LOOP Brings Real Tech to Auto Insurance

October 6, 2021 LOOP, a insurtech company that is launching a new concept of AI-driven auto insurance polices, was able to land $21M in Series A funding last week. The group of investors varied from venture capital groups to media companies to celebrities like hip-hop star Nas. The company claims to do auto insurance differently by changing the way they design premiums and qualify discounts.

LOOP, a insurtech company that is launching a new concept of AI-driven auto insurance polices, was able to land $21M in Series A funding last week. The group of investors varied from venture capital groups to media companies to celebrities like hip-hop star Nas. The company claims to do auto insurance differently by changing the way they design premiums and qualify discounts.

“We get rid of all the stuff that doesn’t matter in pricing [customers],” said John Henry, Co-CEO and Co-founder of LOOP, when explaining how the ways traditional insurance companies price their customer’s rates. This is where LOOP separates themselves from the pack. Things like credit scores, education, and income are not considered when pricing out their customer’s rates according to Henry, rather it’s how and where they are driving that determines the cost of insurance.

As an [Managing General Agent] MGA, LOOP underwrites its own risk and chooses the services they partner with to operate their claims. “This is not some digital brokerage or a quoting engine,” said Henry. “When you are insured by LOOP, it’s our actual product you’re insured by. We don’t sell any other products, we don’t sell leads, we are in the business of insuring people.”

LOOP will provide information to its customers that enables them to improve their driving and decrease their future rates. They will send customers tips on where and when to drive, and how to drive if they are driving erratically via a phone-based app. Their initial rate is based on population-level statistics from the respective area, and their personalized rate is a standard 6-month premium, meaning that the monthly rate won’t change month-to-month based upon how customers drive at certain times.

“We have millennials encumbered with student loan debt, we have immigrant populations with consumer loans, baby boomers selling their homes and losing their home and auto bundles, and the realities of the post-pandemic era means that we need more flexible and contemporary insurance solutions, and we are proud to be emerging as that,” Henry said.

![]() “We are the third step of insurtech,” he said, when asked how LOOP compares to others in the AI-based insurance sphere. “We’ve fundamentally built a novel insurance product from the ground up. Rather than sprinkle a digital layer on top of a legacy product, we completely rearchitected it.”

“We are the third step of insurtech,” he said, when asked how LOOP compares to others in the AI-based insurance sphere. “We’ve fundamentally built a novel insurance product from the ground up. Rather than sprinkle a digital layer on top of a legacy product, we completely rearchitected it.”

Henry boasted about how his company is the only one writing policies without traditional demographics in mind. “Today, I’m really proud to say that LOOP is the only insurance product that is a standard auto product that doesn’t have any of those demographic factors, it’s completely technology driven,” Henry said.

According to Henry, LOOP’s status as a public-benefit corporation, or B-Corp, will give his company the moral obligation it needs to fulfill its mission of being a fair, non-biased, and non-discriminatory auto insurance provider. The B-Corp status creates a “double bottom line” as Henry put it, creating a legal obligation for the company to hold the values in its mission statement for its customers, as well as the traditional corporate obligation to what’s best for its shareholders.

“From a business perspective, it’s kind of a risky thing,” Henry stressed when talking about the obligation to their customers as part of the public-benefit agreement. “The public can sue us if they ever feel like we are straying away from our mission.”

Customers are saving an average of 35% on their auto insurance premiums when quoted by LOOP, according to Henry. The company name directly correlates with the envisioned series of events that a LOOP customer will experience while holding a policy. A LOOP customer signs up, gets a good rate, utilizes the information given by LOOP, their driving is tracked and the data is analyzed, and the rate drops upon renewal after the policy expires. By repeating this, the customer “loops” around a cycle of better information leading to better rates.

“This is a mass market product. There is mass consumer demand. Our waitlist has grown to over 30,000 people across all fifty states, with different age groups and backgrounds,” Henry said. “I think people are excited to have an insurance company they can love again.”

