Alternative Lenders Are Waiting for a Shakeout

October 28, 2015 Back in April at the LendIt conference in New York, the big consensus was that not all underwriting was created equal and therefore several players wouldn’t survive long enough to make it back to LendIt in 2016. Six months later at Money2020 and so far everyone is still standing.

Back in April at the LendIt conference in New York, the big consensus was that not all underwriting was created equal and therefore several players wouldn’t survive long enough to make it back to LendIt in 2016. Six months later at Money2020 and so far everyone is still standing.

Loan terms are getting longer, rates cheaper and the cost to acquire borrowers higher. Somebody has to be feeling the pressure but in a rather benign economic and regulatory environment, it’s clear skies.

Valuations are soaring. SoFi is valued at more than $4 billion and Kabbage at more than $1 billion.

But Robert Greifeld, the CEO of Nasdaq warned attendees about the validity of private market valuations. “A unicorn valuation in private markets could be from just two people,” he said. “whereas public markets could be 200,000 people.” At best he described a private market valuation as being just a rough indicator.

And some wonder if these valuations are based on just scale, rather than the ability to underwrite more intelligently and efficiently than a bank. OnDeck for example, had a Compound Annual Growth Rate (CAGR) in originations of 159% from 2012-2014 when the average originations CAGR for their peers is currently 56%. But OnDeck has the advantage of time. With nearly a decade of data under their belt, they’ve been able to see what works and what doesn’t.

“You have to have enough bad loans to build a good credit model,” said OnDeck CEO Noah Breslow during a Money2020 panel discussion.

For Aaron Vermut, CEO of Prosper, getting their company to the next level was about having access to institutional capital. As a marketplace, and as a company that almost died several years ago, he pointed out, institutional money was the inflection point for them to grow. The peer-to-peer model that actually depended purely on “peers” is what held their company back.

One thing several lenders seemed to agree on was the limited applicability of FICO. FICO is not the thing to use for a small business loan, said Sam Hodges, Managing Director and Co-founder of Funding Circle. His words didn’t come as a surprise since credit scores are generally the domain of consumer lending.

But doubts about FICO’s ability to predict performance didn’t just come from the commercial finance side. Prosper’s Vermut explained that consumers still think their FICO score is the most important factor in the rate they get. So even though they’ve got a system to predict repayment outside of FICO, they’re kind of forced to incorporate it because consumers are being educated to believe that’s what matters most.

The irony was not lost that as Vermut said that on a panel, he was seated next to Kenneth Lin, the CEO and founder of Credit Karma, a company that educates consumers about credit. “A credit score is one of the most important components of a consumer’s financial profile,” says Credit Karma’s website. Such language puts a tech-based lender with their own scoring model perhaps at odds with what their own prospects believe.

For instance if a potential borrower with a 750 FICO score is offered a high interest rate because the lender’s advanced and more in-depth underwriting determined them to be high risk, they’re going to walk away confused.

That of course begs the question, who needs to change? Those educating consumers about credit scores or the lenders who are moving away from them?

Before educational services shift though, it would probably make sense if the lenders can prove that their non-FICO dependent systems will work in the long run. And the sentiment among many lenders is that there are plenty of flawed models out there that will inevitably fail. That makes a shakeout not just a matter of if, but when.

Six months after LendIt, everybody is still standing. Whispers from in and around Money2020’s halls and exhibit floor revealed that the confident lenders wish the correction would happen sooner rather than later but that they are prepared to wait however long it takes.

Right now, confidence about the future on the commercial finance side came in at an 83.7 out of 100, according to the Small Business Financing Report. While there are no other points of reference to compare that to, industry captains are generally very bullish.

That could mean that for those secretly under tremendous pressure already, you could be left waiting for a shakeout for a very long time.

Former SBA Administrator Applauds Growth of Alternative Small Business Lending, Says Loan Brokers are Under Watch by Regulators

October 21, 2015 Former SBA Administrator Karen Mills spoke at the LendIt Europe Conference yesterday. The title of her speech was “The State of Small Business Financing in the U.S.” In her talk, Ms. Mills summarized the negative effects that the last economic recession had on small business lending in the U.S. and how alternative small business lenders have played a large role in countering these effects and expanding access to credit.

Former SBA Administrator Karen Mills spoke at the LendIt Europe Conference yesterday. The title of her speech was “The State of Small Business Financing in the U.S.” In her talk, Ms. Mills summarized the negative effects that the last economic recession had on small business lending in the U.S. and how alternative small business lenders have played a large role in countering these effects and expanding access to credit.

