They Grew Tremendously Through the Pandemic and Landed on the List

September 26, 2022 Inc recently dropped the latest annual list of the fastest growing small businesses in the country. These 5,000 businesses span across a range of industries including health, financial, IT services and more. Companies such as Fundomate, Fountainhead, and Business Lending Blueprint have been featured on this year’s list due to incredible growth.

Inc recently dropped the latest annual list of the fastest growing small businesses in the country. These 5,000 businesses span across a range of industries including health, financial, IT services and more. Companies such as Fundomate, Fountainhead, and Business Lending Blueprint have been featured on this year’s list due to incredible growth.

For Sam Schapiro, the grit to grow Fundomate through a pandemic stemmed from a realization he came to years earlier.

“I think one of the best lessons I learned when I launched Fundomate, I was in Las Vegas at a conference to raise money,” Schapiro said. “…and barely anybody looked at us and I literally left with nothing.”

Full of doubt, Schapiro had lunch with someone he respected that had built several successful startups. That mentor told him that despite what he thought, 99.9% of the people pitching their business at the show were going to fail regardless, even if they really wanted success.

“So if you don’t really really really want it, then don’t bother doing it, because your chances of success are so slim,” Schapiro was told. That hard dose of advice led Schapiro to first question how bad he wanted it and he realized he was fully committed to seeing it through.

“I always say that if I knew how long it would take us to get here and how hard it would be to be down this road, I’d never get on the road,” Schapiro said. “But that’s the thing about life in general. Anything worth having and anything worth doing requires consistency and determination. And over and over and over again. So if something’s not working, and you can obviously see it’s not working and it’s clear, you know, the job is to keep looking at it, and at the point where it becomes a clear message that it just doesn’t work, then you got to pivot.”

Fundomate is a white label funding and banking platform for wholesale processors and MCA funders to automate their funding in a scaled way. Schapiro says that success was due in part to their technology, which collects a true daily percentage of a business’s sales.

As the pandemic subsided “we didn’t have to get back on the phone with every merchant and say, ‘Hey, we want to increase our daily payment again’ because we’re not on daily payments, we’re on instant collections that are happening on a daily basis,” Schapiro explained. “As soon as their sales came back up and even grew to get through the 2021 boom, all the sudden collections happen faster.”

Meanwhile, for Chris Hurn, Founder and CEO of Fountainhead, he had to refocus his non-bank small business lending company into a PPP loan operation.

“Pivoting our business solely to do PPP loans over the last two years was a pretty challenging experience,” said Hurn. “And we did, we worked ridiculous hours. I mean I averaged about three to four hours of sleep a night for months at a time every day. So, you know, that was probably the biggest challenge we had.”

But the work paid off. Hurn said that they were one of the most active PPP lenders over the last two years, making approximately 300,000 loans.

“Obviously, that helped accelerate our growth,” said Hurn, “as well as many of our full time hires that we made during that time are still there. And we’re still growing now.”

The process is no walk in the park when it comes to being listed on the Inc 5000. Thousands of companies apply annually to be ranked on the list. It’s months of lengthy paperwork and long-waited verifications. After realizing that one’s company has made the list, they find out their ranking along with the rest of the world.

“It’s a painstaking process because you can’t just apply and claim that you’re a growing company,” said Oz Konar, Founder at Business Lending Blueprint. “Your CPA needs to send them income verification or revenue verification, and all the things need to be documented and signed off on so they can actually prove that you’re a growing company, and you can make it on the Inc 5000.”

The hardest part of newfound success is maintaining it. With massive growth over the past four years, Konar believes growth happens when you have happy customers. Focusing on democratizing the lending space for new and existing brokers has drawn clients into his business.

“When you do things the right way consistently and stay laser focused on one problem, one solution, one product, that’s what brought us to the Inc 5000,” said Konar. “And to our surprise, we were hoping that we were going to be ranking about 1,000, the first 1,000 companies. We ranked in 799. So, it’s such an honor, we’re so happy, and we’re just getting started.”

In the competitive industry of finance that is always changing and rearranging, SMB finance companies may feel pressured to do all things for all people. But sometimes it may be more beneficial to stick to what one is good at. As Hurn can agree, it is much more complicated to compete in every marketplace.

“I think if you as a business, if you’re starting out, you need to definitely focus on a niche you want to attack and try to be the best at that,” said Hurn.

Got a Mantle, Bryant, or Mahomes Card? This Company Wants to Fund You

September 12, 2022 Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

The value of the Mantle sale came as no surprise to one budding entrepreneur in South Florida. On Instagram, he’d been talking about Mantle cards for weeks, even going so far as to hold up another ’52 Topps Mantle card to the camera to promote what his company can do, which is provide quick cash advances to owners of valuable sports cards.

