Treasury Warns of Audits as Public Companies Return PPP Money

April 28, 2020 In the wake of public outrage at the news that public companies have received millions of dollars from the Paycheck Protection Program, Treasury Secretary Steven Mnuchin today spoke out against such businesses. His comments come after the SBA and Treasury further clarified which businesses actually qualify for PPP, noting that only companies with no access to other forms of capital, such as selling shares or debt, would qualify.

In the wake of public outrage at the news that public companies have received millions of dollars from the Paycheck Protection Program, Treasury Secretary Steven Mnuchin today spoke out against such businesses. His comments come after the SBA and Treasury further clarified which businesses actually qualify for PPP, noting that only companies with no access to other forms of capital, such as selling shares or debt, would qualify.

Speaking on Fox Business, the Treasury Secretary explained that “anybody who took the money that shouldn’t have taken the money, one, it won’t be forgiven and two, they may be subject to criminal liability, which is a big deal … I encourage everybody to look at this and pay back these loans now so we can recycle the money if you made a mistake.” Mnuchin made clear that any company that receives a loan of over $2 million will be audited by the SBA.

A number of cases have made headlines, with Shake Shack and Ruth’s Chris Steak House returning $10 and $20 million, respectively, following calls from the public to refund it. Other publicly funded companies that have returned PPP money include AutoNation ($77 million); Penske Automotive Group Group ($66 million); and the Los Angeles Lakers basketball franchise, which received $4.6 million.

“I’m a big fan of the team but I’m not a big fan of the fact that they took a $4.6 million loan,” Mnuchin said of the Lakers. “I think that’s outrageous and I’m glad they returned it or they would have had liability.”

With the launch of the second round of PPP funding yesterday, the SBA reported that it had processed more than 100,000 loans by 4,000 lenders by 3:30pm that day. Senator Marco Rubio explained on Twitter that a new pacing mechanism had been integrated into the SBA’s E-Tran portal system, lowering the minimum amount of PPP loan applications required for lenders to send a bulk submission from 15,000 to 5,000. The hope for this is that it will enable smaller businesses to reach the funds through more regional lenders and “allow more banks to submit,” explained Rubio.

That’s All Folks? – The PPP Money Is Already Gone

April 15, 2020

Update 4/16/20: The SBA has put up an official statement on its website that says “The SBA is currently unable to accept new applications for the Paycheck Protection Program based on available appropriations funding. Similarly, we are unable to enroll new PPP lenders at this time.”

A number of fintech companies have just joined the Paycheck Protection Program, but they’re a tad late to the PPParty. On Twitter, Senator Marco Rubio, one of the co-sponsors of the CARES ACT that developed this program, confirmed the rumors that the well had run dry. “Sadly it appears #PPP will grind to a halt tonight as the limit on $ allocated to guarantee #PPPloans about to be hit.”

Sadly it appears #PPP will grind to a halt tonight as the limit on $ allocated to guarantee #PPPloans about to be hit.

Now 700000 small business applications are in limbo & no new loans will be made until the game of chicken in Congress ends & additional $ approved.

Inexcusable

— Marco Rubio (@marcorubio) April 15, 2020

Here’s the math

Congress approved $349 billion to guarantee #PPP

At 2pm today had over $300 billion in approved #PPPloans

Need $10 billion to cover fees & processing

When we reach $339 billion limit PPP will stop until they end with the ridiculous games & approve more funds

— Marco Rubio (@marcorubio) April 15, 2020

The SBA has often made reference to total funds “approved” when calculating its numbers rather than loaned out, so if you’re a business that has already been approved, then presumably funds have already been allocated for your business and you will still receive them. But if your application is pending, well it’s possible that funding may require additional congressional authorization. That however, as noted by Rubio’s remarks, will require some political compromise.

Update: 4/16 8 AM: Senator Rubio said on Fox Business that the PPP program was now frozen after having reached its limit and has stopped.

We’ll update this as more information becomes available.

Get The Affidavit or Waive It? Examining Confessions of Judgment

February 1, 2019 Caton Hanson, the chief legal officer and co-founder of the online credit-reporting and business-to-business matchmaker Nav, says that his Salt Lake City-based company would not associate with a small-business financier that included “confessions of judgment” in its credit contracts.

Caton Hanson, the chief legal officer and co-founder of the online credit-reporting and business-to-business matchmaker Nav, says that his Salt Lake City-based company would not associate with a small-business financier that included “confessions of judgment” in its credit contracts.

“If we understood that any of our merchant cash advance partners were using confessions of judgment as a means to enforce contracts,” Hanson told AltFinanceDaily, “we would view that as abusive and distance ourselves from those partners. As a venture-backed company,” Hanson adds, “we have some significant investors, including Goldman Sachs, and I’m sure they would support us.”

Steve Denis, executive director of the Small Business Finance Association, which represents companies in the merchant cash advance (MCA) industry, says that, as an organization, “We’ve taken a strong stance against confessions of judgment.”

He reports that his Washington, D.C.-based trade group is prepared to work with legislators and policy-makers of any political party, regulators, business groups and the news media “to ban that type of practice.

“We’re fighting against the image that we’re payday lenders for business,” Denis says of the merchant cash advance industry. “We’re trying to figure out internally what we can do to stop that from happening and we have been speaking to members of Congress and their staff.”

“Confessions of judgment,” says Cornelius Hurley, a law professor at Boston University and executive director of the Online Lending Policy Institute, “are to the merchant cash advance industry what mandatory arbitration is to banks. Neither enforcement device reflects well on the firms that use them.”

These are just some of the reactions from members of the alternative lending and financial technology community to a blistering series of articles published by Bloomberg News on the use—and alleged misuse—of confessions of judgment (COJs) by merchant cash advance companies. The series charges the MCA industry with gulling unwary small businesses by not only charging high interest rates for quick cash but of using confession-laden contracts to seize their assets without due process.

The Bloomberg articles also reported that it doesn’t matter in which state the small business debtors reside. By bringing legal action in New York State courts, MCA companies have been able to use enforcement powers granted by the confessions to collect an estimated $1.5 billion from some 25,000 businesses since 2012.

“I don’t think anyone can read that series of articles and honestly say what went on were good practices and in the best interest of small business,” says SBFA’s Denis, noting that none of the companies cited in the Bloomberg series belonged to his trade group. “It’s shocking to see some companies in our space doing things we’d classify as predatory,” he adds. “As an industry we’re becoming more sophisticated, but there are still some bad actors out there.”

A confession of judgment is a hand-me-down to U.S. jurisprudence from old English law. The term’s quaint, almost religious phrasing evokes images of drafty buildings, bleak London fog, and dowdy barristers in powdered wigs and solemn black gowns. (And perhaps debtor prisons as well.)

A confession of judgment is a hand-me-down to U.S. jurisprudence from old English law. The term’s quaint, almost religious phrasing evokes images of drafty buildings, bleak London fog, and dowdy barristers in powdered wigs and solemn black gowns. (And perhaps debtor prisons as well.)

Yet while the legal provision’s wings have been clipped—the Federal Trade Commission banned the use of confessions of judgment in consumer credit transactions in 1985 and many states prohibit their use outright or in such cases as residential real estate contracts—COJs remain alive and well in many U.S. jurisdictions for commercial credit transactions.