Ms. Mills urged alternative lenders to continue product innovation to meet the varying needs of small business customers. She stated that she believes that product innovation will be a key differentiating factor among industry participants and a critical component of market success. To that end, she echoed the views of many industry commentators that regulators should allow the marketplace to mature and develop before implementing a new regulatory framework.

“I believe this is a nascent market that is serving a need that small businesses have. These entrepreneurs have found a gap in the market and they are filling it in a cost effective way… The industry should get together and the industry should self-regulate.” Ms. Mills stated.

Ms. Mills did note, however, that some regulators are concerned about certain aspects of the small business finance marketplace.

“In the U.S., we’ve seen the rise of the loan broker. This may or may not be good news.” Ms. Mills stated.

She went on to note that loan brokers were a group that were “under some watch” by policymakers. Ms. Mills’ comments are similar to those she made at the LendIt U.S. conference earlier this year but appear to be the first time she has specifically referenced the monitoring of loan broker activity.

Debt Settlement: A Partner to Alternative Lenders?

August 23, 2015 Call it the flip side of the coin, the part of the universe that helps consumers get out of debt, rather than take more on. Debt settlement, as it’s called, has a bit of a murky reputation thanks to a number of unscrupulous players that operated prior to the implementation of the Telemarketing Sales Rule in 2010.

Call it the flip side of the coin, the part of the universe that helps consumers get out of debt, rather than take more on. Debt settlement, as it’s called, has a bit of a murky reputation thanks to a number of unscrupulous players that operated prior to the implementation of the Telemarketing Sales Rule in 2010.

On October 27th, five years ago, for-profit companies that sold debt relief services over the phone could no longer charge a fee before they settled or reduced a customer’s unsecured debt.

“That law forever changed the industry for the better,” said a company representative at National Debt Relief (NDR), a New York City-based debt settlement firm.

Located right in front of the Bull at 11 Broadway, NDR occupies two floors and employs over four hundred people. And while it may seem that their business model is at odds with the dozens of loan brokers that operate in the neighborhood, they’re actually finding ways to work together.

“We’re monetizing their declines,” said a company representative. Indeed, alternative lenders like to talk about the amount of loans they can issue, but thousands of consumers are ultimately declined.

What those consumers do next and where they go is a storyline that doesn’t get much attention. NDR offers to the consumer an alternative route to become debt free in 36 months.

“NDR is enrolling thousands of consumers per month,” said a company representative. The A+ BBB rating and firm regulatory compliance has enabled them to land several strategic partnerships in this industry ranging from merchant cash advance com- panies to peer-to-peer lenders.

“NDR is enrolling thousands of consumers per month,” said a company representative. The A+ BBB rating and firm regulatory compliance has enabled them to land several strategic partnerships in this industry ranging from merchant cash advance com- panies to peer-to-peer lenders.

“We’ve found that 36% of declines from alternative lenders fit our criteria,” said a company representative. Too much debt is one obvious reason that applicants are getting declined from some of these companies in the first place. And to that end, NDR strives to provide them relief. One condition however is that the client not use credit while in the program.

NDR operates in 42 states and requires a minimum of $10,000 of unsecured debt to be eligible. They are also an accredited member of the American Fair Credit Council, a consumer credit advocacy association that touts the strictest code of conduct in the industry.

At the 2015 LendIt Conference in NYC, NDR stood out as a Gold Sponsor.

“Everybody wanted to know what we did,” said Michael Drehwing who was there as the company’s representative. “I told them we want to monetize your declines. How simple is that?”

Addressing Stress and Depression Over Declined Deals

July 29, 2015 I wanted to add to my series discussion by touching on a topic that isn’t often discussed in our space, and it pertains to dealing with depression, stress and other mental health related conditions over the loss of a deal.

I wanted to add to my series discussion by touching on a topic that isn’t often discussed in our space, and it pertains to dealing with depression, stress and other mental health related conditions over the loss of a deal.

Let’s Be Honest

Let’s face it, most of us (as brokers) work on a 100% commission structure, or derive a significant portion of our income from commission, this means that our compensation is based on performance. This performance is directly correlated to the amount of new/renewal business that we fund. The word fund is the keyword here, as your performance in terms of selling might be excellent with the continued production of new leads, new applicants and new interested parties to our industry’s working capital selections. However, if those new leads and applicants don’t fund, then in terms of your performance, they don’t count. An applicant can be declined for a variety of reasons and all of them are usually totally out of your control. However, your compensation is dependent upon your merchant’s approval as well as the offering of terms/conditions that they deem acceptable. This high level of stress can lead to mild bouts of depression, and that depression could lead to a variety of other issues such as overeating, not eating, over sleeping, not sleeping enough, emotional breakdowns, paranoia, personal relationship issues, along with a variety of other inefficiencies.