The entrepreneur’s name is Edward Siegel, CEO of Card Fi. Siegel’s no stranger to the alternative finance space because he spent about a decade in the MCA industry, most recently as the founder of Bitty Advance, which he sold in 2020. Since then, Siegel returned to his roots and early passion of his youth.

“I had a background in sports cards as a collector, you know as a kid, but then in my early twenties, I was promoting card shows at malls,” Siegel said. “I was heavily into the hobby, setting up the card shows and promoting them and doing player appearances where players come in and do an autograph appearance.”

That was back in the late 80s, early 90s, according to Siegel.

When Covid hit and he exited his most recent company, he noticed a massive resurgence in the sports trading card market. His next business ultimately became Card Fi, a company that will evaluate the market value of a card and make an advance against it. There’s obviously risk involved so they take possession of the card for the duration.

“We have to get a hold of these cards and we’re responsible for them and then we vault them in our in-house bank vault,” Siegel said. The cards are stored in a highly secure climate controlled environment. Card Fi shows the vault off frequently in its Instagram videos.

Such a business requires large amounts of capital so Siegel went searching for investors, a pursuit that led him to a unique place, an Instagram Live pitch competition hosted by famed CEO and reality TV star Marcus Lemonis. Siegel entered himself in as a contestant, knowing full well that the odds of even being chosen to present his business to Lemonis were about a million-to-one.

Somehow, he was called up to pitch.

“So [businesses] went on there during the quarantine and you pitched your business,” Siegel explained. “I went on there and I pitched it […] And he understood it and he thought it made sense.”

The moment eventually led to a deal with Lemonis’ company and Card Fi was on its way.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

“If we look at it, there’s two different markets, you have the modern card market [where] I would say it’s basketball [that leads the pack],” he said. “For the vintage card market it’s baseball.”

Football is huge as well, he explained. A Patrick Mahomes rookie card, for example, an NFL Quarterback that’s still currently playing, recently fetched $861,000. There are only one of five like it in the world, the scarcity playing a major role in the value. Meanwhile, a Justin Herbert rookie card, an NFL Quarterback who’s only in his third year was already receiving bids above $1 million at the time this story was being written.

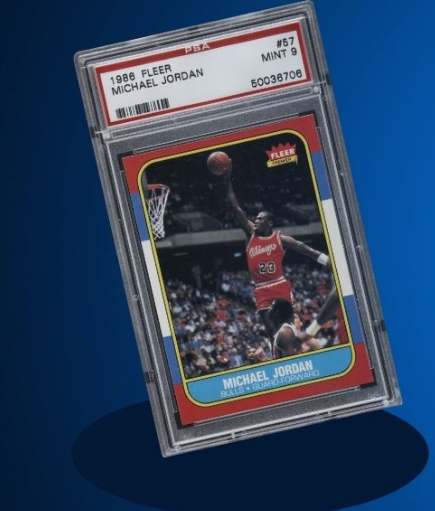

“It really depends on the card itself,” Siegel explained. “Some players might be known for having better careers but then you have cards that have more scarcity to them. Something that’s a one of one or maybe a very low populated card and a graded PSA 10 could very well be worth more than a [Michael] Jordan rookie because it has scarcity in it.”

PSA refers to cards that have been verified as authentic and graded on the condition of the card itself. Ten is the highest level a card can receive. Card Fi will only work with graded cards to avoid any funny business when it comes to advancing funds based upon the value.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

“This financing benefits the market as loans and cash advances have become an increasingly asked-for offering among trading card collectors,” said Chad Fister, PWCC’s CFO in a story that originally appeared on Sportico. “Enabling our clients to access liquidity through a menu of capital offerings is key as trading cards continue to prove themselves to be a valuable tangible asset class.”

For Card Fi, customers that take an advance can track everything through an online portal, including details about their cards, payments, and balance.

“We want to note that we built a full-service automated underwriting and collection platform to where, whether it’s the customer or the broker, they can log into our system and put the description of the card into the system and it’s going to automatically underwrite it and price it out,” Siegel said.

That description sounded like something straight out of the fintech industry of his past, especially the component about brokers.

“Just like the MCA space, we have a whole partnership side, a broker side, where brokers can refer us customers just as an affiliate where they just send the info over,” Siegel said. Similarly, they can earn a commission if a transaction is completed, he explained.

