Bizfi Secures $65 Million in Financing

December 15, 2015NEW YORK–(BUSINESS WIRE)–Bizfi (www.bizfi.com), the premier FinTech company whose online small business finance platform combines aggregation, funding and a participation marketplace, announced that Metropolitan Equity Partners (“Metropolitan”) has provided a structured financing facility of $65 million to the company to drive growth.

Closing this financing round enables Bizfi to:

- Expand its suite of funding programs, increasing its ability to fund America’s small business capital needs.

Increase the speed at which funding applicants access direct financing from Bizfi. - Develop and implement a national marketing campaign designed to increase the awareness of the Bizfi brand and platform within the small to medium-sized business community.

- Bizfi and its proprietary marketplace and funding technologies have provided in excess of $1.3 billion in financing to over 26,000 small businesses across the United States since 2005. Since Bizfi launched its aggregation platform in 2015, the Company has experienced 72% growth in year-over-year gross originations.

“The Bizfi platform is the simplest, fastest and most frictionless process for small businesses to access funding. Metropolitan’s financing will propel our growth plans to the next stage,” said Stephen Sheinbaum, founder of Bizfi. “Every day more and more businesses are turning to Bizfi because of our strong channel partners, enabling business owners to compare all their funding options in one place. The Metropolitan partnership provides Bizfi with additional capital to develop new products and fund more small businesses from its own branded product set.”

Metropolitan’s investment provides the financial flexibility and strength to support Bizfi’s growth plans. The new investment expands upon Metropolitan’s prior involvement as an active buyer of loan participations and a mezzanine lender to the Company for the past three years.

Bizfi’s proprietary technology and aggregation platform efficiently gathers applicant information from a wide variety of sources to quickly offer commercial funding products including loans and other capital products to small businesses. Bizfi’s technology is further strengthened by strategic relationships with more than 45 funding partners, including OnDeck, Funding Circle, IMCA Capital, Bluevine and Kabbage. Bizfi also participates as a lender on the platform. Regardless of what kind of capital is sought from any of the funding partners, the small business owner is guided through the entire process by a Bizfi funding concierge that is assigned specifically to him or her.

Paul Lisiak, managing partner of Metropolitan Equity Partners stated, “Metropolitan believes that the future of small business lending is being built by Bizfi. Their aggregation and direct lending marketplace is disrupting the fast growing FinTech industry. Our new investment is the result of the impressive performance we have directly experienced as a lender and participant in the company’s financing products over the past three years. In the rapidly evolving FinTech space, Bizfi’s management team has elegantly expanded their product offerings to create a platform that holistically meets the dynamic funding needs of small businesses. We look forward to being a part of Bizfi as they further solidify their position as a leader in the financial technology space.”

Metropolitan has been an active investor in the alternative lending and FinTech space with over $100 million committed in 2015 including investments in JH Capital Group, Debt Away, New Credit America and PledgeCap.

Mr. Sheinbaum concluded, “Bizfi has seen radical growth over the last 18 months. Not only have we developed one of the most robust FinTech platforms for the small business lending space, but we have cultivated significant deals with third party companies that service small businesses. These companies will utilize white label versions of Bizfi’s platform to offer financing to their clients. Now, with the Metropolitan financing supporting our growth, we can continue to expand our products, increase our market share and provide solutions to the critical financing needs of the companies that fuel our economy.”

About Bizfi

Bizfi, is the premier FinTech company combining aggregation, funding and a participation marketplace on a single platform for small businesses. Founded in 2005, Bizfi and its family of companies have provided more than $1.3 billion in financing to over 26,000 small businesses in a wide variety of industries across the United States.

Bizfi’s connected marketplace instantly provides multiple funding options to businesses from more than 45 funding partners and real-time pre-approvals. Bizfi’s funding options include short-term financing, medical financing, lines of credit, equipment financing, invoice financing, medium-term loans and long-term loans guaranteed by the U.S. Small Business Administration. The Bizfi API provides a turnkey white label or co-branded solution that easily allows strategic partners to access the Bizfi engine and present their clients with financial offers from Bizfi lenders all while maintaining their customer’s user experience. A process that once took hours, now takes minutes.

About Metropolitan Equity Partners

Metropolitan Equity Partners Management, LLC is an alternative investment manager that provides expansion capital to growing private companies via collateralized loan structures. Metropolitan was founded by Paul Lisiak who has 20 years of experience investing in private U.S companies through both debt and equity. Metropolitan traces its roots to a successful equity strategy managed by the current Metropolitan Principals which was backed by the Man Group plc. Since 2008, Metropolitan has committed over $300MM in collateralized debt investments through call funds, blind pools and institutional managed accounts. Metropolitan is based in New York City.

Contacts

KCSA Strategic Communications

Abbie Sheridan, 212-896-1207

asheridan@kcsa.com

or

Kenneth Cousins, 212-896-1254

kcousins@kcsa.com

or

Bizfi Sales:

855-462-4934

bizfisales@bizfi.com

or

Bizfi Marketing:

212-545-3182

marketing@bizfi.com

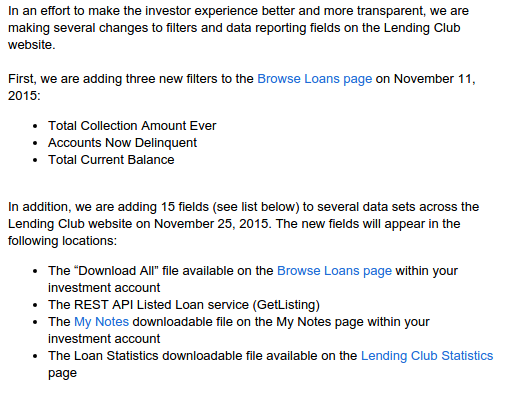

Lending Club Narrowly Avoids Major Transparency Flop

November 18, 2015After many months of Lending Club warning that they would be REMOVING borrower credit data from note listings, they have completely reversed course and ADDED fifteen new credit attributes. On Peter Renton’s LendAcademy forum, one member speculated that this move was made to compete with Prosper for the attention of institutional investors. If true, that would be entirely misguided.

