Q & A with Ryan McCurry of ACHWorks About the Future of Small Business Lending

February 22, 2022 In a recent chat, AltFinanceDaily talked with Ryan McCurry, President of ACHWorks. McCurry discussed the future of his company, payments, small business financing, and the impact of digital assets on the industry.

In a recent chat, AltFinanceDaily talked with Ryan McCurry, President of ACHWorks. McCurry discussed the future of his company, payments, small business financing, and the impact of digital assets on the industry.

Q (Adam Zaki): Your company recently announced an acquisiton. How does this move help take ACHWorks to where the company wants to go?

A (Ryan McCurry): We are excited to share that ACHWorks was acquired by VeriCheck Inc. on December 31, 2021. VeriCheck Inc. (VCI) is a wholly owned subsidiary of Commercial Bank of California (CBC), who has been one of ACHWorks’ sponsor banks for nearly 20 years.

The acquisition brings more resources, both in terms of staffing and capital to ACHWorks’ business efforts. Conversely, ACHWorks’ sales approach, market specializations and diverse technical capabilities will support VCI’s growth goals. By combining the teams and technology, we believe we will compound our benefits to reach an even higher level of success together.

The great news with this acquisition is that where ACHWorks was weak, VCI is strong. Likewise, ACHWorks has some unique technology and expertise that VCI hadn’t leveraged before and can now capitalize upon.

Furthermore, VCI relies heavily on partnerships with ISO’s and third party gateways for processing ACH payments with a high number of merchants across all sectors, whereas ACHWorks tends to specialize in a few verticals while maintaining direct sales and direct relationships with all merchants – even when the merchant is utilizing an integrated software partner.

Q: Are ACH payments here to stay? With so many ideas floating around in this space, what is the future of ACH?

A: The future of the ACH as a payment system is strong and growing quickly. In 2021, the ACH network grew by 29.1 billion payments valued at $72.6 trillion dollars. Same Day ACH grew by 74% over 2020 and total volume was up almost 9%, continuing a 7-year growth trend. Business-to-business ACH payments grew at a rate above 20% and 33% over the last two years, respectively.

We believe the ACH payments space is going to continue to grow and become a more widely used payment rail, and our acquisition is evidence of that growth.

Q: What is the biggest issue your company is currently overcoming?

A: There are always challenges facing the payments industry. Naturally, as a fintech industry, payments companies regularly face emerging technology, regulatory or legislative activity, and ongoing cybercrime.

Currently, our focus is blending the VCI and ACHWorks teams and evolution of our joint technology. We are pleased to share that VCI hired the entire ACHWorks operational team, and is retaining all of our existing technology and benefits to our clients. Bringing the two platforms and teams together will have exponential benefits for clients and partners moving forward.

Q: The small business financing industry is becoming less reliant on the traditional sales models. How will ACHWorks combat this? Will you help the funders/brokers innovate to help secure the current infrastructure or seek new tech clients that are stepping into the space?

A: There’s the old saying that change is the one constant. Initially, business finance companies only wanted ACH for reoccurring daily debits, and as merchant demographics changed weekly or custom payment frequencies have become more prevalent. However, now about half of our business finance clients use ACHWorks’ technology not just for debiting merchant receivables, but also for sending ACH Credits to merchants for funding a deal, automating syndication payments for participation rates or paying commissions to brokers.

Likewise, ACHWorks offered Same Day ACH capability to our clients on the first day it become available on the ACH Network. The use of Same Day ACH has been slowly increasing as funders utilize it both to fund merchants or to act on a merchants request to charge them today (most common on distressed accounts).

As the funder / broker relationship continues to evolve, ACHWorks will be there to help facilitate the movement of the funds. We hope to leverage our unique status of being owned by a bank to bring new technologies to the business finance industry and other spaces that are under-supported by traditional payment processors. We are excited for these new capabilities to come and will keep the AltFinanceDaily community updated as we have more to share.

Q: There seems to be a lot of payments companies across fintech. The elephant in the room at Money 20/20 in October was the ‘payments bubble’ taking place. What is your take on this? Is fintech looking too much into payment processing innovation?

A: Automobiles have been around for about 140 years, and yet innovation continues to happen. They have seen the switch from steam to electric, to internal combustion and back to electric. Computer technology has only been common in business usage since the 50’s and the internet has only been heavily used since the late 90’s. When I started in this business, we used to mail our software to clients on a series of 14 floppy disks. I would argue that the innovation and evolution of payments and fintech is only in its infancy.

As technology continues to permeate all walks of life, we expect to see payments leveraged to make commerce more organic with far less friction. Most payment processors I speak with feel that we are the original “fintech” and that the newly emerging “fintech” market is just utilizing the infrastructure we put in place.

Q: Are cryptocurrencies a topic of conversation in your office? Blockchain tech offers major benefits in the payments world. Do you or your company have any thoughts on how this could be leveraged?

A: You can’t escape crypto, it invades all conversations these days. However, our focus is on working with fiat currency and regulated payment channels because we process ACH payments through the Federal Reserve utilizing State or Nationally chartered banks. Don Singer, the CEO of VCI and I were discussing this topic previously, and he told me crypto is the new shiny sports car, or personal aircraft, but we work on the rail road. ACH is not as sexy as crypto, but it moves nearly all of the money in the U.S. Those debit card, credit card, Venmo, Zelle and real time payments systems are just the messaging systems, the money is being moved later that day, and it’s being moved via ACH.

FDIC Chair Says Community Banks are the Backbone of SMB Lending

February 4, 2022 In a Bipartisan Policy Center forum, outgoing FDIC Chairperson Jelena McWilliams spoke on the future of small business lending post-pandemic. According to her, the future of the industry isn’t in brokering different types of products, but rather merchants relying on community banks to develop and provide interpersonal relationships with businesses who are seeking access to capital.

In a Bipartisan Policy Center forum, outgoing FDIC Chairperson Jelena McWilliams spoke on the future of small business lending post-pandemic. According to her, the future of the industry isn’t in brokering different types of products, but rather merchants relying on community banks to develop and provide interpersonal relationships with businesses who are seeking access to capital.

“Small business lending, which is especially important to community banks, will continue to grow,” said McWilliams. “We monitor these developments through our call report data, and we report it on a quarterly basis. Community banks are a real player in the small business lending space. They are a key resource to small businesses needing credit, they are in a niche area. In most cases, they are more successful lending to small businesses than larger banks.”

McWilliams referenced a study that was published by the FDIC in 2020 dubbed the ‘FDIC Community Banking Study’ that found community banks were playing a much larger role in small business lending than larger banks. According to the study that McWilliams referenced, 36% of small business loans are written by community banks; more than double their share of the industry’s total loan products, which is around 15%.

It seems to show that the belief of regulators is that smaller banks can leverage their size to put a face to the loan. Speaking about fintech and its impact on the lending space, McWilliams stressed that a well-rounded financial product has to have a face to it.

“That personal touch community banks bring to the table is what allows them to be really good in this space, and to actually expand relationships between banks and borrowers. So I think that small business lending today I think they are in a very good place.”

McWilliams concluded her comments on the state of small business lending in a reflection of the overall economy, drawing a connection between the financial health of small businesses and the overall economy post-pandemic.

“Of course, you can never have enough credit or capital to have a vibrant economy and more is better as long as its safe and sound and underwritten well, but I would say that for all the concerns we had at the beginning of the pandemic with so many small businesses not being able to survive and shutting their doors down, we are actually on a really good trajectory in small business lending at this point in time.”

How Hot Is The Legal Cannabis Industry?

February 24, 2020 One gauge of the commercial excitement over legal weed, medical marijuana and cannabis’s byproducts could be witnessed at the Las Vegas Convention Center in early December where the Marijuana Business Conference & Expo was overflowing with 31,523 attendees.

One gauge of the commercial excitement over legal weed, medical marijuana and cannabis’s byproducts could be witnessed at the Las Vegas Convention Center in early December where the Marijuana Business Conference & Expo was overflowing with 31,523 attendees.

Appealing to that audience—roughly the population of Juneau, Alaska—were more than 1,300 exhibitors who hailed from 79 different countries and touted products and services as varied as advancements in crop cultivation, medicinal breakthroughs, and innovative consumer products like marijuana-laden pastry.