In this industry, brands like Topps, Upper Deck, and Panini have become the bread and butter for Card Fi. Even though it’s all business for Siegel these days, he couldn’t help but mention a particular card he had a personal attachment to.

“My personal favorite card in my collection is the 1965 Topps Joe Namath rookie card,” Siegel said. “Of course being a die hard New York Jets fan, that has to be my favorite card.”

The Power of the Suit

August 15, 2022 Getting out of bed in the morning can be rough after a long night’s rest but jumping into your work outfit is like putting on a superhero cape to go out and save small businesses that need capital. Working in the finance industry, wardrobe is the last thing mentioned in regards to the job itself, but it is what allows many to put their best foot forward.

Getting out of bed in the morning can be rough after a long night’s rest but jumping into your work outfit is like putting on a superhero cape to go out and save small businesses that need capital. Working in the finance industry, wardrobe is the last thing mentioned in regards to the job itself, but it is what allows many to put their best foot forward.

“I come from a suit and tie background, it’s like a uniform,” said Mike Brooks, owner of Best Connect Capital. “So, when you’re a broker and you’re dealing with business owners, you’re holding a lot of weight, a lot of power in your hands, especially when you get a good client on the hook. So, I just feel that dressing appropriately whether it’s a suit and tie or work casual is absolutely essential.”

There’s a saying, Brooks continued, “When you look good you feel good.”

“I’m a woman, I like to dress up, it’s fun but most importantly we’re working in a male dominated industry,” said Angelina Fletcher, Director of Business Development at Wing Lake Capital. “A lot of the brokers and lenders that I work with have been in the industry for 20 plus years, they’ve already built their brand, I’m still building my brand. Walking into these events looking fresh and professional makes me feel good and confident so I can focus on networking.”

And when striving to close those business deals, having a special piece of clothing that gives one an extra push can dictate the confidence he/she possess throughout the day. Whether it’s a favorite tie or a favorite pair of shoes, there can be an item that sets the tone.

“My biggest thing is my Rolex watch, when you’re in situations it definitely gives you a sense of confidence,” said Brooks. “It’s a life milestone to be able to purchase a Rolex even if people are way past that point in their mind.”

It’s not so much about accessories, however, to Dr. Rev. R.J. Rochelle, Business Financial Planner & Exit Strategist. Rochelle starts his day off by being active.

“I’ll take a pre-workout,” Rochelle said. “Now that pre-workout gets me pumped, it’s better than coffee. And then I’ll go work out.”

On wardrobe, Rochelle said he finds it important to put his best foot forward when he’s out meeting potential clients in person and that the mindset comes more from starting off the day with music or a sales podcast.

“When I commute or when I’m about to go out to the field in particular to get pumped up, I may play like Commas by Future because we’re talking about making money,” Rochelle said.

Fletcher of Wing Lake also has a routine that gets her started.

“I meditate, I drink my coffee and I have liquid IV,” she said.

Whatever the routine or the gear, there’s a little magic to it all.

“if you’re like a medic or a police officer or you’re in the army and you’re wearing like clothes that don’t match up with what you’re doing… I’m sure [they’d] feel different,” said Brooks of Best Connect Capital.

Funders Weigh in on the New Disclosure Law in Virginia

August 10, 2022 “I think there are pros and cons on this law,” said Boris Kalendarev, CEO at Specialty Capital, in regards to the recently enacted sales-based financing disclosure law in Virginia. “I’m on the pro side and I think first and foremost it allows the good funders and the good brokers in the space to operate in the right manner.”

“I think there are pros and cons on this law,” said Boris Kalendarev, CEO at Specialty Capital, in regards to the recently enacted sales-based financing disclosure law in Virginia. “I’m on the pro side and I think first and foremost it allows the good funders and the good brokers in the space to operate in the right manner.”

The law technically went into effect on July 1st, shaking things up for funding providers and brokers alike, particularly through a set of uniform disclosures that are required every time a contract is put in front of a Virginia-based business.

“It holds a broker more responsible for the transaction that they’re going to complete,” said Sharmylla Siew, Senior Underwriter at Lending Valley. “It builds a deeper bond between the broker and the merchant. And it also creates a better bond between the broker and the funder.”

Echoing Siew’s perspective, Kalendarev also believes that being clear creates an honest business space for the broker, merchant, and funder.

“I think transparency is really the right way to run this business. Let’s try to make sure there’s even more transparency,” said Kalendarev.

One intent behind the law is to provide the business customer with all of the pertinent information in a digestible format. Notably, this includes the commission that a broker may be receiving from the funder.

