Google Penguin 2.1 Takes Swing at Merchant Cash Advance Industry

October 5, 2013 If you noticed a shuffle in search rankings for industry keywords last night, it’s because Google unleashed Penguin 2.1.

If you noticed a shuffle in search rankings for industry keywords last night, it’s because Google unleashed Penguin 2.1.

Penguin 2.1 launching today. Affects ~1% of searches to a noticeable degree. More info on Penguin: http://t.co/4YSh4sfZQj

— Matt Cutts (@mattcutts) October 4, 2013

Penguin focuses on spammy or purchased backlinks so if you did one or the other, you probably got harmed. Given the high cost of traditional marketing and Pay-Per-Click Internet Marketing, many funders, ISOs, and lead generators have turned to SEO to boost their visibility in organic search. Whether undertaken by inside employees or outside contractors to do the job, there is no doubt that building links has been part of the strategy. Some have had major success in rising up through Google’s search results but most haven’t. It’s not easy getting to page 1, but if you get there, don’t celebrate. You won’t be there forever.

Less than two weeks ago on DailyFunder, someone took to the board to pat themselves on the back for ranking #2 for the keyword: merchant cash advance. Wikipedia is #1. They admitted it took a lot of hard work over the course of 8 months. Last night they were thrust back to position #65. That’s on page 7 where they will never be found. 8 months of work for 2 weeks of ranking. You might be saying, “Well my SEO guy will just roll with the punches and get us right back.” Unfortunately with Penguin, it doesn’t work that way. Penguin is basically a permanent penalty, an algorithmic barricade to prevent you from ever ranking for your keywords again. According to a poll on Search Engine Roundtable, only 7% of respondents claimed to have made a full recovery after Penguin 2.0. Most SEOs would advise that you torch your domain, buy a new one and start a whole new website. That’s not exactly an easy thing for a big brand or company to do.

There’s a flaw in all the SEO being done in the merchant cash advance industry anyway and that’s the notion of being on page 1 to begin with. If you read David Amerland’s Google Semantic Search, he explains that “there is no longer a first page of Google”. The results you see on the first page of Google depend completely on whether or not you’re using a desktop or mobile device, what zip code you’re accessing the internet from, what you’ve searched for in the past, and whether you’re logged into your gmail account. And if you use Google+, then forget it! The first page results for someone that uses Google+ are ultra personalized. To rank on their first page, they’ll pretty much need to follow you socially first.

So if you’re thinking about ranking higher in search as a means to generate more leads, you sure as heck better understand how the results work these days. What you see on your screen is not what I see on mine. A site that’s #65 for me, may be #4 for you.

The other angle of Google’s foray into Semantic Search is their desire to be an answer engine, not a search engine. Google wants to answer questions for searchers without them having to click a link. Here’s an example of Merchant Processing Resource acting in that role:

What is voice authorization you ask? Boom! Answered! No need to click anything. That’s where search is going. What this means for companies that are trying to get customers is that they either need to become the absolute authority within their industry or they need to throw in the towel and do Pay-Per-Click.

When I search for merchant cash advance from my desktop in NYC, 7 out of the top 10 results are not company pages, which is astounding considering how much effort companies are putting in to rank high for this keyword. I see:

- 1 Wikipedia

- 4 News articles

- 1 Press release

- 1 Youtube video

Did you get hit by Penguin 2.1? Are you optimized for Semantic Search?

Previous merchant cash advance SEO articles:

- Your Merchant Cash Advance Press Release May be Hurting You 8/8/13

- Is Google Your Only Web Strategy? 12/31/12

- The Other 93% 7/13/12

- Google Penguin Kills Survivors 5/6/12

- The SEO War Continues 4/4/12

- The SEO War for Merchant Cash Advance 2/12/12

Your Merchant Cash Advance Press Release May be Hurting You

August 8, 2013Part of keeping up with the merchant cash advance industry means reading up on the press releases published online, but it’s not such an easy job. Legions of funders, ISOs, and lead generators are competing for valuable real-estate in search results and they’ll use every trick in the book to get it. It almost always comes with a price and these tricks don’t always work. By tricks here, I’m referring to using optimized anchor text in press releases as a way to build backlinks.

Have you ever seen a press release with thin information but lots of embedded links that say something like “best small business loan companies”? There’s a reason for that. These companies are trying to manipulate PageRank, a Google search ranking factor that calculates the value of the page the link is on, calculates the value of the website it’s on, uses the anchor text as a signal of what the page is about, and then passes that value onto the destination page. PRWeb has a solid PageRank of 7 out of 10 and last I checked, they don’t nofollow the links. That means a webpage can gain some serious ranking points by using optimized anchor text in a press release. But that’s just on PRWeb’s domain. Consider the fact that press releases are usually syndicated to tens, hundreds, or even thousands of other websites, most of which will keep the links intact, and multiplying the value being passed to the destination site.

Have you ever seen a press release with thin information but lots of embedded links that say something like “best small business loan companies”? There’s a reason for that. These companies are trying to manipulate PageRank, a Google search ranking factor that calculates the value of the page the link is on, calculates the value of the website it’s on, uses the anchor text as a signal of what the page is about, and then passes that value onto the destination page. PRWeb has a solid PageRank of 7 out of 10 and last I checked, they don’t nofollow the links. That means a webpage can gain some serious ranking points by using optimized anchor text in a press release. But that’s just on PRWeb’s domain. Consider the fact that press releases are usually syndicated to tens, hundreds, or even thousands of other websites, most of which will keep the links intact, and multiplying the value being passed to the destination site.

One press release could result in hundreds of powerful ranking signals for the keyword, “best small business loan companies.” Now if there were on-page signals for that keyword and additional external factors at work, then there’d be no reason for that page not to rank high in search results for best small business loan companies. And so anyone not totally asleep at the wheel has been using that method for months, if not for years.

