Becoming a ‘Certified’ Merchant Cash Advance Professional is Just Around The Corner

April 11, 2016

Update: 11/4/16 – THE ONLINE COURSE IS HERE. The final version offers test takers the chance to earn a certificate in MCA Basics, specifically the characteristics that make loans different from purchases of future receivables.

A survey conducted last year by AltFinanceDaily has contributed to the development of a training and certification course for merchant cash advance salespeople. Co-produced by Hudson Cook LLP, AltFinanceDaily, and other industry veterans, sales representatives that offer the merchant cash advance product will have the opportunity to learn from an online tutorial complete with training videos and quizzes to achieve a new standard of educational excellence.

Being able to expertly understand and communicate the differences between loans and purchases is among the courses’s main goals. Funders and ISOs can supplement their own training procedures with the course. Those that complete and pass it should expect to receive a certificate.

While it’s not ready to go live just yet, Hudson Cook partner Robert Cook, says he will be available at the Lendit Conference should anyone wish to discuss or share their input. He can be reached at rcook@hudco.com.

Retail Investors Can Invest In Business Loans – Thanks To StreetShares Regulatory Approval

March 16, 2016 If not being an accredited investor has kept you on the sidelines of marketplace lending, you’ll soon be able to invest in business loans on the StreetShares platform, thanks to a special regulatory approval by the SEC. While you’re not going to the earn the yields you’d get with merchant cash advance (MCA) syndication, StreetShares makes loans for as short as three months. The available products are 3, 6, 12, 18, 24 & 36 month term loans, according to their website, which are desirable lengths for investors used to MCA. The Funding Circle platform by contrast, requires investors be accredited and loan terms range from 1 to 5 years. If you aren’t eligible to invest through Funding Circle, well that is what will make StreetShares different.

If not being an accredited investor has kept you on the sidelines of marketplace lending, you’ll soon be able to invest in business loans on the StreetShares platform, thanks to a special regulatory approval by the SEC. While you’re not going to the earn the yields you’d get with merchant cash advance (MCA) syndication, StreetShares makes loans for as short as three months. The available products are 3, 6, 12, 18, 24 & 36 month term loans, according to their website, which are desirable lengths for investors used to MCA. The Funding Circle platform by contrast, requires investors be accredited and loan terms range from 1 to 5 years. If you aren’t eligible to invest through Funding Circle, well that is what will make StreetShares different.

Unlike the laborious process that Lending Club and Prosper took with the SEC to sell loan performance-dependent notes to unaccredited investors, StreetShares got a special approval under the JOBS Act’s Regulation A+. That only allows them to raise up to $50 million over a 12-month period so investing availability may be limited.

In a press release, the company specified that “repayment to investors is not tied to the performance of a particular underlying loan.” The LendAcademy blog is reporting that “StreetShares will provide a vehicle for investors to become diversified through some kind of fund” and that details should be revealed around the time of the LendIt Conference.

Though company CEO Mark Rockefeller of StreetShares might not remember this, we spoke during a lunch break at LendIt 2014 when his company was a brand new startup. At that time, he told me about his “veterans funding veterans” lending marketplace model where the costs would be much lower than what can be experienced in the merchant cash advance industry. Since then his company has won the 2015 #1 global Best Investment Award from Harvard Business School and is now the first small business lender to get approval under Regulation A+.

One other person that is trying to bring small business lending investing to the unaccredited investor community is hedge fund manager Brendan Ross. Ross’s Direct Lending Income Fund filed an N-2 with the SEC at the conclusion of last year to become a “40 Act fund,” a special investment company permitted under The Investment Company Act of 1940 that can accept investments from retail investors. In January, Ross explained to CNBC during an interview that the fund’s structure would be converted so that investors become shareholders in what would essentially be a lending business.

StreetShares plans to officially debut their new program at LendIt next month.

Herio Capital Breaks $20 Million in Funded Deals

March 9, 2016 It might feel like 1997, but in early 2016 Herio Capital has surpassed $20 million in funding since inception. Co-founded by Sherif Hassan, the company’s chief executive, Herio launched only one year ago. Hassan was one of OnDeck’s first employees who stayed with the company all the way up until just before they went public.