Even so, most states where COJs are in use, such as California and Pennsylvania, have adopted safeguards. Here’s how the San Francisco law firm Stimmel, Stimmel and Smith describes a COJ.

“A confession of judgment is a private admission by the defendant to liability for a debt without having a trial. It is essentially a contract—or a clause with such a provision—in which the defendant agrees to let the plaintiff enter a judgment against him or her. The courts have held that such a process constitutes the defendant’s waiving vital constitutional rights, such as the right to due process, thus (the courts) have imposed strict requirements in order to have the confession of judgment enforceable.”

In California, those “strict requirements” include not only that a written statement be “signed and verified by the defendant under oath,” but that it must be accompanied by an independent attorney’s “declaration.” If no independent attorney signs the declaration or—worse still—the plaintiff’s attorney signs the document, the confession is invalid.

But if the confession is “properly executed,” the plaintiff is entitled to use the full panoply of tools for collection of the judgment, including “writs of execution” and “attachment of wages and assets.”

In Pennsylvania, confessions of judgment are nearly as commonplace as Philadelphia Eagles’ and Pittsburgh Steelers’ fans, particularly in commercial real estate transactions. Says attorney Michael G. Louis, a partner at Philadelphia-area law firm Macelree Harvey, “They may go back to old English law, but if you get a business loan or commercial lease in Pennsylvania, a confession of judgment will be in there. It’s illegal in Pennsylvania for a consumer loan or residential real estate. But unless it’s a national tenant with a ton of bargaining power—a big anchor store and the owner of the shopping center really wants them—95% of commercial leasing contracts have them.

In Pennsylvania, confessions of judgment are nearly as commonplace as Philadelphia Eagles’ and Pittsburgh Steelers’ fans, particularly in commercial real estate transactions. Says attorney Michael G. Louis, a partner at Philadelphia-area law firm Macelree Harvey, “They may go back to old English law, but if you get a business loan or commercial lease in Pennsylvania, a confession of judgment will be in there. It’s illegal in Pennsylvania for a consumer loan or residential real estate. But unless it’s a national tenant with a ton of bargaining power—a big anchor store and the owner of the shopping center really wants them—95% of commercial leasing contracts have them.

“And any commercial bank in Pennsylvania worth its salt includes them in their commercial loan documents,” Louis adds.

Pennsylvania’s laws governing COJs contain a number of additional safeguards. For example, the confession of judgment is part of the note, guaranty or lease agreement—not a separate document—but must be written in capital letters and highlighted. One of the defenses that used to be raised against COJs, Louis says, was that a contractual document was written in fine print “but we haven’t seen fine print for years.”

Other reforms in Pennsylvania have come about, moreover, as a result of a 1994 case known as “Jordan v. Fox Rothschild.” Says Louis: “It used to be lot worse. You used to be able to file a confession of judgment and levy on a defendant’s bank account before he knew what happened. It was brutal. But after the Fox Rothschild case, they changed the law to prevent taking away a defendant’s right of notice and the opportunity to be heard.”

Because of that case, which takes its name from the Fox Rothschild law firm and involved a dispute between a Philadelphia landlord renting commercial space to Jordan, a tenant, the law governing COJs in Pennsylvania requires, among other things, a 30-day notice before a creditor or landlord can execute on the confession. During that period the defendant has the opportunity to stay the execution or re-open the case for trial.

Defenses against the execution of a COJ can entail arguments that creditors failed to comply with the proper language or procedures in drafting the document. But the most successful argument, Louis says, is a “factual defense.” Louis cites the case of a retail clothing store renting space in a shopping center that has a leaky roof. In the 30-day notice period after the landlord invoked the confession of judgment, the tenant was able to demonstrate to the court that he had asked the landlord “ten times” to fix the roof before spending the rent money on roof repairs. In such a case, the courts will grant the defendant a new trial but, Louis says, the parties typically reach a settlement. “Banks generally will waive a jury trial,” he notes, “because they don’t want to take a chance of getting hammered by a jury.”

Defenses against the execution of a COJ can entail arguments that creditors failed to comply with the proper language or procedures in drafting the document. But the most successful argument, Louis says, is a “factual defense.” Louis cites the case of a retail clothing store renting space in a shopping center that has a leaky roof. In the 30-day notice period after the landlord invoked the confession of judgment, the tenant was able to demonstrate to the court that he had asked the landlord “ten times” to fix the roof before spending the rent money on roof repairs. In such a case, the courts will grant the defendant a new trial but, Louis says, the parties typically reach a settlement. “Banks generally will waive a jury trial,” he notes, “because they don’t want to take a chance of getting hammered by a jury.”

A number of states, including Florida and Massachusetts ban the use of confessions of judgment. That’s one big reason that Miami attorney Roger Slade, a partner at Haber Law, advises clients that “there’s no place like home.” In other words: commercial contracts should specify that any legal disputes will be adjudicated in Florida. “It’s like having home field advantage in the NFL playoffs,” Slade remarked to AltFinanceDaily. “You don’t want to play on someone else’s turf.”

He has also been warning Floridians for several years against the way that COJs were treated by New York courts. Writing in the blog, “The Florida Litigator,” Slade—a native New Yorker who is certified to practice law there as well as in Florida counseled in 2012: “If you live in New York, a creditor can have your client sign a confession of judgment and, in the event of a default on a loan, can march directly to the courthouse and have a final judgment entered by the clerk. That’s right—no complaint, no summons, no time to answer, no two-page motion to dismiss. The creditor gets to go right for the jugular.”

In addition, because of the “full faith and credit clause of the U.S. Constitution,” Slade notes in an interview, a contract that’s enforced by the New York courts must be honored in Florida. “Courts in Florida have no choice,” Slade says. “It’s a brutal system and it’s unfortunate.”

In December, two U.S. senators from opposing parties—Ohio Democrat Sherrod Brown and Florida Republican Marco Rubio—introduced bipartisan legislation to amend both the Federal Trade Commission Act and Truth in Lending Act to do away with COJs. Their legislative proposal reads:

“(N)o creditor may directly or indirectly take or receive from a borrower an obligation that constitutes or contains a congnovit or confession of judgment (for purposes other than executory process in the State of Louisiana), warrant of attorney, or other waiver of the right to notice and the opportunity to be heard in the event of suit or process theron.”

But with a dysfunctional and divided federal government, warring power factions in Washington, and an influential financial industry, there’s no telling how the legislation will fare. Meantime, the New York State attorney general’s office announced in December that it will investigate the use of COJs following the Bloomberg series. And New York Governor Andrew Cuomo has declared support for legislation that will, among other things, prohibit the use of confessions in judgment for small business credit contracts under $250,000 and restrict judgments by New York courts to in-state parties.

But if New York State or Congressional legislation are adopted it can have “unintended consequences” to merchant cash advance firms in the Empire State—and to their small business customers as well—asserts the general counsel for one MCA firm. “Losing the confession of judgment will be removing what little safety net there is in a risky industry,” the attorney says, noting that the industry has roughly a 15% default rate.

“It is not as powerful a tool as the Bloomberg news stories would have you believe,” this attorney, who spoke on the condition of anonymity, told AltFinanceDaily. “The suggestion seems to be that the MCAs can use the confession of judgment to get back the total amount of money due—and then some—while leaving a trail of dead bodies behind. But that’s not the case.