“I do believe that it should be fully transparent on both sides to understand the transaction in full,” said Dylan J. Howell, CEO of Liquidibee. “The merchant should understand that the broker is getting compensated. And if he decides that the broker deserves an additional commission on top of what he’s getting paid from the funder, well, that’s an informed decision between the merchant and broker to come to an agreement with.”

“I do believe that it should be fully transparent on both sides to understand the transaction in full,” said Dylan J. Howell, CEO of Liquidibee. “The merchant should understand that the broker is getting compensated. And if he decides that the broker deserves an additional commission on top of what he’s getting paid from the funder, well, that’s an informed decision between the merchant and broker to come to an agreement with.”

Howell Suggested that some of what is required would be expected in other types of deals.

“If you would go out and buy a $500,000 house, you get to the closing table and you look at the bill, it says it’s $545,000, but the purchase price is 500,000, you would want a reconciliation page to show where that 45,000 of additional capital is going,” Howell said. “And it’s no different than in this transaction, in my opinion.”

Banks and credit unions were exempt from the law but some view targeted regulations like this one as a way to raise the bar and credibility of sales-based financing products in general.

“Merchants who wouldn’t have considered an MCA as a practical form of funding in the past may decide to explore this avenue knowing that the industry is being held to a higher standard of practice,” Howell said.

Siew, of Lending Valley, echoed same.

“I am actually very excited about the new regulations, and I feel that it would make a huge impact on the MCA industry,” she said.

Work With a Broker or Go Direct?

August 2, 2022“I believe that a merchant might be better off going to a broker so the broker can make available to the merchant several different offers,” said Pooja Nene, Broker Relations Manager at Balboa Capital. “And if they’re doing what they need to do correctly and if they’re really consulting the merchant correctly, I think that they would be providing the best offers to the merchant based on their needs.”

It’s the age-old question, are merchants better served by using a broker or going direct? Opinions vary and are usually colored by what role one has in the process.

It’s the age-old question, are merchants better served by using a broker or going direct? Opinions vary and are usually colored by what role one has in the process.

“The advantages of working with a broker is it saves the merchants a lot of time, and in some cases saves them money in fees,” said Randy Guerrier, Senior Funding Executive at Banana Exchange, a company that provides capital to MCA providers. Guerrier’s vantage point makes him less biased. “A lot of brokers do have a lot of preexisting relationships and wholesale rates that they could get with their relationships,” he said.

Matthew Washington, Founder & CEO of Moneywell GRP, says there’s a bit more nuance to the whole thing.

“The reality is that when the merchants go direct with lenders, they’re essentially dealing with the lender’s broker shop, right?” he explained. “Any lender that gets directly contacted by a merchant usually gives them off to their sales team, which [is also able] to send [them] off to other lenders.”

Washington, whose company is a funder, was an advocate for what brokers can accomplish for their clients especially since he relies entirely on them for business. He emphasized that his company is one that doesn’t have a direct sales team to handle any direct inquiries.

“All my business comes from my ISO channel,” he explained. “So when I approve a deal, it’s up to me and the broker to win it if there’s competition, but if I declined the deal, my brokers take that deal to another lender that has an appetite for that particular scenario.”

“[Lenders] may not have the staff available to form that relationship with a merchant,” said Pooja Nene of Balboa about the debate on broker vs. direct. She also cautioned that sidestepping a broker in the process might not translate into an increased likelihood of approval.

“[Lenders] may not have the staff available to form that relationship with a merchant,” said Pooja Nene of Balboa about the debate on broker vs. direct. She also cautioned that sidestepping a broker in the process might not translate into an increased likelihood of approval.

“If it’s the first round of funding, if it’s their first loan schedule, we don’t know who this merchant is, and we may feel a little bit more comfortable with that file coming through the broker and the broker discussing the terms with the merchant,” she said.

Guerrier of Banana Exchange said, “It always comes down to working with the right type of broker, right? It comes down to the person that answers the phone that’s working with you, whether it’s at a big company or small company, I like to look at things from the individual working with the right people.”

And finding the “right people” isn’t automatic because they still have to be found, and once they’re found the lender has to decide if the customer is also right for them. Speaking about that in relation to all the economic uncertainty, Washington of Moneywell GRP said that a funding company should stick to what they’re comfortable with and not “chase deals” that they wouldn’t normally fund.

“But, also [on being found], I would market the heck out of my company and make sure that everyone in the world knows what I do, my product line, my branding, my logo, and make sure that anyone that is looking for capital that they know ‘hey, this company is always popping up,’ and I’d make sure that I stand out,” Washington said.