It might feel like 1997, but in early 2016 Herio Capital has surpassed $20 million in funding since inception. Co-founded by Sherif Hassan, the company’s chief executive, Herio launched only one year ago. Hassan was one of OnDeck’s first employees who stayed with the company all the way up until just before they went public.

Today, Hassan does not appear to be regretting that choice. “We have lots to be grateful for and even more to be excited about in 2016,” he said.

The company’s chief product officer and co-founder, Patrick Janson, summed up their vision like this, “When we started Herio, we saw a huge opportunity to improve upon the software that currently supports the marketplace lending industry.”

The Herio team will be attending the LendIt Conference in San Francisco next month.

“Reaching the $20 million funding milestone is a testament to the execution, creativity, and diligence of everyone at Herio. We are grateful to our team and our loyal industry partners. We are excited about the advancements our industry will make in the next period as we continue to design the future of credit,” concluded Hassan.

OnDeck (ONDK) Stock Continues to Sink. Now What?

February 26, 2016OnDeck reached another new all-time low share price on Thursday, closing at $6.35 but hitting $6.05 intraday. The continued spanking follows their 2015 earnings release that apparently did not impress the market. And there’s many reasons to be troubled by that since the tone of the earnings call oozed of renewed confidence. It was expressed as much in OnDeck Regains Their Swagger in Q4 Earnings Call – Lends $1.9 Billion in 2015

OnDeck can’t win. When growth was high, critics complained about profitability. When OnDeck achieved profitability, critics complained that growth had slowed. On Wednesday, critics hit them with the kitchen sink. Growth has slowed, losses are mounting, guidance was revised down, the JPMorgan Chase partnership isn’t yielding revenue, operating expenses rose, etc.

The real problem now is that they can’t seem to overcome these objections during a period of economic calm. The stock market is currently operating at rather rational levels. The S&P 500 is only down 3% year-to-date. OnDeck is down 35% over that same time period.

In a recession, financial companies can be uniquely vulnerable to irrational fear. JPMorgan Chase for example, lost more than 50% of their market cap between August 2008 and February 2009. This is a nightmare scenario now for OnDeck.

“These companies have been valued as if there’s really no credit risk or capital-markets risk whatsoever,” said Bill Ryan, an analyst at Portales Partners, to the WSJ. “I think that’s what changed.”

“We are not seeing weakness in our portfolio at this time,” said OnDeck CEO Noah Breslow during the earnings call.

Apparently that doesn’t matter and one has to wonder what will in the future.

No, Social Media isn’t the New Credit Score

February 25, 2016 The “social media is the new FICO score” crowd suffered a blow on Wednesday when a Wall Street Journal article reported that it ain’t working too good.

The “social media is the new FICO score” crowd suffered a blow on Wednesday when a Wall Street Journal article reported that it ain’t working too good.

Almost 3 years ago, Kabbage co-founder Marc Gorlin told CNN that small businesses who link up their facebook and twitter accounts up with their system, were 20% less likely to be delinquent on their loans. Around that time, Hong Kong-based Lenddo was heralding other positive claims about the value of social media. In the loans they made in Colombia and the Philippines for example, Slate reported that “they scrutinized the applicants’ connections on Facebook and Twitter and that the key to getting a successful loan from Lenddo was having a handful of highly trusted individuals in your social networks.”

For a time, non-bank lenders were saying that social media was the future of credit. That is until it wasn’t.

The WSJ recently reported that lenders are backing away from social media data because it’s becoming harder to tap into and because of the potential regulatory consequences under fair credit laws. Just last month for example, the FTC published a report titled, Big Data, A Tool for Inclusion or Exclusion? In it, the FTC warned that “if a company targets services to consumers who communicate through an application or social media, they may be neglecting populations that are not as tech-savvy.” The implication is that there is potential for unconscious and unintended discrimination of certain minority groups. “Systemic disparate treatment occurs when an entity engages in a pattern or practice of differential treatment on a prohibited basis. In some cases, the unlawful differential treatment could be based on big data analytics.”