Almost exactly one year ago, Lending Club announced that they were cutting the amount of data points available to investors from 100 to 56. Renton, a marketplace lending evangelist and founder of the LendIt conference, gave it a negative spin in his blog:

It is pretty obvious by now that I don’t like these changes. For quite some time now Lending Club has been reducing the amount of transparency for investors. Now, some changes I completely understood such as removing the Q&A with borrowers and even the removal of loan descriptions. But removing data that investors have been using to make investment decisions is a step too far in my opinion.

I think Lending Club need to ask themselves if they are a true marketplace connecting borrowers and investors in a transparent fashion or whether they are more of a loan origination platform that makes products available to investors. They are certainly moving more towards the latter, I think, and that is a shame for everyone.

The move was seen by many as a way to stop investors from trying to reverse engineer their models and beat their grading system for above average yields. While understanding that perspective, it is mind boggling that they had planned to remove more data points and make the loans on the platform even less transparent. And here’s why…

Lending Club is a key signatory to the Small Business Borrower’s Bill of Rights, a group of political activists that claim innovative small business lending can only achieve its potential “if it is built on transparency, fairness, and putting the rights of borrowers at the center of the lending process.” With transparency being a focal point of their agenda there, one might find their attempts to reduce disclosure and eradicate transparency a bit hypocritical.

Lending Club is a key signatory to the Small Business Borrower’s Bill of Rights, a group of political activists that claim innovative small business lending can only achieve its potential “if it is built on transparency, fairness, and putting the rights of borrowers at the center of the lending process.” With transparency being a focal point of their agenda there, one might find their attempts to reduce disclosure and eradicate transparency a bit hypocritical.

Investors on Renton’s forum who had for months anticipated Lending Club to remove more data points, also viewed it negatively. “I’d have to think hard on whether to continue investing in LC notes without those credit fields — it would be very much like gambling rather than investing,” wrote Fred back on July 8th.

A similarly named user, Fred93, communicated that these data points were all investors had to go off. “We can’t shake a borrower’s hand, feel the firmness of his grip, the sweatiness of his palm. We can’t look a borrower in the eye. We live or die by a handful of numbers, which we hope mean something, on the average,” he wrote.

Clearly some investors weren’t thrilled with the proposed changes. All the while, Lending Club’s co-signatories had been promoting the transparency pledge through speeches, TV appearances, public relation events, and press releases. To be fair, The Small Business Borrowers Bill of Rights is aimed at transparency between business borrowers and sources offering business financing. Lending Club’s planned removal of data was targeted at investors in their consumer notes. It sounds different enough until you consider that 72% of Lending Club’s loans originated in 2014 were funded by investors vastly less sophisticated than the commercial businesses they have pledged to protect. That’s because that money came from consumers, many of whom are unaccredited and went through no screening process. Instead, these investors are presented with a prospectus as if they were buying a stock or bond and stuck with the risk whether they understand it all or not.

These consumers who are legally presumed to be unsophisticated are the very same people that Lending Club planned to reduce disclosures to, all the while heavily promoting to them that they roll over their retirement savings onto their platform. That logic is the very definition of insanity. Obfuscating the reasoning behind certain scoring grades to these investing consumers would be nothing short of unconscionable and would reasonably invalidate any pledge they’ve made towards transparency in other areas.

Lending Club has for now avoided a major flop by reversing course after having added 15 new pieces of data for investors.

While some investors speculated the move had to do with pressure from Lending Club’s institutional investor base. The more likely reason is increasing scrutiny from federal regulators. Less than two weeks ago for example, the FDIC warned banks about marketplace lending and advised them to perform their own underwriting on the loans they buy and not to rely on originator scoring models. A summary of their letter specifically said:

Some institutions are relying on lead or originating institutions and nonbank third parties to perform risk management functions when purchasing: loans and loan participations, including out-of territory loans; loans to industries or loan types unfamiliar to the bank; leveraged loans; unsecured loans; or loans underwritten using proprietary models.

Institutions should underwrite and administer loan and loan participation purchases as if the loans were originated by the purchasing institution. This includes understanding the loan type, the obligor’s market and industry, and the credit models relied on to make credit decisions.

Before purchasing a loan or participation or entering into a third-party arrangement to purchase or participate in loans, financial institutions should:

– ensure that loan policies address such purchases,

– understand the terms and limitations of agreements,

– perform appropriate due diligence, and

– obtain necessary board or committee approvals.

These guidelines conflict with Lending Club’s long sought after goal of getting investors to trust their A-G scoring grades. The banking regulator is advising banks to basically disregard them. “The institution should perform a sufficient level of analysis to determine whether the loans or participations purchased are consistent with the board’s risk appetite and comply with loan policy guidelines prior to committing funds, and on an ongoing basis,” the more complete memo reads. “This assessment and determination should not be contracted out to a third party.”

A law firm with specialized knowledge of the industry, criticized the FDIC’s move when they wrote on their website, “Ironically, given the Treasury Department’s recent request for information, which supported marketplace lending and focused in part on how the federal government could be supportive of the innovations in marketplace lending, we now have a federal banking agency that is creating roadblocks to having banks participate in this dynamic and rapidly growing space.”

Asking banks not to rely on marketplace scoring models alone hardly seems like a roadblock, especially when the models are tucked away in algorithmic obscurity, have hardly been around for very long, and would decide the fate of depositor money. And if this directive indeed contributed to Lending Club’s transparency reversal, then it couldn’t have been any more well-timed.

Asking banks not to rely on marketplace scoring models alone hardly seems like a roadblock, especially when the models are tucked away in algorithmic obscurity, have hardly been around for very long, and would decide the fate of depositor money. And if this directive indeed contributed to Lending Club’s transparency reversal, then it couldn’t have been any more well-timed.

Whether or not the added data points will make any difference to the performance of investment portfolios is irrelevant. If unaccredited investors and/or depositor money are the source of marketplace loan funding, then Lending Club has a responsibility to disclose as much as possible, no matter how little value they believe certain pieces of information are worth. The 15 additional points are a welcome announcement. The question going forward should be, what else can they disclose?