Fintech Déjà Vu: Wait, Has This All Happened Before?

October 6, 2021 All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

All one needs to do is answer a few short questions about their personal and business finances, have their answers evaluated by multiple leading lenders, and they’ll get a loan decision instantly, the advertisement said. Then, “select the loan that’s best for your business and get back to work all in less than 5 minutes.”

Touted as the “5-minute online business loan,” the ad for LoanWise ran in newspapers starting in 1999. That was 22 years ago. Back then, LoanWise was described as a marketplace that connected small businesses with lenders where borrowers could comparison shop for loans.

Provident Bank was the first to join the platform, where it would approve between $5,000 – $50,000 in as little as five minutes. At the time, the Los Angeles Times said that there were only 2,160 matches on Google for the phrase “small business finance.”

“2,160 is a big number no matter how you look at it,” the Times reported.

There’s over 6 million today by comparison.

LoanWise had set up 10 lenders on the platform by the end of 1999, with names that included American Express, Compass Bank, and PNC Bank. There was competition as well. Business Finance Mart and America’s Business Funding Directory also connected interested borrowers with lenders, according to the Times.

Today, all 3 websites no longer exist, forgotten vestiges from the land before fintech.

Or has this all happened before?

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

John P. Clark, a cost economist with Ohio Bell Telephone Co., ran a mortgage number crunching business in Cleveland on the side in 1986. Naming his company “FinTech,” Clark would help people calculate the best time to refinance.

“Clark can generate useful timetables for mortgages that take the mystery out of when refinancing a mortgage makes sense,” wrote The Plain Dealer. Had it been 2021, Clark sounds like it would have been a billion dollar fintech app.

It was not a one-off.

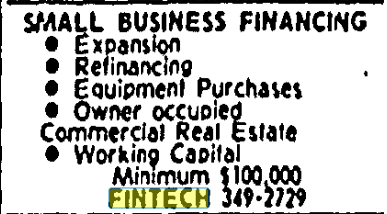

Fintech was the place to call if you wanted a working capital small business loan in San Antonio, TX starting in 1989. Ads for Small Business Financing advised people to call Fintech to get their business funded.

You could also just subscribe to the newletters. The Financial Times had four “FinTech Newsletters” in 1989 that were dedicated to covering electronic office, advanced manufacturing, telecom markets, and mobile communications. The price was £344 to £395 per year to receive them bi-weekly.

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

“FinTech newsletters tend not to be excessively technical,” The Guardian wrote on Aug 10, 1989, “but provide management guides to developments in each field, with lots of bullet points.” Perhaps the striking difference between that and today is that the newsletters arrived “hole-punched for filling in a binder.”

But hey, it’s all just a coincidence that ideas were roughly the same thirty years ago. Out in say, Des Moines, Iowa in the 1960s, for example, none of these things would’ve occurred to anyone.

Or would they have?

Sidney Feintech, a supermarket owner, expanded his store in 1963 to sell appliances, car batteries, clothing, and televisions. He got the idea that selling on credit would boost sales so he formed his own in-house credit company so that customers could Buy Now, Pay Later. Innocent enough, except the newspapers mispelled his last name.

“Fintech,” the papers said, had gotten into the credit business.

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

Fast forward 33 years to 1996 when a 26-year-old named Douglas Lebda thought the process of going from bank to bank to get a loan was too burdensome.

“I thought, ‘why can’t I put my information somewhere and let the banks compete for my business,” Lebda said. Launching a website, his company went on to generate $460 million worth of loans in just the fourth quarter of 1999 alone.

“There are other sites on the internet where you can apply for a loan, but those sites are operated by the lenders themselves,” Lebda said at the time. “We don’t lend money; that’s what makes us unique.”

That website was LendingTree, a company that today still has over 900 employees and a market cap of $1.8B. And Lebda is still the CEO.

In 1999, the hardest part was educating consumers to shop for loans online.