But even then, companies like Kabbage have seemingly softened their stance on the value of social media anyway. “Who your social circle is, or whether you play ‘Mafia Wars’—we haven’t seen that as very valuable,” Kabbage CEO Rob Frohwein said to the WSJ.

Facebook is restricting the depth of data available to third parties now anyway. As a result, dozens of startups (not just lenders) that had been using Facebook data have shut down, according to the WSJ.

Lenders like OnDeck might not be surprised by the industry’s sudden realization. Two years ago at LendIt 2014, company CEO Noah Breslow said you have to be careful with the noise of social media as there can be a lot of false signals. And RapidAdvance COO Joe Looney was already telling CNBC three years ago that his company was “not going to make a decision based solely on a string of online comments on a social-media site” even though they would consider the mere presence of an active social-media footprint to be a “good sign.”

It looks like the future of credit scoring isn’t likely to be social media any time soon. All hail the fundamentals.

Why OnDeck Didn’t Sign The Small Business Borrowers Bill of Rights

January 21, 2016 Recent media reports attempting to spin OnDeck’s loan programs in a negative light have been quick to point out that they have not signed on to the Small Business Borrowers Bill of Rights. There’s apparently an obvious reason for that, they weren’t invited to participate in the drafting of it…

Recent media reports attempting to spin OnDeck’s loan programs in a negative light have been quick to point out that they have not signed on to the Small Business Borrowers Bill of Rights. There’s apparently an obvious reason for that, they weren’t invited to participate in the drafting of it…

In a recent interview with Lend Academy’s Peter Renton, Breslow addressed this even further. “I think if you look at the actual principles and the way the document is written, there is a clear bias towards longer term loans in the document,” Breslow told Renton, pointing out that the group is a small circle of lenders that focuses on 3-year loans. “We don’t think a three-year product is appropriate for many types of small businesses out there, but if you can’t get access to a long term loan we don’t think that means you shouldn’t get a loan at all,” he added. “So what we’d love to see either in the BBOR or some other industry standard that you might see developing over the next year is a broader perspective on what types of financing businesses should have access to and to be clear, we’re very supportive over time, kind of inclusive industry standards that encompass the range of products that we think small businesses should have access to and that access should be fair, efficient and transparent.”

You can listen to the entire interview which covers many more topics below:

Or read the full transcript here.

Renton is a co-founder of the LendIt conference, the biggest marketplace lending event of the year. If you haven’t secured tickets yet to the April conference in San Francisco, you should sign up here before it’s too late. Last year the conference was completely sold out.

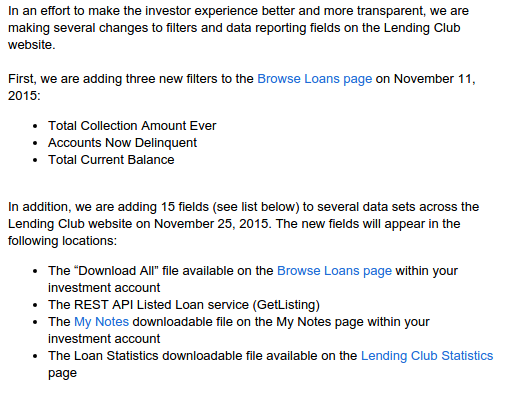

Lending Club Narrowly Avoids Major Transparency Flop

November 18, 2015After many months of Lending Club warning that they would be REMOVING borrower credit data from note listings, they have completely reversed course and ADDED fifteen new credit attributes. On Peter Renton’s LendAcademy forum, one member speculated that this move was made to compete with Prosper for the attention of institutional investors. If true, that would be entirely misguided.

Almost exactly one year ago, Lending Club announced that they were cutting the amount of data points available to investors from 100 to 56. Renton, a marketplace lending evangelist and founder of the LendIt conference, gave it a negative spin in his blog:

It is pretty obvious by now that I don’t like these changes. For quite some time now Lending Club has been reducing the amount of transparency for investors. Now, some changes I completely understood such as removing the Q&A with borrowers and even the removal of loan descriptions. But removing data that investors have been using to make investment decisions is a step too far in my opinion.

I think Lending Club need to ask themselves if they are a true marketplace connecting borrowers and investors in a transparent fashion or whether they are more of a loan origination platform that makes products available to investors. They are certainly moving more towards the latter, I think, and that is a shame for everyone.