Appealing to that audience—roughly the population of Juneau, Alaska—were more than 1,300 exhibitors who hailed from 79 different countries and touted products and services as varied as advancements in crop cultivation, medicinal breakthroughs, and innovative consumer products like marijuana-laden pastry.

That’s some 30% more than the 1,000 vendors who packed into the Central Hall in 2018 and about double the 678 who were showing off their wares in the smaller North Hall two years ago, reports Chris Day, vice president for external relations at Denver-based Marijuana Business Daily, which follows the cannabis industry and sponsored the Las Vegas trade show.

“In December, 2019,” Day declares, “we did not have to turn people away because we expanded. We had enough room for exhibitors but we needed both halls.” Unable to resist a boast, he adds: “We’ve been the fastest-growing trade show in the country three years running.”

One face in the December crowd was seasoned financial broker Scott Jordan, the Denver-based managing director of the Alternative Finance Network. He was occupying a booth accompanied by two attractive female models in fetching T-shirts emblazoned with the message: “How much would you borrow at zero percent?”

The young ladies’ arresting appearance and the message worked to the extent that “it got people talking,” Jordan says. As for the zero-interest rate, it’s not exactly free money. “I’ve got a product that puts together a line of credit,” he explains, “and after they receive the line of credit, it charges them a fee.”

As a broker, Jordan does the spade work of poring through a cannabis business’s financial statements and business model before he tees up a deal—typically between $250,000 and $750,000—to “a cadre” of 35 lenders in 10 states. He’ll ascertain whether the best funding option should be structured as equipment leasing, a working-capital loan, a revolving line of credit, project financing, or a real estate loan.

One recent cannabis deal that Jordan midwifed involved a “post-revenue, pre-profitability” manufacturing and processing company headquartered in Colorado. The financing, which closed in April, 2019, involved a pair of four-year term loans: one for $400,000 to refinance existing machinery, and a second for an additional $500,000 to acquire new laboratory equipment. Both credits carried interest rates in the “mid-teens,” he says, and were secured by the equipment.

Once the debt financing was in place, the manufacturing operation was “fully functioning,” Jordan reports, paving the way for the company to raise $30 million in venture capital financing. Jordan argues that “even if they pay a 10-20 percent interest rate, it’s better to preserve equity and finance through a normal type of loan. If you need an extraction machine or packaging equipment,” he adds, “why give up equity if you can finance it through debt?”

Jordan’s reasoning appears to sit well with clients and funders alike. Since 2014, he has brokered 85 transactions worth $33 million. He reckons that two out of three deals that he takes to funders meet with success. “My best year was 2015 because there were only a few competitors and I was the only guy on the block,” he says.

As the country steadily decriminalizes and legalizes pot, however, early market entrants like Jordan no longer have the cannabis business all to themselves. Thirteen states have legalized recreational marijuana for adults. These include California, Colorado, Oregon, Washington and Nevada in the West; Illinois and Michigan in the Midwest; and Massachusetts, Vermont and Maine in the East. Hawaii and Alaska permit it and, if you’re over 21, you can legally grow, smoke or ingest weed in the District of Columbia, but it cannot be sold commercially.

An additional 24 states have approved medical marijuana. While research on cannabis’s medicinal properties remains thin—largely because of objections by federal law enforcement—it is being prescribed for a range of maladies, including cancer, glaucoma, epilepsy, Crohn’s Disease, multiple sclerosis, nausea, and pain. [“The marijuana plant contains more than 100 different chemicals called cannabinoids,” according to WebMD. “Each one has a different effect on the body. Delta-9- tetrahydrocannabinol (THC) and cannabidiol (CBD) are the main chemicals used in medicine. THC also produces the ‘high’ people feel when they smoke marijuana or eat foods containing it.”]

Industry data assembled by MJBizDaily reflects both the broad acceptance of legal cannabis use and its increasing commercial popularity. U.S. revenues from legal weed and its byproducts are expected to clear $16.4 billion this year, a 40% growth rate over the $11.75 billion in estimated revenues for 2019. The legal cannabis industry now employs about 200,000 persons in the U.S., about the same number as flight attendants (120,000) and veterinarians (80,00) combined.

For more evidence that the cannabis market is hot look no further than the state of Illinois, where recreational marijuana went on sale Jan. 1, 2020. The Prairie State’s governor also pardoned some 11,000 citizens with criminal records for possession and the sale of low levels of marijuana.

For more evidence that the cannabis market is hot look no further than the state of Illinois, where recreational marijuana went on sale Jan. 1, 2020. The Prairie State’s governor also pardoned some 11,000 citizens with criminal records for possession and the sale of low levels of marijuana.

“We’re showing that sales were close to $3.2 million on the first day of 2020,” says MJBiz’s Day. “Illinois is the big story right now,” he adds. “Anytime a new state opens up in the market, you’re seeing enormous pent-up demand and enthusiasm.”

Even as the cannabis industry takes giant strides toward public acceptance, the plant continues to face hostility from the U.S. federal government, which has criminalized its use for 80 years. Marijuana remains classified by the Drug Enforcement Agency as a Schedule 1 drug, keeping company with heroin, LSD and Ecstasy.

Even as the cannabis industry takes giant strides toward public acceptance, the plant continues to face hostility from the U.S. federal government, which has criminalized its use for 80 years. Marijuana remains classified by the Drug Enforcement Agency as a Schedule 1 drug, keeping company with heroin, LSD and Ecstasy.

That designation has also made it hard for the cannabis industry to engage in simple financial transactions, much less obtain financing. “Despite the majority of states’ having adopted cannabis regimes of some kind, federal law prevents banks from banking cannabis businesses,” Joanne Sherwood, president and chief executive at Citywide Banks, a $2.3 billion-asset bank headquartered in Denver, testified to Congress last summer. “The Controlled Substances Act,” added Sherwood, who is chair of the Colorado Bankers Association, “classifies cannabis as an illegal drug and prohibits its use for any purpose. For banks, that means that any person or business that derives revenue from a cannabis firm is violating federal law and consequently putting their own access to banking services at risk.”

And despite the herculean efforts by the cannabis industry to soften its image, obtaining financing from traditional sources like pension funds, insurance companies and university endowments remains a daunting proposition as well, says David Traylor, senior managing director at Golden Eagle Partners. His four-person, boutique investment fund, which makes equity investments in up-and-coming cannabis companies, relies on wealthy individuals and family offices for the bulk of its funds.

“Capital is hard to come by for this industry,” Traylor says. “From day one, most venture capitalists have been staying out of it. It’s still illegal in many states and their limited partners are endowments like Harvard and Yale, which see marijuana as the antithesis of education.”

Sarah Sanger, chief financial officer at Oak Investment Funds, a real estate investment firm based in Oakland, says: “There’s a great deal of economic activity in California but it’s stymied by the lack of financing and difficulty with changing regulations. It provides an opportunity for really expensive debt from private investors willing to do due diligence.”

That absence of establishment financing has opened up a plethora of opportunities for alternative funders, and not just in agriculture and plant cultivation. While agriculture represents the bedrock of the industry there is no downstream product, of course, without the cannabis leaf— growing and harvesting cannabis is just one stage of the industry’s life cycle.

MJBiz’s Day notes, for example, that that the legal cannabis industry is regulated for safety, so growers must show that “the flower has no molds or contaminants.” That means that crops are subject to rigorous testing and decontamination, which requires both materials and expertise. To process the leaf and develop “infused products” by extracting cannabis-based oils entails the purchase and deployment of costly technology. Packaging and labeling along with tracking systems that, Day says, “are stricter than in other places” are also key components of the farm-to-market supply chain.

Meanwhile, in an ongoing effort to appeal to a fresh cohort of customers, Jordan notes, the cannabis industry continues to develop innovative uses for the plant. “There are so many applications and new products that keep appearing, like ice cream with marijuana, vaporizers, inhalers, and syrup,” he says. “Now, there are mints—something I hadn’t seen before—and different ways to ingest the product and get high and not look like a druggie.”