There’s only one problem. Google’s Director of web spam (yes, this is a real title) had said back in December of 2012 that links in press releases shouldn’t count.

The Internet went wild over this statement especially since his choice of words implied that there is a chance they did count, he just wouldn’t expect them too. Search Engine Optimization (SEO) diehards decided this was a battle worth fighting and optimized anchor text in press releases became more used than ever before, that is until Google decided to take action.

Wouldn’t expect was apparently proven to mean definitely does. The fact is that links in press releases were passing PageRank and the sites on the other end of them were getting valuable ranking signals. That’s why to this day we see merchant cash advance releases read like an itemized list of keywords on PRWeb…

The best merchant cash advance company has announced a new program to help provide bad credit business financing to restaurants in need of a fast cash loan.

If you’ve stopped reading the article at this point, you’re in trouble. The gravy train is no longer running express. Less than two weeks ago, Google conceded that optimized anchor text in press releases works and are a form of cheating the system. That means that overuse or quite possibly any usage of a keyword rich anchor in a release means your website is at risk of a rankings penalty. Google advises that in order to be safe, webmasters should nofollow the links. There’s just one problem with that; Credible wire and release services do not under any circumstances allow companies to code in HTML attributes in their releases, rendering this feat impossible.

That means the burden of nofollowing the links is on the release services and syndicating websites, something that isn’t likely to happen anytime soon. Release services have not been shy about the potential SEO benefits they can provide, with some going so far as to offer paid consulting services to clients on how to optimize their anchor text for search engines. To them, a crackdown on links in releases means a crackdown on a very profitable portion of their business model.

Watch Matt Cutt’s explanation of links in advertorials:

Google offers the following guidance on link schemes:

The following are examples of link schemes which can negatively impact a site’s ranking in search results:

- Buying or selling links that pass PageRank. This includes exchanging money for links, or posts that contain links; exchanging goods or services for links; or sending someone a “free” product in exchange for them writing about it and including a link

- Excessive link exchanges (“Link to me and I’ll link to you”) or partner pages exclusively for the sake of cross-linking

- Large-scale article marketing or guest posting campaigns with keyword-rich anchor text links

- Using automated programs or services to create links to your site

Additionally, creating links that weren’t editorially placed or vouched for by the site’s owner on a page, otherwise known as unnatural links, can be considered a violation of our guidelines. Here are a few common examples of unnatural links that violate our guidelines:

- Text advertisements that pass PageRank

- Advertorials or native advertising where payment is received for articles that include links that pass PageRank

- Links with optimized anchor text in articles or press releases distributed on other sites. For example:

There are many wedding rings on the market. If you want to have a wedding, you will have to pick the best ring. You will also need to buy flowers and a wedding dress.- Low-quality directory or bookmark site links

- Links embedded in widgets that are distributed across various sites, for example:

Visitors to this page: 1,472

car insurance- Widely distributed links in the footers of various sites

- Forum comments with optimized links in the post or signature, for example:

Thanks, that’s great info!

– Paul

paul’s pizza san diego pizza best pizza san diegoNote that PPC (pay-per-click) advertising links that don’t pass PageRank to the buyer of the ad do not violate our guidelines. You can prevent PageRank from passing in several ways, such as:

- Adding a rel=”nofollow” attribute to the < a > tag

- Redirecting the links to an intermediate page that is blocked from search engines with a robots.txt file

You can watch John Mueller, one of Google’s lead Webmaster Trends Analyst answer questions to Google’s new link policies in the hangout below:

There are other purposes for publishing thin releases as both Google and Bing can decide to display a snippet of the release on the first page of the results for the keywords used in the announcement. So no, it’s not just about links, at least that isnt’t all of the SEO benefit to be gained.

These news snippets can last up to a week, helping companies that might not be ranking well jump to the front of the line for exposure.

Link Removal

We’re not going to call anyone out by name but ever since Google Penguin 1.0 was released, many merchant cash advance companies and payment companies have hired link removal experts to identify bad links for them and are paying them to have them taken down. The only way to take down a link is to ask the webmaster hosting the site to take it down. Unfortunately, this has led to some companies finding the cheapest link removal service they can find, resulting in a poorly qualified consultant setting off to remove 100% of a site’s links instead of just the bad ones. We know this firsthand because we have had no shortage of e-mails from people claiming to be the hired link removal representative of a merchant cash advance related company.

The e-mails usually look like this:

Hello sir,

I am contacting you on behalf of Cash Advance Funder ABC and recently we have been instructed by Google to remove all of our links to have a penalty removed. Therefore we are asking that you remove our spam link from your website. We appreciate your immediate assistance in this matter.Sincerely

sfahfdspfu547@spamlinkremovalservicecompanyseobest.com

A great way to make sure your website never ranks ever again is to remove all your good links too. We can assure you that links on this website are not bad.

So…

In conclusion, if your hired SEO consultant is still banging away on optimized anchor text in press releases, there’s a good chance now that they’ll be causing damage over the long term. Press releases are for the purpose of making important company announcements and Google is on to anyone using them for any other reasons.

Your press releases might be hurting you with Google. Bing on the other hand…

Other SEO related articles on Merchant Processing Resource:

- Is Google Your Only Web Strategy?

- Google Penguin Kills Survivors

- The SEO War for Merchant Cash Advance Continues

- The SEO War for Merchant Cash Advance

../../

The Other 93%

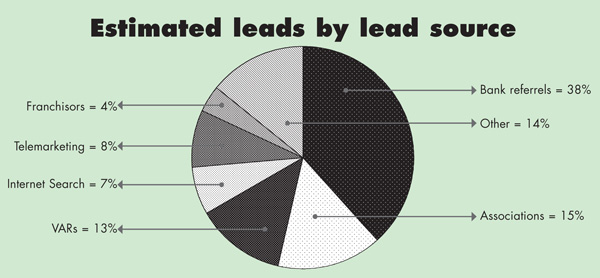

July 13, 2012The SEO war rages on for Merchant Cash Advance providers, ISOs, micro lenders, and other financing firms, but just how much real estate is everyone really fighting over? According to data recently provided in The Green Sheet by First Annapolis Consulting, only 7% of all merchant account leads are generated via the Internet. So if your business plan’s success hinges on getting to page 1 of Google search, you might be shutting yourself out from nearly the entire marketplace. Don’t get us wrong, there’s a lot of money to be made and business to be acquired via the Internet, but even the big firms get roughed up from time to time by competition, new algorithms, and SEO companies that promise the world but deliver few results.