“Consumers have always done this one way, and this requires a behavioral change,” said consultant James Punishill in 1999. “In the old world, you’d pick up the newspaper and see a bunch of rates.”

“I knew from the start this would work because consumers really hate getting loans,” Lebda said at the time. “The market is huge and it’s perfect for e-commerce.”

Cannabis Boom Exposes Difficulties in Lending

September 15, 2021 The legalization of cannabis across the U.S. has exposed an interesting opportunity for banks and small business lenders. With tons of capital, insane amounts of cash flow, and an industry outlook that couldn’t be better, banks and lenders should be swarming in droves to get their hands on a piece of the legal marijuana action. Seemingly a match made in heaven, lenders and cannabis cultivators are running into some serious trouble when it comes to how the cash crop operators manage their businesses’ finances.

The legalization of cannabis across the U.S. has exposed an interesting opportunity for banks and small business lenders. With tons of capital, insane amounts of cash flow, and an industry outlook that couldn’t be better, banks and lenders should be swarming in droves to get their hands on a piece of the legal marijuana action. Seemingly a match made in heaven, lenders and cannabis cultivators are running into some serious trouble when it comes to how the cash crop operators manage their businesses’ finances.

“We had too much cash to keep in one place,” said Charles Ball, the owner of Ball Family Farms, a wholesale grow operation based in Los Angeles. By stashing cash in different safe-houses around LA, Ball had to operate his completely legitimate and legal business like an illegal operation. “Traditional banking wasn’t an option for us,” Ball said.

“We used to drive the cash around,” said Ball. For recent renovations of lighting fixtures, Ball had to pay $125,000 in cash to the company who did the service for him. Ball also paid taxes in cash, a process in which he had to walk into a Los Angeles government building with $40,000 cash on his person. At the time, there was no bank that was willing to hold the cash for him — even for tax purposes.

Prior to going fully cash, Ball did do business with some big banks, but he realized quickly that they weren’t interested in servicing his cash upon learning what his business was doing.

“They closed my account for wearing a shirt with my business name on it, they put two and two together,” said Ball, when referencing the closing of two accounts with Bank of America and Chase after representatives of the banks saw him wearing his company shirt to make deposits. One of the biggest difficulties of running a cannabis distributor isn’t the growing or the distribution of the product, it’s what to do with the money, according to Ball.

“They closed my account for wearing a shirt with my business name on it, they put two and two together,” said Ball, when referencing the closing of two accounts with Bank of America and Chase after representatives of the banks saw him wearing his company shirt to make deposits. One of the biggest difficulties of running a cannabis distributor isn’t the growing or the distribution of the product, it’s what to do with the money, according to Ball.

“We had no way of banking,” he said, up until February of this year, when he was able to secure his first type of deposit account with a local bank in the Los Angeles area that was fully aware of what his business was doing. “I have to pay more fees, and I don’t get the same type of customer service, everything is different,” Ball said.

With service fees on his deposit account between $2,000-$3,000 per month, the security of doing business with a bank must be worth the price. When pursuing a loan with that bank to expand his operation however, the lending process was halted at the last second after federal regulators told the bank they wouldn’t allow the deal to go through.

“We were denied on the approval date [of the loan],” said Ball. According to him, the bank told him the FDIC stepped in and killed the deal. Once again, Ball Family Farms was forced to explore other options outside of banking, such as exploring renovation options through landlords or simply waiting until the cash is on hand to make the move. “The banking system in this industry is very flawed,” said Ball.

“We’ve never taken private investor money,” Ball said when asked about whether he had explored any other avenues of receiving a loan. “We took [the start] slowly and it works, we are a ground up operation.”

This problem is not unique to Ball Family Farms. Legal cannabis cash flow has been a major issue since legalization first took place in the states. It seems like local governments want the tax revenue, but the bank’s regulators want to make it difficult for lenders to get their hit off the cash pipe until the federal government changes the law on their end.