Jordan Fein, chief executive at Greenbox Capital in Miami, says his firm prefers to fund downstream companies selling cannabis products. “We do agricultural lending but it’s less attractive and harder to qualify the business. It’s not as tangible as a retail business which will have a website and product reviews. The same goes for edibles.”

Jordan Fein, chief executive at Greenbox Capital in Miami, says his firm prefers to fund downstream companies selling cannabis products. “We do agricultural lending but it’s less attractive and harder to qualify the business. It’s not as tangible as a retail business which will have a website and product reviews. The same goes for edibles.”

Recent Greenbox Capital deals in 2019, Fein says, included one with merchant cash advances of $80,000 and $60,000 in growth capital to a Colorado dispensary. The operation put the money to work adding two retail outlets during the year, he says, bringing to four its total number of storefronts. In addition to cannabis flower, the dispensary sells “edibles, tinctures, lotions, and wax concentrates,” Fein reports. Both short term cash advances require regular ACH payments.

Greenbox Capital also made a $135,000 cash advance to a cannabis-testing laboratory in Southern California in August, 2019 for the purchase of sophisticated equipment. The company, he says, is doing $140,000-a-month in revenue and cashflow is strong and on the rise.

“Greenbox is always interested in higher risk deals,” Fein says, noting that banking services remain off limits to legal cannabis firms. “But we fund them for the same reason we fund lawyers and auto sales—things that most others will not do. There’s nothing wrong with risk,” he adds, “as long as you clearly assign a proper value to the deal and price to it.”

Steve Sheinbaum, a New York broker and chief executive at Circadian Funding, has unabashedly climbed aboard the cannabis bandwagon. “The market is exploding and it’s attractive to lenders because it’s a product people can put their hands on,” he says. “If I’m dealing with a grower, I can leverage real estate and usually there’s equipment. If they’re producing, there’s inventory and I can look at the income statement to see what kind of cash flow the business is generating.”

He recently brokered a $10 million loan for a licensed grower and distributor of medicinal marijuana in New England with monthly revenues of $3-$4 million. The credit bore a 17% annual percentage rate and a six-year maturity, he says. The deal was brought to Circadian by a private equity investor who was looking to grow the enterprise tenfold. The deal, which was interest-only, was secured by a second position on real estate and a lien on the borrower’s license. “The lender was comfortable with the interest-only loan,” Sheinbaum explains. “They can refinance in six years.”

He recently brokered a $10 million loan for a licensed grower and distributor of medicinal marijuana in New England with monthly revenues of $3-$4 million. The credit bore a 17% annual percentage rate and a six-year maturity, he says. The deal was brought to Circadian by a private equity investor who was looking to grow the enterprise tenfold. The deal, which was interest-only, was secured by a second position on real estate and a lien on the borrower’s license. “The lender was comfortable with the interest-only loan,” Sheinbaum explains. “They can refinance in six years.”

In another recent deal, Circadian arranged an unsecured merchant cash advance for $300,000 to a Pacific Northwest technology company developing specialty, point-of-sale software for the cannabis industry. The firm showed monthly revenues of $300,000.

“It’s not federally permitted for cannabis firms to take payments from Visa, Mastercard or American Express,” Sheinbaum explains. “But this technology company is using debit or credit cards to pay for cryptocurrency which is stored on a prepaid card which customers can then use to purchase cannabis.”

The tech company had been struggling to find money and Sheinbaum took satisfaction in a deal announcement that went out in an e-mail to the industry. “Funding complicated deals is what gets our blood flowing,” Sheinbaum wrote. “Anyone can get a restaurant or dentist funded. No one needs help with that.”

Manny Columbie, a Miami-based senior funding manager at H&J Capital Group, an Orlando firm, reports funding agricultural and dispensary businesses in California, Colorado and Washington State. In the Evergreen State, he says, he recently provided funding to a woman who owned a marijuana-themed café connected to a cannabis dispensary. The deal went through after examining her recent bank statements and two years of federal tax returns.

“The best thing about lending to people in this industry is their ability to repay,” Columbie says. “They’re never lacking in funds.”

He provided more detail on a deal currently in the works involving a physician in Irvine, California, with an 800-plus credit score from the rating agency Experian and personal tax returns showing $2 million in annual income. The doctor, Columbie says, has been making transdermal patches infused with THC in addition to his medical practice and needs specialized equipment to lower his manufacturing costs to 55 cents per patch. The patches sell for $40-$60 apiece, Columbie says, depending on the THC content.

If the deal goes through and is approved by H&J’s credit committee, the physician would likely be extended a $350,000 loan with a 10-year maturity secured by the Chinese-manufactured equipment. Factoring in the doctor’s excellent credit and other positives, the interest rate on the credit could be as low as 5%-7%.

While the environment for legal cannabis seems to grow more favorable by the day, market participants urge funders to remain circumspect. One remaining fly in the legal cannabis ointment has been the persistence of an illegal black market. Estimates are that as much as 60% to 80% of the marijuana market in California is illicit, says Craig Behnke, an equity analyst at MJBiz.

Law-abiding businesses must also contend with overbearing regulators and high taxation. The California Department of Fee and Tax Administration recently jacked up its excise tax on cannabis to 80%, effective on Jan. 1, 2020.

And the state’s constabulary isn’t helping matters either, notes Sanger of Oak Funds. “There are going to be a lot of operators that end up being losers because of the regulatory environment,” she says. “Law enforcement is using all of its resources to make sure legitimate businesses are following the rules instead of clamping down on black market activity. That makes it harder for legitimate retailers to make money because people are still shopping in the black market.”

The recent collapse of the shares of publicly traded Canadian cannabis companies, which some blame in part on the illicit competition from the black market, also stands as a cautionary sign. Last August, the Motley Fool listed ten “Pot Stocks”—including Canopy Growth and Aurora Cannabis, both of which are listed on the New York Stock Exchange—that together lost a stunning $20 billion in market capitalization.

The drubbing that heedless investors have taken in the Canadian stocks reminds analyst Behnke of the debacle in dotcom stocks back in 2001-2002, but with a big difference. “The dotcoms were a brand-new invention and people had no idea how big the Internet companies would be,” he told AltFinanceDaily. “But cannabis has been around for a thousand years. I feel like it was a shame on investors and the companies. This shouldn’t have happened.”

For ISOs Only — How To Develop Your Factoring Brokerage Business (Part 3)

January 9, 2020 CONGRATULATIONS!!! You have finally made the decision to quit “stepping over” those hundred-dollar bills and establish a factoring brokerage business!

CONGRATULATIONS!!! You have finally made the decision to quit “stepping over” those hundred-dollar bills and establish a factoring brokerage business!

But here’s the problem. With literally THOUSANDS of hundred-dollar bills spread all over, WHERE and HOW do you start picking them up?

To be sure, you need a GAME PLAN for doing so, right? Well, today’s your lucky day because that’s exactly what Part 3 of our series is about; “HOW TO establish a GAME PLAN for establishing your factoring brokerage business”.

But first, a couple things to keep in mind. The first is that the closing and funding cycle for factoring is much longer than an MCA, and typically takes from a few days to a couple weeks. However, once your merchant is set up, they will typically fund invoices EVERY MONTH.

What that means to YOU it’s like getting an automatic renewal every month, because you’re GETTING PAID for the life of the factoring relationship. And that automatic monthly paycheck will keep getting bigger and bigger with every new factoring merchant! True “residual income”.

The second thing to consider is that you will need to identify the “mix” of factoring funders to do business with and get set up with as a broker.

While we touched on the topic of finding factoring funders in Part 2, we could actually do a series on this subject alone. Keep in mind that funders specialize by industry, i.e. construction, medical, trucking, etc., while others are generalists, and fund a broad range of industries both domestically and internationally.

OK. So, let’s get started. It’s basically a 2 step process. (Don’t worry. We’ll teach you how to dance.)

STEP 1: Take A Look in The Mirror

3 things you want to look at:

- The first is the size and structure of your existing ISO organization. What size is it? Are you a one-man shop? How many ISOs do you have in-house? How many in the field? Do ISOs in the field work under your umbrella or do they work under their own? Who makes the decision on which MCA funder to use?