“What is much more likely to be the case,” he adds, “is that MCA companies try to get the defaulting merchant back on track. And—probably more than we should and only after we’ve tried to reach out to them and failed—do we then reluctantly use the COJ as a last resort. At which point we hope we can recover some part of our exposure. The numbers vary, but the losses are always in the thousands of dollars. These are not micro-transactions.

“What’s going to happen,” he concludes, “is that It will not make sense for us to work with those merchants most in need of working capital. The unfortunate reality is that businesses who don’t have collateral and can’t get a Small Business Administration product will be left out in the cold.”

All of which prompts BU professor Hurley to argue that the “Swiss cheese” system of financial regulation among the 50 states continues to be a root cause of regulatory confusion. Echoing Miami attorney Slade’s concern about New York courts’ dictating to Florida citizens, Hurley likens the situation governing COJs with the disorderly array of state laws governing usury regulations.

In the 1978 “Marquette” decision, the U.S. Supreme Court ruled that a Nebraska bank, First of Omaha, could issue credit cards in Minnesota and charge interest rates that exceeded the usury rate ceiling in the Gopher State. Since then, usury rates enacted by state legislatures have become virtually unenforceable.

“The problem we’re seeing with confessions of judgment is a subset of the usury situation,” Hurley says. “One state’s disharmony becomes a cancer on the whole system. It’s a throwback to Colonial times with 50 states each having their own jurisdictions—and it doesn’t work.”

Hurley’s Online Lending Policy Institute has joined with the Electronic Transactions Association and recruited a phalanx of “academics, non-banks, law firms and other trade associations as members or affiliates” to form the Fintech Harmonization Task Force. It is monitoring the efforts by the 50 states to align their regulatory oversight of the booming financial technology industry which was recently recommended by a U.S. Treasury report.

Hurley’s Online Lending Policy Institute has joined with the Electronic Transactions Association and recruited a phalanx of “academics, non-banks, law firms and other trade associations as members or affiliates” to form the Fintech Harmonization Task Force. It is monitoring the efforts by the 50 states to align their regulatory oversight of the booming financial technology industry which was recently recommended by a U.S. Treasury report.

Tom Ajamie, who practices law in New York and Houston and has won multimillion-dollar, blockbuster judgments against “dozens of financial institutions” including Wall Street investment firms, also argues for greater regulatory oversight. He urges greater funding and expansion of the powers of the Consumer Financial Protection Bureau to rein in “the anticipatory use” of confessions of judgment in commercial transactions.

However, notes Catherine Brennan, a partner at Hudson Cook in Baltimore, the job of protecting small businesses is outside the agency’s mandate. “The CFPB doesn’t have authority over commercial products as a general rule,” she explained in an interview. “Consumers are viewed as a vulnerable population in need of protections since the 1960’s.” As a society “we want protection for households because the consequences are high. A family could become homeless if they lose a house. Or (they) could lose employment if they lose a car and can’t drive. And there is also unequal bargaining power between lenders and consumers.

“Large institutions have lawyers to draft contracts and consumers have to agree on a take it or leave it basis. So there’s not a lot of negotiation and government has decided that consumers need protections, including a (Federal Trade Commission) ban on confessions of judgment.”

But Christopher Odinet, a law professor at the University of Oklahoma and a member of Hurley’s harmonization task force, sees the efforts of the federal government and the states to grapple with confessions of judgment as further recognition that small businesses have more in common with consumers than with big business. The COJ controversy follows on the recent passage of a commercial truth-in-lending bill by the State of California which, for the first time, stipulated that consumer-style disclosures should be included in business loans and financings under $500,000 made by non-bank financial organizations.

He cites the close-to-home example of an accomplished professional who got in over his head in financial dealings. “I recently observed a situation where a family member who is a very successful and affluent medical professional was relying on his own untrained business skills,” Odinet says. “He was about to enter into a sophisticated and complex business partnership relying on his intuition and general sense of confidence in the other party.”

Odinet says that he recommended that his relative hire a lawyer. Which, Odinet says, he did.

Lights, Camera, Crypto-Transaction – How a Lending Journalist Raised Millions to Build Magic Lamps Through the Murky World of Initial Coin Offerings

November 15, 2017

This past July, the winner of the Best Journalist Coverage category at the 2017 LendIt Conference Awards, announced that he would be stepping outside of his journalistic endeavors to raise money for a futuristic lamp company. The product, dubbed Lampix, is described as a lamp with a projector, a camera, specifically placed light-emitting diodes (LEDs), and a cloud-enabled computer. On the company’s “Medium” blog, Lampix promises that the product is “designed to transform any flat horizontal surface into an interactive computer.”

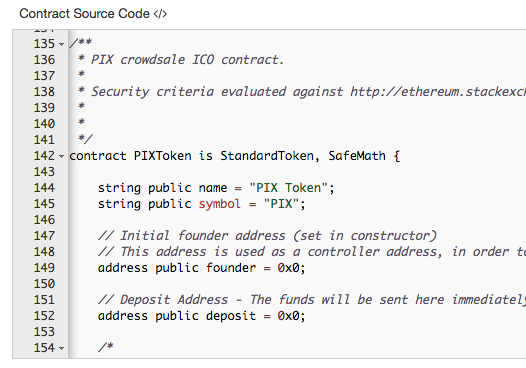

The man behind Lampix, George Popescu (whose Lending Times news site competed against and beat out fellow finalist AltFinanceDaily at the LendIt Awards), makes for an interesting case study in alternative finance. That’s because Lampix shunned traditional capital-raising methods by relying on an Initial Coin Offering (or ICO), an unregulated blockchain-based corporate event which is similar to an initial public offering. Rather than purchasing shares, as is the case in an IPO, investors in an ICO receive digital tokens instead of shares. In August, Lampix raised $14.2 million through its ICO*.

Popescu’s name popped up again a few months after the LendIt award on a regulatory blotter in the UK.

Popescu’s name popped up again a few months after the LendIt award on a regulatory blotter in the UK.

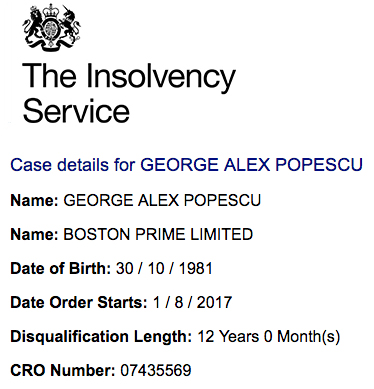

In case details published by the UK’s Insolvency Service on August 1st, the agency announced that Popescu was disqualified from serving as a company director.

Mr Popescu breached his fiduciary duties to act in the best interest of Boston Prime Limited (“Boston Prime”) and/or failed to ensure that both Boston Prime, as the regulated firm, and him individually, as the approved person, complied with the Financial Conduct Authority (“the FCA”) rules and guidance.

$6.2 million was transferred out of the company to a company named FXDD. Boston Prime’s receiver is presently suing FXDD seeking the return of the funds to the company. Proceedings are ongoing. Mr. Popescu is not under investigation and there are no legal proceedings at this time against Mr. Popescu.