So if not the Internet, then what else is there besides cold calling? That’s a question that tons of small ISOs ask themselves when they realize that competing online isn’t easy. It just so happens that the “what else” comprises of 85% of all generated leads in the payments industry. More than 50% are derived from bank referrals and associations alone.

Has anyone ever wondered why companies like AdvanceMe (Capital Access Network) are still number one in the Merchant Cash Advance arena? They’ve managed to defy Darwin’s theory of evolution. In every industry, there is a pioneer that leads the way, gets too comfortable, stops innovating, and is systematically made irrelevant by fresh thinking competition. There was MySpace until there was Facebook. There was Yahoo until there was Google. There was AOL until…there was just everything else.

So one would expect that in 2012, the mere mention of AdvanceMe would be part of a requiem for the founding fathers of the Merchant Cash Advance industry. That isn’t the case and is quite the opposite considering they are on pace to fund at least $700 million this year. So they must be #1 on Google, right? Nope. For all of the main keywords that people are fighting over, they rarely if ever, even show up on the first page of the results.

Chances are a lot of their clients never even bothered to search online for financing, or if they did, it was just to get a second opinion. Once they saw that full page advertisement in the merchant account statement their processor mails them every month, they probably just called the phone number listed on there, went through the steps, and got funded. AdvanceMe and other players have some pretty badass referral connections.

Chances are a lot of their clients never even bothered to search online for financing, or if they did, it was just to get a second opinion. Once they saw that full page advertisement in the merchant account statement their processor mails them every month, they probably just called the phone number listed on there, went through the steps, and got funded. AdvanceMe and other players have some pretty badass referral connections.

All the sales pitches in the world about lower rates and free POS systems aren’t going to compete with a merchant who has just been given a referral by a company they already have a relationship with. Hell, even you have probably enlisted an insurance company, wedding vendor, or mortgage broker because someone you trusted said they were great.

This isn’t another lecture about how referrals are crazy good and that cold calling is wicked bad, especially since we don’t even necessarily feel that way. The point is really to highlight just how much more potential there is out there for small funders and ISOs. You can actually be successful with a sucky website and no SEO if you can just solidify some key relationships.

If you want to be around 14 years later, you can’t ignore the other 93% of the market. The volume of Internet leads will probably increase in the future as more computer savvy people become small business owners. But it’s way too easy to set up a website, hire an SEO guy, and throw money at Pay-Per-Click. Anyone can do it and everyone is doing it. That means most companies are losing the battle and tons of you are saying “what else is there?” Fortunately, the lead generation pie chart offers unlimited hope. You just need to think bigger and try harder.

If the other categories seem too ambitious, well then you’ll never make it in this biz kid…

Job Losses Possible Threat to MCA Industry / Google Penguin Kills Survivors / No Debit Card Savings

May 6, 2012How sure is this recovery?

A few months ago, all signs pointed to a roaring recovery. As the data comes in each month, it’s looking less and less like a definitive thing. Sure the unemployment rate is going down, but mainly because hundreds of thousands of people are giving up on searching for jobs. The Wall Street Journal recently analyzed a less popular statistic, the civilian labor participation rate. At present, the percentage of Americans working is at its lowest point since 1981.

At the same time, the nation’s largest banks are cutting back on loans to businesses yet again. It makes one wonder if the explosive growth being experienced in the Merchant Cash Advance industry will start to fizzle out in the 2nd half of this year.

Google Penguin wipes out the survivors

If you used blog networks like BuildMyRank to game Google into ranking your site higher, you probably noticed your website got whacked in late March. After years of spending precious money on marketing, 2012 brought upon the realization that leads generated from organic searches are not only possible, but free. This is of course before you factor in the thousands and tens of thousands that MCA funders and ISOs are spending a month on SEO. But since many SEO tactics are doomed to fail and because Google’s algorithm can change at any time, investing in organic rankings is incredibly risky.

If you used blog networks like BuildMyRank to game Google into ranking your site higher, you probably noticed your website got whacked in late March. After years of spending precious money on marketing, 2012 brought upon the realization that leads generated from organic searches are not only possible, but free. This is of course before you factor in the thousands and tens of thousands that MCA funders and ISOs are spending a month on SEO. But since many SEO tactics are doomed to fail and because Google’s algorithm can change at any time, investing in organic rankings is incredibly risky.

For example, one mid-sized MCA provider secretly shared that they had spent two years and nearly a hundred thousand dollars to get the rankings for the keywords they wanted on Google. Leads were just finally starting to come in on a daily basis when out of nowhere, they got thrown back to page 25. Blog networks were a big part of their strategy and when Google cracked down on them, the MCA provider’s presence on the Internet went down with the ship.

Some MCA companies survived the blog network armageddon only to become extinct on April 24th when Google made a key algorithm change to help defeat web spam. This major update has become notoriously known as Penguin. If you were a victim, you may need an SEO crisis management plan.

In any case, the changes at Google immediately affected unemployment in India, the country that most U.S. companies turn to for SEO services. As their clients sites disappeared from search results, so too did their contracts. At least that is the gag story surrounding a photoshopped image that has been going viral around the Internet.