This is important because the size and structure of your ISO organization will help you in determining which GAME PLAN OPTION is the BEST FIT. More on that later…

- The second thing you want to look at is how your existing merchant database is organized. This could range from a box of index cards to a computerized database where you can pull up contact info for every prospect, merchants funded, funding date, funded amount, commission, renewal date, and maybe even blood type. (Don’t laugh. Some guys are anal like that).

This is important because, regardless of how or where you keep this info, your existing files are where you’re going to find “low hanging fruit”.

More specifically, these are YOUR merchants who sell B2B with receivables RIGHT NOW! Plus, most are generating new invoices every month, and are PERPETUALLY WAITING to get paid. But let’s face it, you can’t sell the guy a new position every month (even though you might like to) because they obviously can’t sustain it. But now you have a solution that will.

- The last thing you want to look at is how you do your marketing; i.e., telemarketing, lead purchase, direct mail, email marketing, door to door, media advertising, etc. This is important because to be successful with integrating factoring into your existing business, you will need to integrate it into your existing marketing medium and message as well.

There are several ways to do this, but it essentially boils down to 3 simple questions:

- Do you sell B2B? Even restaurants who offer commercial catering could do more business if they didn’t have to wait 30 days or more to get paid.

- Roughly how much do you have outstanding in receivables?

- Would you be interested in looking at how to convert your invoices into cash with no payments?

Why Do We Need to Look in The Mirror?

REGARDLESS of how you operate your business, the purpose of this exercise is NOT for you to be judgmental (it is what it is), but simply to help you determine which GAME PLAN OPTION you feel is the BEST FIT for you. But to do so you have to be honest with what you see. That’s what “LOOKING IN THE MIRROR” is all about.

In starting a new year, we ALL would like to do better. And as much as we might consider making radical changes to our business model and even our personal lives, (i.e. losing 200 lbs. in 3 weeks), the changes that have a better chance of sticking are those we gradually integrate into our lives and business over time.

In other words, establish realistic goals for your new factoring brokerage business, establish a GAME PLAN for doing so, and over time you will gradually, and consistently generate positive results. Now, where’s that pie?

2. Select Your GAME PLAN Option

Once you’ve taken stock of where you are, the next step is to look at options for integrating factoring into your day-to-day operations.

Below are 3 GAME PLAN OPTIONS to consider;

OPTION 1: “Limited Service” Broker/Referral Agent

This option which might appeal to small ISO organizations or one-man shops. Once you have identified a factoring prospect and they have expressed interest in moving forward, make the introduction to your selected factoring funder, and for the most part, step back from the process.

HOW you do the introduction is totally up to you and can range from a three-way call, email, or even text in some cases. Regardless of how you do it, you want to make sure your Factoring Funder knows the referral came from you in order to get paid.

The funder will typically keep you posted as your merchant moves through the process. However, don’t forget. It’s YOUR merchant and YOUR money. So, don’t hesitate to follow-up with both.

This is essentially what I refer to as a “low touch” approach, designed for ISOs who want to start picking up one hundred-dollar bills, but have limited time or resources for doing so. At a minimum, it gets them in the game and launches a “new profit center”.

OPTION 2: “Full Service” Broker/Referral Agent

The full-service referral broker operates much like a traditional ISO does for MCAs. You work with the merchant to compile their factoring app package and submit it to the funder. In addition, as questions arise during underwriting, the funder may reach out and in some instances seek your help in addressing them.

Depending on the size and structure of your ISO organization, you might want to consider establishing an in-house Factoring Desk. This would be an individual designated as the point of contact between the referring ISO, the merchant, and the factoring funder.

There are multiple benefits for taking this approach. For one, you centralize the decision-making on the factoring funder best suited for the merchant. In so doing, your Factoring Desk should be familiar with each funder, their doc requirements, approval criteria, rates, terms, timing, etc.

Second, establishing an in-house Factoring Desk will limit the number of ISOs reaching out directly to your factoring funder. This is important because you don’t want an ISO to suggest, demand, or work outside the scope of your broker relationship and agreement with the funder.

Finally, establishing a Factoring Desk will facilitate a rapid response to getting your factoring deals done. The last thing you need is for a deal to be “stuck on someone’s desk,” simply because they shifted attention to work on something else.

OPTION 3: Broker/ Referral Partner Relationship

This option involves establishing a broker/referral relationship with an established entity which specializes in factoring and other forms of asset-based lending. This relationship can also be blended with Option 1 or 2.

For this arrangement to make sense, the broker/ referral partner should be well established and bring several things to the table including;

- Extensive and detail knowledge of the underwriting, due diligence, documentation, closing and funding process.

- Established relationships and history with a diverse mix of funders.

- Experience in addressing one of the fastest growing issues factoring funders are facing, which is resolving UCC filing issues, particularly within the MCA industry.

- Relationships with factoring funders who fund in “second position” behind other secured parties, including traditional bank financing.

- Knowledge and experience of other forms of financing including purchase order financing, material supply financing, etc.

To be sure, the right relationship will enable you to accelerate the funding process for your merchants while learning from their experience as well.

By the way, in Part 2 of the series, I mentioned a client who needed funding for 63 purchase orders to 63 different locations, of which half were expired. Well, I am pleased to announce they were funded!

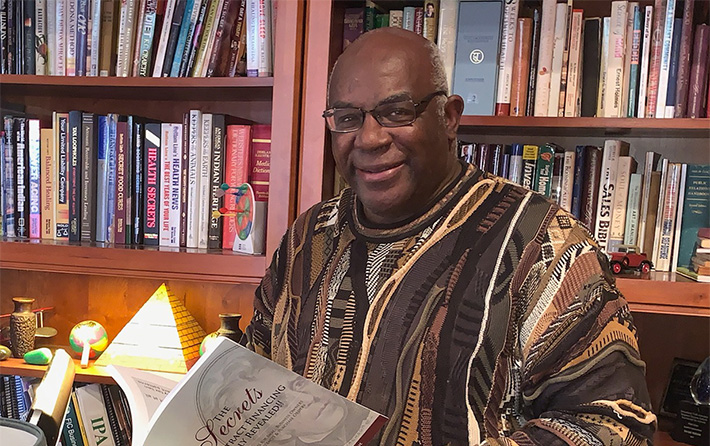

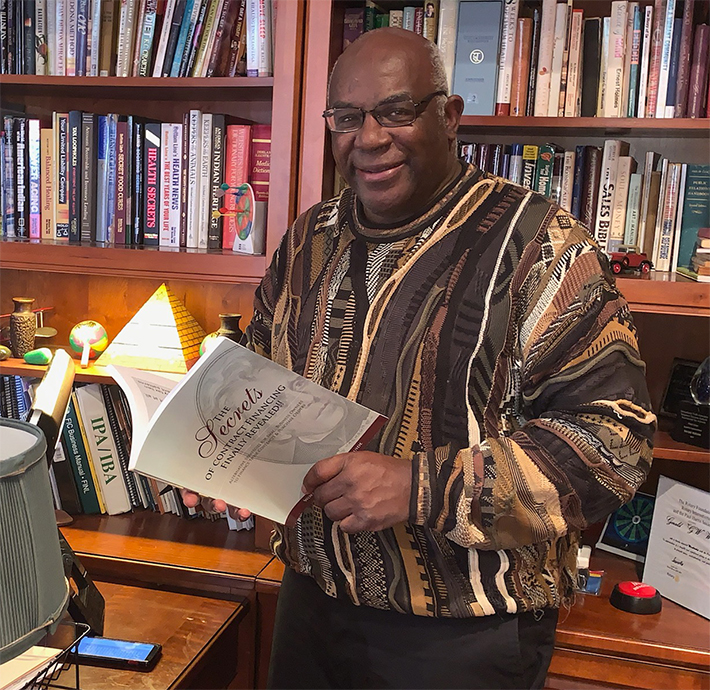

The Broker: How Gerald Watson Mixes Factoring with MCAs

December 3, 2019 Role?

Role?

I’m the owner of The Watson Group, a factoring broker company.

How did you end up in the industry?