The opportunity for funding in the industry isn’t going unnoticed however, as cannabis-exclusive funders and brokers are beginning to pop up across the U.S.

Judy Rinkus, for example, CEO of Seed to Sale Funding, is a Michigan based broker who works exclusively with cannabis businesses.

“[The industry’s] biggest problem is simply finding a lender who isn’t prohibited from lending to cannabis-related concerns,” said Rinkus. According to her, one of the biggest issues is the infancy of the industry, as many cannabis wholesalers and retailers just haven’t been around long enough to be reliable borrowers.

“[The industry’s] biggest problem is simply finding a lender who isn’t prohibited from lending to cannabis-related concerns,” said Rinkus. According to her, one of the biggest issues is the infancy of the industry, as many cannabis wholesalers and retailers just haven’t been around long enough to be reliable borrowers.

“Most businesses have been established for 3 years or less, they haven’t kept good financial records, and accept a lot of cash payments, and they lack sufficient collateral,” Rinkus said.

Rinkus stressed the importance that real estate plays in giving cannabis businesses borrowing power. “Having real estate to pledge as collateral is key,” she said. “There are ways to get other types of loans, but they are often enormously expensive and are limited to no more than 10% of an entity’s historic revenues.”

Rinkus’ outlook on the industry remains positive, and she remains a supporter despite the difficulties associated with cannabis lending. “Businesses in this space are the true American entrepreneurs,” said Rinkus. “In many areas of the country, they are creating jobs and wealth for folks that would otherwise not have the same chances.”

The outlook on the industry is bright. More states are pushing for legalization, social taboo of marijuana is relatively nil, and the potential of an untapped industry in the eyes of both government and banking are becoming too good to pass up. As the industry begins to cultivate its presence, look for the money surrounding cannabis to creep its way into fintech sooner than later.

Aquila Services Inc. Has Ceased Operations

September 9, 2021Aquila Services Inc, a data-driven small business cash flow management platform, ceased operations sometime early last year, AltFinanceDaily has learned. The company had been trying to pivot even before the pandemic began. CEO and Founder Taariq Lewis, who had spoken about AI and machine learning at some length to us in 2018, updated the company’s website with the bad news.

Aquila is now closed for business and we have shut down our servers after a three year run. Thanks to all our 9,688 customers and our many investors for allowing us to provide cash flow analysis for small businesses.

If you are seeking business funding, please be sure to check our partners at Rapid Finance, Credibly, Kabbage, and others for access to capital and please check with Home Depot for discounts on construction equipment.

Lewis is now listed as a co-founder of UniFi DAO, according to LinkedIn.

Knight Capital Technology to Play Continuing SBA Loan Role at Ready Capital Corporation

September 7, 2021 Ever since Ready Capital’s name arrived on the big stage for its leading role in the nation’s PPP lending, the company has continued to be very active in small business lending. They completed round 2 of the PPP program with $2.2B in loans to more than 72,000 small businesses. For comparison’s sake, that’s twice what PayPal contributed, who provided $1B to 43,000 businesses.

Ever since Ready Capital’s name arrived on the big stage for its leading role in the nation’s PPP lending, the company has continued to be very active in small business lending. They completed round 2 of the PPP program with $2.2B in loans to more than 72,000 small businesses. For comparison’s sake, that’s twice what PayPal contributed, who provided $1B to 43,000 businesses.

Ready Capital is the #1 non-bank in the nation in 7(a) SBA loan originations this year so far, according to John Moser, President of the company’s SBA lending division, and is #7 in the entire SBA lending industry nationwide.

Some of the technology behind their success can be attributed to Knight Capital, the company Ready acquired back in 2019. Knight has enabled the company to roll out offerings of SBA loans under $350,000, which it is using to grow its already impressive marketshare.

Speaking about Knight, Ready Capital CEO Thomas Capasse said in the Q2 earnings call, the “[Knight] investment will be levered into more technology affinity-based expansion of the SBA business.”