Read our previous coverage on Merchant Cash Advance and SEO:

The SEO War for Merchant Cash Advance

The SEO War Continues

Debit card savings not being passed along

Remember when all those small business owners got their swipe rates reduced? Oh wait, that didn’t happen. The Durbin Amendment limited the interchange rates, which are the fees that acquiring banks pay to card issuing banks. The rates and fees charged to the small business are still left to the discretion of Merchant Service providers. Sure they can lower the cost if they so choose, but there’s no law that dictates they have to. It seems the Durbin Amendment victory was all one big misunderstanding for America’s retailers. We’ve been following this law since December, 2010. ISO&Agent Magazine just published an article titled, Unintended Results Plague Durbin Amendment. Are they seriously just figuring this out now?

Published by: Merchant Processing Resource

../../

Lenders Love One-Man Broker Shops, Rookie Broker Finds

January 5, 2022 “After meeting so many people at the Broker Fair in New York City, I was like, ‘you know what, now is the time for it. I’m young, so let’s take the risk and start my own company.’”

“After meeting so many people at the Broker Fair in New York City, I was like, ‘you know what, now is the time for it. I’m young, so let’s take the risk and start my own company.’”

Matt Dolecki, a 23-year old entrepreneur who owned and sold two businesses before he graduated high school, is taking the young hustler’s mindset to the alternative finance world. Just this week, Dolecki started his own brokerage; dubbing it Opulent Capital.

Although Dolecki wants to start funding deals immediately and create relationships across the space, he is aware that he needs to also focus on honing in on the foundations of his business if he wants true success.

“I think a lot of people when they enter this space try to grow too fast and too big too quickly,” he said. “I’m not here to grow extremely fast or extremely big. I’m here to establish a well-rounded company and not tarnish my work just trying to grow fast.”

After interning at a funding company after college and subsequently working for a commercial collections agency, Dolecki believes his experience seeing all sides of the process will set him aside from other brokers.

“I have enough knowledge and information for the merchant to not just broker them the deal, but inform the merchant and let them know exactly what they’re getting, what’s possible for them, and what’s the better option,” Dolecki said.

“I have the debt collection side, and I’ve worked in [small business funding], so I have a really well rounded knowledge of how this whole thing works. If someone were to default, I know exactly which way to go. I can guide the lender on exactly which way to go, I have all the contacts on both sides, lenders and brokers, as well as many debt collections agencies. So I can help lenders not only get business, but retain business and get back lost revenue.”

Not only is Dolecki confident that his experience will set him and his company aside from competitors, he also believes his strength in numbers, or lack of, will allow him to operate a smooth show.

“I’m a one man shop,” said Dolecki. “I’ve talked to a lot of lenders, and they like the idea of having one person to deal with. Information is directly to the source, directly to me and directly to the merchant. It’s an easier form of communication. Every lender I’ve talked to agrees that 90% of their best selling ISOs are one man shops.”

When speaking on creating an image for his company from the merchant’s perspective, Dolecki spoke extensively about different types of marketing. He says that a strategy seemingly based on the business owner’s age can determine what type of communication should be used to pitch that particular merchant.

“If you are trying to reach out to small business owners over the age of 60, most likely a call will be more beneficial rather than investing in marketing or SEO,” said Dolecki. “Now there are so many young business owners who all love technology and doing things online, so building a platform where you can use fintech to apply for loans and search different loan options would be much more beneficial to the younger business owners.”

“I think a good mix of using fintech, algorithms, and tech, but also cold calling and [even] reaching out by mail is an effective way of trying to find that perfect mix of using both types of merchants.”

Dolecki has received support from other brokerages in the industry and claims without help, he would never be in the position he is now.

“Shout out to Porsha and Mercedes Brooks at Brooks Partners Finance,” said Dolecki. “They’ve really been a big mentor for me starting out, and helping me to get the ball rolling. I’m now calling merchants, signing on as an ISO with different lenders, and still just getting started.”

Spotlight on AltFinanceDaily CONNECT Toronto

July 30, 2019 As the heat of the Toronto sun split the stones outside, the crowd inside the Omni King Edward’s seventeenth-floor Crystal Ballroom mingled and munched as part of AltFinanceDaily’s most recent CONNECT event.

As the heat of the Toronto sun split the stones outside, the crowd inside the Omni King Edward’s seventeenth-floor Crystal Ballroom mingled and munched as part of AltFinanceDaily’s most recent CONNECT event.

The first of its kind to be held in Toronto, the CONNECT series are half-day events that take place in both San Diego and Miami as well. Despite not being as established as the latter two, Toronto proved just as eventful, with a variety of speakers and topics broached, as well as a host of attendees from differing backgrounds making an appearance. It was par for the course for an inaugural AltFinanceDaily show with the attendance figures being reminiscent of AltFinanceDaily’s first ever event in the USA, a market that’s 10x the size.

The day was kicked off by entrepreneur, a dragon on the Canadian Dragons’ Den series, and co-founder of Clearbanc, Michele Romanow, whose anecdotes detailed the adventures that accompany the beginning of a startup. Regaling the audience with the story of Evandale Caviar, Romanow began with telling the room of a post-college venture that saw her working tooth and nail to secure a fishing license, studying YouTube fish gutting tutorials that were exclusively in Russian, and getting her hands dirty with the other co-founders when the time came to put their time spent online to use.

But it wasn’t all blood and glory for Romanow, as the tale shifted from one of youthful expansion to one of reflection and acceptance of the unknown. Speaking on the effect of tech giants in various fields, Romanow explained that “we have no idea of how these industries will shape out.” The likes of Uber and AirBnb never planned change the world, just to change a product and thus solve a problem, and their meteoric rises are unpredictable as a result. Iteration, rather than innovation, is what drives a company forward according to Romanow.

