and mobile devices, says Sherbatov of Smarter Loans. He notes that adoption of fintech products in Canada has lagged in recent years, partially because there has been a lack of awareness and trust in new financial products available.

One way Smarter Loans has been working to strengthen this trust is by launching a “Smarter Loans Quality Badge,” which acts as a certification for alternative financing companies on its platform. It is issued to select companies that meet specified quality standards, including transparency in fees, responsible lending practices, customer support and more, he says.

![]() The Canadian Lenders Association, whose members include lenders and merchant cash advance companies, has also been working to promote the growing industry and foster safe and ethical lending practices. For example, it recently began rolling out the SMART Box pricing disclosure model and comparison tool that was introduced to small businesses in the U.S. in 2016.

The Canadian Lenders Association, whose members include lenders and merchant cash advance companies, has also been working to promote the growing industry and foster safe and ethical lending practices. For example, it recently began rolling out the SMART Box pricing disclosure model and comparison tool that was introduced to small businesses in the U.S. in 2016.

Another challenge that impacts alternative lenders in the consumer space is having restricted access to alternative data sources. Because of especially strict consumer privacy laws, access is “substantially more limited” than it is in any other geography,” says Jason Mullins, president and chief executive of goeasy, a lending company based in Mississauga, Ontario, that provides consumer leasing, unsecured and secured personal loans and merchant point-of-sale financing.

From a lending perspective, goeasy focuses on the non-prime consumer—generally those with credit scores of under 700. Mullins says the market consists of roughly 7 million Canadians, about a quarter of the population of Canadians with credit scores. The non-prime consumer market is huge and has tremendous potential, he says, but it’s not for the faint of heart.

Another issue facing alternative lenders is the relative difficulty of raising loan capital from institutional lenders, says Ali Pourdad, co-founder and chief executive of Progressa, which recently reached the $100 million milestone in funded loans for underserved Canadian consumers. “The onus is on the alternative lenders to ensure they have good lending practices and are underwriting responsibly,” he says.

What’s more, household debt to income ratios in Canada are getting progressively worse, with Canadians taking on too much debt relative to what they can afford, Pourdad says. As the situation has been deteriorating over time, there is inherently more risk to originators as well as the capital that backs them. “Originators, now more than ever, have to be cautious about their lending practices and ensure their underwriting is sound and that they are being responsible,” he says.

On the small business side of alternative lending, getting the message out to would-be customers can be a challenge in Canada. In U.S. there are thousands of ISOs reaching out to businesses, whereas in Canada, most funders have a direct sales force, with a much smaller portion of their revenue coming from referral partners, says Adam Benaroch, president of CanaCap, a small business funder based in Montreal.

He predicts this will change over time as the business matures and more funders enter the space, giving ISOs the ability to offer a broader array of financing products at competitive rates. “I think we’re going to see pricing go down and more opportunities develop, and as this happens, the business is going to grow, which is exactly what has happened in the U.S,” he says.

Generally speaking, Canadian businesses are still somewhat skeptical of merchant cash advance and require considerable hand-holding to become comfortable with the idea.

“You can’t wait for them to come to you, you have to go to them and explain what the products are,” says Pitcher of SharpShooter, the MCA funding company.

While Pitcher predicts more companies will continue to enter the Canadian alternative financing market, he doesn’t think it will be completely overrun by new entrants—the market simply isn’t big enough, he says. “It’s not for everyone,” he says.

Merchant Relationship Status: It’s Complicated

May 14, 2019

Brokers will often say that building strong relationships with their merchants is critical to their success. John Celifarco, Managing Partner at Horizon Financial Group, a five person ISO in Brooklyn, said that the advantage they have over larger competitors is the relationships they’ve developed with their merchants. Celifarco’s office is even in a streetfront store, where a number of their merchants are actually neighboring stores. Celifarco sees this as a strength.

But Michael Bernier, Vice President of 1 West Finance, a 14-person brokerage based in New York, said that things have changed as competition has increased in the space.