Overall, the company is optimistic. “Ready Capital is off to a strong start in 2021,” Capasse said during the call. “We have accomplished much in the first quarter of the year with our small balance commercial or SBC, CRE lending operations and Small Business Administration or SBA 7(a) lending businesses, posting record originations, including high volume in round two of the Paycheck Protection Program or PPP.”

Knight’s merchant cash advance business is combined with its small business lending division for quarterly reporting purposes so its individual stats are not easily ascertainable. The company still touts “same day business funding” on its website.

Cross River Bank Makes Moves as Fintech Acquirer, VC

July 13, 2021 Known in the space as the fintech partner bank, Cross River took another step down the path leading the industry: Last month, the bank bought PeerIQ, a company that does data analytics for loan underwriting. The bank also launched a venture capital arm to continue investing in startup fintechs in a more formalized way- though they have been partners for years.

Known in the space as the fintech partner bank, Cross River took another step down the path leading the industry: Last month, the bank bought PeerIQ, a company that does data analytics for loan underwriting. The bank also launched a venture capital arm to continue investing in startup fintechs in a more formalized way- though they have been partners for years.

“PeerIQ is a company we’ve known for a number of years; we’ve been working with them, partnering with them and in various ways for two or three years,” Phil Goldfeder, Senior Vice President of Public Affairs at Cross River, said. “We recognized that we would probably better serve our customers and partners if we came together, so we’re happy that we’re able to acquire Ram [Ahluwalia, CEO of PeerIQ] and his team at PeerIQ and we’re excited about the collaboration moving forward.”

PeerIQ will function as a part of Cross River, bringing intelligent analytics to every transaction. Cross River, located 14 floors up just across the George Washington Bridge in New Jersey, has about $13.5 billion of assets and has originated more than $46 billion in loans since 2008, Bloomberg estimates. The way forward, as Goldfeder said, was through innovation, leveraging tech and teams like PeerIQ’s to better serve clients. That also means using the formal VC branch to help new firms grow their platforms and future acquisitions.

“Number one is to grow on PeerIQ’s core business, providing data analytics, and creating technology in the secondary market, but more importantly, for Cross River to help our partners and our clients serve,” Goldfeder said. “There’s, no question that we will continue to explore companies that would help strengthen Cross River and the fintech ecosystem and provide additional services to our partners.”

The bank has over 15 partnerships with top fintechs, like publicly traded Affirm, Rocket Loans, Coinbase, and private firms funded through VC rounds like Stripe. The bank most recently became a significant part of the PPP government emergency loan program. Ranking among giants like JP Morgan and Bank of America, Cross River ranked 6th overall for dollar amount approved. According to the bank, they doled out 490,000 PPP loans for a total of $13 billion, making up 4% of the entire program volume.

The bank has over 15 partnerships with top fintechs, like publicly traded Affirm, Rocket Loans, Coinbase, and private firms funded through VC rounds like Stripe. The bank most recently became a significant part of the PPP government emergency loan program. Ranking among giants like JP Morgan and Bank of America, Cross River ranked 6th overall for dollar amount approved. According to the bank, they doled out 490,000 PPP loans for a total of $13 billion, making up 4% of the entire program volume.

The way forward is clearly through embracing what it always has been at its base: the bank across the Hudson that is willing to partner with upstart brands and help them take over the world. With a flurry of consolidation purchases in the “post-pandemic” world (if that isn’t too early to say) that are only going to increase, Cross River seems to be on to something. Goldfeder said that Covid showed the rest of the world what the fintech space has known for ten years, that added value for customers and partners means innovation.

“Post-pandemic, where I think there was a larger recognition from the financial services industry of the need to innovate,” Goldfeder said. “Cross River is always known that we need to innovate… The post-pandemic dynamic we recognize that there’s tremendous value in creating a more formal venture arm to examine, explore companies that we can invest in to help them grow, help them succeed, and …. increase our support of our partners.”

