AltFinanceDaily’s Top Five Stories of 2021

December 20, 2021 deBanked’s most read stories of 2021 were similar but different to those read in 2020. We broke them down into categories by popularity.

deBanked’s most read stories of 2021 were similar but different to those read in 2020. We broke them down into categories by popularity.

1. Scandal

A South Florida business apparently masquerading as a small business finance company, was by far and away the most read story of 2021. Authorities now believe that it was a $200M+ ponzi scheme with more than 5,500 investors. Unlike other alleged schemes that have rocked the finance world, thousands of people believe the allegations are not true and have rallied around the CEO.

2. Domain Life after Death

The Death of a Thousand Financial Companies, the leading story of AltFinanceDaily’s March/April 2021 magazine issue, was the 2nd most popular across 2021. In it, AltFinanceDaily went undercover to find out what happened to the domain names of financial companies that went out of business. The findings were terrifying. (See: Video discussion about the story)

3. Real Estate Investing

Think what you want about crypto as the future because when it came down to it, AltFinanceDaily readers were vastly more interested in real estate investing. Why Funders Are Investing in Real Estate As Their Side Hustle of Choice was the 3rd most read story of 2021. “[Real estate is] just a way that people who have been successful and spin off a lot of cash for their businesses see as a safe way to diversify their income,” said a lawyer that was interviewed for the story.

4. Regulation

It was a close call between several stories pertaining to regulation. While interest in CFPB-related activity ranked high, so too did a court decision in Florida that ruled on the legality of merchant cash advances. The New York commercial financing disclosure law was also top of mind for many readers as was interest in proposed legislation in Maryland.

5. An Exit

The fall of LendUp, an online consumer lending company, was apparently of great interest in 2021. After some difficult encounters with regulators, the company ceased lending operations. “Although we are no longer lending, we also offer a series of free online education courses designed to boost your financial savvy fast,” the company’s website now says.

The Current State of SME Lending in Canada

December 1, 2019 According to the latest statistics, there were 1.18 million employer businesses in Canada, with the majority of them located in the provinces of Ontario and Quebec.

According to the latest statistics, there were 1.18 million employer businesses in Canada, with the majority of them located in the provinces of Ontario and Quebec.

- 1.15 million (97.9%) represented small businesses

- 21.926 (1.9%) referred to medium-sized ventures

- Only 2.939 (0.2%) accounted for large corporations

Small and medium companies are blooming in Canada: they represent 99.8% of all businesses, and they are the heart of the local economy. However, these businesses are facing extreme challenges when it comes to raising capital – a crucial element of SME growth.

The Canadian banking sphere, dominated by five large banks, often overlooks these businesses. Banks in Canada typically require 32 articles of information when applying for a loan and still 78% of applications from SMEs are rejected. It is especially stressful for startups: you can’t get a loan unless you have customers, but you can’t start your business and get customers without a loan. Cash flow, on the whole, is a complex concept that may be confusing for small business owners, and this kind of financial exclusion only makes it worse. The problem is global, but this Catch-22 has given the green light to alternative lenders worldwide.

THE ALTERNATIVE

One of the alternative funding options for SMEs to bypass the banks and find the right level of capital that they need is called a merchant cash advance (MCA). MCAs aren’t loans. Instead, they represent the sale of a business’s future revenues in exchange for quick cash — the majority of applications are approved within 2 days. This way, a funder provides a lump sum payment with a predetermined percentage (the factor rate) of a merchant’s future credit or debit card sales — cash and check sales typically don’t qualify to be counted. The process goes on until the contractual terms are satisfied. The MCA industry is growing on Canadian soil, but since it is a relatively new domain, the sector remains heavily influenced by American providers, especially when it comes to business models and pricing. But domestic providers don’t see it as a threat. Bruce Marshall, VP of British Columbia-based Company Capital told AltFinanceDaily in 2016 that “We are happy that some of the bigger US players are coming up here and they are spending millions of dollars on advertising. These companies raise awareness of the industry to a higher level and with us being a smaller company, we can ride on their coattails.”

The question of raising awareness of new technology is vital. In comparison to American SME owners, their Canadian colleagues are slower to adopt technology — for instance, only 27% say they currently use technology to analyze customer data. Another study by BDC claims that only 19% of Canadian businesses are digitally advanced.

On the other side, those established companies find the Canadian alternative lending market to be “a very manageable extension of the US market.” However, it’s a smaller market, and Canada’s geographical position (the majority of businesses are located in four main provinces out of thirteen) and regional differences play their part as well. For instance, because of the restrictions that require businesses to advertise and produce marketing materials in French, the majority of alternative lenders from the US don’t operate in Quebec.