Customers gravitate towards companies that can provide them with not only the best pricing, but also the best user experience, which is why we believe so many new players in the space have achieved scale so quickly.

While customer relationships are important, funders in the space that are improving their speed, efficiency, and pricing are going to win the deals.

“In general, if [end users] find a better price on Amazon, 9 times out of 10 they’re going to buy that product on Amazon, regardless of the sales person on the phone” Bernier said.

Bernier suggests that rate or speed may win the customer but another more legally-binding circumstance may guide the relationship accordingly.

Kapitus CEO Andy Reiser served as moderator.

“Contractually, we own the customer,” said National Funding CEO Dave Gilbert on a panel at Broker Fair. “But we work in conjunction with the broker.”

Fellow panelist and Chairman of Rapid Finance, Jeremy Brown, said that he used to say what Gilbert said, but now says: “We own the loan. [And] we have the right to first renew the customer.”

Brokers seeking a very cozy relationship with their clients should therefore consider what rights and responsibilities are afforded to them under their referral contracts so that there’s no confusion with actions taken by either party with the customer down the road.

“I get close to people very quickly, it’s just who I am,” Kemp, a broker, told AltFinanceDaily in an interview last year. “And in my opinion it works to my advantage because I have merchants that renew with me multiple times a year. And I know that no matter how many calls they get [from other brokers], they’re going to turn to me. I know that they trust me.”

Likewise, Chad Otar, CEO of Excel Capital in New York, has said that building trust with merchants is very important and is what leads to renewal business. Otar introduced one of his merchants, a marketing company, to his other clients. A few of them ended up working with the marketing company, which was a win for everyone and led to even stronger word of mouth from Otar’s merchants.

“I don’t think anyone owns the customer,” said CEO of BFS Capital Mark Ruddock on the panel alongside Gilbert and Brown. “Customers are a privilege, not a right.”

So God Made a Farmer, But Who’s Financing The Farms?

May 1, 2019 Most mornings, farmers and ranchers wake up worrying about uncooperative weather and volatile commodity prices. Just the same, they pull themselves out of bed to spend the morning tinkering with crotchety machinery or wrangling uncooperative livestock. When they break for lunch, the kitchen radio alerts them to trade wars with distant countries and the unintended results of federal regulation. As they make their way back outdoors for the afternoon’s work, they can’t help but notice another new house taking shape in the distance as suburban sprawl encroaches on the fields and pastures. By evening, their thoughts have turned to their need for short-term capital and how the local banker seems increasingly wary of providing funds.

Most mornings, farmers and ranchers wake up worrying about uncooperative weather and volatile commodity prices. Just the same, they pull themselves out of bed to spend the morning tinkering with crotchety machinery or wrangling uncooperative livestock. When they break for lunch, the kitchen radio alerts them to trade wars with distant countries and the unintended results of federal regulation. As they make their way back outdoors for the afternoon’s work, they can’t help but notice another new house taking shape in the distance as suburban sprawl encroaches on the fields and pastures. By evening, their thoughts have turned to their need for short-term capital and how the local banker seems increasingly wary of providing funds.

It’s that last challenge where the alternative small-business funding industry might be able to help, says Peter Martin, a principal at K-Coe Isom, an accounting and consulting firm focused on the ag industry. “If you as a farmer need operating funds and you can’t get them from a bank, you don’t have a lot of options,” he says. “Historically, nobody outside of banks has had much interest in lending operating money to a farmer.”

The result of that reluctance to provide funding? “I can’t tell you the number of calls I get to say, ‘Hey, I need $100,000 and I need it in a couple of days because of X, Y, Z that’s come up,’” says Martin. “We don’t have a place that we can send those people to. You could make a lot of quick turnaround loans in rural America.” What’s more, it’s a potential clientele that makes a lot of money and prides itself on paying back what they owe.