The Loss Of Hope

Google says that the definition of depression is related to “the feelings of severe despondency and dejection.” Despondency and dejection refers to a state of low spirits caused by the loss of hope, and hope is sometimes all we have as Brokers. All we have going for us is an internal “hope” that our sales abilities will produce the commissions needed to not just cover our business/tax expenses, but cover our personal expenses, insurance, etc., and leave some left-overs to allow us to save for retirement. If you put your soul into this (like I do), then with every funded deal you will rejoice internally, and with every deal declined or approved with terms that are unacceptable to your client, you might feel sudden emotions of panic, fear and uncertainty. As a one man show, I have funded hundreds of deals while also building up a side merchant processing portfolio that processes tens of millions in volume every year. But I have also lost a ton of potential deals on both the funding side and the merchant processing side through declines or approvals that were unacceptable to my client. If left unchecked, still to this day I feel emotions of sickness and depression over declined and lost deals, so much so that sometimes I just have to go home and lay down in the bed for a minute.

Tackling The Stress Through Other Means Of Management

So how do I handle depression and stress over declined and lost deals for the most part? Here are some tips on how I handle the stress and depression of this industry, and perhaps they too can provide some assistance for you in those critical, nerve-racking situations of receiving emails from your Funder with “Declined” or “Application Ineligible” typed out in the Subject Line:

Diversify, Diversify, Diversify

This isn’t just true in Stocks, but it’s also true in being an Independent Agent/Broker. You are a 1099 Independent Sales Office and there’s just no reason why you ought to only be selling one product. Remember as I touched on in prior AltFinanceDaily articles, as a Broker your job is to be as Jeff Thull from Prime Resource Group explains, which is to be a valued source of business advantage for your prospective and current clientele. You should have access to knowledge, resources, networks, products and platforms that your prospective and current clientele lacks access to, allowing them to see you as a “valued extension” of their organization in terms of the value of your expertise and network.

So there’s no reason that you should just be selling Merchant Cash Advances or Alternative Business Loans, you should be selling a variety of other products in various different segments such as POS Systems, Merchant Processing, Equipment Leasing, Insurance, Big Data, Marketing Programs, Cost Reduction Programs, etc., just to name a few.

Do This Because It’s Your Purpose, Not Just For The Money

Listen, I’m not here to convert anybody to any particular Religion, but I believe that if you are going to be an entrepreneur (which is what you are as a 1099 Broker/Agent) then you need to have a very strong internal spirit or soulful foundation. Your motivation, joy, peace and confidence should extend beyond your earthly circumstances. You should see this industry as something you do as a Purpose that aligns with your spirit or soulful foundation, rather than just seeing it solely as a means to make an income.

Continued Learning and Development

The Merchant Services related industry continues to evolve and you should be following all of the trends and updates. The best places to do this for the Merchant Services related industry, is to make sure to follow AltFinanceDaily as well as other sources such as The Green Sheet, Payment Source’s ISO/Agent, The ETA, The SBFA, as well as various industry trade conferences such as LendIt and The AltLend Summit.

Focus On Total Financial Management

Focus On Total Financial Management

Financial management is not just about bringing in decent income, it’s about managing the six pillars of finance which are Income, Investments, Insurance, Credit, Expenses and Taxes.

For example, you might be bringing in $100,000 a year in commissions from your Home Office, but you might be living in a high cost of living area, have horrible spending habits, have inefficient tax reduction strategies, and you have four children from four different women paying very high child support claims. This means that your expenses are too high and your financial efficiency is going to be off.

On the other hand, you might be making $50,000 a year in commissions from your Home Office, with no children, living in a low cost of living area, with efficient budgeting and tax reduction strategies, putting away let’s say $7,500 a year into your retirement accounts. If you do this for 40 years from 25 – 65 for example, with just a conservative 5% per year return, you will have over $1 million at age 65. You will have made yourself a self-made millionaire and you didn’t need a six figure annual commission compensation to do it. All you needed was Total Financial Management.

To Wrap

So in a nutshell, I manage the stress and depression of our industry through having a totally efficiently managed financial system in place, not selling just one product, always learning, and making sure that everything I do is grounded in Purpose. I believe that if you too were to adapt some of these techniques, the loss of that deal you worked so hard on, might not “sting” as bad after all.