As a company that pledged so strongly to protect corporations from transparency issues in the developing commercial finance market, they should be trying twice as hard to protect the unsophisticated consumers that invest in the loans they approve and make available for investing. Some of these consumers are prodded into putting their retirement funds on the platform and we all know some people will irresponsibly place their entire retirement portfolio in it. The “Number of credit union trades” a borrower has might not unlock the secret to better investing performance but if it’s something Lending Club knows, the investing public deserves to know it too, if only in the name of transparency which they have so committed themselves to uphold…

Federal Reserve Governor Lael Brainard Speaks About Alternative Lenders

October 4, 2015Federal Reserve Governor Lael Brainard gave the September 30th closing keynote address at the Community Banking in the 21st Century 2015 Conference and here are some of the highlights of what she had to say about online lenders and merchant cash advances:

The data that are available suggest that the various types of online alternative lenders have captured a small but rapidly growing share of lending since the financial crisis. In aggregate, the outstanding portfolio balances of these lenders have doubled every year since the mid-2000s. It is estimated that online alternative lenders originated $12 billion in 2014, with unsecured consumer loans representing $7 billion and small business loans accounting for approximately $5 billion.13 While this amount represents only a small fraction of U.S. unsecured consumer and small business lending overall, the rate of growth is notable.

Although rates vary by platform and borrower characteristics, when taking into account origination fees and repayment periods, the average annual cost of borrowing, or APR, associated with loans and credit products offered by online alternative small business lenders tend to be higher than those associated with traditional bank products. Reports suggest that some borrowers are willing to pay a higher price in exchange for an easy application process, a quick decision, and rapid availability of funds.

While some see online alternative lenders as a disruptive threat to traditional lenders, banks increasingly are finding ways to partner with online alternative lenders, including through loan purchases and referral agreements. Loan purchases by community banks of loans originated by online alternative lenders have been focused on unsecured consumer debt. As the percentage of unsecured consumer debt outstanding held by community banks has been declining in recent years, several banks have partnered with online alternative lenders to grow and diversify their portfolios of unsecured consumer debt.

In contrast to the consumer loan activity, the small business partnerships that have developed so far are largely fee-based referral partnerships. In these partnerships, banks refer to online alternative lenders some of their small business customers who are usually seeking loan amounts that the referring banks may see as too costly to underwrite and service, particularly in the size range below $100,000.

Across the Federal Reserve System, we are actively following developments in the alternative online lending space and have engaged with several alternative online lenders over the past few years to learn more about the industry, the technology, and the business models as well as engaging with bankers to understand how these developments are affecting their markets.Most recently, several alternative lenders have participated in events where we have joined with community development finance experts to discuss ways to adopt platform lending technology to better serve low- and moderate-income borrowers and small business owners.

We want to better understand the opportunities presented by technological advances that may bring new data to bear and help lenders make available credit to a more diverse set of small business borrowers. In some cases, partnerships between community banks and online platforms may help expand access to credit for consumers and small businesses, and help banks retain and grow their customer base.

As regulators, we also want to help the various stakeholders anticipate and carefully manage the associated risks. Of course, third-party and vendor risks are factors that banks should always take into account when introducing new products and services. Taking the time to identify and mitigate risks is a prudent step that banks can take to avoid unintended consequences when entering into partnership agreements with alternative online lenders. In addition, banks should consider whether the partnerships provide new opportunities to diversify their portfolios if they are purchasing loans, and whether the partnerships provide opportunities to offer new products that are a good strategic fit for their bank and their customers.

It is also important for banks to carefully consider regulatory compliance. When purchasing consumer loans originated by online alternative lenders, banks should examine whether fair lending or unfair or deceptive acts or practices issues result from the origination and underwriting methods used by online alternative lenders. To the extent that the underlying algorithms used for credit decisionmaking use nontraditional data sources, it will be important to ensure that this does not lead to disparate treatment or have a disparate impact on a prohibited basis.

Aside from these risks, banks should consider a variety of others, including the implications of credit risk stemming from the purchase of loans and reputational risk if referrals to online alternative lending platforms end badly.

The risks I have described so far have primarily been from the perspective of banks considering partnerships with online alternative lenders. Another important set of concerns are focused on the small business borrowers who may be considering online alternative loans. Some have raised concerns about the high APRs associated with some online alternative lending products. Others have raised concerns about the risk that some small business borrowers may have difficulty fully understanding the terms of the various loan products or the risk of becoming trapped in layered debt that poses risks to the survival of their businesses. Some industry participants have recently proposed that online lenders follow a voluntary set of guidelines designed to standardize best practices and mitigate these risks. It is too soon to determine whether such efforts of industry participants to self-police will be sufficient. Even with these efforts, some have suggested a need for regulators to take a more active role in defining and enforcing standards that apply more broadly in this sector.

Alternative Fintech Pioneer Merchant Cash and Capital Transforms into Bizfi

September 15, 2015NEW YORK–(BUSINESS WIRE)–Merchant Cash and Capital, one of the pioneers in the alternative finance space, announced today that MCC has transformed into Bizfi, an online lending and aggregation platform. Due to the success of Bizfi.com, launched earlier this year, Merchant Cash and Capital is completing its operational and brand metamorphosis in a way that better reflects the Company’s commitment to financial technology. The name change is a consideration of the Company’s rapid growth – in the second quarter of 2015 alone, the Company provided $115 million to more than 3,000 small business owners – as well as its online expansion.

Bizfi’s aggregation platform provides small businesses access to products from more than 35 funding partners including OnDeck, Funding Circle, CAN Capital, IMCA, Bluevine, Kabbage, and SBA lender SmartBiz. Bizfi, which is also a direct lender on the platform, can finance a small business owner in as little as 24 hours. It is the only funding platform that allows a business owner to go directly to contract online.

“Since the launch of Bizfi.com, we have received an overwhelming response from both business owners and funding partners,” said Stephen Sheinbaum, Founder of Bizfi. Bizfi and its family of companies over the past two years has doubled originations to fund more than 25,000 small businesses totaling $1.3 billion. Sheinbaum continued, “Bizfi stands at the nexus of alternative finance and financial technology. With Merchant Cash and Capital becoming Bizfi, we will provide fast and unparalleled funding options to businesses across all types of sectors in the United States and internationally.”

With 80 percent of small business owners today turning online to search for financing, and 66 percent making loan applications after traditional banking hours, Bizfi is positioned to be the leader in the future of small business financing. Bizfi offers a range of funding options including short-term funding, medium term-loans, SBA loans, equipment financing, invoice financing, medical financing, lines of credit, and franchise financing.

Mr. Sheinbaum concluded, “The marketplace for business funding has changed dramatically throughout the ten years that we have been in the industry. We are continuing to grow, adapt and combine our deep expertise with cutting-edge technology to meet the needs of small business owners around the country.”

