The End of an Era

September 19, 2012It’s the end of an era. Sound ominous for a blog that reports on the Merchant Cash Advance (MCA) industry? It shouldn’t. In the last 10 years, MCA firms played in the minor leagues. No one was really paying attention to them and truthfully, a lot of critics didn’t think this business model would still be around. But today it still stands, funders are still funding, and this blog is practically struggling to keep up with the incredible amount of action that is taking place. Coincidentally, 2012 marks the end of the Mayan Calendar. Yes, it’s the end of an era.

MCA Goes From 0 to 60

There were a few big firms in the Mid-2000s (RapidAdvance, Merchant Cash and Capital, Strategic Funding Source, AdvanceMe, etc.) and they’ve all experienced modest success. It was “modest” in the sense that it is nothing compared to today’s standards. The level of play is changing. Wining and dining an Independent Sales Office (ISO) that could bring in $300,000 a month in deal flow used to be all the rage. 300k for one company was 300k less for a competitor. An extra point of commission here or a freebie approval there was enough to make you the big dog in town, at least for awhile. Despite all the supposed innovation and growth, the talent pool remained the same. Lead generators became agents, agents became ISOs, ISOs became syndication partners, syndication partners became funders, and funders became technology companies that were basically clearing houses for groups of funders. If the industry was Sally, Joe, and Tom in 2005, it was still Sally, Joe, and Tom in early 2011, just with new company names or titles. Then everything changed…

Money poured in:

Merchant Cash and Capital Announces $25 Million in new financing 10/4/11

Snap Advances raises $3 Million from TAB bank 11/21/11

Capital Access Network raises $30 Million 2/7/12

RapidAdvance Receives new financing facility through Wells Fargo 4/2/12

1st Merchant Funding | $5 Million re-discount line of credit from TAB bank 6/12

Strategic Funding Source secures $27 million 6/27/12

On Deck Capital raises $100 Million 8/23/12

Kabbage raises $30 Million 9/17/12

Industry insiders loosely redefined what a Merchant Cash Advance was:

Merchant Cash Advance Redefined Merchant Processing Resource 3/25/12

Big companies entered the market:

American Express Announces Their Own Merchant Cash Advance Program 9/22/11

PayPal Pilots Merchant Cash Advance Program in the U.K. 7/13/12

Some funders became licensed lenders in major states such as California:

A New Chapter Opens for Merchant Cash Advance The Green Sheet 6/25/12

Search the California licensed lender registry

New products formed:

FundersCloud creates platform to raise capital and find syndicate partners faster 8/29/12

A charity announces a new way to make subsidized business loans using the split-funding method 9/6/12

These barely scratch the surface of industry events. What used to be a competition to score the local neighborhood ISO has morphed into a race to be the first to partner up with Facebook, twitter, Groupon, and Square. Anyone not moving full speed ahead to integrate technology and social media will be gone in the next 24 months.

May 18, 2012 was the first time we noticed and commented on what was happening. In How The Facebook IPO Affects the Merchant Cash Advance Industry, venture capitalists and Silicon Valley had finally found MCA and there’s no hiding from them. Now it seems all of our far-fetched predictions are not only coming true, they’re happening moments after we predict them. In our last article we instructed everyone to keep their eyes on Kabbage. Six days later they announced they had raised $30 million in new financing and would be expanding overseas. For a company that makes wild claims about the correlation of facebook fans with account performance, all while humorously being named after a boring vegetable, they sure seem perfectly able to threaten the status quo. Nobody dared touch Ebay or Amazon businesses until they came around.

Price

On the cost basis front, the middle ground is eroding even further. We first discussed this phenomenon on April 25, 2011 in The Fork in the Merchant Cash Advance Road. In it, we explained that the combination of competition and defaults were placing downward pressure and upward pressure on price at the same time. Today, there is surging demand for “starter deals” at 1.49 factors that are payable over 3 months at the same time that more and more new lenders are offering 1 year loans at 10%. The low rate, 12-18 month term deals are nothing new. A few funders tried them in the past and most suffered irrecoverable consequences. This is history that the new players didn’t witness.