RATES, COSTS, AND FIGURES

All in all, MCAs are slowly becoming a financing option for Canadian SMEs looking for quick cash. That “slowness” comes from a lack of understanding about how exactly merchant cash advances work. Some alternative funders take advantage of their non-bank status to neglect regulations that require clarity resulting in somewhat unethical lending practices. Because of this, a certain number of business owners still hesitate to take a chance on a merchant cash advance program.

MCAs in Canada are generally available to businesses that have a steady volume of credit card sales, such as retail stores or restaurants. The amount of personal and business information required when applying for an MCA is much lower in comparison to a regular bank loan application: the documentation generally includes proof of identity, bank statements, and business tax returns. Merchant cash advance rates and costs differ from provider to provider. As MCAs aren’t loans, there are no fixed amounts for repayment installments and no fixed terms either. Typically, the percentage of credit card sales taken to enable the transaction ranges from 5 to 10%. Some companies in Canada charge premiums on their cash advances (which can be as high as 30% or even more.)

THE CHALLENGE

The main challenge for Canadian MCA providers is the absence of reliable data necessary for making underwriting decisions. As previously mentioned, only a small group of large financial institutions dominate the market, so the data is available solely to a handful of businesses. The information obtained from credit bureaus doesn’t help either: in most cases, it isn’t complete for making a wise credit decision. “The availability and access to government and financial data are scarce in Canada compared to other markets,” said Jeff Mitelman, the former CEO of Thinking Capital in an interview with AltFinanceDaily in a past interview. “Most of the data relationships that fintech companies rely on, need to be developed on a one-to-one basis and is often proprietary information.”

When it comes to the process of underwriting, the availability of data presented in the proper format is a crucial factor. It provides the full picture and saves an enormous amount of time for risk officers. “We pay a lot of attention to our underwriting and decision-making process because if we make a mistake, we can lose a lot of money,” Andrew D’Souza, the CEO of Clearbanc, told TechCrunch.

At the moment, the financial data available to Canadian alternative lenders is meager and needs improvement. Another issue is the legislation that varies with each province. Many alternative lenders find the Canadian rules and regulations that govern the industry rather unclear. However, those challenges are associated with a growing market and emerging ecosystem. One way or another, the business loan landscape has changed for good, and alternative financing methods have captured much attention, with giants like PayPal stepping in the game.

THE NEXT STEP

As the industry is new, and has lots of challenges, the banking sphere and fintechs are turning to partnerships accelerating online lending to small business members. It makes perfect sense to MCA providers to license their automated platforms, banks, and credit unions. Traditional players are familiar with regulations and have data for fine-tuned underwriting, while fintech providers bring innovative technology and customer experience. “We saw that Canada is ripe for technology but the differences in regulation among other things made us go the partner route,” said Peter Steger, the head of business development at Kabbage, to AltFinanceDaily – a perfect illustration of the growing partnership trend. These mutual interests create a lot of business opportunities, and that’s a good sign for all parties involved.

When small business owners need financing, timing is essential. Small and medium businesses are vital to the Canadian economy, so for them, the proper financial support means fast and convenient access to credit. In the new fintech-driven reality, applications should be completed within thirty minutes, decisions made within hours, and funds deposited in the applicant’s bank account within days. Canadian small businesses contribute around 30% of the total GDP, so the need for simple finance is acute. The technology has already made small business lending more accessible, and over time, financing alternatives such as MCA will become mainstream.