Martin’s not alone in that assessment. While farmers enjoy abundant long-term credit to buy big-ticket assets, such as land and heavy machinery, they’re struggling to find sources of short-term credit for operating expenses like labor, repairs, fuel, seed, feed, fertilizer, herbicides and pesticides, notes Mike Gunderson, Purdue University professor of agricultural economics.

But remember that nobody’s saying it would be easy for alt funders to break into the agricultural sector. City folks accustomed to the fast-paced rhythms of New York or San Diego would have to learn a whole new seasonal business cycle. Grain farmers, for example, plant corn and soybeans in April, harvest their crops September or October, and may not sell the grain until the following January, says Nick Stokes, managing director of Conterra Asset Management, an alternative-funding company that places and services rural real estate loans.

But remember that nobody’s saying it would be easy for alt funders to break into the agricultural sector. City folks accustomed to the fast-paced rhythms of New York or San Diego would have to learn a whole new seasonal business cycle. Grain farmers, for example, plant corn and soybeans in April, harvest their crops September or October, and may not sell the grain until the following January, says Nick Stokes, managing director of Conterra Asset Management, an alternative-funding company that places and services rural real estate loans.

That seasonality results in revenue droughts punctuated by floods of revenue – a circumstance far-removed from the more-consistent credit card receipt split that launched the alternative small-business funding industry. Alternative funders seeking customers with consistent monthly cash flow won’t find them in the agricultural sector, Stokes cautions.

And while the unfamiliarity of farm life might begin with wild swings in cash flow, it doesn’t end there. Operating in the agricultural sector would require urbanites to learn the somewhat alien culture of The Heartland – a way of life based on hard physical labor, the fickle whims of the weather, and friendly unhurried conversations, even with strangers.

Even so, the task of mastering the agricultural funding market isn’t hopeless, and help’s available. Experts in agricultural economics profess a willingness to help outsiders learn what they need to know to get involved. “Selfishly, the first place I’d love to have them reach out to is me,” Martin says of alternative funders. “I’ve been writing and thinking for years about the importance of getting some non-traditional lenders into agriculture.” He would have “no qualms” about featuring specific prospective funders in a column he writes for one of the nation’s largest farm publications.

It also requires meet-and-greets. During the winter, when farmers aren’t in the fields, funders could make connections at trade shows, Martin advises. “Word would get around rural America really quick,” he predicts. Networking with advisers such as crop insurance agents, agronomists and ag CPS’s – all of whom deal with farmers daily – would also help funders find their way in agriculture, he contends.

It also requires meet-and-greets. During the winter, when farmers aren’t in the fields, funders could make connections at trade shows, Martin advises. “Word would get around rural America really quick,” he predicts. Networking with advisers such as crop insurance agents, agronomists and ag CPS’s – all of whom deal with farmers daily – would also help funders find their way in agriculture, he contends.

Investors who are curious about extending credit in the agricultural sector could rely upon Conterra to help them locate customers and help them service the loans, says Stokes. He can even help acclimate them to the world of agriculture. “If they’re interested in investing in agricultural assets – whether that be equipment, real estate or providing operating capital – we would enjoy the opportunity to visit with them,” he says.

GETTING STARTED

Alt funders could begin their introduction to the agrarian lifestyle by taking to heart a quotation attributed to President John F. Kennedy: “The farmer is the only man in our economy who buys everything at retail, sells everything at wholesale and pays the freight both ways.”

“Agriculture is a very different animal,” Martin notes. He sometimes presents a slide show to compare the difference between a typical farm and a typical manufacturer of the same size. At the factory, revenue ratchets up a bit each year and margins remain about the same over time. On the farm, revenue and margins both fluctuate wildly in huge peaks and valleys from one year to the next.