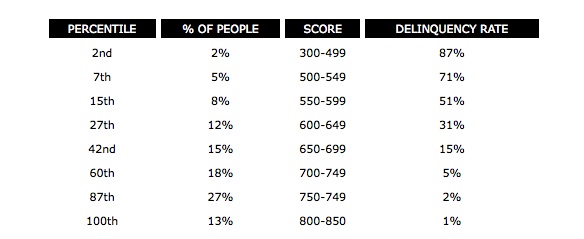

Some outsiders view the MCA industry as a bunch of Wall Street guys that got fat, happy, and disincentivized to lower costs. On the contrary, one only needs to take a single look at this chart to realize that undercutting the entire market isn’t so genius after all. How can a funder survive with extremely low margins when 15% – 71% of their target market is likely to experience problems repaying their loans? These aren’t our stats, these are FICO’s:

Veteran industry insiders know this and acknowledge that the coming tide of low rate financing is a bubble that has burst before. On the DailyFunder, a few folks have offered this insight:

The mca/unsecured loan biz is very risky. It’s all fun and games till deals start going south. My guess is they either adjust rates to match defaults or go out of business. I know first hand that this is not a get rich quick business. It may look like it is from the outside but once you are inside you see the world differently pretty quickly.

[these new low rate deals are] just like On Deck did. When they first came out, they offered 12 month 1.09’s. Then it dropped to 6 month 1.12’s, then 1.18’s. Now you see 1.25’s to 1.35’s offered by them

Governance

On the other side of the cost war is potential federal regulation. At least one D.C. consulting firm is prodding the leaders of the MCA industry to take a proactive approach on self-governance. According to Magnolia Strategic Partners, MCA is on the radar of regulators and members of congress, especially in light of the Dodd-Frank Wall Street Reform and Consumer Protection Act. The new MCA playing field has invited media attention, and not all of it is positive.

The North American Merchant Advance Association is the only organization for industry cooperation but their ability to dictate policies and standards is weak. They receive very little press and their website has been down for weeks. Many argue that they have been effective in minimizing defaults by sharing data on fraudsters. While this does stand to serve the community, it is but a footnote in their orignal intended purpose.

New Barriers to Entry

For the first time ever, potential resellers are facing barriers to entry. Becoming an ISO has long been as simple as owning a phone and purchasing a list of businesses that have used MCA financing before. Today, it’s not that easy. These lists have been sold literally hundreds of times over and called tens of thousands of times over. Pay-Per-Click marketing is dominated by the million and billion dollar firms with money to burn. If John Doe ISO wants to advertise on Google, he better be prepared to compete with the likes of American Express and Wells Fargo. Good luck! Putting skin in the game has also become more of a prerequisite for ISOs to succeed. Funders want to know if a sales agent would put his or her own money into a deal… and then actually commit them to doing just that. The odds are becoming stacked against the undercapitalized and it isn’t likely to change.

In 2009, the most prevalent pitch used by sales agents was to inform prospects that they themselves were “a direct lender” and that anyone else the prospect might be talking to was a broker. “Cut out the middleman and go direct with us,” they’d convincingly argue. This line became less effective when prospects heard this from all five agents they spoke to. Name dropping strategic partnerships will be the new way to build credibility. “We’re partnered with Facebook, twitter, Groupon, and Square,” a sales agent will soon be saying. “Can our competitors make the same claims? Go with us.”

See You On the Other Side

See You On the Other Side

2013 will kick off a single elimination tournament. Funders that didn’t realize 2012 was the end of an era will begin to fade. 2014 will eliminate the weaker firms that remain and by 2015, Merchant Cash Advance will no longer be a term that anyone uses. Big banks and billion dollar technology companies will go on to rebrand all that which the funding warriors of the last decade have worked so hard to establish. MCA will simply assimilate into other financial products. The metaphorical Sally, Joe, and Tom will probably still be in the business, but be working for companies like Capital One, Wells Fargo, and American Express. And as for us…well… we’re going to need something else to talk about. But we’ll keep you posted until that day. 🙂

– Merchant Processing Resource

../../

The Bubble That Wasn’t

August 17, 2012“The smaller the loan, the more likely a lender will deny it. The denial rate for applications for small loans (less than $100,000) was more than twice as high as it was for bigger loans.”