GoDaddy Now Offers Kabbage Business Lines of Credit To Its Customers

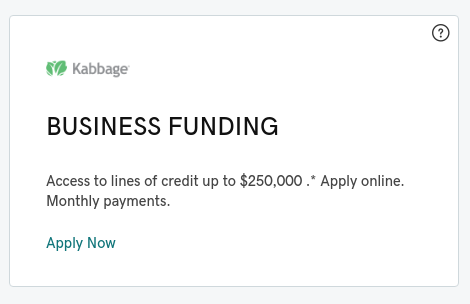

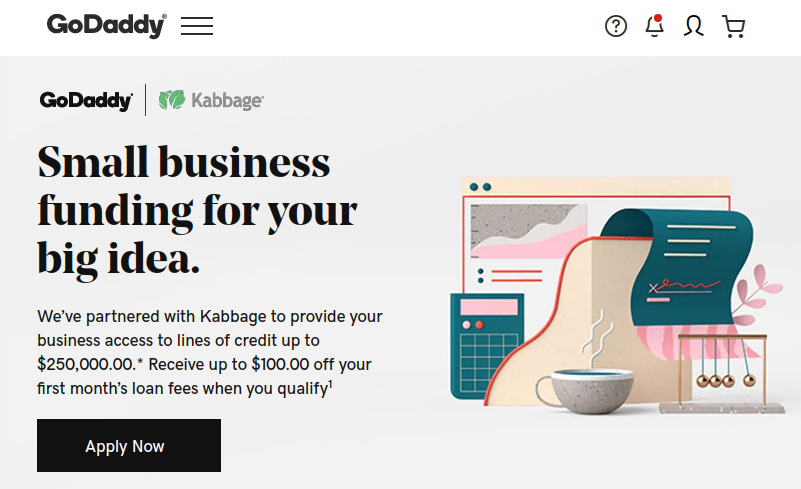

November 4, 2019 A curious thing popped up in my Godaddy account dashboard on Monday. Underneath the section to manage my domains, a “Deals from GoDaddy Partners” box offered me $300 in Free Yelp Ads on one side and a business line of credit from Kabbage up to $250,000 on the other.

A curious thing popped up in my Godaddy account dashboard on Monday. Underneath the section to manage my domains, a “Deals from GoDaddy Partners” box offered me $300 in Free Yelp Ads on one side and a business line of credit from Kabbage up to $250,000 on the other.

The Kabbage offer is brand new, according to a joint announcement that came out the same day publicizing a “strategic partnership” between the two companies.

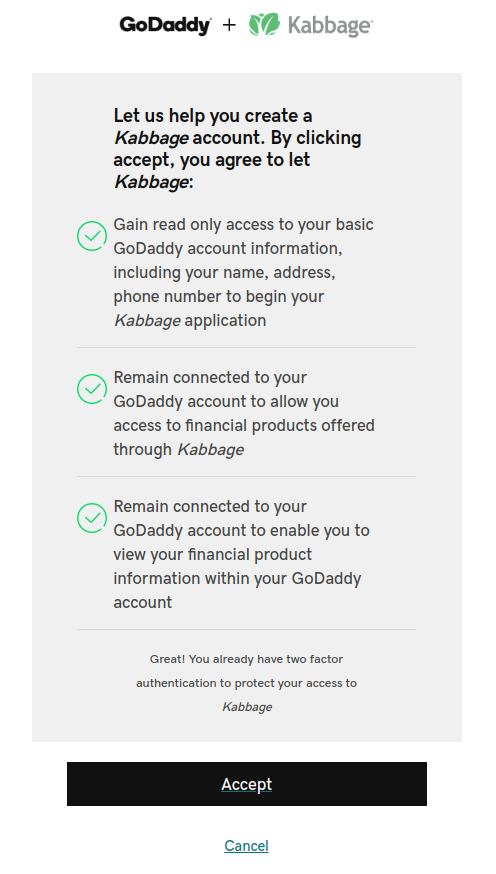

By clicking on it, I found that GoDaddy customers can transmit their account information to Kabbage by clicking a button to begin the loan application process. If a loan is approved, GoDaddy customers save up to $100 on their first monthly loan fee, the website states.

While a simple web domain may only cost around $10 a year, Kabbage has suggested that funds be used for other purposes like staffing up for the busy holiday season, purchasing additional inventory or equipment, or applying it toward digital marketing initiatives.

Borrowers will be able to access the Kabbage dashboard from their Godaddy accounts, an FAQ says.

Below are some screenshots:

Strategic Funding Source Announces Launch of New Brand Identity; Unites its Funding Arm and Servicing Arm Under the name Kapitus

January 15, 2019New York, NY – January 15, 2019 – Strategic Funding Source, a veteran of the small and medium-sized business alternative lending space, today announced the launch of a new corporate brand identity, including a new name. As part of this rebrand, the funding division and servicing division will be united under the name Kapitus. The unification of these two divisions will allow for an improved experience for both clients and partners.

Since its inception in 2006, Strategic Funding Source has provided over $2 billion to almost 40,000 businesses in hundreds of industries across the U.S. Over the past two years, the organization has been proactively building out its executive team, bringing in a wealth of experience to transform its risk model, underwriting processes, lending capacity and product line, technology capabilities and customer experience.

With these and other planned advancements, the company required a new brand that better reflected the company’s commitment to be a reliable source of capital to all small and mid-sized business owners.