About Bizfi

Bizfi.com is the premier alternative finance company combining both aggregation and funding on one platform with proprietary technology and unmatched customer service. Bizfi’s connected marketplace instantly provides multiple funding options to businesses with a wide variety of funding partners and real-time approvals. Bizfi.com’s funding options include short-term financing, franchise funding, equipment financing and invoice financing, medium-term loans and long-term loans guaranteed by the U.S. Small Business Administration. A process that once took hours, now takes minutes.

Formerly Merchant Cash and Capital, Bizfi and its proprietary marketplace and funding technologies have provided more than $1.3 billion in financing to over 25,000 small businesses across the United States since 2005. Businesses across all industries and sectors have received funding through Bizfi, including restaurants, retailers, health service providers, franchises, automotive service shops and many others.

Alternative Funding: Over The Top Down Under

September 2, 2015 San Francisco had its gold rush, Oklahoma had its land rush and now Australia is experiencing a rush of alternative funding. After a slow start a few years ago, foreign and domestic companies have been flocking to the market down under in the last 18 months.

San Francisco had its gold rush, Oklahoma had its land rush and now Australia is experiencing a rush of alternative funding. After a slow start a few years ago, foreign and domestic companies have been flocking to the market down under in the last 18 months.

As many as 20 new alt-funders are doing business in Australia, but that number could swell to a hundred, said Beau Bertoli, joint CEO of Prospa, a Sydney-based alternative funder. “The market in Australia has been very ripe for alternative finance,” Bertoli, said. “We see an opportunity for the alternative finance segment to be more dominant in Australia than it is in America.”

Recent entrants to the embryotic Australian market include Spotcap, a Berlin-based company partly funded by Germany’s Rocket Internet; Australia’s Kikka Capital, which gets tech backing from U.S.-based Kabbage; America’s Ondeck, which is working with MYOB, a software company; Moula, which began offering funding this year but considers itself ahead of the curve because it formed two years ago; and PayPal, the giant American payments company.

The new entrants are joining ‘pioneers’ that have been around a few years, like Prospa, which has been working for three years with New York-based Strategic Funding Source, and Capify (formerly AUSvance until it was consolidated into the international brand Capify), which came to market in 2008 with merchant cash advances and started offering small-business loans in 2012.

Some don’t take the newcomers that seriously. “There are small players I’ve never heard of,” said John de Bree, managing director of Capify’s Sydney-based office, in a reference to local Australian funders. “The big ones like OnDeck and Kabbage don’t have the local experience.”

But many players view the influx as a good sign. “I think it’s an endorsement of the market,” Bertoli said. “There’s more publicity and more credibility for what we’re doing here in terms of alternative finance.” It’s like the merchant who gets more business when a competing store opens across the street.

Besides, the market remains far from crowded. “I’m not concerned about the arrival of OnDeck and Kabbage because it really does validate our model,” maintained Aris Allegos, who serves as Moula CEO and cofounded the company with Andrew Watt.

The market’s relatively small size – at least compared to the U.S. – doesn’t seem to bother players accustomed to the heavily populated U.S., a development some observers didn’t expect. “I’m very surprised,” de Bree said of the American interest in Australia. “The American market’s 15 times the size of ours.”

Others see nothing but potential in Australia. “This is a market that will evolve over time, and we think the opportunity is enormous,” said Lachlan Heussler, managing director of Spotcap Australia.

Some view the Australian rush to alternative finance not so much as a solitary phenomenon but instead as part of a worldwide explosion of interest in the segment, driven by banks’ reluctance to provide loans since the financial crisis, de Bree said.

Viewed independently or in a larger context, the flurry of activity in Australia is new. “The boom is probably only getting started,” Bertoli maintained in a reference to the Australian market. “Right now, it’s about getting the foundation of the market established.”

To get the business underway in Australia, alternative funders are alerting small-business owners and the media to the fact that alternative funding is becoming available and teaching them how it works, de Bree said. “Half of our job is educating the market,” noted Heussler.

New players are building the track record they need to bring down the cost of funds, according to Allegos. “Our base rate is 2 percent or 3 percent higher than yours,” he said, adding that the cost of funds is more challenging than gearing up the tech side of the business.

Although the alternative-lending business started later in Australia than in the United States and lags behind America in in exposure, it’s maturing rapidly, said de Bree. Aussie funders are benefitting from the lessons their counterparts have learned in the U.S., he said.

But the exchange of information flows both ways. Kabbage, for example, chose to enter the Australian market with a local partner, Kikka. Kabbage learned from its earlier foray into the United Kingdom that it makes sense to work with colleagues who understand the local regulatory system and culture, said Pete Steger, head of business development for Atlanta-based Kabbage.

But the exchange of information flows both ways. Kabbage, for example, chose to enter the Australian market with a local partner, Kikka. Kabbage learned from its earlier foray into the United Kingdom that it makes sense to work with colleagues who understand the local regulatory system and culture, said Pete Steger, head of business development for Atlanta-based Kabbage.

Such differences mean that risk-assessment platforms that work in the United States or Europe require localization before they can perform effectively in Australia, sources said.

Sydney-based Prospa, for example, got its start three years ago and has been working ever since with New York-based Strategic Funding Source to localize the SFS American risk-assessment platform for Australia, said Bertoli, who shares the company CEO title with Greg Moshal.

Moula, which has headquarters in Melbourne, sees so many differences among markets that it decided to build its own local platform from scratch, according to Allegos.

One key difference between the two markets is that Australia does not have positive credit reporting. “We have nothing that even comes close to a FICO score,” said Allegos. The only credit reporting centers on negative events, he said.

Without credit scores from credit bureaus, funders base their assessments of credit worthiness largely on transaction history. “It’s cash-flow analytics,” said Allegos. “It’s no different from the analysis you’re doing in your part of the world, but it becomes more significant” in the absence of positive credit reporting, he said.

Australia lacks credit scores at least partly because the country’s four main banks control most of the financial sector and choose not to release credit information, sources said. The banks have warded off attacks from all over the world because the regulatory environment supports them and because their management understands how to communicate with and sell to Australian customers, sources said.

The big banks – Commonwealth Bank, Westpac, Australia and New Zealand Banking Group, and National Australia Bank – set their own rules and have kept money tight by requiring secured loans and long waiting periods, Bertoli said. It’s difficult for merchants who don’t fit into a “particular box” to procure funding, he maintained. “It’s almost like an oligarchy,” Allegos said of the banks’ grip on the financial system.