– CNNMoney 8/16/12

In early 2009, a very wise friend of mine gave me a bit of advice. As an ex-stock broker who made his fortune in the 80s, he’d seen his fair share of bubbles. And so he bestowed upon me his wisdom that the Merchant Cash Advance (MCA) industry’s days were numbered. “It’s got 6-8 months left of life in it and then it’ll go away. Everyone’s in freakout mode right now but things will go right back to the way they were and banks will push you right out of a job,” he lectured me. My expression didn’t change, for he wasn’t the first one to sing me this cautionary tale. He continued on, “You’re a nice guy so I suggest in the next few months, you go out and get into another line of work. You can always look at this experience as a wild ride but MCA is a fringe industry borne out of the financial crisis.” I thanked him for looking out for me and went home that night to mull over what he and a few others had been saying.

No one wants to believe their thriving business is part of a bubble that will inevitably burst. But at the same time, no one wants to later on be perceived as that naive fool that couldn’t see an obvious end coming either. And while the career itself seemed honorable and sustainable (helping small businesses get financing), there were a lot of pivotal moments along the way that made me think for a second that at any day I could be told to pack up my stuff and go home because there was suddenly no more demand for MCA.

No one wants to believe their thriving business is part of a bubble that will inevitably burst. But at the same time, no one wants to later on be perceived as that naive fool that couldn’t see an obvious end coming either. And while the career itself seemed honorable and sustainable (helping small businesses get financing), there were a lot of pivotal moments along the way that made me think for a second that at any day I could be told to pack up my stuff and go home because there was suddenly no more demand for MCA.

I am reminded of the time when a Craigslist Ad was answered by over 500 recently laid off mortgage brokers and underwriters. Some had literally been hired to underwrite mortgages, only to be told days later that their division was closing down. Similarly, there were hot shots from the payday loan industry who stopped by to learn what our business was all about. These people looked like they had been punched in the gut and told stories of major success followed by unforeseen ruin as states legislated them out of business overnight. And still others had the mentality that MCA was a get rich quick scheme and went on to run their own funding companies or brokerage offices into the ground within a matter of months. They cursed the MCA gods and the bubble they believed they were a victim of, ignoring the reality that they had poorly managed themselves into oblivion.

As the 6 to 8 month timeline for destruction expired and the light shone on those still standing, I realized I had made the right choice by sticking it out. MCA was not a progeny of the financial meltdown. Heck, the product itself had already been around since the late 1990s and had gained significant popularity around 2005 when other players began entering the market. It also had none of the trademark signs of a bubble. If financing businesses was a bubble, there would be no such thing as banks today. Business financing has been around for literally thousands of years. MCA firms just catered to the ones that banks ignored and by 2008 that included nearly every small business in the country. One could argue that the growth rate of MCA would eventually slow down, supporting the claim with the same wisdom I had heard nearly a year before, that everything would return to “normal.”

Today’s world is anything but the world of yesterday. The unemployment rate in July was 8.3% and according to a survey reported by CNN, “[Today], the option most often sought by businesses — opening a new credit line — face[s] the lowest approval rate at 13%” Banks never did return to their old ways, nor does it seem likely that they will any time soon. Those that doubted MCA’s longevity in 2009, including those who left the industry altogether back then in fear, did not foresee the many roads of evolution that would allow it to thrive.