Why We Shouldn’t Stop Calling it Peer-to-Peer Lending

June 1, 2015 There’s a troubling undercurrent brewing in the marketplace industry, the death of the word peers. We’re not supposed to say peer-to-peer lending anymore since few platforms actually allow for people to lend directly to their peers. In the case of Lending Club and Prosper, investors are actually lending money to the platforms themselves.

There’s a troubling undercurrent brewing in the marketplace industry, the death of the word peers. We’re not supposed to say peer-to-peer lending anymore since few platforms actually allow for people to lend directly to their peers. In the case of Lending Club and Prosper, investors are actually lending money to the platforms themselves.

Emphasizing the appropriate terminology probably makes it easier for people to understand. If it’s not peer-to-peer after all, then calling it that only serves to mislead potential borrowers and investors alike. And yet the term persists largely because the average person is still able to invest in an asset class it never was able to before, notes backed by the performance of individual consumer loans.

It could be argued that without money from peers to buy these notes, the loans themselves would never get issued, making it still peer-dependent or at least peer-relevant.

A game for Wall Street

Jorge Newberry wrote several months ago that the little guy as most of us imagine a peer to be, is dead. He was replaced by Wall Street, BlackRock, and Wealthy bankers. “These were killers,” He wrote. He added that while the industry “initially attracted ordinary citizens to invest in modestly sized consumer loans to people like them, over the last few years those peer investors often have been elbowed out and replaced by Wall Street’s finest.”

Retail investors have bemoaned the trend via online message boards, sometimes even accusing the platforms of giving the institutions first dibs on the highest quality loans and leaving the little guys to fight over nothing but the scraps that are more likely to underperform.

Even Dara Albright, the co-founder of the LendIt conference has acknowledged the takeover. In The Financial Advisor’s Guide to P2P Investing, Albright writes, “Unfortunately, what began as a true person-to-person marketplace – with the ordinary individuals lending to and borrowing from one another – has since become monopolized by institutional investors whose deep pockets and technological advantages have all but driven the individual lenders out.”

Further along in the paper, Albright makes the case that individuals need to take advantage of the yield these loans offer to narrow the wealth divide. She makes a compelling argument for investing but stops short of proposing a solution to regain market share. “There aren’t enough p2p loans to facilitate the strong investment appetite,” she concluded.

But just as the marketplace community has conceded the death of peers, the numbers don’t exactly reflect their sentiment.

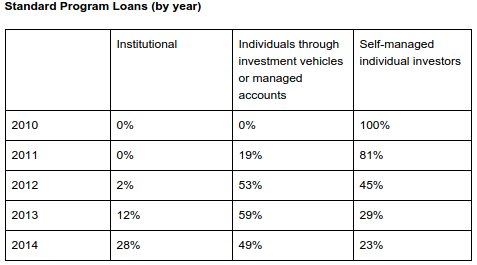

Only 28% of Lending Club’s loans went to institutional investors in 2014.

Only 28% of Lending Club’s loans went to institutional investors in 2014.While Newberry and Albright have made the case that retail investors are being locked out, there’s a dangerous flip side, they just might be getting locked in. If marketplace lending truly is becoming a game for Wall Street by Wall Street, then the few retail investors who are invested in it could eventually become collateral damage in a pissing match between wealthy bankers.

Investor faith

There are already concerns that the incentive for marketplaces are not aligned with those of their investors. PeerCube co-founder Anil Gupta wrote this on the LendAcademy forum about Prosper, “The quest to increase originations and revenue will trump any such risk management attempts, like what happened with banks issuing mortgages to unqualified borrowers in order to boost their own bottom lines.” He wrote that in response to an upset user whose borrower declared bankruptcy before making even a single payment towards their Prosper loan.

The user was questioning how Prosper would handle this since the timing of the loan prior to the bankruptcy filing had all the hallmarks of fraud.

Gupta added, “There is very little incentive for LC and Prosper to pursue such collections and recoveries claims. When LC was investing its own money in loans, they pursued collections and recoveries more vigorously (11.19% collection in 2007 vs 5.53% collection in 2011). It is no longer Prosper and LC money at risk.”

The user is not alone in his collections fears. Just a few days earlier I realized that 4.6% of all the notes I had purchased on Lending Club had already defaulted, a number that troubled me considering my average note is only 10 months old. With another 3-4 years still to go until maturity, the rate of defaults is already quite high.

The user is not alone in his collections fears. Just a few days earlier I realized that 4.6% of all the notes I had purchased on Lending Club had already defaulted, a number that troubled me considering my average note is only 10 months old. With another 3-4 years still to go until maturity, the rate of defaults is already quite high.