Bloomberg reported Cross River is in secret talks to raise $200 million of funding at a valuation of $2.5 billion or more. The bank previously raised $100 million in 2018 in a round led by KKR, AltFinanceDaily reported, and in 2016 raised $28 million.

PPP Deadline Extended, Jobs Act Proposed

April 1, 2021 President Biden signed a law extending PPP lending until May 31st. The PPP Extension Act passed through Congress on March 25th and will allow businesses to access emergency loans past the original March 31st deadline.

President Biden signed a law extending PPP lending until May 31st. The PPP Extension Act passed through Congress on March 25th and will allow businesses to access emergency loans past the original March 31st deadline.

According to the PPP loans tracker, as of 3/21 the SBA has disbursed $718 billion of the $806 billion available, leaving $88 Billion left for funding. Businesses will be able to apply until the new deadline, and the SBA will be able to process applications until the end of June. The new filing deadline gives the SBA some breathing room to review the 234,000 applications currently in the queue.

Biden signed it a day after unavailing a $2 trillion American jobs and infrastructure plan, aimed at revitalizing roads, bridges, and protecting the environment. The money is split into a cross-section of infrastructure, subsidies, like $100 billion toward bringing broadband internet to 30 million Americans, $50 billion toward semiconductor research, and $174 billion toward electric car manufacturing.

Not every spending point is for future tech. There are lump sums for healthcare, like $400 billion for long-term elderly care, and $30 billion for pandemic preparedness.

Biden has said he plans to pay for the expenses through the Made In America corporate tax plan raising the corporate tax rate from 21% to 28% after President Trump leveled the tax from 35%.

Merchant Cash Advance is as Old as The Renaissance

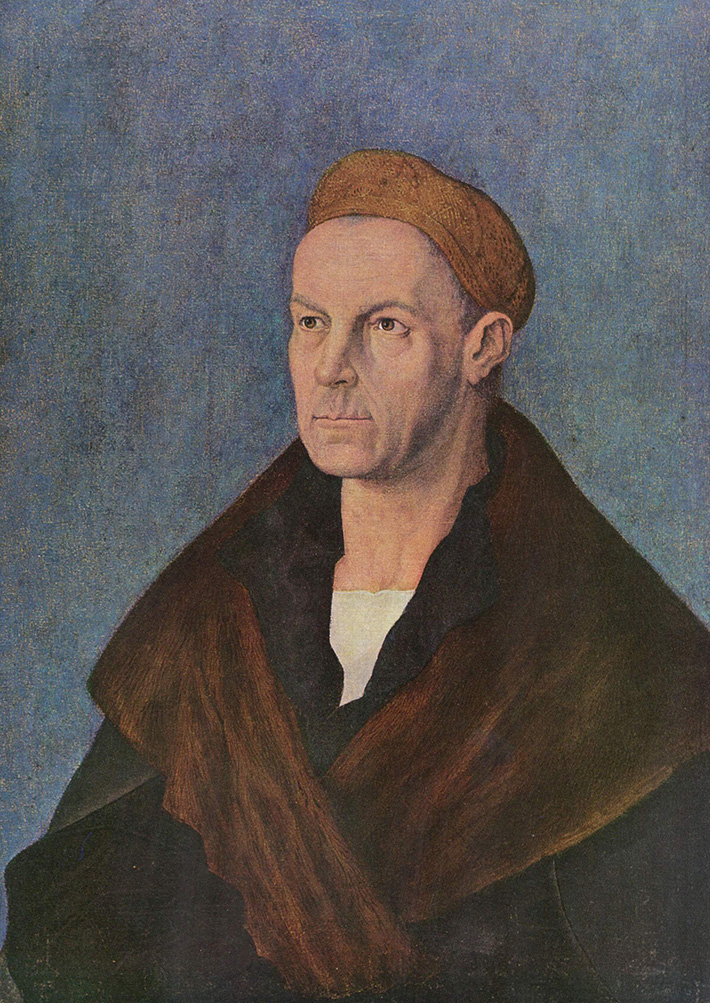

March 21, 2021 The first merchant cash advance enthusiast ended up the richest man in the history of the world. Jakob Fugger was the cash king of Europe 500 years ago, and his climb to wealth indirectly caused the Protestant Reformation. One of the pivotal events in western history, the Reformation led to the eventual “fad” of democratic representational government— all because some guy bought the future receivables of a silver mine.