I got started in what I call the contract financing industry about 35 years ago, kind of by accident. I had spent years working with a large management consulting company in Boston and we had some major contracts in the DC area. I was on an assignment there and my son was in school there with another kid, and I met the parents and the dad told me what he was doing and he said I needed to come by the offices to check it out.

I really had no intention of going at all, but finally to get this guy off my back, I went by one day and he showed me the business they were in. When I left I was totally on board. I had been working for several years in management consulting, but this was all new and I was excited because it was helping real businesses solve real problems and it was very hands-on.

I came on board and I’ll never forget my first day on the job: I didn’t know anything from anything – rights, factoring, contracts financing – this was years before the MCA industry even existed, and my boss said he just got a job, 911 call from a printer and they needed some funding help. “Can you help them? Why don’t you come ride with me? It’d be good on the job training for you.” And so we sat down with the guy and found a solution for him. And to this day he hasn’t had to close his business.

How were those early days?

Interesting because this was before the internet, almost before cell phones, in fact. I remember at one point when I was being hired, the Motorola flip phone was just coming out and they were like $1,500 around 25 years ago. And I said okay, I’ll take the job but you’ve got to give me one of these Motorola phones, so he did and it was great but this is before the internet and I didn’t really believe in traditional advertising or mailing out brochures, so the strategy I take is called “institutional referral-based marketing.”

In a nutshell, what that is, is working with various institutions that refer clients to use on a regular basis and as part of that process, I’d give talks or seminars and workshops and sit on panels and teach some of these referral groups how to assess deals and package them and get them ready for funding. You know, develop a pretty solid reputation in the industry for what we did and even today we’re 100% referral.

What can you tell me of the style in which you approach deals?

The approach that I’ve always taken is really a diagnostic approach, we kind of almost see ourselves as doctors. If you go to a doctor and you have pain, you may not know what’s causing that pain, you just want to feel better. And so what does the doctor do? They have to understand what’s going on in order to make you feel better.

Client’s got a pain: “I need money. I need working capital and I need it now.” And so we get a clear picture of what their objectives are and what they’re looking to accomplish: how much they need, what they need it for, timing, etc., and like a doctor, we go through a series of diagnostic tests, which can involve getting a list of documents – financials, bank statements, whatever it is – and going through them. You’re drilling down on where they’re at and coming up after that, coming up with what I call a treatment plan or funding strategy.

Here’s the key: you’ve got to ask the right questions, because if you don’t ask the right questions you’ll never get the right answer. All too often what a broker will do is they’ll get right into solutions and answers and talk about why what they offer is the best or why their funder is the best thing since sliced bread without having a picture of what their client’s true needs are in this situation. So I have a whole series of quizzes I’ve done a million times so I don’t need to write them down. I know what they are but I systematically go through ‘em, and we call that a preliminary underwriting interview.

What is the value of combining MCAs and factoring?

Funding solutions typically involve multi-funding products. And that’s where the advent of MCAs came in, and why they’re such a real asset. Because you meet a client today and it’s Wednesday, or Tuesday, hell maybe even Thursday, and the guy’s siting there with half a million dollars in receivables that we can convert into cash but we may need 3 days to do it, but he needs 2 days.

MCAs are a great product because we can step in, solve the problem, get him an immediate injection to stop the bleeding, and take it out from factoring proceeds a few days later. So it’s a great compliment and tool and this is something I’ve tried to educate on both sides. It’s not a threat it’s a complement. The key is how you use it. It’s like two medications. You go to a doctor, they’ll prescribe a list of meds, the key is to make sure they all complement each other.

Any advice for those looking to combine MCAs and factoring?

The first thing you want to do as an ISO who’s interested in developing a factoring brokering business is to understand the basics of factoring: what is factoring, how does it work, how do you qualify, how much does it cost?

The second thing you want to do is look internally to develop your customer base and the quickest customer base is what we call the low-hanging fruit. These are existing merchants that didn’t fund. Any merchant that is in B2B, whether they got funded or not, is a candidate for factoring. So go back through the files, look at the database and you may find out you probably have a lot more than what you ever imagined.

The third is to develop your database of funding resources – of funders.

And the last thing you want to have is a game plan. What’s your game plan and what’s your strategy for moving forward with your factoring broker business?

Less Than Perfect — New State Regulations

December 21, 2018

You could call California’s new disclosure law the “Son-in-Law Act.” It’s not what you’d hoped for—but it’ll have to do.

That’s pretty much the reaction of many in the alternative lending community to the recently enacted legislation, known as SB-1235, which Governor Jerry Brown signed into law in October. Aimed squarely at nonbank, commercial-finance companies, the law—which passed the California Legislature, 28-6 in the Senate and 72-3 in the Assembly, with bipartisan support—made the Golden State the first in the nation to adopt a consumer style, truth-in-lending act for commercial loans.

The law, which takes effect on Jan. 1, 2019, requires the providers of financial products to disclose fully the terms of small-business loans as well as other types of funding products, including equipment leasing, factoring, and merchant cash advances, or MCAs.

The financial disclosure law exempts depository institutions—such as banks and credit unions—as well as loans above $500,000. It also names the Department of Business Oversight (DBO) as the rulemaking and enforcement authority. Before a commercial financing can be concluded, the new law requires the following disclosures:

The financial disclosure law exempts depository institutions—such as banks and credit unions—as well as loans above $500,000. It also names the Department of Business Oversight (DBO) as the rulemaking and enforcement authority. Before a commercial financing can be concluded, the new law requires the following disclosures:

(1) An amount financed.

(2) The total dollar cost.

(3) The term or estimated term.

(4) The method, frequency, and amount of payments.

(5) A description of prepayment policies.

(6) The total cost of the financing expressed as an annualized rate.

The law is being hailed as a breakthrough by a broad range of interested parties in California—including nonprofits, consumer groups, and small-business organizations such as the National Federation of Independent Business. “SB-1235 takes our membership in the direction towards fairness, transparency, and predictability when making financial decisions,” says John Kabateck, state director for NFIB, which represents some 20,000 privately held California businesses.

“What our members want,” Kabateck adds, “is to create jobs, support their communities, and pursue entrepreneurial dreams without getting mired in a loan or financial structure they know nothing about.”

Backers of the law, reports Bloomberg Law, also included such financial technology companies as consumer lenders Funding Circle, LendingClub, Prosper, and SoFi.

But a significant segment of the nonbank commercial lending community has reservations about the California law, particularly the requirement that financings be expressed by an annualized interest rate (which is different from an annual percentage rate, or APR). “Taking consumer disclosure and annualized metrics and plopping them on top of commercial lending products is bad public policy,” argues P.J. Hoffman, director of regulatory affairs at the Electronic Transactions Association.

The ETA is a Washington, D.C.-based trade group representing nearly 500 payments technology companies worldwide, including such recognizable names as American Express, Visa and MasterCard, PayPal and Capital One. “If you took out the annualized rate,” says ETA’s Hoffman, “we think the bill could have been a real victory for transparency.”

The ETA is a Washington, D.C.-based trade group representing nearly 500 payments technology companies worldwide, including such recognizable names as American Express, Visa and MasterCard, PayPal and Capital One. “If you took out the annualized rate,” says ETA’s Hoffman, “we think the bill could have been a real victory for transparency.”

California’s legislation is taking place against a backdrop of a balkanized and fragmented regulatory system governing alternative commercial lenders and the fintech industry. This was recognized recently by the U.S. Treasury Department in a recently issued report entitled, “A Financial System That Creates Economic Opportunities: Nonbank Financials, Fintech, and Innovation.” In a key recommendation, the Treasury report called on the states to harmonize their regulatory systems.

As laudable as California’s effort to ensure greater transparency in commercial lending might be, it’s adding to the patchwork quilt of regulation at the state level, says Cornelius Hurley, a Boston University law professor and executive director of the Online Lending Policy Institute. “Now it’s every regulator for himself or herself,” he says.

Hurley is collaborating with Jason Oxman, executive director of ETA, Oklahoma University law professor Christopher Odinet, and others from the online-lending industry, the legal profession, and academia to form a task force to monitor the progress of regulatory harmonization.