Years ago, an MCA was easily defined as a purchase of future sales that would ideally be completed in 6 to 9 months. Virtually every provider offered identical terms and costs, which stymied competition and eventually created stereotypes that would come to haunt the image of MCA for quite some time. For a while, America had a hard time envisioning MCA as anything but a 1.38 factor rate that was available to those that fit a certain credit criteria and processed a minimum amount of credit card sales monthly. So imagine the shock some small business owners felt when approved by RapidAdvance, a veteran MCA firm, for a ::gasp:: small business loan. A loan?! could it be? Yes, MCA has been semantically broadened to include many forms of short term lending. And then there’s Florida based Merchant Cash Group that became famous with their Fast Funding program, a financing option for businesses that fell outside the box for traditional MCAs. Some companies don’t even require businesses to accept credit cards as a form of payment. “Credit card sales? Who cares how much they’re doing in credit card sales?!” Would you ever imagine an MCA rep making such a statement in 2009?

MCA is still widely considered to be tied to credit card processing and it doesn’t ever need to officially evolve away from that. Withholding a percentage of sales directly from a payment processor is what initially allowed the many business owners that were horrible at making monthly payments suddenly eligible to receive capital. But for all the changes that have been applied to the financing product itself, something has changed with the companies offering it as well.

Competitors used to be ultra secretive about their practices. An MCA firm could be underwriting an application that another MCA firm funded the day before. Sure, the merchant wasn’t supposed to hop around and do this with more than one company at a time, but the other firm wouldn’t even confirm if they funded them if you asked. One of the great failures of the past was the lack of cooperation amongst the players in the industry. An ‘every man for himself’ mentality hurt more than it helped in a business that was struggling to create its identity in the mainstream world of finance. The North American Merchant Advance Association (NAMAA) sought to correct that through data sharing and the promotion of common standards. Some of the major members have years of experience under their belt including Merchant Cash and Capital, Strategic Funding Source, RapidAdvance, and Merchant Cash Group. These firms have been around the block and back. “MCA bubble? What bubble?,” they’ll say with 100% confidence in their tone.

So why a boring history lesson on MCA today? It’s only fitting on the day that CNN declared the bursting of the social media bubble, that I re-visit a decision I made 3 years ago. “I’m just looking out for you kid,” a mentor once told me. Bad advice for sure. This year, I am noticing many people that left MCA years ago are coming back. After so much time has passed, they are STILL getting in early on something that’s going to be huge, rather than coming back to ‘manage the decay’ (did I just take a swipe at Obama?!). VCs are having a field day trying to get in on it. Accel Partners recently forged an equity deal with Capital Access Network with the ultimate goal of what I’m guessing is to one day go public.

So why a boring history lesson on MCA today? It’s only fitting on the day that CNN declared the bursting of the social media bubble, that I re-visit a decision I made 3 years ago. “I’m just looking out for you kid,” a mentor once told me. Bad advice for sure. This year, I am noticing many people that left MCA years ago are coming back. After so much time has passed, they are STILL getting in early on something that’s going to be huge, rather than coming back to ‘manage the decay’ (did I just take a swipe at Obama?!). VCs are having a field day trying to get in on it. Accel Partners recently forged an equity deal with Capital Access Network with the ultimate goal of what I’m guessing is to one day go public.

The only things bubbly in MCA these days are the excited account reps, underwriters, and support staff that are working to get America’s small businesses humming again. Some have taken to wearing their FUNDED pants 7 days a week. I know I have practically worn mine out.

I’m always struck now by the college grads that ask me if this business is sustainable. Their anxious parents are worried sick that their babies are going to be caught up in some bubble and be out of a job 6 to 8 months from now. To this I offer a few words of wisdom. “Providing small businesses with capital isn’t going away anytime soon. Sure, the product might evolve and the economy will change, but the fundamental demand for short term financing is here to stay. You seem like nice parents so I’d hate to see your kid get involved in some other industry at the end of its life cycle. He or She is getting in early on something big, something long lasting, something that has become a permanent staple of the American financial system.” Good advice for sure.

By: Sean Murray

Founder of Merchant Processing Resource (../../)

Began career in the MCA industry in August, 2006

P.S.

The FUNDED pants do exist and were created by Next Level Funding in early 2010.