It’s an inauspicious beginning for someone financing the “lamp of the future” using an unregulated and controversial strategy. Even so, when its ICO concluded on August 19, Lampix declared its gambit a success after raising $14.2 million through the sale of its digital tokens, which are known as PIX.**

By mid-November, the market value of those digital tokens, which exist on the Ethereum blockchain, had dropped by 50%, causing Lampix investors to suffer losses of $7 million. Unlike shareholders in publicly traded companies, token buyers have few investor protections. It’s not clear they are even considered to be actual investors at all. Buried in the fine print of Lampix’s 85-page “white paper” – a convenient way to avoid the label of prospectus – is a disclaimer. “Buyer should not participate in the [PIX] Token Distribution or purchase [PIX] Tokens for investment purposes. [PIX] Tokens are not designed for investment purposes and should not be considered as a type of investment.”

Additional disclaimers, moreover, declare that the white paper is not a prospectus, that the tokens “are not securities, commodities, swaps on either securities or commodities, or a financial instrument of any kind.”

But the distinction has not deterred people from joining in the frenzy of buying digital tokens like PIX. So much so, TechCrunch reports companies employing this strategy had raised nearly $800 million by means of ICOs in the first half of 2017.

And the SEC is not exactly excited about ICOs. “Fraudsters often use innovations and new technologies to perpetrate fraudulent investment schemes,” a July 29 directive by the SEC states. “Fraudsters may entice investors by touting an ICO investment ‘opportunity’ as a way to get into this cutting-edge space, promising or guaranteeing high investment returns. Investors should always be suspicious of jargon-laden pitches, hard sells, and promises of outsized returns. Also, it is relatively easy for anyone to use blockchain technology to create an ICO that looks impressive, even though it might actually be a scam.”

On September 29, moreover, the SEC brought an enforcement action against REcoin Group, charging Los Angeles businessman Maksim Zaslavskiy and two companies he controls with defrauding investors “in a pair of so-called initial coin offerings (ICOs) purportedly backed by investments in real estate and diamonds,” an SEC press release said.

The SEC alleges that Zaslavskiy and his companies –REcoin Group Foundation and DRC World (also known as Diamond Reserve Club) — have been selling unregistered securities, and that “the digital tokens or coins being peddled don’t really exist.”

Meanwhile, telephone calls and an e-mail to the SEC seeking the federal regulator’s view on Lampix’s ICO drew a terse response from Ryan T. White, a public affairs specialist, who replied that the agency would “decline comment.”

Meanwhile, telephone calls and an e-mail to the SEC seeking the federal regulator’s view on Lampix’s ICO drew a terse response from Ryan T. White, a public affairs specialist, who replied that the agency would “decline comment.”

Deborah Meshulam, a partner in the Washington office of law firm DLA Piper and a former SEC enforcement official, told AltFinanceDaily: “Regarding the lack of equity ownership, Lampix is seeking to establish that the tokens are not securities. Whether the SEC would agree should it decide to look into the offering depends on the facts and circumstances. The SEC staff would look past form to substance to assess whether the sale of the tokens constitutes an investment contract under legal standards. If so, then the SEC would view the Lampix offering as a securities offering. It may be that Lampix (or its lawyers) already vetted the offering with the SEC but I don’t know the answer.”

Popescu tells AltFinanceDaily in an e-mail interview, “We had to respect all securities rules and regulations of course, respect the Howey test and so on. There were no hoops to jump through as we are not trying to avoid anything or prevent anything. We honestly built a token to build a community to help us crowdsource (mine) pictures for all applications among which, Lampix.”

“Each PIX token,” the Lampix website explains, “will be used as a form of payment to picture image miners, voters and app developers or to purchase a Lampix, cloud computing and apps.”

Meshulam also notes that the June, 2017, date of the Lampix white paper pre-dates the SEC’s enforcement activity in this area. She adds, “The statement that ‘token sales or ICOs are not currently regulated by the U.S. Securities and Exchange Commission may be very literal in the sense that there is not a specific regulation, but the SEC has stated that, in the right situation, ICOs are subject to the US federal securities laws.”

Erin Fonte, an attorney in the Austin, Texas, office of Dykema Cox, and the leader of the firm’s regulatory & compliance group, says, “The ICO stuff is so up-in-the-air. The SEC is looking at it closely. But it’s fairly new. And some of them (ICO’s) have been tied to fraud and Ponzi schemes. If a client came to us (seeking advice), we’d want to vet the people behind the offering.”

But what of Lampix, the company that won the Augmented and Virtual Reality category of the South by Southwest (SXSW) Accelerator Pitch Event earlier this year in March – and put a pretty feather in the cap of Popescu?

Popescu’s resume is no doubt impressive. He holds a trio of master’s degrees in various scientific and technological disciplines, including one from Massachusetts Institute of Technology. And he is a serial entrepreneur who lays claim to having founded 10 companies: they include, according to his LinkedIn profile, online lending, a craft beer brewery, an exotic sports car-rental space, a hedge fund, a peer-reviewed scientific journal, and a venture-debt fund.

He’s charmed journalists like Forbes contributor Roger Aitken, who declared: “The founders (of Lampix)…believe that Lampix will impact humans as much as computers or smart phones in the future…Think Tom Cruise in Minority Report. Imagine your room in five years: you will be able to use any surface around you as if it was a computer. The ability to transform any surface into an interactive computer (augmented reality) is going to unleash applications we have not even conceived of.”

The Lampix website hyped its ICO with the aid of an infographic listing “active product inquiries” the company has in its pipeline, the likes of which includes Amazon, Apple, Samsung, Microsoft, Sony, IBM, BMW, Bloomberg, PwC, and the Aspen Institute. With all of these names seemingly lining up, it begs the question: Why did Lampix choose the controversial route of an ICO to raise capital?

But it’s hard to determine the seriousness of these corporate relationships. Florin Mihoc, Lampix’s Strategic Partnerships & Development Advisor, said he could not assist us with confirming any of them, citing the slow and cumbersome bureaucracy of dealing with Fortune 500 companies. He did invite us to try reaching out to some of them on our own, which we did.

Bloomberg is one of the few acknowledging a relationship with Popescu’s company. Chaim Haas, head of innovative communication at Bloomberg, told AltFinanceDaily that the New York-based media and financial communications company “collaborated” with Lampix. Bloomberg, he says, “has used Lampix hardware in its fellowship program (Bloomberg AR Fellows) as a prototype for augmented reality applications.” But Haas declined to elaborate on whether Bloomberg’s relationship with Lampix was more than an experimental one.

Edward Caldwell, director of public relations for East Coast markets and sectors at Pricewaterhouse Coopers, the Big Four accounting firm, declined to comment about Lampix. “We can’t discuss individual companies, clients or engagements,” he reports.

Douglas Farrar, senior manager for communications and public affairs at the Aspen Institute, told AltFinanceDaily that he could find no business relationship between Aspen and Lampix. “I have gone down quite a few rabbit holes here,” he said in an e-mail, “But I’m coming up empty.”

When Popescu was directly confronted about this, he wrote, “The companies would only figure [in the infographic] if they actually themselves reached out to us and we exchanged emails with somebody from that entity. Most of these entities have many people and most of the companies’ people will have no idea [that] somebody else in the company is talking to us.”

Telephone calls and e-mail requests for comment to Microsoft were not returned.

A spokesperson using BMW of USA’s official twitter account, however, responded to an inquiry by saying they were a customer of Lampix, “but only for office usage.”