The volatility makes it difficult to manage the risk of lending, Martin admits, while noting that agriculturally oriented banks still have higher returns than non-ag banks, according to FDIC records. “You have to go back to 2006 to find a time when ag banks didn’t outperform their peers on return on assets,” he says. “What this tells us is that, generally speaking, ag borrowers are better at repaying their loans,” he asserts. Charge-offs and delinquencies in ag portfolios are lower than in other industries, he says.

Many of the nation’s farms have remained in the same family for more than a century – a stretch of time that’s seldom seen in just about any other type of business. Besides making potential creditors comfortable that a particular operation will stay in business, the longevity of farms provides lots of documents to examine – not just tax records but also production history that’s tracked by government agencies. A particular farmer’s crop yields, for example, can be compared with county averages to calculate how good the borrower is at farming.

Debt to asset ratio on the nation’s farms stands at about 14 percent, which Martin views as “insanely low.” But that’s not the case on every farm. Highly leveraged farms have ratios of 60 percent or even 80 percent when farmers have grown their businesses quickly or encountered debt to buy land from their parents, he says. Commodity prices are low now, but farms with 14 percent debt to asset ratios still don’t have a problem, even in hard times. Farmers deeply in debt, however, have little ability to climb out of the hole. The latter are using operating capital to fund losses.

Farmers with debt to asset ratios of 10 percent have little trouble finding credit and aren’t going to pay anything other than bank rates, Martin says. The target audience for non-traditional funding are farmers who are having trouble but will be fine when commodity prices rebound. Another potential client for alternative finance would be farmers who are quickly increasing the size of their operations when opportunities arise to acquire land. Both groups need funders willing to contemplate the future instead of demanding a perfect track record, he maintains.

Farmers with debt to asset ratios of 10 percent have little trouble finding credit and aren’t going to pay anything other than bank rates, Martin says. The target audience for non-traditional funding are farmers who are having trouble but will be fine when commodity prices rebound. Another potential client for alternative finance would be farmers who are quickly increasing the size of their operations when opportunities arise to acquire land. Both groups need funders willing to contemplate the future instead of demanding a perfect track record, he maintains.

Farmers generally need loans for operating capital for about 18 months, according to Martin. “Let’s say I borrow that money, get my crop in the ground, harvest that and I may not sell my grain right after harvest,” he says. The whole cycle can easily take 18 months, he says. Shorter-term bridge lending opportunities also arise in situations like needing a little extra cash quickly at harvest time. Farmers usually have something to put up as collateral – like producing 50 titles to vehicles or offering up some real estate, he says.

An unsecured loan – even one with high double-digit interest – could succeed in agriculture because no one is offering that type of funding, Martin says. Small and medium-sized farms would probably benefit from funding of $100,000 or less, while larger farms might sign up for that amount but often require more, he notes.