For now, though, all eyes are on California to see what finally emerges as that state’s new disclosure law undergoes a rulemaking process at the DBO. Hoffman and others from industry contend that short-term, commercial financings are a completely different animal from consumer loans and are hoping the DBO won’t squeeze both into the same box.

Steve Denis, executive director of the Small Business Finance Association, which represents such alternative financial firms as Rapid Advance, Strategic Funding and Fora Financial, is not a big fan of SB-1235 but gives kudos to California solons—especially state Sen. Steve Glazer, a Democrat representing the Bay Area who sponsored the disclosure bill—for listening to all sides in the controversy. “Now, the DBO will have a comment period and our industry will be able to weigh in,” he notes.

While an annualized rate is a good measuring tool for longer-term, fixed-rate borrowings such as mortgages, credit cards and auto loans, many in the small-business financing community say, it’s not a great fit for commercial products. Rather than being used for purchasing consumer goods, travel and entertainment, the major function of business loans are to generate revenue.

A September, 2017, study of 750 small-business owners by Edelman Intelligence, which was commissioned by several trade groups including ETA and SBFA, found that the top three reasons businesses sought out loans were “location expansion” (50%), “managing cash flow” (45%) and “equipment purchases” (43%).

The proper metric to be employed for such expenditures, Hoffman says, should be the “total cost of capital.” In a broadsheet, Hoffman’s trade group makes this comparison between the total cost of capital of two loans, both for $10,000.

Loan A for $10,000 is modeled on a typical consumer borrowing. It’s a five-year note carrying an annual percentage rate of 19%—about the same interest rate as many credit cards—with a fixed monthly payment of $259.41. At the end of five years, the debtor will have repaid the $10,000 loan plus $5,564 in borrowing costs. The latter figure is the total cost of capital.

Compare that with Loan B. Also for $10,000, it’s a six month loan paid down in monthly payments of $1,915.67. The APR is 59%, slightly more than three times the APR of Loan A. Yet the total cost of capital is $1,500, a total cost of capital which is $4,064.33 less than that of Loan A.

Meanwhile, Hoffman notes, the business opting for Loan B is putting the money to work. He proposes the example of an Irish pub in San Francisco where the owner is expecting outsized demand over the upcoming St. Patrick’s Day. In the run-up to the bibulous, March 17 holiday, the pub’s owner contracts for a $10,000 merchant cash advance, agreeing to a $1,000 fee.

Once secured, the money is spent stocking up on Guinness, Harp and Jameson’s Irish whiskey, among other potent potables. To handle the anticipated crush, the proprietor might also hire temporary bartenders.

When St. Patrick’s Day finally rolls around—thanks to the bulked-up inventory and extra help—the barkeep rakes in $100,000 and, soon afterwards, forwards the funding provider a grand total of $11,000 in receivables. The example of the pub-owner’s ability to parlay a short-term financing into a big payday illustrates that “commercial products—where the borrower is looking for a return on investment—are significantly different from consumer loans,” Hoffman says.

SBFA’s Denis observes that financial products like merchant cash advances are structured so that the provider of capital receives a percentage of the business’s daily or weekly receivables. Not only does that not lend itself easily to an annualized rate but, if the food truck, beautician, or apothecary has a bad day at the office, so does the funding provider. “It’s almost like the funding provider is taking a ride” with the customer, says Denis.

SBFA’s Denis observes that financial products like merchant cash advances are structured so that the provider of capital receives a percentage of the business’s daily or weekly receivables. Not only does that not lend itself easily to an annualized rate but, if the food truck, beautician, or apothecary has a bad day at the office, so does the funding provider. “It’s almost like the funding provider is taking a ride” with the customer, says Denis.

Consider a cash advance made to a restaurant, for instance, that needs to remodel in order to retain customers. “An MCA is the purchase of future receivables,” Denis remarks, “and if the restaurant goes out of business— and there are no receivables—you’re out of luck.”

Still, the alternative commercial-lending industry is not speaking with one voice. The Innovative Lending Platform Association—which counts commercial lenders OnDeck, Kabbage and Lendio, among other leading fintech lenders, as members—initially opposed the bill, but then turned “neutral,” reports Scott Stewart, chief executive of ILPA. “We felt there were some problems with the language but are in favor of disclosure,” Stewart says.

The organization would like to see DBO’s final rules resemble the company’s model disclosure initiative, a “capital comparison tool” known as “SMART Box.” SMART is an acronym for Straightforward Metrics Around Rate and Total Cost—which is explained in detail on the organization’s website, onlinelending.org.

But Kabbage, a member of ILPA, appears to have gone its own way. Sam Taussig, head of global policy at Atlanta-based financial technology company Kabbage told AltFinanceDaily that the company “is happy with the result (of the California law) and is working with DBO on defining the specific terms.”

Others like National Funding, a San Diego-based alternative lender and the sixth-largest alternative-funding provider to small businesses in the U.S., sat out the legislative battle in Sacramento. David Gilbert, founder and president of the company, which boasted $94.5 million in revenues in 2017, says he had no real objection to the legislation. Like everyone else, he is waiting to see what DBO’s rules look like.

“It’s always good to give more rather than less information,” he told AltFinanceDaily in a telephone interview. “We still don’t know all the details or the format that (DBO officials) want. All we can do is wait. But it doesn’t change this business. After the car business was required to disclose the full cost of motor vehicles,” Gilbert adds, “people still bought cars. There’s nothing here that will hinder us.”

With its panoply of disclosure requirements on business lenders and other providers of financial services, California has broken new legal ground, notes Odinet, the OU law professor, who’s an expert on alternative lending and financial technology. “Not many states or the federal government have gotten involved in the area of small business credit,” he says. “In the past, truth-in-lending laws addressing predatory activities were aimed primarily at consumers.”

The financial-disclosure legislation grew out of a confluence of events: Allegations in the press and from consumer activists of predatory lending, increasing contraction both in the ranks of independent and community banks as well as their growing reluctance to make small-business loans of less than $250,000, and the rise of alternative lenders doing business on the Internet.

In addition, there emerged a consensus that many small businesses have more in common with consumers than with Corporate America. Rather than being managed by savvy and sophisticated entrepreneurs in Silicon Valley with a Stanford pedigree, many small businesses consist of “a man or a woman working out of their van, at a Starbucks, or behind a little desk in their kitchen,” law professor Odinet says. “They may know their business really well, but they’re not really in a position to understand complicated financial terms.”

The average small-business owner belonging to NFIB in California, reports Kabateck, has $350,000 in annual sales and manages from five to nine employees. For this cohort—many of whom are subject to myriad marketing efforts by Internet-based lenders offering products with wildly different terms—the added transparency should prove beneficial. “Unlike big businesses, many of them don’t have the resources to fully understand their financial standing,” Kabateck says. “The last thing they want is to get steeped in more red ink or—even worse—have the wool pulled over their eyes.”

California’s disclosure law is also shaping up as a harbinger—and perhaps even a template—for more states to adopt truth-in-lending laws for small-business borrowers. “California is the 800-lb. gorilla and it could be a model for the rest of the country,” says law professor Hurley. “Just as it has taken the lead on the control of auto emissions and combating climate change, California is taking the lead for the better on financial regulation. Other states may or may not follow.”

California’s disclosure law is also shaping up as a harbinger—and perhaps even a template—for more states to adopt truth-in-lending laws for small-business borrowers. “California is the 800-lb. gorilla and it could be a model for the rest of the country,” says law professor Hurley. “Just as it has taken the lead on the control of auto emissions and combating climate change, California is taking the lead for the better on financial regulation. Other states may or may not follow.”

Reflecting the Golden State’s influence, a truth-in-lending bill with similarities to California’s, known as SB-2262, recently cleared the state senate in the New Jersey Legislature and is on its way to the lower chamber. SBFA’s Denis says that the states of New York and Illinois are also considering versions of a commercial truth-in-lending act.

But the fact that these disclosure laws are emanating out of Democratic states like California, New Jersey, Illinois and New York has more to do with their size and the structure of the states’ Legislatures than whether they are politically liberal or conservative. “The bigger states have fulltime legislators,” Denis notes, “and they also have bigger staffs. That’s what makes them the breeding ground for these things.”