Meanwhile, George Popescu has been on the sales trail. A case in point was his October 5, Youtube interview conducted by Ian Balina, a self-described influential investor in blockchain technology and cryptocurrency – and someone with a reputation as an industry promoter and evangelist. (Balina caters to the get-rich quick crowd and publishes how-to guides trumpeting promises like “How ICOs can make you a millionaire in 3 years” and “make millions with bitcoin.”)

Meanwhile, George Popescu has been on the sales trail. A case in point was his October 5, Youtube interview conducted by Ian Balina, a self-described influential investor in blockchain technology and cryptocurrency – and someone with a reputation as an industry promoter and evangelist. (Balina caters to the get-rich quick crowd and publishes how-to guides trumpeting promises like “How ICOs can make you a millionaire in 3 years” and “make millions with bitcoin.”)

Balina asked Popescu the softball question, could he show viewers a demonstration of the product? Popescu admitted he wasn’t prepared to do that and when he attempted to set one up on the fly, it didn’t work. The incident is notable because Lampix has been promoting the video through its social media network.

Popescu corroborates a number of details about the ICO, however. He confirmed the ICO price of a PIX token to be 12 cents, the US dollar price people had to pay per token. Cryptocurrency exchanges, where token speculators can buy and sell tokens online, show the trading value of a PIX token currently hovering around 6 cents, which translates into roughly a 50% loss in value.

Investors feeling hurt by such a loss can’t contest the purchase of PIX tokens with their credit card issuers. That’s because of a requirement that token sales had to be purchased with ether (ETH), the currency of the Ethereum blockchain. While ether is arguably similar to Bitcoin, it operates on an entirely different blockchain.

To participate in the ICO, in a Youtube video, Lampix also explained to purchasers, for example, how they could first buy ether with dollars through an online exchange known as Coinbase** before forwarding the ether to a digital wallet. Next, investors were instructed to send the ether from the digital wallet to a specially designated PIX address. An automated “smart contract” would then release the appropriate amount of tokens to the buyers’ digital wallets 31 days after the ICO was consummated.

It’s a byzantine procedure. And for investors – especially for those who are not exactly tech-savvy – the rigmarole makes it nearly impossible for them to recover their money should they feel buyer’s remorse. Neither the video nor the Lampix white paper mentions any buyer restrictions. Indeed, Lampix’s white paper specifies that “anyone” in the global market can participate. That means that an investor could theoretically be underage or a citizen of Iran or North Korea. (When asked what steps Lampix took with regards to KYC/AML, Popescu said, we “implemented the standard ones with partners specialized in it.”) Investors could even be citizens of the UK where Popescu is banned from being a company director.

And global they are. AltFinanceDaily interviewed Rudy (whose last name we are withholding), a graduate student who lives in Singapore that says he bought approximately $2,200 worth of PIX tokens during the ICO. The drop in value has gotten him so frustrated that he’s contacted securities regulators in the United States to investigate Lampix. Despite the caveat in the white paper that tokens are not an investment and should not be used for investment purposes, Rudy said he considered himself to be an “investor” and that his reason for buying the tokens was to sell them in the future for a profit.

Popescu, who wasn’t asked about Rudy’s experience specifically, told AltFinanceDaily that Lampix is not selling PIX tokens as an investment but rather to primarily build a community. “What people do with the tokens is their choice and we cannot prevent them,” he asserted.

English is not his first language but Rudy said, “I think that [the] SEC should regulate ICOs in the USA. There are no rules currently, teams can promise anything before the ICO and forget everything after the ICO. Things have to change, there should be legal pressure on crypto teams.”

Rudy added that he was “so enchanted” by Lampix’s ideas that he had promised himself not to sell the tokens for at least two years even if they were losing value. He conceded that he was not a tech expert. But, he says, the award at the SXSW competition was an important milepost to him.

AltFinanceDaily found 700 more people interested in Lampix on the company’s official Telegram channel. The chat history since September 20, which we were able to obtain, has been dominated by talk of the PIX token’s trading value. Those bemoaning the low price regularly use the term “investors” to describe themselves – never mind that the white paper specifies that PIX tokens are not supposed to be an investment or to be used for investment purposes.

The chat’s administrator, who uses the nickname Chester, identifies himself as a “community manager” at Lampix. At one point he too refers to PIX holders as investors. “Hey guys,” he wrote in the channel on October 1, “Lampix is a company, not a single person, we don’t do things that quick, but pretty quick and we try not to confuse our investors by telling you unconfirmed news. Be patient, things will be just fine.”

Laura Toma, another community manager for Lampix, responded to complaints about the depressed price in the channel by saying, “The issue is that people want to get rich in a month.”

Indeed, investors hound not only the community managers, but also Popescu himself, who frequently joins in on the chat and fields questions about the trading price of PIX. “You should care more about the company revenue, clients, users.” Popescu replied to one user.

“Are you serious?” a user calling himself Dante fired back. “We are investors, and we care about the return on investment.” Another user with rough English tells Popescu, “As you know, most people come to ICOs for short-term profit. We cannot deny it.”

“Are you serious?” a user calling himself Dante fired back. “We are investors, and we care about the return on investment.” Another user with rough English tells Popescu, “As you know, most people come to ICOs for short-term profit. We cannot deny it.”

Others keep the faith. “PIX will be the real Aladdin’s magic lamp,” writes one user. Another hyperbolically predicts the price will “fly out of the earth, fly to the moon, and finally fly out of the galaxy.”

There is very little discussion about the use of the product itself while numerous inquiries are written in Mandarin. “Lampix has a lot of Chinese investors,” writes one. Other users self-identified as citizens of Russia, Romania, and France. Meanwhile, Toma writes, “Yes, there are investors from USA as well.”

Despite the losses that investors have so far experienced with Lampix, among other concerns, Popescu isn’t limiting himself to just one ICO. According to his online statements, Popescu is connected as an “advisor” to another company engaged in an ICO. AirFox, a Boston-based start-up launched by two Google alumni, provides free data to mobile phone users in return for eyeballing advertising. In early October, Airfox’s ICO raised $15 million. But a month later its AIR tokens, which sold for two cents apiece during the ICO, had lost 75% of their trading value. That means investors in AIR, the company’s ICO ticker symbol (which is becoming an increasingly ironic moniker) have seen more than $11 million go up in smoke almost overnight.

Popescu says in their defense, “The AIR tokens are meant to solve a real problem, of remunerating people who watch ads in exchange of getting more data and minutes on their mobile phone. The ecosystem is still being worked upon, the product is not live. Once the ecosystem is live we will see what really happens. Until then the token is mostly being handled by speculators. The price can therefore vary widely and it doesn’t reflect their true value.”

Even as Lampix and AirFox have been racking up massive losses for investors, Popescu announced on November 5 in a LinkedIn post that he would be involved in five more ICOs.

Among them is DropDeck Technologies, at which Popescu is listed as the chair of the advisor board; its ICO is scheduled for November 21. Another company, Factury, for which he is listed as an advisor, is initiating its ICO on December 15.

He’s an ambitious man.

And his ICO familiarity hasn’t escaped the scrutiny of PIX investors. “I find it strange that you are directing 5 other ICOs,” writes one user in the Telegram chat on November 4. “To make Lampix big, this will require a CEO [who is working] full time working on the project.”

Popescu responds personally. “I am working full time on the project but people have asked me to advise on their ICOs and this grows Lampix’s notoriety a lot in the crypto space,” he writes. He offered further assurances that he wouldn’t be advising those companies’ projects beyond their ICOs.