The move was seen by many as a way to stop investors from trying to reverse engineer their models and beat their grading system for above average yields. While understanding that perspective, it is mind boggling that they had planned to remove more data points and make the loans on the platform even less transparent. And here’s why…

Lending Club is a key signatory to the Small Business Borrower’s Bill of Rights, a group of political activists that claim innovative small business lending can only achieve its potential “if it is built on transparency, fairness, and putting the rights of borrowers at the center of the lending process.” With transparency being a focal point of their agenda there, one might find their attempts to reduce disclosure and eradicate transparency a bit hypocritical.

Lending Club is a key signatory to the Small Business Borrower’s Bill of Rights, a group of political activists that claim innovative small business lending can only achieve its potential “if it is built on transparency, fairness, and putting the rights of borrowers at the center of the lending process.” With transparency being a focal point of their agenda there, one might find their attempts to reduce disclosure and eradicate transparency a bit hypocritical.

Investors on Renton’s forum who had for months anticipated Lending Club to remove more data points, also viewed it negatively. “I’d have to think hard on whether to continue investing in LC notes without those credit fields — it would be very much like gambling rather than investing,” wrote Fred back on July 8th.

A similarly named user, Fred93, communicated that these data points were all investors had to go off. “We can’t shake a borrower’s hand, feel the firmness of his grip, the sweatiness of his palm. We can’t look a borrower in the eye. We live or die by a handful of numbers, which we hope mean something, on the average,” he wrote.

Clearly some investors weren’t thrilled with the proposed changes. All the while, Lending Club’s co-signatories had been promoting the transparency pledge through speeches, TV appearances, public relation events, and press releases. To be fair, The Small Business Borrowers Bill of Rights is aimed at transparency between business borrowers and sources offering business financing. Lending Club’s planned removal of data was targeted at investors in their consumer notes. It sounds different enough until you consider that 72% of Lending Club’s loans originated in 2014 were funded by investors vastly less sophisticated than the commercial businesses they have pledged to protect. That’s because that money came from consumers, many of whom are unaccredited and went through no screening process. Instead, these investors are presented with a prospectus as if they were buying a stock or bond and stuck with the risk whether they understand it all or not.

These consumers who are legally presumed to be unsophisticated are the very same people that Lending Club planned to reduce disclosures to, all the while heavily promoting to them that they roll over their retirement savings onto their platform. That logic is the very definition of insanity. Obfuscating the reasoning behind certain scoring grades to these investing consumers would be nothing short of unconscionable and would reasonably invalidate any pledge they’ve made towards transparency in other areas.

Lending Club has for now avoided a major flop by reversing course after having added 15 new pieces of data for investors.

While some investors speculated the move had to do with pressure from Lending Club’s institutional investor base. The more likely reason is increasing scrutiny from federal regulators. Less than two weeks ago for example, the FDIC warned banks about marketplace lending and advised them to perform their own underwriting on the loans they buy and not to rely on originator scoring models. A summary of their letter specifically said:

Some institutions are relying on lead or originating institutions and nonbank third parties to perform risk management functions when purchasing: loans and loan participations, including out-of territory loans; loans to industries or loan types unfamiliar to the bank; leveraged loans; unsecured loans; or loans underwritten using proprietary models.

Institutions should underwrite and administer loan and loan participation purchases as if the loans were originated by the purchasing institution. This includes understanding the loan type, the obligor’s market and industry, and the credit models relied on to make credit decisions.

Before purchasing a loan or participation or entering into a third-party arrangement to purchase or participate in loans, financial institutions should:

– ensure that loan policies address such purchases,

– understand the terms and limitations of agreements,

– perform appropriate due diligence, and

– obtain necessary board or committee approvals.

These guidelines conflict with Lending Club’s long sought after goal of getting investors to trust their A-G scoring grades. The banking regulator is advising banks to basically disregard them. “The institution should perform a sufficient level of analysis to determine whether the loans or participations purchased are consistent with the board’s risk appetite and comply with loan policy guidelines prior to committing funds, and on an ongoing basis,” the more complete memo reads. “This assessment and determination should not be contracted out to a third party.”