Eventually, the banks may form partnerships with alternative lenders, but that day won’t come soon, in Allegos’ estimation. It could be 12 months or more away, he said.

Even as the financial system evolves, deep-seated differences will remain between Australia and the U.S. Most Americans and Australians speak English and share many views and values, but the cultures of the two countries differ greatly in ways that affect marketing, Bertoli said. “In your face” advertising that can work well with “loud, confident” Americans can offend the more “laid-back” Australian consumers and business owners, he said.

Australians have become tech-savvy and comfortable with online banking, but they guard their privacy and often hesitate to reveal their banking information to a funding company, Allegos said. The entrance of OnDeck and Kabbage should help familiarize potential customers with the practice of sharing data, he predicted.

Cost structures for businesses differ in Australia from the U.S., Bertoli noted. Australian companies pay higher rent and have to pay minimum wages set much higher than in the United States, he said. Published reports set the Australian minimum wage at $13.66 U.S. dollars. The higher costs down under can take a toll on cash flow. “Take an American scorecard and apply it to Australia?” Bertoli asked rhetorically. “You just can’t.”

Distribution’s not the same for commercial enterprises in the two countries, Bertoli maintained. Despite having about the same geographic area as America’s 48 contiguous states, Australia has a population of 23 million, compared with America’s 322 million.

Distribution’s not the same for commercial enterprises in the two countries, Bertoli maintained. Despite having about the same geographic area as America’s 48 contiguous states, Australia has a population of 23 million, compared with America’s 322 million.

No matter how many people are involved, changing their habits takes time. Australian merchants prefer fixed-term loans or lines of credits instead of merchant cash advances, Bertoli said. In many cases Australian merchants simply aren’t as familiar as Americans are with advances, Allegos said.

Besides, the four big banks in Australia tend to solicit merchants for credit and debit card transactions without the help of the independent sales organizations and sales agents. In the U.S., ISOs and agents play an important role in explaining and promoting advances to merchants, Bertoli said. Advances make sense for merchants because advances adjust to cash flow, and they help funders control risk, but just haven’t caught on in Australia, Bertoli said. Australians resist advances if too many fees are attached, said Allegos.

Pledging a portion of daily card receipts might seem too frequent, too, he said. Besides, advances are limited to merchants who accept debit and credit cards, while any business could conceivably choose to take out a loan, said de Bree.

Advances have to compete with inventory factoring, which has become a massive business in Australia, according to Heussler. The business can become intrusive because funders may have to examine balance sheets and talk to customers, he said.

Australia’s reluctance to turn to advances, leaves most alternative funders promoting loans and lines of credit. Prospa, for example, uses some brokers to that end but also relies on online connections, direct contact with customers, and referrals from companies that buy and sell with small and medium-sized businesses.

“Anyone that touches a small business is a potential partner,” said Heussler, including finance brokers, accountants, lawyers and even credit unions, which have the distribution but not the product.

Moula finds that most of its business comes from well-established companies and that loans average just over $27,000 in U.S. currency and they offer loans of up to more than $77,000 U.S. The company offers straight-line, six- to 12-month amortizing loans.

Using a model that differs from what’s common in the U.S., Moula charges 1 percent every two weeks, collects payments every two weeks and charges no additional fees, Allegos said. A $10,000 (Australian) loan for six months would accrue $714 (Australian) in interest, he noted.

Spotcap Australia offers a three-month unsecured line of credit and doesn’t charge customers for setting it up, Heussler said. If the business owner decided to draw down, it turns into a six-month amortizing business loan for up to $100,000 Australian. Rates vary according to risk, starting at half a percent per month but averaging 1.5% per month.

Spotcap Australia offers a three-month unsecured line of credit and doesn’t charge customers for setting it up, Heussler said. If the business owner decided to draw down, it turns into a six-month amortizing business loan for up to $100,000 Australian. Rates vary according to risk, starting at half a percent per month but averaging 1.5% per month.

If companies have all of the necessary information at hand, they can complete an application in 10 minutes, Allegos said. Moula has to research some applications offline if the company’s structure deviates too greatly from the usual examples – much the same as in the U.S., he maintained. The latter requires strong customer-service departments, he said.

Kikka uses a platform based on the Kabbage model, which gives 95 percent of customers a 100-percent automated experience, Steger said. “It goes to show the power of our automation, our algorithms and our platform,” he maintained.

Spotcap prefers to deal with businesses that have been operating for at least six months, Heusler said. The funder examines records for Australia’s value-added tax and other financials, and it likes to connect with the merchant’s bank account. Spotcap can usually gain access to the account information through cloud-based accounting systems and thus doesn’t require most companies to download a lot of financial documents, he noted.

Despite the differences between the two countries, banking regulations bear similarities in Australia and the United States, sources said. In both nations the government tries harder to protect consumers than businesses because they assume business owners are more financially savvy. For consumers, regulators scrutinize length of term and pricing, sources said, and on the commercial side the government is concerned about money laundering and privacy.

Regulation of commercial funding will probably intensify, however, to ward off predatory lending, Bertoli said. Government will consult with businesses before imposing rules, he said. A couple of alternative business funders aren’t transparent with their pricing and they charge several fees – that sort of behavior will encourage regulation, Allegos said.

“I know they’re watching us – and watching us very closely,” he added.

In general, however, the Australian government supports alternative finance, Bertoli said, because they want there to be options other than the four big banks and wants small business to have access to capital. Small businesses account for 46 percent of economic activity in Australia and employ 70 percent of the workforce, he noted, saying that “if small businesses are doing badly, the economy is doing badly.”

Hence the need, many in the industry would say, for more alternative funding options in Australia.

Commission Chargebacks: The Good, the Bad and the Ugly

August 10, 2015 Imagine you’re a 20-something-year-old broker who’s just, in good faith, referred a merchant to a funder. You walk away with a few thousand dollars in your pocket, and you promptly spend it on rent and a celebratory steak dinner. Then all of a sudden…BAM! Just like that the merchant goes belly up and the funder’s knocking on your door to clawback your hard-earned commission money, which, of course, you’ve already spent.