And while I’ve been told that my own personal stats are relatively normal, other retail investors occasionally run into quirks that force them to question the soundness of the reporting they receive.

For example, veteran users commonly rely on the FICO score updates Lending Club will publish for each issued loan. If a borrower’s score is dropping, you could sell the note for a discount to an interested buyer on a marketplace such as folio. Several people have admitted to using this strategy to mitigate losses. There’s just one problem, a user discovered a discrepancy in Lending Club’s FICO reporting. In at least one case, the borrower’s FICO score may have been overstated by more than a hundred points. For users beholden to the accuracy of these figures in order to properly execute their investment strategy, it’s a difficult pill to swallow.

Call it a kink or an oddity. Maybe it’s something that needs to be fixed or maybe something is being miscommunicated. Whatever is going on there, these are the kinds of risks that institutional capital is supposed to be able to tolerate in their quest for yield, but it’s gut wrenching for retail investors.

In the instance of the suspected bankruptcy fraud, several responses by fellow investors gave the impression that the platform simply isn’t going to care because they make money off of issuing loans, not collecting on them. That’s the exact type of Wall Street attitude that could come back to hurt retail investors.

Marketplace lending might not technically be designed as peer-to-peer but the little guy and their actual peers certainly have their funds at stake. Calling it a game for big banks, the wealthy, and Wall Street only encourages the players involved to take bigger risks, reduce transparency, and shrug off genuine criticism.

We can’t let that happen.

PSC and Hudson Cook, LLP Align to Promote Best Practices in Merchant Cash Advance Industry

May 18, 2015 Earlier today, New York-based PSC announced an alliance with nationally renowned law firm Hudson Cook, LLP to educate members of the merchant cash advance industry. PSC provides full backend systems and support staff for more than a dozen merchant cash advance companies.

Earlier today, New York-based PSC announced an alliance with nationally renowned law firm Hudson Cook, LLP to educate members of the merchant cash advance industry. PSC provides full backend systems and support staff for more than a dozen merchant cash advance companies.

The move is significant because it focuses on the adoption of best practices. The only other similar initiative has come from from the Small Business Finance Association (SBFA), but no organization has ever actually made guidelines public, at least not since the Electronic Transactions Association published a white paper in March 2008.

Both Hudson Cook and the SBFA are said to be separately working on their own public best practice frameworks in collaboration with industry participants.

Three attorneys for Hudson Cook recently took on the industry’s most polarizing topic, stacking, when they authored, Stacking: Is it Tortious Interference?. “The analysis of what is ‘improper’ interference versus vigorous, but acceptable, competition will be based on the specific facts of each case,” they wrote.

The law firm may draw from another well established best practice playbook, like the one that exists for the Online Lenders Alliance in the consumer lending space.

PSC recently hired Amanda Kingsley, the woman behind the headline, “Year of the Broker” in our last issue. Kingsley spoke often of best practices in her interview with AltFinanceDaily Magazine.

PSC recently hired Amanda Kingsley, the woman behind the headline, “Year of the Broker” in our last issue. Kingsley spoke often of best practices in her interview with AltFinanceDaily Magazine.

A month ago at the LendIt conference, Karen Mills, the former head of the Small Business Administration, said she asked several regulatory bodies who would stand up to oversee small business lending. “No one stood up,” she said.

For now, that seems to mean that the industry is on its own. “PSC also intends to maintain its commitment to its members by providing standards to help them better adhere to all new legal requirements and regulatory practices,” the release said.

It’s a step in the right direction.

Brokers, Ferraris, Stacking and More

March 10, 2015 Not yet signed up to receive AltFinanceDaily’s print magazine? You can subscribe to receive it FREE here. This upcoming issue covers a lot of ground!

Not yet signed up to receive AltFinanceDaily’s print magazine? You can subscribe to receive it FREE here. This upcoming issue covers a lot of ground!

Some sneak peeks and commentary:

* I interviewed the president of a Ferrari-driving MCA brokerage who started off as a telemarketer that lived in his car.

* A CPA firm and Law firm submitted interesting takes on different industry practices.

* As much as I wanted to cool off on the topic of stacking for a while, those interviewed by our journalists couldn’t stop talking about it. It is apparently unavoidable and inescapable. Whether you stack or you don’t it’s one of the first nuggets to pop up in any conversation about short term business financing. Coincidentally, I had the privilege of being in the room with some industry leaders a few weeks ago and a discussion about stacking inevitably dominated the debate.