In an email to AltFinanceDaily, he writes, “I run right now Lending Times, Lampix and Block X Bank only. The ICOs are just customers of Block X Bank. I have built about a dozen companies in 9 years, sold a few, closed a few. Each company has a team to help me, I am not doing this alone. For the ICOs I am more or less involved as an advisor / helping them project-manage their ICOs. How to run 3 companies? It’s about being effective, organized, delegating, partnering and being productive. Oh and I don’t watch TV, so maybe I have a few more hours per day than the average person. I do work long hours.”

Block X Bank, through which Popescu extends his efforts toward other ICOs, is described on the company website as “a boutique investment consulting company specializing in connecting blockchain projects with funding.”

In all of these ICOs, money is seemingly being created out of thin air. A consultant who was hired by AltFinanceDaily to help analyze the technical aspects of both ICOs and smart contracts determined that Lampix raised much more than just the $14.2 million in token sales. In addition to the 114 million PIX tokens sold to investors, our consultant explained, the company also issued 220 million tokens to itself. At the ICO price of 12 cents apiece, those tokens would theoretically be worth $26.4 million – a huge piece of the total ICO pie that Lampix could sell on cryptocurrency exchanges if it wanted to rake in even more money.

There’s a kicker too. At scheduled intervals over the next four years, the smart contract that made PIX tokens possible in the first place is slated to automatically create – and allocate – 330 million new tokens to Lampix. Thus, when Lampix raised $14.2 million in August, the company reserved $66 million worth of PIX tokens for their corporate use.

Popescu said in his e-mail to AltFinanceDaily that these company tokens are for “corporate usage like employee incentives, M&A, other company investments…etc.”

It’s a mind-boggling sum of money for the development of a futuristic lamp whose followers mostly seem to reside on internet chats like Telegram, reddit, and bitcointalk.org.

And this has occurred despite the company’s withholding any information regarding Popescu’s status in the UK. Balina, who interviewed Popescu on Youtube, told AltFinanceDaily he wished he had known about his disqualification in the UK. “This is definitely a big issue and I wish I would have known about it so that either my audience or I could have asked him this directly on the live stream,” he said.

AltFinanceDaily asked Paul Savchuk, Co-founder, CEO, and Chief Product Officer at Cryptocurrency Capital LLC, a US-based hedge fund that only invests in utility tokens as commodities, if Popescu’s ban in the UK would have been relevant information in the Lampix ICO. “Yes, that might be a red flag for us in some cases and require us to perform additional research,” he wrote in an emailed response. “We look at management very seriously – especially since a lot of projects are treated like startups and management is a key component to whether or not many of these ICOs can make it. We try to find such events and spot red flags whenever we conduct our due diligence research on ICOs. The reason: each project has something that needs to be improved. ‘Red flag’ – sometimes conversely can lead to a great opportunity when other market participants ignored it or were too skeptical.”

Mr. Savchuk further said, “Lampix is a perfect example of a coin that on the surface looks very promising, but when you dig a little deeper, you do find red flags that can dampen the excitement for this investment.”

And yet Savchuk spoke rather positively of the Lampix product after reading their white paper. “We believe the project is looking to change the current AR/VR tech industry,” he said, referring to augmented reality/virtual reality. “The project is promising for two reasons. First, they have multiple companies in their pipeline. Second, they have a legitimate product which they will manufacture and sell. They are one of the few blockchain products to offer a tangible product with the ability to disrupt the market.”

“Third,” he went on, “most companies have gaps in building a strong structure at the outset of their existence. Some have bugs in initial code that cause breaches in cybersecurity. Others release product with a low level of usability – the ones who are aware of such problems have a greater chance of success. We would prefer to see publicly known strengths and weaknesses of such companies. Management has to be transparent about their team and product no matter what. Whenever possible, we want to be in touch with the management team.”

“Third,” he went on, “most companies have gaps in building a strong structure at the outset of their existence. Some have bugs in initial code that cause breaches in cybersecurity. Others release product with a low level of usability – the ones who are aware of such problems have a greater chance of success. We would prefer to see publicly known strengths and weaknesses of such companies. Management has to be transparent about their team and product no matter what. Whenever possible, we want to be in touch with the management team.”

With regard to the price drop, Savchuk said, “This is a danger for all purchasers of ICOs. Sometimes it’s caused by token purchasers (swayed by) fear and greed and (hoping for) easy money and fast money. I doubt somebody sold Apple Inc.’s stock right after its IPO. It is also very difficult to restrict exchanges from allowing massive pump and dumps. That’s not even mentioning the difficulty of measuring the value of tokens,” Savchuk concluded. “Consequently, such projects are struggling with low credibility. However, it also creates a possibility for those who believe in the idea and product on a long-term run.”

Popescu downplays the significance of the UK issue. The root of the debacle, he says, is the result of Boston Prime – the company he previously ran – being forced into bankruptcy by the actions of a company he is now suing called FXDD. “FXDD bought the companies and then bankrupted them and that’s why Boston Prime [went bankrupt],” he writes. “Myself personally and each company separately are suing FXDD for this. UK has archaic laws where if you are a director of a bankrupted company you get disqualified from being a director again for a time. Attorneys charge about 40,000 GBP to defend this automatic case and I weighed the pros and cons and decided to ignore it as I have no plans to be a director in the UK for time being.”

Investors unhappy with underperforming ICOs may be willing to challenge their legality. On October 25, for example, a class action lawsuit was filed against Tezos, a computer networking project that raised $232 million in one of the largest ICOs ever. In a complaint, the lead plaintiff alleges that, among other things, Tezos unlawfully engaged in the unregistered offer and sale of securities and fraud in the offer or sale of securities. “In July 2017, Defendants conducted an ICO in which they sold 607,489,040.89 tokens (dubbed ‘Tezzies’ or ‘XTZ’) in exchange for digital currency worth approximately $232 million at the time,” the complaint reads. The plaintiff, who purchased 5,000 Tezzies, feels he was misled about the company and the offering.

Internal squabbling at Tezos which has delayed the release of its product and the sheer amount of money at stake have put the company on the map with the mainstream media and business press. The New York Times, Wall Street Journal, and Fortune as well as news services Reuters and Bloomberg have all covered the allegations of fraud.

The day before the class action lawsuit was filed, moreover, a AltFinanceDaily reporter attended an explosive session at Money2020 in Las Vegas that saw Tezos co-founders, Arthur and Kathleen Breitman, attempting to give a status report of the company. A crowd that had gathered outside prior to the doors opening had attendees speculating whether the Breitmans “would actually show their faces” in the midst of all the drama.

To date, no lawsuits have been filed against Lampix despite the drop in the token’s value.

At a cryptocurrency/ICO meetup in NYC in October, a AltFinanceDaily reporter met with executives at one company preparing an ICO who said they would not allow American investors to participate because of securities-enforcement fears. Pressure is mounting in the Far East as well. Citing their illegality, Chinese regulators in September issued a blanket cease-and-desist order on all ICOs in their country. What that means for Lampix’s Chinese investors bears watching.

Popescu says that Lampix supports regulation in China. “Of course, all Chinese people have to follow Chinese regulation,” he writes.