Imagine you’re a 20-something-year-old broker who’s just, in good faith, referred a merchant to a funder. You walk away with a few thousand dollars in your pocket, and you promptly spend it on rent and a celebratory steak dinner. Then all of a sudden…BAM! Just like that the merchant goes belly up and the funder’s knocking on your door to clawback your hard-earned commission money, which, of course, you’ve already spent.

For many brokers, it’s a familiar-sounding story—with an ending they’d like to rewrite. Their thinking goes like this: underwriters, not brokers, are the ones who are supposed to dig into a company’s finances before approving a deal. Underwriters, not brokers, are the ones who make the financial decisions about whether or not a deal can go forward. Therefore, underwriters, not brokers, should be responsible when deals implode.

“There are a lot of people who think there should not be commission clawbacks—that they’re unfair,” says Archie Bengzon, who runs the New York sales office for Miami-based Rapid Capital Funding, a direct funder. Bengzon was previously the president of Merchant Cash Network, an ISO in New York.

While there’s a fair amount of closed-door grousing by brokers, most funders are standing their ground—with only a select few companies kicking these controversial policies to the curb. More commonly, funders claim clawbacks, despite being hated by brokers, are a necessary evil. These funders say that without them, they’d stand to lose too much on bad deals and that they need a way to protect themselves from rogue brokers.

“There is a group of people out there who are trying to game the system,” says industry attorney Paul Rianda, who heads a law firm in Irvine, California.

The Case for Scrapping Clawbacks

Brokers in favor of changing the status quo understand the need to prevent bad apples from smelling up the entire industry. But even so they believe that chargebacks are patently unfair to the honest majority of brokers who often make just enough to scrape by. In most cases, the brokers are typically young—18-to-26-year-olds trying to make money and learn the industry. They don’t have the financial resources that the funders do and the onus shouldn’t be on them if the deal they brought in—with good intentions—goes bust in a short time, according to the owner of a top-tier ISO/Hybrid in Staten Island, New York, who requested his name not be used.

This is especially true in cases where the underwriter took risks they shouldn’t have or decided to fund merchants in cases where they shouldn’t have. “It’s the underwriter’s job to protect the money that their company is lending out,” he says. “[Chargebacks] shouldn’t be going on in this industry.”

One solution might be for more ISOs to stand up to funders and refuse to send them future deals. That’s exactly what the Staten Island executive did a few years ago when a funder he repeatedly worked with tried to claw back his commission on a particular deal. He made a big stink and told them he’d never send them business again. It was enough of a threat to convince the funder to back off. “If more ISOs start saying that…then the funders will start sweating and change their contracts. Because it really isn’t fair,” he says.

For some brokers, however, taking such a strong position with funders is a risky strategy in a cottage industry where all the major players know each other and there’s no shortage of hungry young brokers willing to do business. So while these brokers don’t like losing money, they aren’t necessarily loudly crying foul either.

Matthew Ross, managing member of Go Ahead Funding, a broker and funder in Basalt, Colorado, has been in the business for nine years. He’s only had one commission clawed back once in this time period—it was a commission for $1,500 on a $25,000 deal that went sour within a month, he recalls. He was upset at the time and felt the underwriter should have done more to vet the merchant who went belly up. “Why didn’t the underwriters catch this?” he remembers asking at the time.

Matthew Ross, managing member of Go Ahead Funding, a broker and funder in Basalt, Colorado, has been in the business for nine years. He’s only had one commission clawed back once in this time period—it was a commission for $1,500 on a $25,000 deal that went sour within a month, he recalls. He was upset at the time and felt the underwriter should have done more to vet the merchant who went belly up. “Why didn’t the underwriters catch this?” he remembers asking at the time.

Nonetheless, Ross was a lot calmer than some brokers might have been under the circumstances. For instance, he says he never threatened to stop sending the funder business as many brokers might have done. “I don’t necessary like it, but I understand it. I’m not going to fight it,” he says.

Some brokers are making their displeasure with the practice known by declining to sign contracts that contain clawback clauses. Nathan Abadi, founder and president of Excel Capital Management, a New York-based funder and ISO, says he either refuses to do business outright or he comes to a verbal agreement with a funder that he’ll wait two weeks for payment to make sure the deal has legs. “I meet them in the middle,” he says.

The reason he likes this approach is that it’s more palpable for brokers to lose paper commissions versus actual money that they’ve already been given and possibly spent. Otherwise, as a business owner working with numerous agents, it’s bad for business. “It causes an internal conflict because now you have to penalize the person who’s working for you,” Abadi says.

The Flip Side of the Chargeback Coin

Meanwhile, there’s a whole other camp within alternative funding—including some brokers—who feel chargebacks are important as a fraud-deterrent. Given the fact that the industry is still largely unregulated, many believe that funders need some type of fire retardant to prevent being burned by unscrupulous brokers.

“We think that they serve an important role,” says Stephen Sheinbaum, founder of Merchant Cash and Capital, a New York-based funder. “Most of our stronger referral partners do not object to it. It’s a way of aligning our interests with the sales force.”

About 60 percent of the company’s funding business comes from third-parties including ISOs; its direct sales force accounts for the other 40 percent.

Even some brokers concede that clawbacks can serve a valuable purpose. Sure, it’s aggravating to lose money, but they feel that without clawbacks the industry would be even more of a free-for-all than it already is.

“I can see both sides,” says Bengzon, the funder and broker. Wearing his broker hat, Bengzon has felt the sting of losing a commission once or twice in the 100 or so deals he’s done. But he still understands why funders—who take a big monetary hit when deals go sour—would want to protect themselves and require brokers to have some skin in the game.

“If we’re going to reap the rewards of a nice commission, we should also understand that it can still be taken away if a deal goes bad,” he says.

When he sends leads to funders, Ross of Go Ahead Funding says he does his best to make sure he’s sending only high quality merchants. He tries to vet them upfront—to the limited extent he can—in order to avoid problems later on. Clawback provisions serve as “an incentive for [brokers] to keep their eyes open,” he says.

Know What You’re Signing

About 80 percent of the agreements that come across the desk of Rianda, the industry attorney, have a 30-day clawback provision. But he’s seen some agreements that have longer time frames—60, 90 or even 120 days. Those types of contracts aren’t as common, but they’re out there.

It’s important for brokers to carefully read the fine print of a contract before signing on the dotted line. “It sounds obvious, but a lot of people don’t do that,” says Bengzon.