LAY OF THE LAND

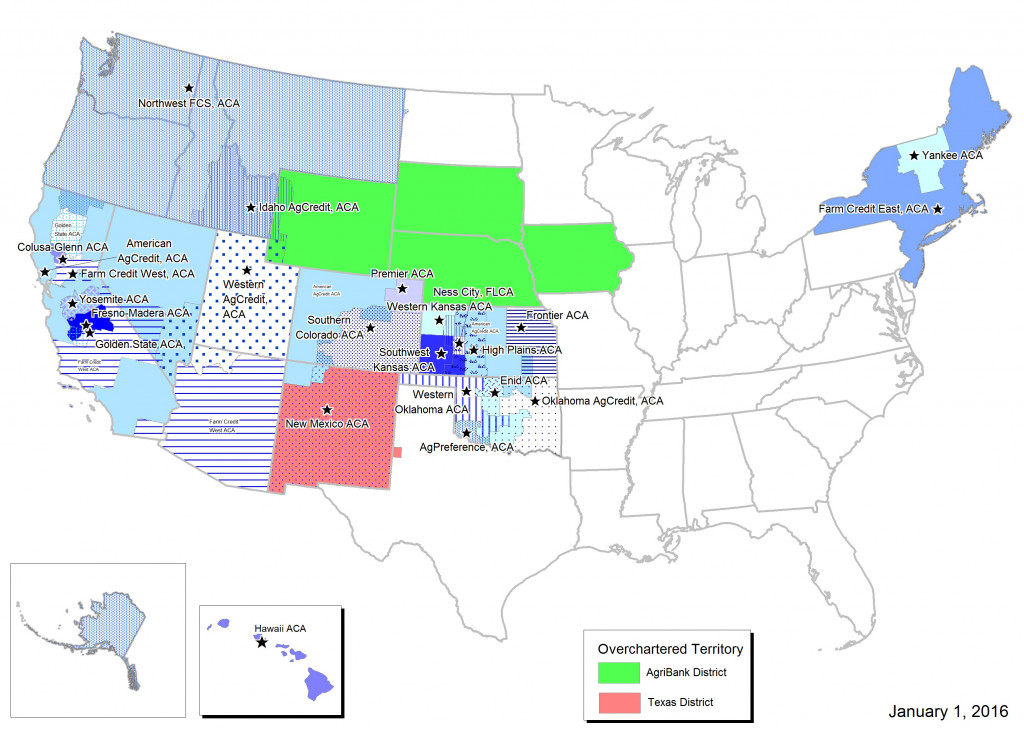

The Farm Credit System, a nationwide quasi-governmental network of borrower-owned lending institutions, provides more than a third of the credit granted in rural America. That comes to more than $304 billion annually in loans, leases and related services to farmers, ranchers, rural homeowners, aquatic producers, timber harvesters, agribusinesses, and agricultural and rural utility cooperatives, according to published reports.

Congress established the Farm Credit System in 1916, and the Farm Credit Administration was established in 1933 to provide regulatory oversight. “All they’re doing is lending money to agriculture,” says Martin.

However, the system can go astray in the eyes of some observers. An arm of the Farm Credit System called CoBank lends to co-operatives and other rural entities. At one point Verizon Wireless became a borrower from CoBank, which angered some observers because the system was supposed to be helping rural America, not corporate America, Martin says.

That anger arises partly because the federal government doesn’t require Farm Credit to pay income tax, which enables it to lend at lower rates, Martin says. “Part of the allure of borrowing from Farm Credit is you can typically borrow cheaper,” he notes. “You’d be very hard pressed to find a farmer who over the years hasn’t had some interaction with Farm Credit.”

Observers sometimes fault the system for what they perceive as a tendency to extend credit only to those who don’t really need it, notes Purdue’s Gunderson. People working for the system believe they’re doing a good job of supporting agriculture, he says, noting that the system is charged with the responsibility of helping new and young farmers.

Another entity, the Federal Agricultural Mortgage Corp., also known as Famer Mac, works with lending institutions to provide credit to the agricultural sector. It’s a publicly traded company that serves as a secondary market in agricultural loans, including mortgages. It purchases loans and sells instruments backed by those loans and was chartered in 1988. Conterra, the alternative-funding company mentioned earlier in this article, -works with Farmer Mac and financial institutions to make real estate loans to farmers and ranchers in financial distress. The loans are designed to help borrowers get back on their feet in three to five years so that they would then qualify for regular bank loans.

Then there are the ag lending divisions at the large banks such as Wells Fargo, Chase and the Bank of the West, Martin says. “Lots of these big national banks are doing at least some ag lending,” he says. “Some, obviously, have bigger ag portfolios than others.”

Some regional banks focus on agriculture, Martin continues. “When you get into the middle of the corn belt, there are going to be some regional banks where traditional ag lending’s a huge part of what they do,” he says. Local banks in small towns get involved, too. “Most small community banks are going to have some kind of ag lending portfolio,” Martin notes. Hometown bankers can provide operating capital to some farmers, but only to those who haven’t experienced recent hiccups in revenue or expenses.

