A Decade of Funding

July 7, 2015Next month is my 9 year anniversary in the merchant cash advance industry, which means I’ll be starting my 10th year. A decade of merchant cash advance… holy shit. I’ve had the opportunity to view it from many different angles and have accrued my fair share of adventures, plenty of which I’ve written about and others I’ll have to take to my grave.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

Looking back now, there weren’t many people keeping a live diary of events as the industry dove headfirst into the financial crisis. Who would’ve bothered to report on an industry that was arguably made up of only a thousand people?

In April 2009, even before AltFinanceDaily launched, I submitted a story to the only merchant cash advance magazine of its kind. It didn’t have a very clever name, just Merchant Cash Advance Publication. My story, titled, An Underwriter in Salesman’s Clothing, rambled on about the end of the industry’s glory days, the wave of declined deals in the recession, and how funders should be more appreciative of ISOs.

Here’s a summary of what I wrote more than six years ago:

Here’s a summary of what I wrote more than six years ago:

I was complaining about stacking as far back as 2007 apparently. I addressed it as a merchant problem. Merchants were taking advantage of funders, not the other way around like some frame the argument in 2015.

I left my post as Director of Underwriting in late 2008 because “I wanted the ringing phones, the commotion, the markerboards with stats, the glory, the $20,000 [monthly] checks.”

Funding companies became super conservative during the financial crisis and all my deals were being killed (25 deals declined in a row at one point.)

I had recently charged my first closing fee, felt bad about it, and got in trouble for it.

I said 1.40 factor rates wouldn’t last (I was wrong about this!)

I bitched about algorithmic declines (I apparently thought computers underwriting files was a good way to upset ISOs.)

I acknowledged my own hypocrisy when I realized how hard it was to be a sales rep after thinking sales reps were overpaid and overrated in my previous years as an underwriter.

I continued on as a sales rep for another two and a half years after I wrote that. That means that in 2010 when I started AltFinanceDaily, I was still calling UCCs, closing deals and boarding merchant accounts while sitting in a windowless room rented by a startup ISO.

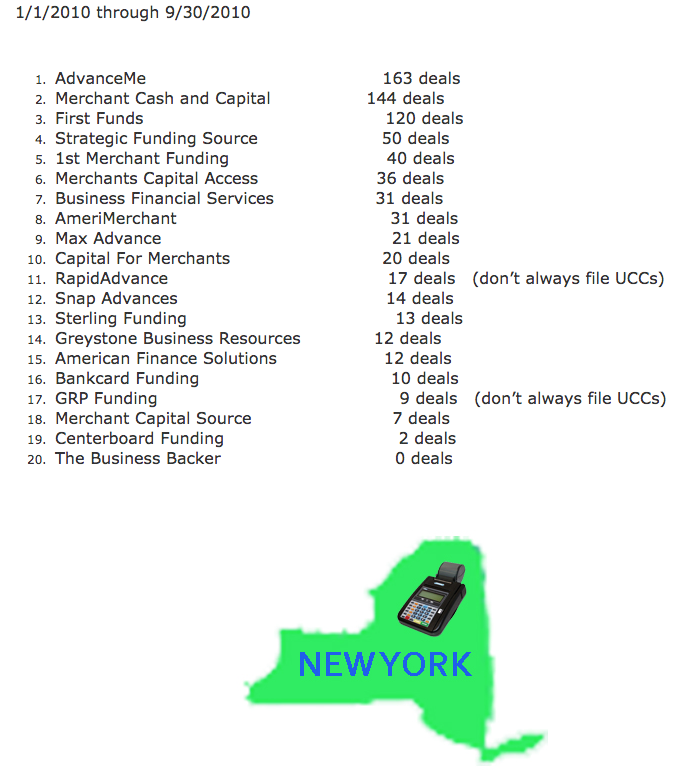

But what was there to blog about in 2010? Oh little stuff like who the biggest funding companies were at the time by checking UCC filings since almost everyone filed UCCs back then. Notably, the third largest merchant cash advance company of 2010, First Funds, is no longer in business.

I also wrote about shopping deals around and the impact that might have on a merchant’s credit report. That was the day-to-day stuff though, information I was just putting out there hoping someone on the Internet might see it. What got everyone excited was the 2010 New York State leaderboard which eventually prompted me to spend my nights and weekends investigating the industry on a wider level.