The shorter the clawback time frame, the less brokers tend to balk. “People don’t want to be paid on a deal and three months later they lose that commission, which they’ve already spent,” he says.

Bengzon believes a clawback that extends any more than a month is excessive. “I would never sign something greater than 30 days,” he says.

According to Sheinbaum of Merchant Cash and Capital, 30 days is an appropriate time frame to help weed out fraud without putting unnecessary burden on brokers who are sending legitimate business. “The purpose of the provision is to try and stop people from committing fraud at the outset,” he says.

According to Sheinbaum of Merchant Cash and Capital, 30 days is an appropriate time frame to help weed out fraud without putting unnecessary burden on brokers who are sending legitimate business. “The purpose of the provision is to try and stop people from committing fraud at the outset,” he says.

David Sederholt, executive vice president and chief operating officer at Strategic Funding Source Inc. in New York, says clawback provisions in the contracts Strategic uses range from 30 to 45 days depending on the contract. He says he understands brokers don’t like them, but that it’s nonetheless important to have the provision in order to protect the funders. “There’s got to be some partnership involved here,” he says.

Clawbacks Not A Free-For-All

Many funders recognize that there’s a fine line between protecting their business and cutting off potential revenue sources.

“You start clawing back commissions on every default, a broker will stop sending business,” says Ross of Go Ahead Funding.

Sheinbaum of Merchant Cash and Capital notes that clawbacks aren’t used as often as some brokers might think. He says out of 800 deals in a 30- or 31-day period, his company enforces its clawback policy only a handful of times each month.

He also points out that while the clawback policy is on the books, Merchant Cash and Capital looks at each situation individually. If it’s clear that the broker tried to defraud the funder, that’s one thing, he says. But, if for instance, a merchant has a heart attack and dies 20 days into a deal and can’t pay back the funds, Merchant Cash and Capital wouldn’t try to clawback the broker’s commission in that situation, he says.

Strategic Funding has only clawed back commissions once or twice in the past nine years, says Sederholt, the EVP.

The company works with a variety of brokers. Some have less than a 1 percent default rate and others have 12 percent to 14 percent default rates. As extra protection with brokers who have bad track records, Strategic Funding either declines to work with them at times, or has in place a stronger underwriting procedure with these deals.

Being more careful upfront is a better tactic than trying to go after commissions, which is extremely hard, Sederholt says.

Changing the Modus Operandi

While it’s not the industry norm, there are a few funders who have stopped using clawbacks, or are considering doing so, given all the headaches they can cause. Isaac D. Stern, chief executive of Yellowstone Capital LLC, a New York-based funder, says his company no longer tries to clawback commissions when deals go bust. The few times they tried to clawback commissions several years back, the brokers they went after were upset and threatened not to do business with them anymore. Yellowstone decided this approach was bad for business and that it would be more prudent to try something else.

“There’s too much competition, and if we were going to do clawbacks it would decimate our business,” he says. “It’s the broker’s job to bring in the deals. It’s our job to underwrite it. If something goes wrong on the deal, that’s on us. It’s not the broker’s fault.”

As protection, the contracts Yellowstone uses with brokers contain a provision allowing it to seek damages when fraud’s alleged. But in cases where brokers send what seems to be a legitimate deal that goes bad for something other than fraud, Yellowstone turns the other cheek. Yellowstone can afford to eat the $5,000 or $6,000 commission to ensure ongoing—and hopefully more positive leads—or so the thinking goes, according to Stern.

Overtime—if peer pressure continues to mount—it’s possible that more even more funders will decide chargebacks just aren’t worth the trouble. “I think the reason why some funders are moving away from [clawbacks] is because people are afraid of losing volume. Once one funder acquiesces, others will follow suit,” says Sheinbaum of Merchant Cash and Capital.

The Rest of the Alternative Lending Industry’s Funding Numbers

July 1, 2015 Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Right after AltFinanceDaily sent the final file off to the printers in May, PayPal announced that the widely circulated $200 million lifetime funding figures were slightly outdated.

How off were they?

Oh, just by about $300 million or so. By May 7th, PayPal’s Working Capital program for small businesses had already exceeded $500 million. The industry leaderboard has been revised to reflect the news. PayPal says they are funding loans at the rate of $2 million per day, which puts them on pace for more than $700 million a year. Um, wow?

One name that’s missing from that list is Amazon, whose secretive short term business loan program is reported to have already generated hundreds of millions of dollars in loans. Given the $300 million discrepancy that PayPal let ruminate for months, we’re in no position to speculate on Amazon. Anyone could try to assess what they’ve been up to however, since they file UCCs on their clients under the secured party name “AMAZON CAPITAL SERVICES, INC.”

Of course if you’re craving specific numbers, an anonymous source inside Yellowstone Capital revealed that Yellowstone produced $35.5 Million worth of deals in the month of June alone. Yellowstone has a strategically diverse business model that allows them to either fund small businesses in-house (essentially on their own balance sheet) or broker them out to other funders. Yellowstone was listed on AltFinanceDaily’s May/June industry leaderboard at $1.1 Billion in lifetime deals and $290 Million in 2014. June’s figures indicate that they are probably well on their way to surpassing last year’s numbers.

Curiously, platform/lender/broker/marketplace company Biz2Credit has been hanging on to the same stodgy old number for more than a year.

Funded over $1.2 billion. 200,000+ happy customers.http://t.co/3h64lI4cgG #smallbusiness #Funding

— Biz2Credit (@biz2credit) June 19, 2015

They were touting that same $1.2 Billion number exactly 1 year ago. Surely they have done more since then? Biz2Credit’s service covers a much wider scope however so a direct comparison with their peers may not be appropriate. A lot of their loans are arranged through traditional banks which are typically transacted in amounts larger than the average $25,000 deal alternative lenders do.

A source familiar with Biz2Credit’s breadth said he observed a deal where the company helped a businessman in Mexico obtain financing to purchase a new helicopter, a transaction which apparently necessitated a team to fly down there to sign paperwork. Definitely not a standard transaction!

When we published the industry leaderboard initially, it admittedly omitted some of the industry’s largest players. Many firms are fairly secretive about the numbers they release and we’re in no position to disclose numbers that aren’t supposed to be public. Below is data that we hadn’t published previously.