The SEO War for ‘Merchant Cash Advance’

February 12, 2012 Let’s admit it, we’re all at war. If you’ve uttered the terms Panda, PageRank, Backlinks, or Organic in the last few months, you know what we’re talking about. We didn’t choose this fight, Google forced it upon us. And so after a long day of phone calls and handshakes about affordable working capital, we return to our homes at night and search the web. Not for information of course, but to find out where our company website pops up when we Google the phrase: Merchant Cash Advance or other relevant terms. Today we ask, is the fighting worth it?

Let’s admit it, we’re all at war. If you’ve uttered the terms Panda, PageRank, Backlinks, or Organic in the last few months, you know what we’re talking about. We didn’t choose this fight, Google forced it upon us. And so after a long day of phone calls and handshakes about affordable working capital, we return to our homes at night and search the web. Not for information of course, but to find out where our company website pops up when we Google the phrase: Merchant Cash Advance or other relevant terms. Today we ask, is the fighting worth it?

In 2007, back when the industry hadn’t put much thought into the Internet, the #1 search result for Merchant Cash Advance was the blog by David Goldin, the CEO of Amerimerchant. It made sense because it was a self proclaimed “online resource dedicated to the merchant cash advance industry.” There, small business owners and competitors could read about the trials and tribulations of an industry on the verge of explosive growth. It was interesting, it was informative, and best of all, he ranked first without trying.

Nowadays, it’s all commercial. Merchant Cash Advance companies with fat advertising budgets are spending thousands to rank for their favorite keywords, with Merchant Cash Advance still high on that list. The friendly information resource has been replaced by a website that not only crushed the competition in search positioning but seems to publicly brag about it too.

As we write this article, the top 10 Google search results for Merchant Cash Advance are:

1. Merchant Cash in Advance

2. YellowStone Capital

3. Entrust Cash Advance

4. Merchants Capital Access

5. Merchant Resources International

6. American Finance Solutions

7. Nations Advance

8. Bankcard Funding

9. Rapid Capital Funding

10. Paramount Merchant Funding

Do keep in mind that your results may differ slightly depending on your region. Google geographically targets searchers to bring them the most relevant matches.

How much is the #1 spot worth? The market priced it at $75,000 three months ago when MerchantCashinAdvance.com was sold in an online auction for that amount (saved in pdf). So which powerful Merchant Cash Advance company unloaded their precious website? None. The owner of the site was actually an SEO guru looking to make a quick buck. He studied the industry a bit and then within two months ranked a site at the top of Google.

75k might even be considered a steal, as we were actually approached to purchase that website ourselves in August 2011. The exchange was a bit contentious, with them being unwilling to accept less than $200,000 and us making an insulting offer of $100. Perhaps it was jealousy or perhaps it was because we didn’t realize how a Merchant Cash Advance website could be worth so much, but the discussion quickly degraded into name calling and we never spoke again.

How many small businesses are searching for Merchant Cash Advance anyway? According to Google, there are 14,800 searches for it a month. We assume that at least 75% of those are from the companies offering it. You probably Google the phrases several times a day yourself. Admit it!

The real money is in the long tail keywords, since merchants are more likely to personalize their search. Being first for merchant loan for bad credit might be more potent than Merchant Cash Advance. It’s tough to say since AltFinanceDaily doesn’t really rank for either of those. Then again, we’re an information destination, much like David Goldin’s Blog was/is.

We’re not SEO experts, but we do quite alright with Google ourselves. Without giving away all of them, this is our current placement for just the following keywords:

- Merchant Cash Advance directory: 1, 2

- Largest Merchant Cash Advance companies: 1

- Merchant Cash Advance UCC: 1, 2, 3

- Merchant Cash Advance statistics: 1

- Merchant Cash Advance stats: 1, 2

- Merchant Cash Advance default: 1, 2

- Merchant Cash Advance UCCs: 2, 3, 4, 5

- Merchant Cash Advance laws: 2

- Merchant Cash Advance forums: 2

- Merchant Cash Advance articles: 3

- Merchant Processing: 3

- Merchant Cash Advance Jobs: 8

- Sell your mom for cash: 1 (don’t ask)

MerchantCashinAdvance.com was no different and they claimed to be #1 for over 300 business lending related keywords. A spreadsheet of the analysis they put up during the auction can be found here.