A law firm with specialized knowledge of the industry, criticized the FDIC’s move when they wrote on their website, “Ironically, given the Treasury Department’s recent request for information, which supported marketplace lending and focused in part on how the federal government could be supportive of the innovations in marketplace lending, we now have a federal banking agency that is creating roadblocks to having banks participate in this dynamic and rapidly growing space.”

Asking banks not to rely on marketplace scoring models alone hardly seems like a roadblock, especially when the models are tucked away in algorithmic obscurity, have hardly been around for very long, and would decide the fate of depositor money. And if this directive indeed contributed to Lending Club’s transparency reversal, then it couldn’t have been any more well-timed.

Asking banks not to rely on marketplace scoring models alone hardly seems like a roadblock, especially when the models are tucked away in algorithmic obscurity, have hardly been around for very long, and would decide the fate of depositor money. And if this directive indeed contributed to Lending Club’s transparency reversal, then it couldn’t have been any more well-timed.

Whether or not the added data points will make any difference to the performance of investment portfolios is irrelevant. If unaccredited investors and/or depositor money are the source of marketplace loan funding, then Lending Club has a responsibility to disclose as much as possible, no matter how little value they believe certain pieces of information are worth. The 15 additional points are a welcome announcement. The question going forward should be, what else can they disclose?

As a company that pledged so strongly to protect corporations from transparency issues in the developing commercial finance market, they should be trying twice as hard to protect the unsophisticated consumers that invest in the loans they approve and make available for investing. Some of these consumers are prodded into putting their retirement funds on the platform and we all know some people will irresponsibly place their entire retirement portfolio in it. The “Number of credit union trades” a borrower has might not unlock the secret to better investing performance but if it’s something Lending Club knows, the investing public deserves to know it too, if only in the name of transparency which they have so committed themselves to uphold…

Blurring Small Business: A Troubling Narrative is Gaining Steam

October 30, 2015Almost 18 months ago at LendIt’s 2014 conference, Brendan Carroll, a partner and co-founder of Victory Park Capital said that in regards to business lending, “the government doesn’t have the same scrutiny on this sector as it does in the consumer space.”

This double standard is the crux of American capitalism. In business you can win or lose, be smart or foolish, risk it all or play it safe. Government regulations don’t let the average consumer be subjected to the same stakes. They are viewed to be at a natural disadvantage against businesses and thus there are laws to protect them, and perhaps rightly so.

Since entrepreneurship is a choice, businesses and the people that own businesses are held to a higher standard of acceptable risk taking. In the free market, the pursuit of profit holds the system together.

This economic worldview is part of the reason why entrepreneurial TV shows such as Shark Tank are so popular. In the Tank, contestants can just as easily walk away with a terrible deal as they can a good one. And when bad deals get made, and they do, I’ve yet to see regulators descend on the set to fine or arrest Daymond John, Kevin O’Leary, or Barbara Corcoran.

But Shark Tank features entrepreneurs on a remote stage detached from their daily environment, giving it the look and feel of a game show. If you want to see cold hard dealmaking with mom-and-pop shops on an up close and personal level, just watch CNBC’s The Profit. On the show, small business expert Marcus Lemonis does not sugarcoat what he is. “I’m not a bank. I’m not a consultant. And I’m not the fairy godmother,” he bluntly told one small business owner. It doesn’t matter if it’s a family owned store or a full fledged corporation, Lemonis is looking to make a deal and make some money. When it comes to business, he is well… all business.

Just as the CFPB hasn’t shut down Shark Tank, (which one has to wonder if they’ll be subject to Reg B of Dodd Frank’s Section 1071) none of Lemonis’ deals have been scrutinized by a Federal Reserve study, nor has the Treasury Department issued an RFI to better understand why entrepreneurs go on the show in the first place.

It’s no wonder then at LendIt 2014, Carroll also said that there wasn’t the same sort of moral hurdle when it came to institutional capital investing in business lenders as opposed to consumer lenders.