The industry’s unsung behemoths

The industry’s unsung behemoths

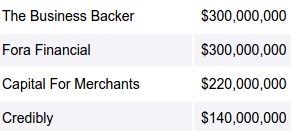

The $300 million lifetime funding figure publicized by NYC-based Fora Financial can’t be that stale. It’s the number currently stated on their website and a late February 2015 company announcement revealed they were only at $295 million at the time. We feel comfortable enough to now have Fora Financial on the leaderboard.

In 2014, Delaware-based Swift Capital revealed that they had funded more than $500 million. It’s unclear how much that’s increased since then.

Credibly (formerly RetailCapital), has publicized that they’ve funded more than $140 million in their lifetime. Founded in Michigan, the company has opened offices in New York, Arizona, and Massachusetts. They’ve been added to the lifetime leaderboard.

New York City-based AmeriMerchant has a claim on their website that they have funded more than $500 million since inception. How much more exactly? We’re not sure.

Coral Springs, FL-based Business Financial Services keeps their figures mostly under wraps but a good guess would place their lifetime figures at somewhere between $700 million and $1.2 billion.

Miami, FL-based 1st Merchant Funding had reportedly funded close to $100 million in the Spring of 2014. It’s uncertain as to where they might be now.

Woodland Hills, CA-based ForwardLine surpassed $250 million in funding as far back as 2013.

Orange, CA-based Quick Bridge Funding disclosed more than $200 million in funding in late 2014.

Troy, MI-based Capital For Merchants has funded $220 million since inception. But there’s more to the story. Capital For Merchants is owned by North American Bancard, a merchant processing firm that acquired another merchant cash advance company, Miami, FL-based Rapid Capital Funding in late 2014. And coincidentally, Rapid Capital Funding had just acquired American Finance Solutions months earlier, which is an Anaheim, CA-based merchant cash advance company that had funded more than $250 million since inception. All told, North American Bancard owns at least three merchant cash advance companies: Capital For Merchants ($220 million), American Finance Solutions ($250 million+), and Rapid Capital Funding (undisclosed). There are rumors that they’re in talks to acquire at least one more company in the space, which, if true, would make North American Bancard one of the industry’s most powerful players.

Don’t bother counting up the above totals

These figures all barely scratch the surface as AltFinanceDaily’s database indicates there are literally hundreds of genuine direct funders in the industry.

Thanks to the company representatives that took the time to confirm their funding numbers with us directly. Anyone interested in sharing their figures can email sean@debanked.com. If there is a gross inaccuracy somewhere as well, please report it to us.

This page might be updated in the future so check back!

Wall Street Has a New Landlord

June 20, 2015 “You stole my deal bro!”

“You stole my deal bro!”

“No I didn’t. The merchant hated your offer,” replies back a 25-year old dressed in a dark pinstripe suit with no tie.

He then takes a pull from his half-smoked cigarette and continues, “The guy wanted 90k and you offered him twenty. I was at least able to get him fifty. What’d you think was going to happen?”

I walk past the two who eye me suspiciously and am quickly out of hearing range of their conversation. They were strangers, but I know exactly what they were talking about. Walking around the neighborhood here, I feel oddly at home.

This is Wall Street, a new stronghold for the small business financing industry. Midtown has traditionally been the epicenter for merchant cash advance companies, but somewhere along the way, new players started opening up their shops in lower Manhattan.

As a born and bred New Yorker, I never really saw a need to visit the actual street of Wall Street. To my knowledge, it was simply emblematic of high finance, not really a physical place anymore.

But earlier this year when I signed a lease at 14 Wall Street, I would be thrust into the middle of America’s biggest breeding ground for financial brokers and learn once and for all that the ebb and flow of Wall Street isn’t exactly gone, just transformed.

From my office up on the 20th floor, I can see into the windows of the top five stories of the New York Stock Exchange building. The floors appear to be set up for traders, with long white continuous desks peppered with large monitors on both sides. Everyone sits and stares intensely at their screens, pressing buttons on their keyboard at rapid fire pace. Nobody runs around screaming orders anymore.

Outside, tour guides tell excited onlookers about the stock exchange’s past. It’s a historical landmark, a place to learn about history, not necessarily witness it. The spirit is still alive though in a zombified made-for-the-cameras kind of way. OnDeck recently kicked off their IPO there and so too did Lending Club.

Outside, tour guides tell excited onlookers about the stock exchange’s past. It’s a historical landmark, a place to learn about history, not necessarily witness it. The spirit is still alive though in a zombified made-for-the-cameras kind of way. OnDeck recently kicked off their IPO there and so too did Lending Club.

While tourists dance around aimlessly and upload photos to facebook to show they were there, men and women in the office floors above them are engaged in a different kind of dance. Packed in elbow to elbow with phones glued to their ears, commercial financing brokers shout large numbers at an accelerated pace.

Often lacking luxury amenities such as windows, brokers on Wall Street are weathering the heat and lack of oxygen to move money to Main Streets all across America.

When they come out for air to breathe, the tourists move out of their way, as if they’ve suddenly become aware that people are actually trying to get some work done down here.

The little strip of Broad Street between Wall Street and Exchange Place is kind of like a schoolyard for the merchant cash advance industry. War stories are exchanged, cigarettes shared and dreams dreamed. One day, I’m going to start my own ISO and I’ll do it differently because…

You can walk in any direction. The industry can be found on Broad Street, William Street, Pine Street, and Broadway. It’s on Water Street, Rector Street, Maiden Lane, and Fulton Street. It extends outward almost infinitely to Midtown, Brooklyn, Queens, Long Island, Staten Island, The Bronx, Westchester, Orange County, and New Jersey.

You can walk in any direction. The industry can be found on Broad Street, William Street, Pine Street, and Broadway. It’s on Water Street, Rector Street, Maiden Lane, and Fulton Street. It extends outward almost infinitely to Midtown, Brooklyn, Queens, Long Island, Staten Island, The Bronx, Westchester, Orange County, and New Jersey.

And while there are hubs in the outer parts, the most unique experience by far is down here on Wall Street, where you’re infinitely more likely to overhear professionals shouting “ACHs” and “stacks” than “puts” and “calls.”

Although the guides teach tourists that Wall Street as they imagined it to be is dead, Wall Street itself can never die.

Every now and then a pedestrian will look up at the offices above and wonder if the magic of fast-talking finance still exists. Is that world gone forever?

Not quite…

The stockbrokers may be gone, but there’s a new landlord. Wall Street belongs to the small business financing industry now.