THE NON-BANKS

“Then you get into the non-bank lenders,” Martin observes. “A really good example of this is John Deere,” the tractor and equipment manufacturer. The company provides a tremendous amount of capital to rural America through equipment lending and also through other credit facilities, he says. In fact some observers estimate that John Deere is the largest lender to agriculture. Even so, the company usually doesn’t provide enough non-equipment credit to become the only lender a farmer would use, he says.

“Then you get into the non-bank lenders,” Martin observes. “A really good example of this is John Deere,” the tractor and equipment manufacturer. The company provides a tremendous amount of capital to rural America through equipment lending and also through other credit facilities, he says. In fact some observers estimate that John Deere is the largest lender to agriculture. Even so, the company usually doesn’t provide enough non-equipment credit to become the only lender a farmer would use, he says.

The same holds true with other lenders to agriculture, Martin says. Co-operatives, for example, lend money to agriculture even though they’re not banks. Typically, they begin by extending credit for products like seed, fertilizer or pesticides and then start making additional credit available to farms and ranches. In recent years, a large co-operative called CHS loaned hundreds of millions of dollars in addition to selling products on credit. Some large CHS loans went bad caused a ripple effect throughout the cooperative structure, Martin maintains. Other co-ops have looked at CHS and wondered if they’re moving too far outside their core competency. So now many co-ops are tying funding to products they’re selling.

Some other non-bank lenders have shown up in agriculture, and they fall into two categories, Martin says. One group is making real estate loans in agriculture, so their loan programs are geared to farmers looking to buy land or anything that can be secured by land. Conterra and Ag America are examples. Farmer Mac lends a lot of money against farmland, as well. So farmers who have agricultural land have a lot of access to capital and a lot of lenders who want to provide it, he says.

The second group of non-bank lenders is providing operating capital. “That is a very, very small club,” Martin says. “There’s really not anybody doing this on a regular basis – with just one or two exceptions.” Probably the biggest name among the exceptions is Ag Resource Management, usually known as ARM, he continues. ARM places a value on the potential productivity of a famer’s land. Then it looks at the crop insurance the farmer’s able to buy to protect the investment in that crop. ARM then lends part of the value of that crop insurance.

Let’s say a farmer can grow $10 million worth of crops, according to ARM’s projection,” Martin says. “You can get crop insurance to cover 80 percent,” he continues. “For a total crop failure, you will get $8 million for that crop.” Using a formula based on type of crop, location and type of crop insurance, ARM will lend some amount less than $8 million. “Their collateral is pretty rock solid,” Martin observes.

ARM uses a system to make sure farmers use the funds only for expenses related to growing the crop they’re using as collateral. “Their risk of not getting a crop in the ground that qualifies for the insurance is next to nothing,” Martin says. ARM offers differing interest rates, depending upon risk, in at least the high single digits or double digits, and they also charge fees. “So you’re going to be paying a lot, but they are the lender of last resort in agriculture right now,” he says, adding that ARM operates multiple offices has grown quickly.

Through lenders like ARM, the agricultural sector’s becoming familiar with alternative finance. But much remains to be done if alt fin pioneers want to venture into the sector. Those who do will encounter a complicated credit landscape, but one that offers opportunities for anyone willing to learn about unfamiliar business cycles and lifestyles.

Shopify Capital Issued $87.8M in Merchant Cash Advances in Q1

April 30, 2019Shopify’s small business funding division, Shopify Capital, issued $87.8 million in merchant cash advances in the first quarter of 2019, according to the company’s earnings report. The figure is a 45% increase over the same period last year. Overall, the company has funded more than $535 million in MCAs since inception.

Shopify is primarily an e-commerce platform, but they are quickly becoming a competitor to both Square and PayPal, both of whom also offer funding solutions.

Online Lender Offering “Incredible” Returns to Investors is Recording Massive Losses

March 29, 2019 StreetShares continues to rack up astronomical losses, according to the company’s recently filed unaudited financial statements. The company recorded a $6.4 million loss for the second half of 2018 on only $1.88 million in operating revenue. As in previous periods, payroll continues to be the largest expense.