But it wasn’t all blood and glory for Romanow, as the tale shifted from one of youthful expansion to one of reflection and acceptance of the unknown. Speaking on the effect of tech giants in various fields, Romanow explained that “we have no idea of how these industries will shape out.” The likes of Uber and AirBnb never planned change the world, just to change a product and thus solve a problem, and their meteoric rises are unpredictable as a result. Iteration, rather than innovation, is what drives a company forward according to Romanow.

And this sentiment was brought further along with the following panel, which featured Vlad Sherbatov of Smarter Loans, Paul Pitcher of SharpShooter Funding, and SEO expert Paul Teitelman, speaking on the trials and novelties of the sales and marketing scene. Offering wisdom on various aspects of the field, the three men covered the need to go beyond the traditional forms of advertising, instead looking outward towards unorthodox methods of marketing; the hardships that come with the grind of a sales job; and the role that SEO can play when raising public awareness of your company; respectively.

“It’s a matter of spreading the word,” one conference goer noted when asked about the sales panel afterwards. “Businesses have to know who we are, and we’re working on that.”

“It’s a matter of spreading the word,” one conference goer noted when asked about the sales panel afterwards. “Businesses have to know who we are, and we’re working on that.”

Similarly, Martin Fingerhut and Adam Atlas discussed the existing legal topics of note to Canadian alternative financing companies, as well as those incoming rulings that may be worth knowing about. Covering both the English-speaking provinces and Quebec, the duo gave a comprehensive crash course on the legal landscape of the industry, highlighting laws unique to the regions. Aaron Iannello of Top Funding considered the talk to be particularly engaging, commending it for relaying information that might otherwise be unknown to American companies.

Following this, Kevin Clark, President of Lendified, took to the stage to talk about the importance of the Canadian Lenders Association (CLA). Saying that in the absence of a regulatory body, the CLA seeks to offer guidance to those companies who are looking for it. Clark asserted that “it’s a good thing for our industry to have oversight from a regularly body,” and that he looks forward to the day when one is established.

Following this, Kevin Clark, President of Lendified, took to the stage to talk about the importance of the Canadian Lenders Association (CLA). Saying that in the absence of a regulatory body, the CLA seeks to offer guidance to those companies who are looking for it. Clark asserted that “it’s a good thing for our industry to have oversight from a regularly body,” and that he looks forward to the day when one is established.

And before wrapping up the speakers for the day, Clark was joined by IOU Financial’s President, Robert Gloer, to discuss contemporary risk management. Covering everything from the next recession to the emergence of AI, the pair, which accumulatively have been in the industry for decades, offered knowledge learnt from years of experience in both the pre- and post-crash eras.

And the prophesizing of what will be the next big episode to shake the industry continued beyond the day’s scheduled agenda as many attendees continued on well into the evening at smaller networking functions offsite.

As the sun started to touchdown on the tips of Toronto’s skyscrapers, the salvo of excited conversation briefly harmonized to produce a singular axiom, that there was an abundance of opportunity in Canada.

How Most Americans Handle a $1000 Emergency Expense

December 26, 2018 A recent survey conducted by LendingTree found that more than half of Americans cannot cover a $1,000 emergency with cash or savings. Forty-eight percent of Americans say they could handle a $1,000 emergency expense by using cash or savings in their bank accounts.

A recent survey conducted by LendingTree found that more than half of Americans cannot cover a $1,000 emergency with cash or savings. Forty-eight percent of Americans say they could handle a $1,000 emergency expense by using cash or savings in their bank accounts.

Of the those Americans who could not handle a $1,000 emergency, whether it be a health issue or an urgent home repair, 16 percent said they would borrow from friends or family. Nine percent said they would sell something, another nine percent said they would use a credit card, seven percent said they would work more, and six percent said they would get a loan or paycheck advance.

Additionally, according to the report, six out of 10 Americans have had an emergency in the past year that cost them $1,000 or more and one-third of Americans are currently in debt from an emergency expense they could not afford cover. Of Americans who had to go into debt to cover a past emergency, one-third still owe $5,000 or more for this expense and about 18 percent have emergency debt balances of $10,000 or more.

LendingTree also announced at the end of last week that it has reached an agreement to acquire ValuePenguin for a total consideration of $105 million. ValuePenguin presents consumers and business owners with loan alternatives. In October, LendingTree acquired QuoteWizard.com, an insurance comparison marketplace, rounding out LendingTree as a more full financial advisory company.

“We are thrilled to add ValuePenguin’s talented team and expertise to our portfolio,” said Doug Lebda, Founder and CEO of LendingTree. “Our recent QuoteWizard acquisition was our first step toward leadership in insurance customer acquisition. Adding ValuePenguin’s high-quality content and SEO capability to QuoteWizard’s proprietary technology and carrier network will set us apart and enable us to provide immense value to carriers and agents. Both businesses will benefit from LendingTree’s strong brand and extensive marketing capabilities. We are in a great position to achieve further scale in the insurance space as well as the broader financial services industry.”

GOING NATIONAL: How David Gilbert Built One of the Largest Small Business Lenders in the Country

October 17, 2018 When Ty Austin, who owns a florist shop in West Palm Beach, secured a $5,000 loan from National Funding last year, he was happy to have working capital and could build inventory for mini-gardens and landscaping,

When Ty Austin, who owns a florist shop in West Palm Beach, secured a $5,000 loan from National Funding last year, he was happy to have working capital and could build inventory for mini-gardens and landscaping,

The experience, moreover, was surprisingly pleasant. “The guy I worked with was really cool,” Austin says, referring to the sales representative at the San Diego-based financial technology firm. “It turned out that he was getting married and I ended up giving him and his fiancé advice on floral arrangements.”

The borrowing worked out so well that the Floridian, who is 46 and the sole proprietor of Austintatious Designs, re-upped for a second loan of $12,000 to help purchase a commercial van. The van will be used to transport flowers, plants and tools while doubling as a billboard-on-wheels. “It gives me more ‘street cred,’” he jokes.

To register his approval with National Funding, Austin went online to TrustPilot and posted a rave review of the sales rep: “James Johnson Rocks!”