“The small business lending landscape is consolidating around a few strong and reputable companies. Over the last several years, Kapitus has experienced tremendous growth both in its product offerings to small and medium-sized businesses and in the total number of businesses it serves” said Andy Reiser, CEO of Kapitus. “We chose a name and identity that represents our strength and stability as well as our promise to be a responsible and fair source of capital to small and medium-sized businesses nationwide.”

Along with the name change there will be a new logo, tagline (“Let’s Grow Together”) and domain name (kapitus.com). The rebrand is the first step in the company’s strategy to grow its own financing product line, add to its marketplace of 3rd party lenders and create a foundation for new partnership opportunities. The new brand also represents the company’s commitment to keep the human touch throughout the financing process, while improving customer experience through technology to aid the decisioning process and improve speed to funding.

“This is an exciting change for us,” added Reiser. “This new branding builds upon our history and pays allegiance to our standing as a leader in a fast-evolving industry, opening the door for future opportunities for us, our clients and our partners.”

About Kapitus

Founded in 2006 and headquartered in NYC, Kapitus is one of the most reliable and respected names in small business financing. As both a direct lender and a marketplace built with a trusted network of lending partners, Kapitus is able to provide small businesses the financing they need, when and how it is needed. With one application business owners can save time and money, while eliminating the stress that comes with applying to different lenders. At Kapitus, we believe that business owners should be able to focus on running their business, while we take care of the financing. To learn more, visit www.kapitus.com.

Lending Club Stock Price Hits Record Low

February 27, 2018Lending Club’s stock dropped to its lowest level on Monday, closing at $3.27, according to the online lending tracker. That puts the company down 78% from its IPO price of $15 and down 87% from its all-time high.

Since going public, the company has been mired in litigation, losses, and scandal. The company has also put funding from peers aside in favor of funding from Wall Street banks.

Worse yet though for the company is that competitors like Goldman Sachs have been able to undercut Lending Club’s rates (Goldman Sachs’ Marcus charges no late fees or origination fees), while simultaneously tapping into a cheaper cost of capital (deposits).

Will 2018 Be a Special Year?

December 29, 2017 2018 is going to be different, in a good way. That’s word on the street in the alternative finance industry, many of whom have told me that it’s just something they feel.

2018 is going to be different, in a good way. That’s word on the street in the alternative finance industry, many of whom have told me that it’s just something they feel.

I feel it too. The S&P 500 is at an all-time high, Bitcoin is up more than 1,400% for the year, lenders are lending in full force, and on top of it all, Donald Trump is president. The world is changing and from a one thousand foot view, it’s an exciting time for finance.

2018 will welcome Broker Fair, the inaugural conference for MCA and business loan brokers.

2018 will transform alternative finance into just finance. For example, a mailer I received from PayPal advertising a small business loan up to $500,000 in as quick as 1 business day, included a letter signed by a top manager of Swift Capital. PayPal acquired Swift in 2017. Yesterday’s alternative loan is simply today’s loan. The one-day small business loan is becoming normalized and being offered by widely recognized financial companies.

Ripple surpassed Ethereum this morning to become the 2nd largest cryptocurrency by market cap. Cryptocurrency, once the domain of Bitcoin-obsessed internet anarchists, is quickly being adopted by the world’s largest banks.

It’s one thing to just talk about innovations in finance and another to realize that you now rely on those innovations. My company got a loan from Square, I got insurance through CoverWallet, I have funds in Lending Club, Prosper, Bitcoin, Ethereum, and Bitcoin Cash. Coinbase is the new etrade. MCA and online business loans are the new community banks. Payments can be made instantly and cost effectively.

2018 will be special because the world that we predicted would come, has come. That means it will be time to think about what will come even next. Online lending has come, instant payments has come, cryptocurrency is fast approaching. What will be the cool edgy hip thing in the ’20s that we may once again refer to as alternative? Mull that one over for a bit and consider that in the next decade the sexy fintech companies of the 20-teens will be stodgy financial institutions in the 2020s. This decade’s innovation will become part of the boring normal manner in which finance is transacted. That’s a fact.

Enjoy 2018. I know I will.

Happy new year,

– Sean

Reaction to Lending Club’s New Credit Model

September 13, 2017The few retail investors discussing the recent change Lending Club made to their credit model weren’t exactly optimistic, according to comments on the Lend Academy forum. Of particular concern is grade inflation wherein borrowers who previously scored a C or lower may now find themselves in the A or B category.