* There’s lot of new brokers in the space and not just human middlemen, but platforms that are really just technology-based brokers. We investigated what’s driving the new brokers and how to handle them. Separately, we interviewed a technology company that automates loan picks so that retail lenders don’t have to.

There’s more of course. You’ll just have to subscribe and wait for it to arrive in the mail. They’ll be sent out at the end of this month.

And if you plan on going to the LendIt Conference in NYC, use coupon code: AltFinanceDailyVIP to get 25% off the ticket price. All attendees will get a copy of the magazine in their swag bag. I hope to see you there.

On Deck Capital IPO, An Insider’s Perspective

August 16, 2014It was August 23, 2011, the day the Virginia Earthquake could be felt all the way up in New York City. The four of us were enjoying outdoor seating at a restaurant on the Upper East Side. The ground shook, my drink spilled and Ace looked at each one of us and said, “Okay so I’m putting you down for five deals this month.” OnDeck Capital’s relationship managers were aggressive. If you were a small Independent Sales Organization (ISO), they didn’t expect to get all of your dealflow so they roped you in little by little. It was hard to say no. If five deals was too much, Ace would say three and if three was too much, then he’d put you down for three anyway. Zero was not in the cards. OnDeck owned a specific niche and if you didn’t send your premium credit clients to them, then any ISOs you were competing against would. That was a death knell in those days. Just a few years earlier I would’ve shrugged them off, but public sentiment was changing. Merchants were embracing the fixed daily payment methodology and the merchant cash advance industry would never be the same.

OnDeck Capital is now going public. Will you buy stock?

I’m in a unique position to discuss OnDeck. I started my career in this industry before they even existed. I’ve competed against them as an underwriter at a rival firm, worked with them as a referral partner when I was in sales, and covered them in my capacity as Chief Editor of an industry trade publication.

I’m in a unique position to discuss OnDeck. I started my career in this industry before they even existed. I’ve competed against them as an underwriter at a rival firm, worked with them as a referral partner when I was in sales, and covered them in my capacity as Chief Editor of an industry trade publication.

I left my post as Merchant Cash & Capital’s Director of Underwriting in late 2008. I was 25, about a year or two older than the average employee in the industry. Several of MCC’s rivals got demolished in the financial crisis but OnDeck wasn’t one of them. They also weren’t much of a competitor either. Struggling to define themselves as the anti-merchant cash advance, their product ran counter to the spirit of the industry’s rise. The single biggest allure of a merchant cash advance wasn’t that it was easy to obtain but that there was no fixed repayment term. The funds came with a pre-determined net cost but no specific date on when the delivery of future sales would be due.

Outsiders like the news media aren’t exactly sure what separates merchant cash advance from OnDeck except for maybe the cost of funds. Cash advance just sounds expensive, doesn’t it?

Outsiders identify the company by three characteristics.

1. They’re a non-bank business lender

2. They’re more expensive than a bank

3. They’re a tech company

These bullet points gloss over the fact that OnDeck’s loans require payments to be made every day. Can you imagine a credit card company forcing you to send a payment every day of the month? Or your landlord asking for rent on the 1st of the month, the 2nd, the 3rd, 4th, 5th, and so on every day until your lease is up?

This is not to say that this system is necessarily bad for borrowers, but that it is quite possibly the most unique and important part of what makes OnDeck different. It’s their secret sauce. It is why OnDeck gets lumped in with merchant cash advance companies in many conversations. OnDeck and the legion of copycats they have spawned are part of a broader industry that includes merchant cash advance companies. I call them daily funders. Daily funders provide financing on the condition that payments are made daily. I don’t call them daily lenders because traditional merchant cash advance products are not made by lenders, but by a unique group of investors that purchase future revenue streams.

Transition

Under company founder Mitch Jacobs, OnDeck had established themselves as the de facto loan option.

The merchant’s not biting on merchant cash advance? Send it to OnDeck. The merchant doesn’t accept credit cards? Send it to OnDeck.

They were every merchant cash advance ISO’s frenemy. They’d solicit you for your deals and then throw you under the bus to journalists as evil purveyors of expensive financing. They needed us to source dealflow and we needed them to maximize closing ratios but neither was quite satisfied with the arrangement.

When the company’s first employee took over as CEO in June 2012, the rhetoric changed. While still happy to be portrayed as the anti-merchant cash advance, OnDeck transformed their image from a niche Wall Street lender to a Silicon Valley-esque tech company. Noah Breslow was a curious choice. He has a BS from MIT and an MBA from Harvard Business School. He’s tall, charismatic, and he introduced vocabulary words such as algorithm to an industry that relied entirely on manual human underwriting.