Pam, a Texas wellness coach who provides clients with an array of holistic health therapies, needed extra money to buy an infrared sauna to add to her portfolio of services. But her credit rating was “poor,” she told AltFinanceDaily in an e-mail interview, “from when I changed careers and lost my health and struggled to make my credit card and student loan payments on time.”

Like Austin, Pam — who asks to be identified by her first name —found National Funding through an online search. And she too secured $5,000, although her transaction was structured as a merchant cash advance, rather than a loan. The terms of the MCA require a daily debit from her bank account. She reckons that the total cost of the MCA to be roughly $1,500.

Pam pronounces herself satisfied with the deal and mightily impressed with the way National Funding treated her. The process took about three days — and would have gone even quicker if she’d located her professional licenses sooner. Best of all, she says, the agent at the company tailored the financing to suit her circumstances. “They were great as far as getting my questions answered, even listening to my past situation, which others may not have cared about,” she says.

Pam pronounces herself satisfied with the deal and mightily impressed with the way National Funding treated her. The process took about three days — and would have gone even quicker if she’d located her professional licenses sooner. Best of all, she says, the agent at the company tailored the financing to suit her circumstances. “They were great as far as getting my questions answered, even listening to my past situation, which others may not have cared about,” she says.

“They really wanted to get me an option that they knew I’d be able to repay,” Pam adds. “They said they were in the business of helping small businesses grow rather than putting them in a hard financial situation.”

The positive experiences that Austin and Pam had with National Funding are not isolated instances. Rather, they are representative of clients’ dealings with the company. Witness its online reviews from business borrowers at TrustPilot which go back three years, run for 36 pages, and merit National Funding a 9.4 rating on a scale of 10. That’s a straight-A grade on any report card. Although there’s the occasional naysayer — four percent assert that their experience was “poor” or “bad” (and some negative comments can be blistering) — the weight of the reviews is almost embarrassingly positive.

Typical postings find that National Funding and its agents win kudos for, among other things, being “prompt and professional,” providing service that is “hassle free and about as friendly as you can be,” and even being “accommodating and gracious.” A man named Al McCullough spoke for many when he declared: “My experience was great. Professional and on time. Couldn’t ask for more.”

All of which helps account for why National Funding — its 230 employees working out of a sleek suburban office building guarded by a tall stand of palm trees in San Diego — is a rising star in the world of alternative business lending and financial technology. In 2017, the company raked in $94.5 million in revenues, a 24.8 percent bounce over the $75.7 million recorded a year earlier and nearly fourfold the $26.7 million posted in 2013.

All of which helps account for why National Funding — its 230 employees working out of a sleek suburban office building guarded by a tall stand of palm trees in San Diego — is a rising star in the world of alternative business lending and financial technology. In 2017, the company raked in $94.5 million in revenues, a 24.8 percent bounce over the $75.7 million recorded a year earlier and nearly fourfold the $26.7 million posted in 2013.

In recognition of the company’s three-year growth rate of 142%, Inc. magazine included National Funding in its current list of the country’s 5,000 fastest-growing companies, the lender’s sixth straight appearance on the coveted roster. Since its inception in 1999, National Funding reports that it has originated more than $2 billion in loans to some 35,000 borrowers.

The company’s impressive performance has similarly merited accolades for David Gilbert, the 43-year-old chief executive who started the company on little more than a shoestring and whom employees regularly describe as “visionary.” Among Gilbert’s trophies: Accounting firm Ernst & Young recently presented him with its “Entrepreneur of the Year 2017 Award” for San Diego finance.

At first glance, the San Diego financier doesn’t look too much different from its cohorts. The company proffers unsecured loans of $5,000 to $500,000 to a mélange of small businesses in all 50 states and across multiple industries, including retail stores, auto repair shops, truckers, construction companies, heating-and plumbing contractors, spas and beauty salons, cafes and restaurants, waste management, medical and dental clinics, and insurance agencies.

To qualify for financing, a prospective borrower should have been in business for a year, have at least $100,000 in revenues, and boast a personal credit score of at least 500. While there’s no collateral required for loans, National Funding insists on a personal guarantee. The website reviewer NerdWallet cautions borrowers that this “puts your personal assets and credit at risk if you fail to repay the loan.”

Along with unsecured loans, National Funding offers equipment leasing – usually for heavy trucks and construction equipment – as well as merchant cash advances. The equipment lease is secured by the machinery. As in the case of Pam, the wellness coach cited above, MCAs are debited daily, the money automatically withdrawn from bank accounts.

There are a number of businesses that National Funding disdains, no matter how stellar their credit. “We won’t finance casinos, strip bars, tobacco, or firearms,” Gilbert says. “We’re not going to support industries like that.”

For CEO Gilbert, doing business ethically is a signature feature of the company. Among other things, National Funding presses its salespeople to steer clear of putting people into dodgy loans that are likely to default. “We’re lending capital,” Gilbert says, “and one of our core values is the way we support our customers. Are we placing people with the right product to meet their needs or are we being selfish? The best way to be customer oriented is to get a better understanding of what capital will do for them.”

That corporate ethos, coupled with the company’s remarkable performance, has raised its profile while earning it a measure of esteem among industry peers. “What I do know about National Funding,” says Douglas Rovello, senior managing partner at Fund Simple, a lender and broker in the Tampa area, “is that they have five or six different programs and set their rates high but competitively. They’re known for fitting their products to a client’s needs,” he adds. “And in a business that has its share of bad actors, they have a reputation as a company with a conscience.”

A company with a conscience. Customers come first. And yet National Funding turns heads with its sales production of roughly 1,000 financings a month and triple-digit growth rate. So how do they it? A good place to start is with Gilbert, whose leadership skills, business acumen, and second-to-none work ethic “set the tone,” says Kevin Bryla, the company’s 52-year-old chief marketing officer.