With nothing more than an organic search presence, they claimed to have had the following results:

Month of July for 2011: Received 647 calls & 148 online business lending applications: Funded 81 deals, $26,000.00 profit.

Month of August for 2011: Received 731 calls & 234 online business lending applications: Funded 113 deals, $29,500.00 profit.

Month of September 2011: Received 1026 calls & 276 online business lending applications: Funded 147 deals, $41,750.00 profit.

If that’s the case, then $75,000 was a bargain. That no doubt led to the auction of a similar site just a month later. MerchantCashAdvances.org is currently ranking 51st for Merchant Cash Advance. They claimed to earn $12,500 annually in ad revenue and $200,000 in commissions. The starting bid was $10,000 and although there were many inquiries, it didn’t sell.

That doesn’t mean it wasn’t worth the price. Most Merchant Cash Advance companies are secretly or not-so-secretly investing thousands into SEO campaigns. Black hat SEO is rampant and even the most reputable companies have engaged in it at some point. The underwriting room is the one they show their clients. The sales floor is the one they show their new recruits. But ask where the internet marketing room is, and they’ll claim it doesn’t exist. But it does of course. They’re usually small quarters with no windows that are filled with computers armed with software like ScrapeBox, Article Marketing Robot (AMR), XRumer, and a list of working proxies.

Even the white hats are building backlinks manually and creating endless articles for use on their own company blogs or for services like BuildMyRank. One moderately sized Merchant Cash Advance company in New York City has just as many SEO employees as they do sales representatives. For some, this is just the beginning. It’s not unusual to spend $10,000 – $20,000 a month on pay-per-click campaigns.

The Internet has become a place where the person with the most to spend wins. Because of competition, a paid Google campaign for Merchant Cash Advance keywords can cost $20 per click! We did a phone call with Google and were told that less than 10% of clickthroughs convert into a sale or completed form. If only 1 out of every 10 visitors calls or inquires through the site, that amounts to $200 for a single lead. If only 1 out of every 5 of those leads turn into a closed deal, the acquisition cost is effectively $1,000. That number is awful especially considering commissions and factor rates have been rapidly declining over the last year. And merchants wonder why this financing is more expensive than a bank loan…

It also explains why the practice of closing costs and service fees have survived internal industry scrutiny. Some resellers would be operating in the red without them. Organic traffic is in essence free, that is if you don’t consider the salary or fees you pay your SEO team. Hopefully they don’t overdo it and place your site in the Google sandbox. Until then, the rewards outweigh the risks and every day the industry pushes the envelope a little further in the quest to rank on page 1.

If you can earn $200,000 a year from a website or sell one for $75,000 after two months of work, then there is plenty of room for growth. If the industry was saturated, it wouldn’t be that easy. If your mother is getting into the Merchant Cash Advance business, make sure she knows how to market her website. It’s a war out there.

– AltFinanceDaily

../../

New York Funding Race 2010

October 8, 2010

New York State ranks in the top 5 for Merchant Cash Advance volume. We checked with the Secretary of state to find out just how many deals had been done in NY this year so far. Here is what we found:

1/1/2010 through 9/30/2010

- AdvanceMe 163 deals

- Merchant Cash and Capital 144 deals

- First Funds 120 deals

- Strategic Funding Source 50 deals

- 1st Merchant Funding 40 deals

- Merchants Capital Access 36 deals

- Business Financial Services 31 deals

- AmeriMerchant 31 deals

- Max Advance 21 deals

- Capital For Merchants 20 deals

- RapidAdvance 17 deals (don’t always file UCCs)

- Snap Advances 14 deals

- Sterling Funding 13 deals

- Greystone Business Resources 12 deals

- American Finance Solutions 12 deals

- Bankcard Funding 10 deals

- GRP Funding 9 deals (don’t always file UCCs)

- Merchant Capital Source 7 deals

- Centerboard Funding 2 deals

- The Business Backer 0 deals