At a recent lending conference, the younger crowd characterized Breslow as the Steve Jobs of business loans. He commands a cult-like following inside and outside the company, and in 2013 was embraced by New York City’s Mayor Bloomberg.

Breslow fast tracked OnDeck. With only $43 million raised in the first 5 years, the company went on to raise more than $300 million in the first 24 months under Breslow’s leadership.

This was their plan all along

In November 2012, OnDeck entertained a buyout offer from UK-based payday lender Wonga in which they reportedly received a $250 million valuation. The deal fell apart in the late stages but at the time I believed the negotiations were all a ploy for OnDeck to get a true market valuation. With a solid offer on the table, they knew both where they stood and where they needed to go. Last week the WSJ reported that preliminary IPO discussions valued them at $1.5 billion, six times higher than where they were two years ago.

With stock options being offered to new employees at least as far back as 2012, the plan to go public should come as no surprise. Later this year, those employees may actually get to do something very few startup workers ever get to do, convert those options into real shares.

So will OnDeck ride off into the sunset of billion dollar bliss? Not so fast say several industry insiders, some of whom are itching to short the stock on the first day they can.

Smoke and mirrors?

Smoke and mirrors?

As OnDeck took advantage of the swing in public consensus (that fixed terms were better and lower costs increased the attactiveness ), insiders began to ask an important question. Why weren’t merchant cash advance companies collectively countering with lower prices to remain competitive? Greed was fingered by journalists especially in the wake of the financial crisis. But greed is a weak prerogative if you consider that merchant cash advance companies were filing for bankruptcy left and right in 2009.

And oddly or perhaps even ominously, an entire segment of merchant cash advance companies began to raise their prices just as OnDeck was lowering theirs. When I wrote The Fork in the Merchant Cash Advance Road in April 2011, I said:

While the margins earned on high credit accounts shrank, funding providers were dealing with another challenge simultaneously, defaults. Whether the business owner intentionally interfered with their credit card processing or the store went out of business altogether, bad debt in the MCA world was mounting…FAST!

Risk was and still is the number one reason that merchant cash advances cost so much. While it’s true that OnDeck serviced higher credit businesses, insiders speculated that the spreads were too thin. For years, OnDeck’s merchant cash advance competitors have doubted the soundness of their model.

It’s a debate that continues even to this day and yet OnDeck has secured hundreds of millions in investments from companies like Google Ventures, Goldman Sachs, Peter Thiel, and Fortress Investment Group. Their notes got an investment grade rating from DBRS. And as far as volume is concerned, they have likely eclipsed the industry’s all time reigning giant CAN Capital. If they had reached none of these milestones, OnDeck would have little credibility to convince critics of their sanity.

It’s a debate that continues even to this day and yet OnDeck has secured hundreds of millions in investments from companies like Google Ventures, Goldman Sachs, Peter Thiel, and Fortress Investment Group. Their notes got an investment grade rating from DBRS. And as far as volume is concerned, they have likely eclipsed the industry’s all time reigning giant CAN Capital. If they had reached none of these milestones, OnDeck would have little credibility to convince critics of their sanity.

With a mountain of circumstantial evidence through big name backing in OnDeck’s favor, it seems to be indicative that the skeptics are wrong. But maybe they’re not. Could their model be both seriously flawed and superior at the same time?

It’s all about eyeballs

Going back to the 1990s, Internet companies have been judged, valued, and made famous by the price of eyeballs and the number of site visits. It’s a measure that’s never disappeared and according to USA Today is making a comeback. And while OnDeck Capital has always been based in New York City, true to their Silicon Valley form, their model has been to conquer market share first  and take on profitability second. In their case, it’s not eyeballs or site visits, it’s loan origination volume.

and take on profitability second. In their case, it’s not eyeballs or site visits, it’s loan origination volume.

Five months ago Breslow was quoted in the WSJ as saying OnDeck is “imminently profitable“. With seven years in business, it’s proof that their critics have been right all along, that their model doesn’t make money.

What scares their competitors though, is that this strategy has been intentional. Very few if any players in the industry have had the luxury, guts, or the purse to lose money for seven years as part of a coup to conquer the market. Disbelievers in this long term wildly risky strategy are salivating at the opportunity to inspect the company’s financial statements in the IPO.

In When Will the Bubble Burst?, RapidAdvance CEO Jeremy Brown, whose company became part of the Quicken Loans family last winter, fired shots at OnDeck, “To accomplish high growth rates, which may be driven by a desire or need for an IPO or to raise investment or to sell to private equity, assets are being overpaid for through higher than economically justified commissions (I’ve heard 12-15 points upfront from the more aggressive companies) and stretch the repayment term of the MCA or loan even further (On Deck24, I am talking about you).”