Meanwhile, on the product front, Popescu says that right now a Lampix lamp can be purchased for $10,000, a tidy sum because they must be hand-made. “We plan to improve the manufacturing costs and then we’re planning to do a kickstarter early next year for around $500 [per] Lampix,” Popescu told AltFinanceDaily in his e-mail interview.

But for investors, it always comes back to the trading value of PIX. On October 25, one investor asks Popescu if the company will buy back its own PIX tokens at the ICO price to pump up their market price. “If you want a pump and dump please go to other companies,” Popescu responds. “We are here for 5-10 years to build a $100 billion dollar company and compete with Apple.”

And it all began with an ICO.

“ICOs also help with bootstrapping the user base – breaking the chicken and egg problem,” Popescu also explains in his e-mail to AltFinanceDaily. “In addition, given that Lampix is looking to crowdsource images, we prefer many different people hold PIX tokens rather than 2-3 VC funds. And last but not least I think tokens are better rewards for the community (liquid, mark to market, etc.) than illiquid instruments.”

Not everyone agrees that PIX is the most liquid instrument to grow the community. US Dollars come to mind, for example. “Let’s say I’m a customer,” one investor poses to Chester, a Lampix community manager. “I want to use the cloud computing service but then I see I have to pay with PIX. I have no experience in crypto and have no idea how to do that. I just want to use your service fast and don’t want to buy PIX coins first before I can make use of it. Will there be a fiat option?”

Chester is awed by the idea. “Well, you are so professional,” he writes. “Man, you are good. You are good, the question you threw just hit the spot seriously. I guess there is always something Lampix needs to figure out and choose the best solution. Technically speaking they are jolly good at this point, but it doesn’t mean it’s perfect.”

Chester, who assures him that he isn’t being sarcastic, goes on to refer to the investor who asked that fairly elementary question as a “big shark” that is “born to bite.”

It remains to be seen if the PIX “user base” shares the same philosophy as Lampix. Ian Balina, who interviewed Popescu on Youtube, separately asked his social media followers: “What’s the first thing you’re going to do once you hit your goals in cryptos?”

It remains to be seen if the PIX “user base” shares the same philosophy as Lampix. Ian Balina, who interviewed Popescu on Youtube, separately asked his social media followers: “What’s the first thing you’re going to do once you hit your goals in cryptos?”

The responses fly in:

“Buying my Lambo”

“Travel to Paris”

“Buy an island”

“Buy my mum her dream home”

“Quit my job and start up something for me”

“Pay off mortgage and be financially free”

“Buy house in Miami, buy Lambo, enjoy life”

“Retire”

“Easy. Buy more crypto”

Meanwhile on Telegram, where investors continue to engage Lampix management on a daily basis, Dante offers a sobering reminder of what they’ve bought into, “We don’t have equity, we only have tokens,” he writes. “And we are taking a big risk.”

* The amount of tokens sold multiplied by the 12 cent ICO price doesn’t exactly match the dollar amount Lampix says they had raised. That’s because Lampix not only issued bonus tokens to buyers at each stage of their ICO but also because the market value of ether, which users had to convert to from dollars to buy PIX, had fluctuated when they reported how much they raised. Like Bitcoin, the value of ether is volatile.

** The smart contract Lampix wrote to launch Lampix’s tokens into existence specifically named them PIX tokens and dubbed their publicly identifiable symbol to be PIX.

*** Coinbase is a respected digital currency wallet platform based in San Francisco.

Prosper Loan Linked to Terror – A Preliminary Assessment

December 9, 2015By now you have probably heard that one of the San Bernardino terrorists received a $28,500 deposit from WebBank.com two weeks prior to committing the attack. After Fox News broke that story, I may have been the first to publicly connect it to an alternative lender which was later revealed to be marketplace lender Prosper about 12 hours later.

As a Prosper investor myself, here are some things you should know:

The $28,500 deposit (if that was the exact true amount) would have been net of the origination fees. In all likelihood this was a loan for around $30,000 and the borrower only netted $28,500.

Those that have speculated that it would be impossible for someone making $53,000 a year (as Syed Farook did) to qualify for an unsecured loan of this amount are wrong. There are loans on the platform right now that fit these parameters. Online Lenders like Prosper and Lending Club are pretty aggressive with their lending.

The notion that Prosper somehow could’ve detected what the borrower planned to do two weeks later just isn’t possible. In lending, this is known as the asshole factor, meaning that even if the applicant meets all the criteria, they could just decide to be an asshole, and there’s no way to predict that.

There are strict laws in place to prevent all kinds of discrimination, meaning that even if Prosper had formed some kind of suspicion about the borrower, it may have been illegal to act on that suspicion. Such is the hypocritical paradigm of fair lending where factors that are measurable predictors of negative performance (or worse) cannot be legally used. Federal laws have purposely tried to create an environment where lenders make decisions on an objective basis they consider to be fair. In business lending for example, there is a law within Dodd-Frank that has not been implemented yet, but seeks to prevent loan officers from knowing the gender or even the name of the prospective borrower to protect them from subconscious discrimination.

Investigators have publicly announced that the terrorists were not on any watch lists and therefore there are no systems or checks that Prosper could’ve plugged into to have gotten the information.

Prosper and other alternative lenders already have Anti-Money Laundering Policies. I know this because I complained about Lending Club’s over a year ago.

The Wall Street Journal stated, “Only some nonbank financial institutions, such as mortgage lenders, are subject to Treasury rules requiring lenders to report suspicious activity to the government under the Financial Crimes Enforcement Network.” Maybe that’s true, but there is nothing suspicious about someone applying for a loan online who is not on any watch lists. I can’t think of anything that could’ve been suspicious unless they submitted fake pay stubs or forged documents.

“There’s no due diligence that’s done into how these loans are actually going to be used,” said Brian Korn, a partner at the law firm Manatt, Phelps & Phillips, LLP in the WSJ. This is true and at the same time related to anti-discrimination laws. Judging a loan applicant by their detailed monetary plans could potentially induce gender or ethnicity bias, even if subconscious.

There will be plenty of questions in the coming days from Americans, the media, and government officials about what alternative lenders are doing to make sure they’re not funding terrorists. Part of what they may learn is that for all the data that alternative lenders have at their disposal to make intelligent decisions on an automated basis, some of them cannot be legally used. They’ll also find out that there’s only so much that predictive analytics can actually predict.

It’s very unlikely that Prosper could’ve handled anything differently…

Tech-based Lenders Clobbered On Dose of Bad Economic News

June 29, 2015How would tech-based lenders fare in a slumping market? Not very well apparently…

OnDeck (ONDK) and Lending Club (LC) set new record lows earlier today amid bad news coming out of Greece and Puerto Rico. OnDeck is down almost 43% from its IPO price and down 61% from its all time high. It was down more than 8% today even though the Dow was only down 2%.

$ONDK was unaware that it focused on Greek loans…. interesting 8.6% drop.

— Mark Holder (@StoneFoxCapital) Jun. 29 at 05:48 PM

The downward trend was dissected in a post that was published just hours before today’s further fall.

Meanwhile Lending Club is in new territory, down 3% from its IPO price and down 50% from its high. So what are investors saying about this?