The first merchant cash advance enthusiast ended up the richest man in the history of the world. Jakob Fugger was the cash king of Europe 500 years ago, and his climb to wealth indirectly caused the Protestant Reformation. One of the pivotal events in western history, the Reformation led to the eventual “fad” of democratic representational government— all because some guy bought the future receivables of a silver mine.

In Jakob Fugger the Rich, historian Jakob Strieder writes the Fugger enterprise began as one of the upstart merchant families of the Renaissance. The Fuggers were traders and cloth merchants from Augsburg, Germany. They created a network of aristocratic clients, furnishing weddings and parties through trading warehouses in modern-day Venice, Florence, and Austria. Jakob Fugger I lent some money around, but when Jakob Fugger II joined the family shipping warehouse in Venice, he looked for a better return on capital.

According to International Business History: A Contextual and Case Approach, Fugger entered an agreement to supply some cash- 23,627 Florins to a silver mine owned by Archduke Siegmund in 1487.

Siegmund had plenty of silver laying around for collateral; he just needed cash for the day-to-day. It was a collateral-backed loan, common today: if he couldn’t pay it back, the Fuggers would get paid in silver. The transaction worked so well that a year later, Siegmund reapplied, this time in a revolutionary way. Siegmund would get 150,000 florins, and the Fuggers would get paid the future receivables of the silver mine: unrefined and cheap future silver for cash now.

The problem, written by historian Greg Steinmetz in The Richest Man Who Ever Lived, was the Church. Any interest-based transaction was specifically outlawed, though there were hundreds of lenders during this era. The line from Luke 6:35, “Lend and expect nothing in return,” was taken by the Church to mean an outright ban on usury, defined as the demand for any interest at all.

Even savings accounts were considered sinful, but Venetians ignored these rules as they preferred making money to pleasing God, entombed in the motto “First Venetians, then Christians.” Fugger began accepting deposits like a bank to his clients, with a 5% return to investors.

But convicted usurers could be excommunicated and denied a Christian burial, a nightmare for a capitalist who relied on a Christian network. Fugger did not worry about punishment or the apparent sin of money lending, but as he became a fixture in European society, his reputation became increasingly vulnerable.

Fugger needed the laws to be changed, or at least relaxed, or his lending business was in trouble. In 1515, he wrote a letter to Pope Leo X and funded a debate in the St. Petronius Basilica in Bologna. The debate ran for five hours, a back and forth of philosophy, scripture, and rampant crowd heckling. In the end, it was declared a tie, but Pope Leo X that year signed a papal “bull” reforming the concept of usury.

Originally, the Church pointed to the philosopher Aristotle’s model for determining what was okay to charge for and what wasn’t. Aristotle had said that charging someone for a cow because it produced milk was fine, but money was a dead thing and unfair to profit from.

A silver mine produced silver and as such paying cash for the future proceeds of the mine had allowed Fugger to more or less carry on his business. It wasn’t called merchant cash advance back then but he applied that model wherever he could. Not everyone in need of money had a business, however, and it was critical that he be allowed to charge interest when circumstances called for it.

More than a millennium after Aristotle, Pope Leo X found that risk and labor involved with safeguarding capital made money lending a living thing. As long as a loan involved labor, cost, or risk, it was in the clear. This opened a flood of church-legal lending: Fugger’s lobbying paid off with a fortune.

Jakob Fugger was off to the races and he greatly expanded his financial services business. Historian Dennis McCarthy found that the Fugger family grew their war chest nine times over in the next seventeen years, a gain of 927%. Their funding efforts bought a trading empire, and they entered into agreements with nobles that placed entire countries as collateral.