StreetShares continues to rack up astronomical losses, according to the company’s recently filed unaudited financial statements. The company recorded a $6.4 million loss for the second half of 2018 on only $1.88 million in operating revenue. As in previous periods, payroll continues to be the largest expense.

StreetShares’ funding comes in part from mom & pop investors that are offered a fixed annual return of 5% regardless of how the company’s underlying loans perform. Advertisements on the website call it “incredible” and trumpet that you can “grow your money like a 2x World War champ” and that “your balance will grow every day.” The offering is called a veteran business bond but it has no government backing and can suffer a total risk of loss, all while the underlying loans may not even be made to veteran-owned businesses.

A simple explanation on the site for how it works is that you just open an account, transfer funds from your bank and then just “watch the interest start piling up.” You can withdraw your money anytime but large withdrawals over $50,000 can take up to 30 days to process, the company states. The attractive terms have allowed StreetShares to take in millions of dollars from everyday people with amounts as small as $25.

Institutional investors can earn even higher returns. Lendit Co-founder Peter Renton recently called StreetShares his “top performing investment by a long way,” beating his investments in Lending Club, Prosper, P2Binvestor, Peerstreet, Yieldstreet, Money360, Fundrise, and even the returns previously and erroneously reported by Direct Lending Investments.

AltFinanceDaily previously reported that on January 1st, Jesse Cushman, the company’s Chief Business Officer and Principal Financial & Accounting Officer, resigned. However, his name continues to remain on the website’s Leadership page a full 3 months later. The company still has not named a permanent successor. AltFinanceDaily emailed StreetShares earlier in the week about Cushman’s departure and was told that he left to pursue another opportunity. “Steve Vickrey, has been in place since before he left,” President Mickey Konson responded. Konson has been filling in as acting Principal Accounting Officer in the meantime.

In a press release published by StreetShares on Tuesday about a new credit card offering, StreetShares CEO/co-Founder & Iraq War Veteran Mark L. Rockefeller, said, “Veterans love to help other veterans. StreetShares is a veteran-run company, and the goal of the card is not only to provide a veteran focused payments tool, but also to benefit the veteran community as a whole by funding programs that benefit veteran entrepreneurship.”

Yalber Announces $20 Million Credit Facility

March 26, 2019

Yalber announced today that they have obtained a new $20 million credit facility from Park Cities Asset Management. Brean Capital served as exclusive financial advisor to Yalber on the transaction. This follows an earlier $20 million credit facility in December 2018 from a different investment fund.

“The small business funding space has drastically changed in the past two years,” said Yalber CEO Amir Landsman. “We see more and more sophisticated players in the space and to me, it’s a sign that the industry is on the right track to be the major funding source of businesses in America. Being able to close two facilities within 15 months is strong evidence that Yalber has a lot to offer.”

Yalber provides American small businesses with royalty-based investments. They can fund small businesses with up to $500,000. Founded in 2007, the company is an early player in the alternative lending space and is unique in that it generates 90 percent of its business in-house. Less than 10 percent of their leads come from ISOs, although they do look to build relationships with high quality ISOs, according to Yalber COO Amotz Segal.

Segal said that, aside from business with ISOs, all of their marketing efforts are internal and span from social media to local advertising on radio, TV and in newspapers. Yalber does not use direct mail and does not pay for leads.

“It makes the job for our salespeople a little easier because they’re not making cold calls,” Segal told AltFinanceDaily. “We [mostly] get incoming calls.”

As of the beginning of last year, Yalber had funded more than 5,000 business with over $300 million, and Segal said that they had funded approximately $65 million in 2018. On the subject of regulation, Segal said that they remain very aware of regulatory changes and they don’t necessarily see regulations as a negative thing.

Headquartered in New York, Yalber employs about 25 people and has two very small offices in Dallas and Los Angeles.