$LC hmm i really dunno what to say about this…

— mike pham (@mincogneto) Jun. 29 at 05:30 PM

That’s kind of the overall gut feeling. Many feel this company is being unfairly dragged down and yet it continues to fall. A mounting campaign by the Puerto Rican government to declare bankruptcy and a Greek debt disaster clobbered everything today including Lending Club. One tweeter came up with a great idea last week, bail out Greece with a loan from Lending Club…

If all else fails with the IMF #Greece should just apply on @LendingClub pic.twitter.com/RbtnMm5JaO

— World First USA (@WorldFirstUS) June 22, 2015

Last week no one was even talking about Puerto Rico. Now all of the sudden they’re in a “death spiral.”

Watch the death spiral coverage on CNN

The market’s tech lending darlings might’ve gotten pummeled like everyone else but the ease with which they drop should probably be a warning sign. Neither offshore dilemma stands to have any impact on their businesses. So what would happen if a relevant issue were to arise such as a domestic disaster, a sudden rise in unemployment, a recession, a financial crisis, skyrocketing fuel prices, a steep increase in the fed funds rate, or even something no one dares talk about like a legal ruling that could jeopardize the entire bank charter model?

It’s quite possible that both companies haven’t bottomed out just yet….

——–

Note: I have no equity positions in either company. I do own Lending Club notes however.

Mayor Rahm Emanuel Declares War on Merchant Cash Advance

January 16, 2015 FOX 32 in Chicago is reporting that Mayor Rahm Emanuel is going on the offensive against merchant cash advance companies. Specifically it says,

FOX 32 in Chicago is reporting that Mayor Rahm Emanuel is going on the offensive against merchant cash advance companies. Specifically it says,

Mayor Rahm Emanuel will call on state and federal agencies to regulate business to business lenders. Emanuel said cash advance companies have accelerated their marketing efforts in recent months, resulting in small businesses taking loans they cannot afford.

The article states that business owners have turned to the City of Chicago for help in paying back loans with high rates of interest.

While the mention of APRs reaching into the ranges of triple digits is supposed to shock you, one business lender that charges such rates recently went public and had been backed by Google Ventures, Fortress Investment Group, Goldman Sachs, and Peter Thiel.

Less than 30 days ago we were celebrating these companies as the solution to a problem that has plagued small businesses for all time, access to capital.

While Emanuel is obviously famous for being the 23rd White House Chief of Staff and Obama’s right hand man for a period in his first term, he is not the first mayor to consider the role merchant cash advance companies and high interest business lenders have in cities across America.

All the way back in 2008, the U.S. Conference of Mayors (USCM) adopted a resolution titled, Protecting Main Street Small Business Owners from Predatory Lenders, from which some of the excerpts below are from:

WHEREAS, merchant cash advance companies have already lent approximately $2 billion at egregious rates and have been quoted in leading main stream media publications such as Forbes, Business Week, Dallas Morning News, and American Banker claiming that their new originations have increased 75% in the first half of 2008

WHEREAS, as with payday lenders and predatory lenders in the home mortgage community, Mayors need to take a leadership role to scrutinize predatory merchant cash advance companies, educate small business owners of the dangers posed by these firms, and increase awareness and promotion of alternative, more affordable funding sources to support this vital segment of our economy

BE IT FURTHER RESOLVED, that to protect the general health and viability of their small business communities, cities should investigate whether they can effectively regulate or ban merchant cash advances.

3 months after this resolution was passed, Lehman Brother’s collapsed and the economic crisis was in full swing.

According to a few industry leaders familiar with the 2008 mayoral resolution, UCSM privately retreated from their stance when all other types of commercial lending had dried up. Their seeming reversal, though not publicly stated invited merchant cash advance companies into their communities at the moment when Main Street was arguably at its weakest.

According to a few industry leaders familiar with the 2008 mayoral resolution, UCSM privately retreated from their stance when all other types of commercial lending had dried up. Their seeming reversal, though not publicly stated invited merchant cash advance companies into their communities at the moment when Main Street was arguably at its weakest.

Who do they think rolled up their sleeves and kept local economies alive when things were at their worst?

While non-bank funding can obviously be expensive, countless business owners have praised merchant cash advances in particular as a solution that came through when none other were available.

Emanuel will learn that companies such as Square and PayPal are part of the crowd that provides merchant cash advances. This is not a shadow industry. Non-bank business-to-business financing is already becoming less expensive nationwide.

According to Fox, the Commissioner of the Chicago Department of Business Affairs and Consumer Protection said the goal is to offer small business owners loans at affordable rates with full disclosure.

Merchant cash advance companies would undoubtedly feel the same way. The dilemma is that advocates of affordable rates tend to really mean single digit rates. When single digit rates are not possible given the risk, they seem to argue that no financing should be given at all, leaving the business to fail or miss out on an opportunity. That’s the exact type of flawed thinking alternative financing companies address…

Ironically, a report from the Federal Reserve Bank of Cleveland last week concludes that small business job creation is lagging with a possible culprit being a lack of access to credit.

Coming out of the most recent recession, however, job creation by small businesses has lagged, and the new business formation rate continues to fall. While it is not clear that these trends are driven by weaker borrowing or limited access to loans, it is evident that businesses need adequate credit to succeed and grow. As such, policy makers should not lose sight of the trends related to small business credit, even with the recent positive reports showing improvements.

And of course in a supposed exposé on merchant cash advances that aired on Chicago Public Radio in November, clips of an interview I did with them were aired to fit the narrative of merchant cash advance as predatory. When asked by the interviewer what a small business owner should do if they didn’t understand a contract, I advised that they hire an attorney or an accountant, and if they couldn’t afford those then to find somebody they felt qualified to offer an opinion. “They should always get a 2nd set of eyes to review a contract if they don’t understand,” I said.

My advice did not air, nor did my explanation that there were two separate types of products that they were confusing as one, one being loans and the other being purchases of future receivables. I suppose it didn’t fit the characterization they were going for.

As quoted in Fox, Financial Advisor Kent Travis advised business owners to “read the documents, don’t sign anything on the spot, make sure you read it thoroughly and if you have trouble understanding it seek the advice of an advisor, CPA, an attorney or a financial planner.”

I couldn’t have said it better myself because I already did.

And in an interview I had with former Congressman Barney Frank, a chief architect of the Dodd-Frank Wall Street Reform and Consumer Protection Act, Frank voiced his opposition to regulations on business-to-business lending in early 2014.

There’s one thing the Fox story does mention that’s hard to argue with and that’s the need for greater transparency. I am all in favor of that.

—————–

For those that haven’t already signed up, this is a reminder that the Law Office of Pepper Hamilton LP is hosting a lunch at their office in New York on January 27th to specifically discuss the merchant cash advance industry’s future.

Interested in discussing legal issues, best practices, and the path forward for alternative business financing? Are you an ISO or funder interested in sharing your thoughts? Send me an email to let me you know if you’d like to attend. sean@debanked.com.

—-

Watch the Fox news report about merchant cash advances:

Industry Takes ALS Ice Bucket Challenge

August 24, 2014Have you been nominated to take the ALS ice bucket challenge yet?

Kabbage below:

Their video made the local Atlanta news.

OnDeck in Times Square NYC:

Noah Breslow, their CEO also did it:

Funding Circle:

PayPal

Coincidentally, in the industry’s 2012 fantasy football competition for charity, league winner Sure Payment Solutions chose to donate all funds raises ($7,100) to the ALS Association.

Whether you get nominated or not, you can donate at http://www.alsa.org/.

Feel free to tweet @financeguy74 if you or your company accepted the challenge. 🙂