Buried in Appendix B of Treasury’s report on nonbank financials, fintechs and innovation is the recommendation that, to build a 21st century economy, the 50 states should harmonize and modernize their regulatory systems within three years. If the states fail to act, Treasury’s report calls on Congress to take action.

The triumvirate of Hurley, Oxman and Odinet report, meanwhile, that they are forming a task force and, with the tentative blessing of Treasury officials, are volunteering to monitor the states’ progress. “I think we have an opportunity as independent representatives to help state regulators and legislators understand what they can do to promote innovation in financial services,” ETA’s Oxman asserts.

The ETA is a lobbying organization, Oxman acknowledges, but he sees his role—and the task force’s role—as one of reporting and education. He expects to be meeting soon with representatives of the Conference of State Bank Supervisors (CSBS), the Washington, D.C.-based organization representing regulators of state chartered banks. It is also the No. 1 regulator of nonbanks and fintechs. “They are the voice of state financial regulators,” Oxman says, “and they would be an important partner in anything we do.”

The ETA is a lobbying organization, Oxman acknowledges, but he sees his role—and the task force’s role—as one of reporting and education. He expects to be meeting soon with representatives of the Conference of State Bank Supervisors (CSBS), the Washington, D.C.-based organization representing regulators of state chartered banks. It is also the No. 1 regulator of nonbanks and fintechs. “They are the voice of state financial regulators,” Oxman says, “and they would be an important partner in anything we do.”

Margaret Liu, general counsel at CSBS, had high praise for Treasury’s hard work and seriousness of purpose in compiling its 200-plus page report and lauded the quality of its research and analysis. But Liu noted that the conference was already deeply engaged in a program of its own, which predates Treasury’s report.

Known as “Vision 2020,” the program’s goals, as articulated by Texas Banking Commissioner Charles Cooper, are for state banking regulators to “transform the licensing process, harmonize supervision, engage fintech companies, assist state banking departments, make it easier for banks to provide services to non-banks, and make supervision more efficient for third parties.”

While CSBS has signaled its willingness to cooperate with Treasury, the conference nonetheless remains hostile to the agency’s recommendation, also found in the fintech report, that the Office of the Comptroller of the Currency issue a “special purpose national bank charter” for fintechs. So vehemently opposed are state bank regulators to the idea that in late October the conference joined the New York State Banking Department in re-filing a suit in federal court to enjoin the OCC, which is a division of Treasury, from issuing such a charter.

Among other things, CSBS’s lawsuit charges that “Congress has not granted the OCC authority to award bank charters to nonbanks.”

Previously, a similar lawsuit was tossed out of court because, a judge ruled, the case was not yet “ripe.” Since no special purpose charters had actually been issued, the judge ruled, the legal action was deemed premature. That the conference would again file suit when no fintech has yet applied for a special purpose national bank charter— much less had one approved—is baffling to many in the legal community.

“I suspect the lawsuit won’t go anywhere” because ripeness remains a sticking point, reckons law professor Odinet. “And there’s no charter pending,” he adds, in large part because of the lawsuit. “A lot of people are signing up to go second,” he adds, “but nobody wants to go first.”

Treasury’s recommendation that states harmonize their regulatory systems overseeing fintechs in three years or face Congressional action also seems less than jolting, says Ross K. Baker, a distinguished professor of political science at Rutgers University and an expert on Congress. He told AltFinanceDaily that the language in Treasury’s document sounded aspirational but lacked any real force.

“Usually,” he says, such as a statement “would be accompanied by incentives to do something. This is a kind of a hopeful urging. But I don’t see any club behind the back,” he went on. “It seems to be a gentle nudging, which of course they (the states) are perfectly able to ignore. It’s desirable and probably good public policy that states should have a nationwide system, but it doesn’t say Congress should provide funds for states to harmonize their laws.

“When the Feds issue a mandate to the states,” Baker added, “they usually accompany it with some kind of sweetener or sanction. For example, in the first energy crisis back in 1973, Congress tied highway funds to the requirement (for states) to lower the speed limit to 55 miles per hour. But in this case, they don’t do either.”

Grooming The Best Sales Reps

August 22, 2018The best sales reps have a lot in common – they’re smart, honest, likable, well-organized, thick-skinned and hungry for success. They navigate the difficult early days of their careers in the alternative small-business funding community by persevering despite long hours, countless outbound telephone calls and meager commissions.

“Persistency is really, really the key – putting in the time,” says Evan Marmott, CEO of Montreal-based CanaCap and CEO of New York-based CapCall LLC. “It’s not always easy, but you’ve got to stay late, make the phone calls, send the emails and do the follow-ups. It’s a numbers game.”

Being relentless counts not only when pursuing merchants but also when matching merchants with funders, Marmott emphasizes. “If they can’t get an approval one place, they’re going to shop it out until they get approval someplace else so they can monetize everything that comes in,” he says.

“It’s all mindset and work ethic,” in sales, according to Joe Camberato, president at Bohemia, N.Y.-based National Business Capital. His company works to create a culture that supports the right mindset by working with a firm called “Delivering Happiness.” Together, they forge to a set of core values based on integrity, innovation, teamwork, empathy, and respect for fellow employees, clients and clients’ businesses.

National Business Capital employees learn to live those ideals by working and playing together on the company volleyball team, through work with local and national charities, and at company mixers and staff picnics, Camberato maintains. “We adapt and change, and we’re committed to helping small businesses grow,” he says of the company culture, “and we have fun while doing all that.”

Likeability helps build relationships with customers, says Justin Thompson, vice president of sales for San Diego-based National Funding. “People will do business with people they like and trust,” says Thompson. “It’s really about establishing a relationship first and then establishing quality discovery.” From there, presentation and execution become paramount, he says.

Methodology can make the difference between success and failure in sales, observes Justin Bakes, co-founder and CEO of Boston-based Forward Financing LLC. “Have a defined process and stick to it,” he advises. A well-organized approach inspires trust among clients, establishes and maintains a great reputation; and fosters understanding of the customers’ needs, wants and business operations that help the rep choose the right financing option and appropriate funder. Using technology to wrangle multiple leads and high volume counts for a lot, too, he says.

It’s all part of the consultative approach to sales, says Jared Weitz, CEO of Great Neck, N.Y.-based United Capital Source. Long ago, sales reps may have succeeded by mimicking carnival barkers, sideshow pitchman and arm-twisting medicine-show peddlers. Thankfully, those days have ended – if they ever really existed. Most of today’s successful salespeople earn clients’ respect by becoming knowledgeable, trusted business consultants, says Weitz.

THE CONSULTATIVE SALE

“Someone calls, and there are two ways of handling a deal, right?” Weitz asks rhetorically. Using one method, a salesperson can say, “We’ll fund you this much at this rate today – are we good?” he says. The other way calls for understanding the client’s business – how long has it been open, does it make more cash deposits or credit card deposits, would it be best-served by an advance, a loan, an equipment lease or a line of credit, how much can it afford in monthly payments?

Establishing how the merchant intends to use the funding plays a crucial role in the consultative sale, Marmott agrees. Objections can arise when a merchant learns that receiving $100,000 this week will require paying back $150,000 in four or five months, he notes. So it’s essential to demonstrate that using the money productively will more than pay for the deal. A trucking company can realize more income if it deploys two more trucks, or a restaurant can increase revenue by placing another bar outside for the summer, he says by way of example.

“A lot of salespeople ask a business owner what they need the money for,” observes Thompson. “The merchant says, ‘Inventory,’ and the rep stops right there. I train my reps at National Funding to go two or three clicks deeper.” Examples abound. When does the merchant need the inventory? From whom do they order it? How long does it take to ship? How long does it take to turn it over? What are the shipping terms?

The consultative approach can require salespeople to pose a lot of open-ended questions that can’t be answered yes or no, according to Thompson. Ideally, the conversation should adhere to the 80-20 rule, with the client talking 80 percent of the time and the sales rep speaking 20 percent, he asserts, adding that “a lot of times it’s reversed in this industry.”