For his part, Gilbert credits his family background and an upbringing in which education and academic achievement were strongly encouraged. The fifth of six children, he’s the only one who opted for a business career. “There are three doctors, two lawyers – and me,” Gilbert says.

The son of a prominent physician, his mother a homemaker and volunteer docent at the nearby Nixon Library for the past 25 years, Gilbert grew up in Yorba Linda. He attributes his keen interest in business to observing how his father, a pathologist, operated his own laboratory, which employed 60 people. “It was the business side of medicine that fascinated me,” he asserts.

The son of a prominent physician, his mother a homemaker and volunteer docent at the nearby Nixon Library for the past 25 years, Gilbert grew up in Yorba Linda. He attributes his keen interest in business to observing how his father, a pathologist, operated his own laboratory, which employed 60 people. “It was the business side of medicine that fascinated me,” he asserts.

Even so, his two closest friends at the University of Southern California — fraternity brothers Marc Newburger and Sean Swerdlow– tell a somewhat different story. They remember Gilbert as someone who found his true calling, his métier, during his college years. Enrolled initially in pre-med courses, he was a diligent student but, his friends assert, manifestly unsuited for a career in medicine.

“Formative,” says Swerdlow, the older of the two fraternity brothers and now a management consultant based in Southern California, “would be a very good word” to characterize that period during which Gilbert abandoned medicine in favor of the world of commerce. In 1997, he earned a bachelor’s degree in business administration “with an emphasis in entrepreneurship.”

But it was fraternity life just as much as the classroom, his friends agree, that shaped him and foreshadowed his future. “It wasn’t ‘Animal House,’” Swerdlow says of Alpha Epsilon Pi. “We boasted the highest GPA (grade point average) on fraternity row.”

Nonetheless, Gilbert took to the social life and camaraderie that the fraternity offered with gusto, and his friendship with the colorful Newburger was especially fateful. A freewheeling entrepreneur today, Newburger takes a measure of credit — Gilbert’s disapproving parents might have preferred the word “blame” — for contributing to his fraternity brother’s metamorphosis. “Dave hated all of his pre-med classes,” Newburger insists. “He had zero stomach for it. He was so much like I was: a natural people person and a born entrepreneur.”

Newburger is the quintessential soldier of fortune. After college, he tried his hand as an actor, supporting himself by playing poker and getting paid to be a contestant on TV game shows including “The Dating Game,” “Card Sharks,” and “3’s A Crowd.” He’s now the co-president and co-inventor of Drop Stop, a patented device that “minds the gap” between a car’s front seat and the console and prevents coins, keys, glasses, and mobile phones from disappearing down that rabbit hole. (Drop Stop really took off after Newburger and his business partner appeared on the television show “Shark Tank” and scored a $300,000 capital injection from celebrity-investor Lori Greiner who took a 30% stake in the company and slapped her name on the brand.)

Back at the frat house, Newburger and Gilbert collaborated on business ventures. The pair once sold T-shirts sporting an off-color message about USC’s archrival, the University of California at Los Angeles. “The (anti-UCLA) message was pure hatred,” Newburger recalls. “But it was just for the day of the football game and it was all in fun.”

At first, sales at the stadium were lackluster. USC students kept trying to bid down the price or importune them to throw in an extra tee. As for the game itself, USC’s chances for victory looked equally unpromising. As time ran out, however, the Trojan quarterback completed a Hail Mary pass and USC won. The two fraternity brothers grabbed the bundle of shirts and sprang into action. “We got to the exit just in time and sold out in a matter of seconds,” Newburger recalls.

Newburger takes credit too for introducing his friend to Las Vegas’ gaming tables. Gilbert, his friend says, immediately demonstrated a knack for counting cards, handling money, and taking risks. “It was typically blackjack,” recalls Swerdlow, who sometimes accompanied them. “We didn’t have much money then. But there were moments when Dave would bet a big pile of chips. He’s willing to make a bet and live with the consequences.”

Sports are another of Gilbert’s enthusiasms. His friends say that, whether he’s returning serve at ping pong or standing over a putt — he plays to an 11 handicap at golf – he wants to win. Remarks Newburger: “He’s competitive to the point that — when he beats you — he wants the Goodyear blimp flying overhead to announce his victory.”

Gilbert, who is married with two children, is legendarily loyal to friends and family. While most members of a college fraternity might keep up with old companions after graduation by exchanging greeting cards and attending college reunions, Gilbert goes the extra mile.

He once footed the bill for Swerdlow to travel with the USC football team to an away game, arranging it so that his fraternity brother could view the action from field-level. After Newburger had a recent health scare (no worries, he’s O.K.), Gilbert rounded up a couple of dozen fraternity brothers and their wives (or companions), and put together a four-day bash in his buddy’s honor. The event was held at Cabo, the Mexican beach resort in Baja California, and Gilbert underwrote a fair amount of the cost. “He shares his success with his friends,” Newburger says, adding: “I don’t know anybody who works harder on friendships.”

He once footed the bill for Swerdlow to travel with the USC football team to an away game, arranging it so that his fraternity brother could view the action from field-level. After Newburger had a recent health scare (no worries, he’s O.K.), Gilbert rounded up a couple of dozen fraternity brothers and their wives (or companions), and put together a four-day bash in his buddy’s honor. The event was held at Cabo, the Mexican beach resort in Baja California, and Gilbert underwrote a fair amount of the cost. “He shares his success with his friends,” Newburger says, adding: “I don’t know anybody who works harder on friendships.”

Many of the personality traits described by friends and colleagues — tenacity and competitiveness, self confidence and leadership — played a key role in the development and success of National Funding, which Gilbert founded just two years out of college with $10,000 borrowed from his uncle, Howard Kaiman, of Omaha.