Moral was a telling word choice because the morality of certain commercial transactions have recently come under fire by groups claiming to represent small businesses. The premise of their argument is that commercial entities are no more sophisticated than consumers, that a corporation and the average joe are equal in their ability to take risks and make decisions for themselves.

Their evidence is that sometimes in business-to-business transactions, particularly in lending, one side accepts terms that would be considered far outside the norm for consumers, terms that violate a moral threshold. One has to wonder where a loan with an infinity percent interest rate ranks on this morality scale, a deal that’s actually been made and accepted several times on a TV show. Referred to as a “Kevin deal” since they are Kevin O’Leary’s favorite, the borrower is obligated to pay a perpetual royalty on top of repaying the loan itself. In simple terms, it’s a loan that can never be paid off.

In the case of Wicked Good Cupcakes, a business that appeared on Shark Tank in 2012, a mother-daughter team struck a deal that would cost them 45 cents per cupcake in perpetuity to Kevin O’Leary. Many fans criticized them for it and yet the two have said that they have no regrets.

In the case of Wicked Good Cupcakes, a business that appeared on Shark Tank in 2012, a mother-daughter team struck a deal that would cost them 45 cents per cupcake in perpetuity to Kevin O’Leary. Many fans criticized them for it and yet the two have said that they have no regrets.

The fact that Wicked Good Cupcakes decided what made sense for them and was happy about it, damages the storyline that businesses need to be saved from their own decisions. But there’s another problem, government entities themselves may be inadvertently effectuating this false narrative by inferring incorrect conclusions from their own research.

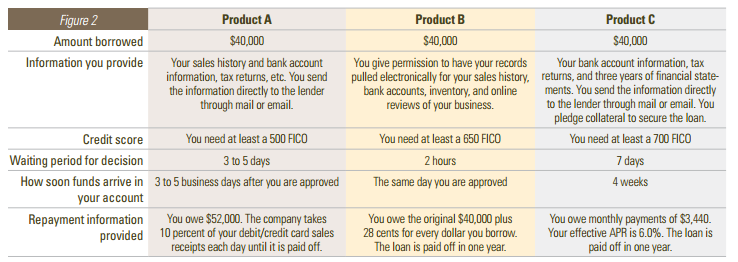

Nowhere is this more evident than in a report recently published by the Federal Reserve Bank of Cleveland that analyzed small businesses and their understanding of “alternative lending.” The report shared the results of two focus groups that had been shown terms for three hypothetical products that supposedly represented actual products in the real world.

Unsurprisingly, the report concedes “when comparing the products, participants initially reported the three were easy to compare and that they had all the information to make a borrowing decision.” But the researchers pressed on until they got an answer that fit their expectations, that small businesses are confused when it comes to money and finance.

In a hypothetical scenario where a commercial entity sold $52,000 of future receivables for $40,000 today, it stated that the “lender” would withhold 10% of each debit/credit card transaction until satisfied. Participants were then asked to guess the interest rate on this loan if they paid it back in one year. That caused a lot of folks to scratch their heads and that’s because it was a trick question.

The question itself introduced conflicting facts and lacked crucial variables to make an intelligent guess. Nevermind that respondents prior to that question said that there was “nothing confusing” about the products presented as is. The original feedback should’ve been enough. Below are some of the responses offered before they were deliberately tricked.

- “Nothing Confusing.”

- “No, it’s pretty straight-forward.”

- “I can’t think of anything more I would need to see, really.”

- “This is enough info for me to make a decision.”

The researchers concluded however that the answers to their trick question suggested there were “significant gaps in their understanding of the repayment repercussions of some online credit products and the true costs of borrowing.”

And while it might be true that they semi-admit to what they did when they wrote, “using only this information, calculating a true effective interest rate would not have been possible without making some assumptions,” the headline that spread thereafter was that small business owners are confused by alternative lenders.

And while it might be true that they semi-admit to what they did when they wrote, “using only this information, calculating a true effective interest rate would not have been possible without making some assumptions,” the headline that spread thereafter was that small business owners are confused by alternative lenders.

But even if that was the case, at what point does confusion become unfair in a purely commercial transaction? And what would be an appropriate remedy?