Sometimes, however, salespeople should set aside the time-consuming consultative approach and instead find funding for a merchant as soon as possible. That’s true when the business owner can make an opportune purchase of inventory or when it’s time to acquire a competitor quickly. More often, however, it pays to take the time to understand the merchant’s needs and search out the best type of funding for that particular case, top sales people maintain.

Much of the alternative small-business finance industry has caught on to the importance of the consultative approach to sales as the array of available alternative financial products has grown beyond the industry’s initial offerings of merchant cash advances, according to Weitz. The days of scripted pitches and preplanned rebuttals to objections have ended, he says. Today, management trains reps for success.

THE RIGHT TRAINING

Are top salespeople born that way? “Some people hit the ground running, but sales can be taught – that’s for sure,” Weitz says. “The tougher thing to teach is integrity.” Much of the training process focuses on learning the products to enable a rep to make a consultative sale and shoulder financial responsibility, he maintains.

Believing that some people are born to sell provides a crutch to avoid learning what really works, according to Bakes. Training can teach a smart, motivated person how to succeed, he maintains. They don’t have to be born that way.

However, some people do seem born to exert influence, which can translate into sales prowess, says Thompson. Still, those born with a strong work-ethic can overcome other deficiencies, he notes. The work ethic drives them to “come in every day,” he notes. “They’re organized and disciplined. They follow the National Funding philosophy, and they make a ton of money.”

National Funding trains salespeople to view their craft as being defined by two broad elements – art and science, Thompson continues. The science proves easier to master and includes asking the right questions to learn about the customer and the deal. The hard part, the art of the sale, consists of getting to know the business owner, building a relationship and demonstrating expertise. In one example, that’s based on learning how many trucks are in the fleet, whether they’re long-haul or short haul and whether they use dumpsters versus box trailers, he says.

Beyond those important basics, training should be ongoing because selling techniques change slightly as new products and systems emerge, according to Weitz. “One of the things I like about being a broker is the ability to pivot and add another arrow to your quiver,” he says.

Salespeople at United Capital Source talk sales among themselves almost nonstop, which amounts to daily sales training, Weitz observes. That can take the form of describing a challenge and explaining how to overcome it, he notes. A particularly good idea merits an email to the group to share the new piece of wisdom. It’s a matter of constantly refining the approach.

Training can help sales reps understand the businesses their clients run, according to Marmott. Knowing the margins in a restaurant, for example, can help the salesperson explain that the increase in revenue from an expansion will quickly pay the cost of capital, he notes.

Training should teach new employees how business works because common elements arise in enterprises ranging from dog grooming to asphalt paving, Thompson notes. There’s inventory, marketing, employee expense, payroll taxes, insurance and 401k’s in almost any business. “We teach all that to the reps,” he says. Then after conversations with thousands of merchants, reps have a solid foundation in the workings of businesses.

National Business Capital’s formal two-week classroom training usually lasts three hours a day, focusing on systems, guidelines, product, general business principles and the company’s processes, says Camberato. Teachers include the sales management team, company culture leaders and the managers of IT and Tech, Marketing, Processing, and Human Resources.

National Business Capital’s formal two-week classroom training usually lasts three hours a day, focusing on systems, guidelines, product, general business principles and the company’s processes, says Camberato. Teachers include the sales management team, company culture leaders and the managers of IT and Tech, Marketing, Processing, and Human Resources.

New hires spend much of their time working with mentors for the first six months and a team leader who works with them indefinitely, Camberto continues. The company sometimes hires in groups and sometimes hires individually, he notes.

National Funding provides three eight-hour days of regimented classroom training on the fundamentals to each of the four groups of 12 to 17 hired each year, says Thompson. The classes cover processes, sales strategy, marketing and the lender matrix. Next comes three months of working with a sales manager dedicated to working with the class. After a total of nine to 12 months, management knows which reps will succeed.

Some shops operate on the opener-closer model, with less experienced salespeople qualifying the merchant by asking questions like how long they’re been in business and how much revenue they bring in monthly, Marmott says. If the merchant qualifies, the newer salesperson who’s working as an opener then hands off the call to an experienced closer to complete the deal. Good openers become closers, but opening isn’t easy because it requires lots of calls, he notes.

National Funding doesn’t use the opener-closer approach because the company believes reps should Participate “from cradle to grave,” Thompson says. “They hunt the business down, build the relationship and handle the transaction from A to Z.” East Coast shops often focus on cold calling and use the opener-closer model, while West Coast shops tend to invest more in marketing and reject the opener-closer method, he noted.

But where do these top salespeople come from?

THE RIGHT BACKGROUND

Prospective sales reps who have just finished college should have a grounding in communications or business, Weitz believes. Experience in sales and a familiarity with dealing with merchants helps prepare reps, he notes. Job history doesn’t have to be in the finance industry. Someone who’s sold business services in a Verizon store or worked for a payroll company, for instance, has been dealing with small-business owners and may succeed more quickly than those without that background.

Sales experience in other industries counts, Bakes agrees, especially in businesses that require dealing with a large number of leads. “Organization and process is just as important as being born with the traits of a salesperson,” he opines.

Life experience that breeds a positive attitude can prove vital, says Marmott. That’s especially important in the beginning when a new rep might take home a paltry $300 in the first month. Later, when the rep has a $50,000 month, he or she will see that their optimism wasn’t misplaced, he declares.

GUYS WHO ARE HUNGRY”

“The biggest thing I look for is guys who are hungry,” Marmott maintains. I don’t need somebody with a doctorate or a master’s degree or even a degree,” he says. “I need somebody who is going to put the work in.” Of a roomful of 25 new reps, two or three will succeed and stay on the job, he calculates. “You get to eat what you kill. If you’re not killing anything, you don’t get to eat.”

“We look for potential candidates who come from backgrounds of rejection,” says Thompson. Their previous sales experience has taught them not to take the answer “no” personally. “It’s part of the business and you continue to move on.”

Although most regard the financial services industry as a white-collar pursuit, “it has blue collar written all over it,” Thompson says, referring to the work ethic required for success. But it’s not just the volume of work. Sixty good phone calls generate more business than 300 mediocre calls, he emphasizes.

GETTING UP TO SPEED

Succeeding at sales requires taking the time to form relationships, understand guidelines, become familiar with lenders and acquire a working knowledge of how clients’ businesses operate, Camberato says. How long does it take? “It’s a solid year,” he contends while conceding that most who succeed operate at a fairly high level before then.

Others disagree about what constitutes being up to speed and how much time’s necessary to achieve it. “I’ve seen it take 30 days, and I’ve seen it up to 120 days,” says Weitz. “The hope is that it’s within 60.”

A salesperson should start feeling better after 30 days and should start feeling good after 60 days, Marmott says. Management can usually identify the strong and the week reps within two to three weeks, he says. “You get the lazy ones that drop out, the guys who aren’t making any money, the ones who aren’t putting the effort in,” he says. “The first two weeks are the toughest because you’re learning the product and how to sell it.”

“It depends on the person,” Bakes says of the time needed to begin selling successfully. “It takes time. It is not something that will just happen overnight.” About six months should suffice to become confident as a closer, he estimates.

Even when sales reps hit their stride, some outsell others, Marmott notes, citing the 80-20 rule that 80 percent of the business comes from 20 percent of the salesforce. Outbound sales to merchants who may feel beleaguered by offers of funding requires more effort than when a merchant makes an inbound call to seek funding, he adds.

And even the best salespeople need great marketing and tech support from the their companies, sources agree.

INVESTING IN SALES

A shop just starting out might have a marketing budget as low as $2,500 a month, which won’t do much more than pay for direct mail pieces that might prompt a few potential clients to pick up the phone, Weitz says. With a little more money to spend, a shop can begin buying leads, he notes. “Don’t break the bank before you understand what formula works for you,” he advises.

“The key to sales is marketing,” says Marmott. “You can be the best sales guy but if you don’t have anything qualified to call or follow up with, it’s a waste of time.” Social media doesn’t work as well for business-to-business contact as it does for business-to-consumer marketing, he says. Pay per click and key words have become more expensive and isn’t as cost-effective as it once was, especially for smaller shops, he contends. Mailers can work but require heavy volume and repetition, he says, adding that could mean at least 25,000 pieces and at least three mailings.