“We expect loan volume to shift toward higher quality grades (grades A and B) because some borrowers will qualify for lower interest rates under the new model,” Lending Club stated in an email last week.

Retail investor sentiment may not be all that important, however, as capital from self-managed accounts on the platform has waned after peaking in the first quarter of 2016. In Q2 of 2017, self-managed accounts only accounted for 13% of the capital used to fund loans. The majority came from banks and institutions.

Lending Club: Charge-offs will happen

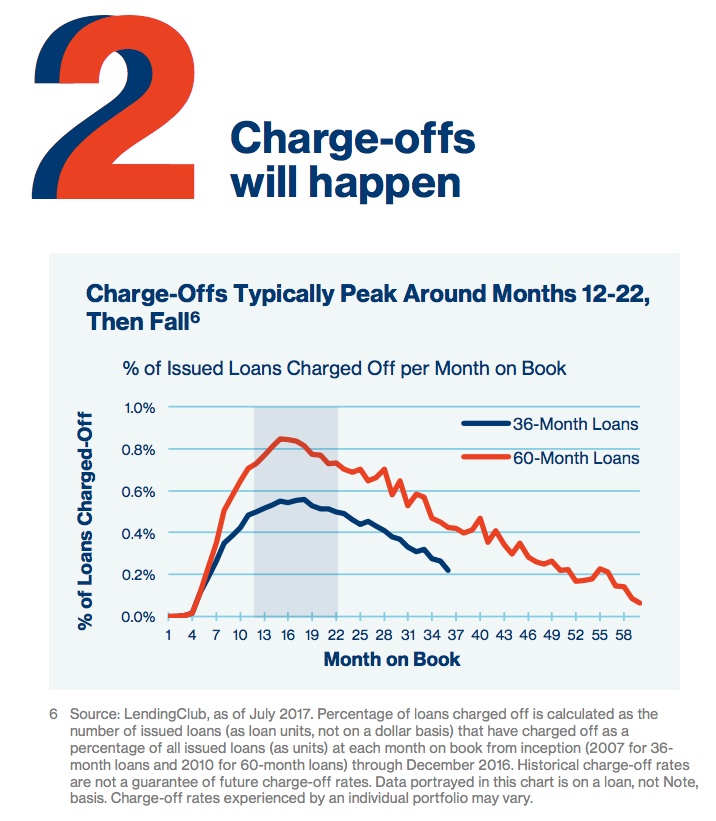

August 16, 2017 A short guide that Lending Club circulated to retail investors yesterday offers them five key pieces of advice.

A short guide that Lending Club circulated to retail investors yesterday offers them five key pieces of advice.

1. Focus on net returns

2. Charge-offs will happen

3. Diversification is key

4. Monthly payments include principal and interest

5. Reinvestment is critical for consistent returns

Lending Club has gradually drawn more attention to the effect of prepayments on loans and this guide is no different.

“Prepayments impact returns because they reduce the amount of principal earning interest from Notes. A Note is considered prepaid when the dollar amount received is greater than the amount due for any given month,” they say. “It is inevitable that certain loans will charge-off or prepay and result in a loss of investment capital.”

Not mentioned however is that investors are charged a 1% fee on all outstanding principal if a borrower pays off their entire loan early despite it being no fault of the investor. And investors are less likely to monitor the impact of these fees if they keep reinvesting their cash which of course Lending Club advises investors to do.

The guide is still helpful in setting expectations for retail investors who ignored or did not understand all the fine print when they signed up. Quoted below about charge-offs:

“It’s inevitable that some borrowers will get behind on their loan payments. Some of these borrowers will get back on track and others will stop repaying their loans. After it’s clear that a borrower won’t make any more payments a loan is considered ‘charged-off.’ All investors in consumer credit experience some charge-offs, so it’s important to understand them and consider how they might impact your investment strategy.”

Overall, the guide is a nice way of keeping retail investors engaged. As someone who invested on the platform for a few years, one of the biggest disappointments I found was that the platform did not feel like a “club” at all. There was no sense of peer community and there was almost no communication whatsoever from Lending Club about anything other than requests to deposit more money.

But lately, peer funding has been dropping off the platform after reaching an all time high back in the first quarter of 2016. In Q2 of this year, only 13% of loans were funded by peers. 44% of loans were funded by banks. Maybe they’re not entirely ready to see individuals disappear completely or maybe they just want those that remain to keep the faith as returns slide. Hopefully, they continue to supply interesting and helpful materials in the future.