He’d worked a couple of quick jobs right after college, including a stint at small-business lender Balboa Capital, but he was always destined to be his own boss. Gilbert’s start-up was called Five Point Capital and, at first, it was located in the affluent Chatsworth section of Los Angeles and concentrated on equipment leasing.

“The first two years we were a cold-calling company and then we got into direct mail and saw some success and then we moved to San Diego and started to scale up the company,” Gilbert says. The decampment, he explains, was “for the quality of life, but we also felt we could hire from a better talent pool than L.A. We wanted to set ourselves apart.”

By 2007, Five Point was cranking up operations, revenues shot to $28 million and its headcount totaled 210 employees. “Then the Great Recession hit” in 2008-2009, Gilbert says. The company was forced to furlough 140 employees, two-thirds of its workforce. Yet even as it retrenched, the company managed to branch out. It began making merchant cash advances, Gilbert says, and, also in 2007, it linked up with CAN Capital to do broker financings. “We were pretty well known and they were looking for partners for factoring and leasing,” Gilbert explains.

It took time to recover after the financial crisis. But by 2013 – the year that Gilbert re-branded his company “National Funding” – the company was able to hire back as many as 15% of its laid-off employees (most had found other jobs, in many cases relocating to Silicon Valley, Gilbert reports). By then, the company had secured a $25 million credit facility from Wells Fargo Bank, which allowed it to move up the food chain to “become a balance-sheet lender,” Gilbert says, and offer a wider selection of financing options.

Key to driving the company’s phenomenal growth has been its flood-the-zone marketing and sales strategies. The company spends $16 million annually on marketing using a full panoply of channels and media, both online and offline. These include direct mail and targeted marketing, paid advertising, search-engine optimization or SEO, and sports sponsorships. “We try to build a whole range of marketing mechanisms,” explains marketing chief Bryla, “and when you get the mix right, they all help each other.”

Gilbert is a big believer in the benefits of sports marketing, the company’s website featuring the logos of the San Diego Padres (baseball), and Anaheim Ducks and Los Angeles Kings (hockey). Ever the faithful alumnus, Gilbert and his company back USC football as well. During the 2015 2016 college football season, the company paid for naming rights for what became, for one night, the “National Funding Holiday Bowl” at Qualcomm Stadium.

Gilbert is a big believer in the benefits of sports marketing, the company’s website featuring the logos of the San Diego Padres (baseball), and Anaheim Ducks and Los Angeles Kings (hockey). Ever the faithful alumnus, Gilbert and his company back USC football as well. During the 2015 2016 college football season, the company paid for naming rights for what became, for one night, the “National Funding Holiday Bowl” at Qualcomm Stadium.

Janet Fink, department chair at the McCormack School of Sports Management located at the University of Massachusetts-Amherst, told AltFinanceDaily that sponsorship programs can easily cost a million dollars or more. “It’s not cheap,” she says. “When a company sponsors a team, they get a number of benefits. One is that they get to put the team’s logo on their website. The idea is that fans are passionate or have an affinity for the team and that it will rub off on a sponsor.

“Sports enthusiasts,” Fink adds, “often make good customers. When you have enough disposable income to go to these sporting events, you’re probably a good prospect for a loan.”

The sponsorships — which include civic involvement such as offering Holiday Bowl tickets to members of San Diego’s large military contingent as well as to company employees — also build good will in the community and team spirit among the workforce. (National Funding also makes an effort to hire veterans, says Bryla.)

Gilbert believes in the old adage that you have to spend money to make money. The company spends $14 million rewarding its network of outside brokers. Inside the company, high-performing salespeople are compensated with commissions, bonuses and an assortment of rewards, including resort trips.

But sales representatives’ must conform to company guidelines. Justin Thompson, National Funding’s sales chief, explains that the “customer comes first” philosophy is not just a slogan but a core value. “We’re not a factory spitting out widgets,” Thompson says. “We’re here to build relationships and sell a repeatable product. We want that customer to come back to us. Every loan is customized. Six of ten customers who pay off their loans come back for a second financing. Whether your business is dog grooming or you’re an asphalt company,” he adds, “people will do business with people they like and trust.”

Using the software program “customer relationship management” (CRM), National Funding expends a lot of effort gathering data on its business customers and extrapolating the information for use in credit evaluations. But the use of technology only goes so far.

Gilbert reckons that the art of the deal involves about “70 percent algorithm and 30 percent people.” He adds, “You still need the people component to look at credit profiles. The algorithm spits out a recommendation but we still need the human element.”

Gilbert reckons that the art of the deal involves about “70 percent algorithm and 30 percent people.” He adds, “You still need the people component to look at credit profiles. The algorithm spits out a recommendation but we still need the human element.”

If there’s a fly in the National Funding ointment, it’s that the company’s fees can be more expensive than a bank loan.

But borrowers who have been denied loans at a bank or other lender are likely to overlook those costs. Austin, the florist in West Palm Beach, for example, came to National Funding when his bank, North Carolina-based BB&T Bank, gave him the cold shoulder despite the $15,000 in deposits that he averages each month. “I’ve been with them for six years,” he fretted, “and they treated me shabbily.”

Even more grateful was Jimmy Frisco, of Annapolis, who is co-owner with his wife of Lisa’s Luncheonette, a business that includes a food trailer and several cafeterias located in the city’s office buildings. They employ about a dozen people.

Frisco had taken a nasty spill and was laid up for seven months. Health insurance covered the $18,000 in medical costs but he and Lisa fell behind in their bills and needed working capital to pay for food purchases and other business expenses. By the time a flyer from National Funding popped up in his mailbox, he and his wife “had been turned down by several other lenders, including banks,” he says, adding: “Things happen in life and we don’t have the best of credit.”

Getting that loan for $25,000 from National Funding took just three days. Frisco’s health is much improved and business is back to normal. He won’t discuss the terms of the financing, other than to say “it was reasonable.”

He adds: “There were no problems with National Funding, no hassle with the paperwork. They’re great people to work with.”