We’ve been down this road before where federal regulators have set mandatory disclosures in order to bring transparency to a lending environment believed to be obscure. And just recently on September 17th, 2015, the House Committee on Small Business Subcommittee on Economic Growth, Tax and Capital Access pressed community bankers on the impact of such measures dictated by Dodd-Frank.

Congressman Trent Kelly asked if all the added new pages to loan agreements make it easier for their borrowers to understand. “Do they understand what they’re signing?” he asked.

B. Doyle Mitchell Jr., the CEO of Industrial Bank that was speaking on behalf of the Independent Community Bankers of America responded that they do not. “It is not any more clear,” he answered. “In fact it is even more cumbersome for them now.”

If anything, the Federal Reserve study offered compelling evidence that small businesses are happy with the way alternative lenders are currently disclosing their terms. It is only when government researchers tricked them that they became confused. That should say it all.

One consequence of entrepreneurship is that businesses are not created equal in their ability to assess financial transactions and no amount of disclosures or intervention can save them. There must be losers in order for there to be winners.

Case in point, there are lenders out there doing deals so lopsided that they actually turn to each other and say, “I can’t believe she took that.” Such is the case of RuffleButts, a children’s fashion line that appeared on Shark Tank in 2013.

“When they wake up, they’ll realize they messed up,” said Mark Cuban in reference to the deal Lori Greiner proposed and closed. An article on BusinessInsider.com covered the episode and unabashedly concluded, “Shark Tank isn’t a charity. The investors are putting in their own money, so they have every incentive to push to get the best deal possible for themselves.”

Shark Tank has risen in popularity because it is a reflection of a culture that believes dealmaking, both good and bad, is inherent to the endeavor of entrepreneurship. When a bad deal is made, regulators don’t come on the show to urge a do-over.

But what’s dealmaking got to do with the local pizza joint seeking $20,000 that doesn’t have the time to mess around on TV shows? Unlike lenders who refer to their transactions as loans or units, merchant cash advance companies and the agents who negotiate the transactions appropriately refer to their agreements as deals. How else would one label an agreement in which a commercial entity sells future receivables for a mutually agreed upon price?

But what’s dealmaking got to do with the local pizza joint seeking $20,000 that doesn’t have the time to mess around on TV shows? Unlike lenders who refer to their transactions as loans or units, merchant cash advance companies and the agents who negotiate the transactions appropriately refer to their agreements as deals. How else would one label an agreement in which a commercial entity sells future receivables for a mutually agreed upon price?

And if the Federal Reserve study indicated anything, it’s that business owners feel there’s nothing confusing about these deals.

So it would seem that everything as Americans know it, watch it and understand it, is business as usual.

Even Brendan Ross, the president of Direct Lending Investments, was quoted by the BanklessTimes as saying, “I want to emphasize there’s absolutely nothing novel about lending money to businesses. This isn’t some phenomenon we are rediscovering. There isn’t going to be increased regulation because this isn’t new.”

Perhaps the only thing that could be considered new is that loan sizes have gotten smaller and the types of products small businesses can access has diversified. Along the way, some of these new startups have decided to offer products in line with a self-professed moral code, which is to deliberately lend money at a loss and lash out at lenders who seek profit.

There’s a term for lending startups that don’t make money. They’re called “failed startups.” By casting small businesses as being no different from unsophisticated consumers, it’s quite possible that shows like Shark Tank and The Profit would become illegal in the process. Disclosures meant to help make things more transparent could actually make things less clear and more cumbersome, just as they have in the past.

I don’t think anybody is in favor of small business failure or an environment where confusion prevails, including the guys making infinity percent interest loans like Kevin O’Leary. But if the goal is to increase transparency, it should be in a way that businesses on both sides are content with.

The Federal Reserve study showed the system is working well as is and that prescribing mandatory changes to fit some universal standard would only serve to usher in an era of confusion that everyone is trying to avoid. Lenders can always do better to serve their clients, but the free market must prevail. As Mitchell, Industrial Bank’s CEO said when he testified in front of the Small Business Committee, “the problem with Dodd-Frank is you cannot outlaw and you cannot regulate a corporation’s motivation to drive profit at all costs so while it has a lot of great intentions in over a thousand pages, it has not helped us serve our customers any better.”