Insiders testify that OnDeck’s strategy has not so much been about lower costs but about growth at all costs. Among the evidence is the sudden removal of an industry-wide practice of verifying the business owner is current on their rent. Repayment terms are getting stretched out, commissions have shot up, and for a while they ran a program that allowed applicants to get funding with the submission of just a single bank statement.

Merchant cash advance companies look at their own default figures and scoff at the notion that OnDeck’s aggressive practices could produce low single digit defaults as they’ve publicly claimed.

Imminent

Through it all, there remains the fact that OnDeck has never claimed their methodologies to be profitable, at least not yet. Red ink at IPO time might reward their detractors with a certain delicious satisfaction, but what will they say if and when they become profitable?

Through it all, there remains the fact that OnDeck has never claimed their methodologies to be profitable, at least not yet. Red ink at IPO time might reward their detractors with a certain delicious satisfaction, but what will they say if and when they become profitable?

I’m reminded of The 20 Smartest Things Amazon Founder Jeff Bezos ever said. Below is a few of them.

- “There are two kinds of companies: Those that work to try to charge more and those that work to charge less. We will be the second.”

- “Your margin is my opportunity.”

- “We’ve done price elasticity studies, and the answer is always that we should raise prices. We don’t do that, because we believe — and we have to take this as an article of faith — that by keeping our prices very, very low, we earn trust with customers over time, and that that actually does maximize free cash flow over the long term.”

- “If you never want to be criticized, for goodness’ sake don’t do anything new.”

- “Invention requires a long-term willingness to be misunderstood. You do something that you genuinely believe in, that you have conviction about, but for a long period of time, well-meaning people may criticize that effort. When you receive criticism from well-meaning people, it pays to ask, ‘Are they right?’ And if they are, you need to adapt what they’re doing. If they’re not right, if you really have conviction that they’re not right, you need to have that long-term willingness to be misunderstood. It’s a key part of invention.”

I wonder if the executive team at OnDeck would share these philosophies.

They’ve always claimed themselves to be a tech company, much to the bewilderment of their competitors. Will technology come through for them?

The data available on businesses has changed. Bank statements and a credit report might’ve been all there was to go on when the company first started, but in Automated Intelligence Breslow said, “the fact is most businesses operating today, in 2014, are already technology focused to one degree or another. They have computers, they have online banking, they use credit card processors, their customers are reviewing them online, there are public records, etc. All this electronic data helps paint a deeper and more accurate picture of the health of a business.”

With such easy access to important data, it might be possible that through the use of 2,000 data points, OnDeck doesn’t need to do all the manual investigations that their competitors still place high values on. The available data might be able to predict loan repayment success just as well as a human analyst.

And if that’s true, then they can reduce the cost of overhead as they scale. As their predictive algorithms get fed more data, they might be able to eliminate humans altogether. At the May 2014 LendIt conference, Breslow admitted that 30% of their loans were still manually underwritten but said that “if customers want full automation, we are prepared to deliver it.”

By that charge, a sustainable model should not be that far out of reach. Through advanced data analysis and decreasing fixed costs, profitability may indeed be imminent.

Winner

If the story of the merchant cash advance industry has been a race to the top, then OnDeck might be declared the winner in a successful IPO. It would be an ironic achievement for the company that positioned itself as the anti-merchant cash advance. In their wake today are hundreds of daily funders offering fixed payment products.

OnDeck’s critics are in a paradoxical position because a successful IPO is good for them too. They want to believe OnDeck’s model never worked, can’t work, and have it be proven a failure. But if it goes the other way, the legitimacy of the daily funder universe will be solidified in the mainstream. What’s good for the goose is good for the gander.

OnDeck’s critics are in a paradoxical position because a successful IPO is good for them too. They want to believe OnDeck’s model never worked, can’t work, and have it be proven a failure. But if it goes the other way, the legitimacy of the daily funder universe will be solidified in the mainstream. What’s good for the goose is good for the gander.

As AmeriMerchant CEO David Goldin said to Inc, “the OnDeck IPO shows that Wall Street is now taking this industry seriously.”

So does that mean he’d buy stock? Somewhere out there at a restaurant in New York City, an OnDeck relationship manager is probably putting Goldin down for five shares.

Cue the earthquake, the industry will never be the same.

Curious how it will change it exactly? Read my magazine published prediction, The Retail Investor.