DailyFunder Marks 10 Year Anniversary

July 26, 2022 The DailyFunder.com domain was registered ten years and 1 month ago. Formed two years after the debut of AltFinanceDaily, DailyFunder went on to become the most active small business finance community in North America. The forum has generated more than 160,000 posts and has more than 12,000 members. It has regularly surpassed two million page views per year.

The DailyFunder.com domain was registered ten years and 1 month ago. Formed two years after the debut of AltFinanceDaily, DailyFunder went on to become the most active small business finance community in North America. The forum has generated more than 160,000 posts and has more than 12,000 members. It has regularly surpassed two million page views per year.

“There is no doubt that the DF has impacted the trajectory of the industry over the last decade,” said Sean Murray, who founded it. “The site receives thousands of visitors per day. In the early years it ushered in an era of broker commission transparency.”

Murray recalled a time when sales agents were not always aware that there were even commissions being paid at all.

“There were reps who thought that they had to charge merchants a separate fee in order to earn anything at all,” Murray said. “And their bosses were taking 50% of that. When I would bring up commissions, they’d be like ‘wait, the funders are paying my boss for these deals too?’ and I’d be like ‘how do you not know this?’ Widespread communication via the forum eliminated a lot of the secrets.”

One of the most popular categories on the forum in more recent times has been the Deal Bin, where brokers try to find placement for deals. It’s recorded more than 41,000 posts.

“Ten years is a lifetime as far as I’m concerned,” Murray said. “Love it or hate it, everybody knows the DF. If you’re a lender or funder, your brokers are lurking on there whether they admit it or not.”

North Mill Enhances Rate Card Program

July 18, 2022 JULY 18, 2022, NORWALK, CT – North Mill Equipment Finance LLC (“NMEF”), a leading independent commercial equipment lessor headquartered in Norwalk, Connecticut, announced that the company has implemented major enhancements to its pricing scheme, simplifying its buy rate structure and connecting each price point directly to the credit parameters company analysts use to assess each transaction.

JULY 18, 2022, NORWALK, CT – North Mill Equipment Finance LLC (“NMEF”), a leading independent commercial equipment lessor headquartered in Norwalk, Connecticut, announced that the company has implemented major enhancements to its pricing scheme, simplifying its buy rate structure and connecting each price point directly to the credit parameters company analysts use to assess each transaction.

The upgrades provide a decisive benefit to the hundreds of referral agents with whom NMEF partners. Brokers can now identify the credit variables NMEF reviews when analyzing a deal. As such, they can determine readily whether a borrower’s credit background matches the parameters associated with a particular buy rate outlined on the new price cards. Moreover, the revised pricing is configured in a “waterfall” format. If a borrower does not meet all the credit requirements outlined in one price panel, the transaction will generally flow to the next price panel, and so on.

“The feedback we receive from our broker partners often provides the blueprint for change,” said Paul Cheslock, Vice President, Customer Relations, North Mill. “As a lender that remains totally committed to the third-party channel, we take the recommendations we receive from referral agents very seriously. In this case, imparting a level of transparency and connectivity between our pricing and credit review methodology was cited as an opportunity. They spoke, we listened.”

The new pricing scheme comprises two sets of rate classifications based on equipment type. One class includes buy rates for most of the equipment that NMEF will consider financing while the other class is designed solely for heavy duty Class 8 sleeper trucks, logging equipment, and printers. Additionally, the cards have rates for borrowers with better credit backgrounds and more time in business vs. those with more challenged credit histories and/or less business experience. For questions on North Mill’s rate card program, please contact Don Cosenza at (203) 354-1710 or dcosenza@nmef.com.

About North Mill Equipment Finance

North Mill Equipment Finance originates and services small to mid-ticket equipment leases and loans, ranging from $15,000 to $1,000,000 in value. A broker-centric private lender, the company accepts A – C credit qualities and finances transactions for many asset categories including construction, transportation, vocational, medical, manufacturing, printing, franchise, renovation, janitorial and material handling equipment. North Mill is majority owned by an affiliate of WAFRA Capital Partners, Inc. (WCP). The company’s headquarters is in Norwalk, CT, with regional offices in Irvine, CA, Dover, NH, Voorhees NJ, and Murray, UT. For more information, visit www.nmef.com.

AltFinanceDaily Happy Hour is SOLD OUT

July 17, 2022The AltFinanceDaily happy hour scheduled for July 28th in NYC has hit its registration limit.

Missed out? Register for Broker Fair 2022 taking place on October 24 at the New York Marriott Marquis in Times Square. This is one event that small business finance brokers won’t want to miss!