Jakob Fugger was off to the races and he greatly expanded his financial services business. Historian Dennis McCarthy found that the Fugger family grew their war chest nine times over in the next seventeen years, a gain of 927%. Their funding efforts bought a trading empire, and they entered into agreements with nobles that placed entire countries as collateral.

McCarthy wrote: That was one of the problems with the Fugger model- “how does one take possession of Austria or France or Spain when its rulers default or lag behind debt repayment schedules?”

After gaining the good faith to lend in the Church’s eyes, the papacy itself became a Fugger customer. Positions in the Church were inseparable from social and political power, and the only way to get a place on the totem pole was by paying for a title. Just as the richest silver mine owners didn’t have the cash to pay for lunch- so did wealthy aristocrats need capital to afford positions in the cloth.

By the time Martin Luther “nailed” his 95 theses to the door of a church in 1517, he was rallying against the Fugger funding family and its stranglehold on the Roman Catholic Church.

It all came down to an in-house promotion. Albert Brandenburg brought a whole new meaning to the concept of “moneychangers in the temple.” A German Archbishop of Magdeburg, Brandenburg was promoted to Elector of Mainz: the second in command of the Holy Roman Empire. Unfortunately, he had to pony up 21,000 ducats to pay the Roman Curia (the Church’s admin)- for the title. Naturally, he didn’t have the cash, and the Fuggers stepped in.

Brandenburg got a loan on interest. To pay it back, he also paid Pope Leo X for the right to sell indulgences. Indulgences were contracts the church sold to forgive sins, allowing believers to purchase their way out of purgatory and into heaven. A fresh round of indulgences was printed to fund the construction of St. Peter’s Basilica, and Brandenburg was entrusted to sell them in 1517. (Their sale was later banned by the Church in 1567).

The sale of indulgences  interlinked the Church with Fugger, and solidified Luther’s desire to maintain the Faith through an alternate system. Luther’s complaints spawned the Reformation, and his followers and independent revolutionaries like John Calvin would bring the rise of Protestantism, the Church of England, and ultimately what historian Alec Ryrie wrote as the foundation of modern mercantilism.

interlinked the Church with Fugger, and solidified Luther’s desire to maintain the Faith through an alternate system. Luther’s complaints spawned the Reformation, and his followers and independent revolutionaries like John Calvin would bring the rise of Protestantism, the Church of England, and ultimately what historian Alec Ryrie wrote as the foundation of modern mercantilism.

“I’m saying that there are some specific parts of modern life that derive directly from the Protestant Reformation. We couldn’t have these features if it hadn’t happened.” Ryrie said. “That combination of free inquiry, democracy, and limited government is pretty much what makes up liberal, market democracies. It runs the modern world.”

To this day, no one is sure of the extent of the Fugger fortune. Historian Mark Häberlein found that Fugger struck a deal with Augsburg Tax authorities in 1516: he agreed to pay an annual lump sum on the condition that his family’s true wealth would never be revealed. He died in 1525.

To get an idea of the extent of his wealth, we can base calculations on the cost of butchering a pig in 1522 (yes, that’s a real metric.) It cost one Gulden, a new coin minted in 1500 to butcher a hog. The German coin contained about the same amount of gold as a Florin.

Based on those ham prices, Jim Ulvog from Ancient Finances estimated that in 2017 a single florin would be worth ~$900, and other writers have put the florin in the same range. Though the true wealth of the Fuggers may never be known, when Charles V aimed to take control of the Holy Roman Empire in 1519, the Fuggers were lending Charles 543,000 guldens to buy votes: approximately $448 million. That’s just in a single deal.

It’s been said that merchant cash advances or sales-based financing is relatively new, but it could be argued that such transactions are so old that life as we know it in the modern world only exists because a guy 500 years ago was engaged in non-loan transactions to fund businesses in a manner that was Church-compliant and wanted to expand.