I began talking to people at other funding companies about their monthly numbers. It wasn’t that hard to get information as an industry insider, especially if you had deals to send somebody’s way. I also spent money to acquire secured party lists to count the number of UCC filings by funders in all 50 states rather than just look at one free state like I did with New York originally. I think I was the only person in the industry at the time running up their personal credit card bill to conduct such research. I had also been in the industry for four years at that point and had a great network of contacts who could clue me in on their volume.

While I said that I also looked at census records and department of labor records, I’ll admit that data wasn’t extremely useful. The end result was a best guess estimate that in 2010, there were approximately 21,000 merchant cash advances transacted for $524 million.

My data would go on to be republished in ISO&Agent Magazine, The Scotsman Guide, and Leasing News, and also end up in many other places I didn’t expect, like in the business plans of merchant cash advance companies that were looking to raise capital. In fact, in a private meeting I had with an MCA company months later in South Florida, the CEO let me take a peek at the docs they had just submitted to a bank for a credit facility. Included was a printout of these numbers with my name on it and all. Apparently there was something to this writing thing…

My last day as a sales rep was in the Fall of 2011. I left the commission-only life (oh what, you 2015 pansy closers actually get a base salary?) for something even more risky, an entrepreneurial life. For a couple years, I played underwriting consultant to a handful of merchant cash advance companies and industry expert to institutional investors interested in the space. I learned how to code in my spare time and spent more than a year in online lead generation.

I never stopped writing.

Along the way I’ve visited the offices of dozens of ISOs and funders, syndicated in deals, and test-drove new technology.

None of this makes me particularly special, especially when I hear about how much some of my old sales buddies are making these days on deals. “Are you SURE you don’t want to come back?” they ask. It’s enticing no doubt. A part of me wants to grab the phone out of their hand and attempt to shatter their record on the markerboard this month even though I’m pretty sure I’m rusty as hell.

One thing noticeable between now and 9-years ago is that my hair turned grey. This industry will do that to you (or at least it did to me.) And I still get a kick out of meeting folks who got into the industry years before I did. The 90s/early 2000s AdvanceMe crowd likes to tell me that they were funding merchants while I was still in diapers. They are practically right.

As I enter my own tenth year in the biz however, it’s exciting to think that the industry is just now getting started. OnDeck was the first IPO in the space and the general public is learning about short term business funding for the first time. There’s no shortage of news to report and that keeps me plenty busy these days.

And so even after a decade of MCA, it’s never too late to put on your Funded pants. Opportunity awaits and I hope you’ll continue to ride the wave with me. Thanks for reading since 2010!

The Challenges in Offering Financing to Latino Businesses

June 20, 2015 The number of minority-owned businesses jumped nearly 46% from 2002 to 2007, according to the Minority Business Development Agency. The growth rate is three times as much as for U.S. businesses as a whole. These businesses increased 55% in revenues over that five-year period. There are a number of minority groups within this category. Latino businesses are leading the way. Latinos are the fastest growing ethnic group in the United States today. Like it or not these numbers are likely to increase due to economic blocs. The U.S. has created a number of free trade agreements with Mexico, Central America and South America. Latinos are our next door neighbors.

The number of minority-owned businesses jumped nearly 46% from 2002 to 2007, according to the Minority Business Development Agency. The growth rate is three times as much as for U.S. businesses as a whole. These businesses increased 55% in revenues over that five-year period. There are a number of minority groups within this category. Latino businesses are leading the way. Latinos are the fastest growing ethnic group in the United States today. Like it or not these numbers are likely to increase due to economic blocs. The U.S. has created a number of free trade agreements with Mexico, Central America and South America. Latinos are our next door neighbors.

The SBA is the largest guarantor in the U.S. and does not offer any specific minority business loan program to Latinos. The U.S. Hispanic Chamber of Commerce offers advice to Latino business owners, but does not offer any loans. Traditional banks continue to maintain stringent guidelines for all businesses. Alternative finance companies and online lenders have a long way to go to tap into this

niche market.

Alternative lenders, online lenders and peer-to-peer lenders can cater to this niche market, but it requires a lot of resources and knowledge. We can categorize Latino businesses into one broad category. However, as a Hispanic entrepreneur, my experience has been that the Latino business community is complex in nature.

Latino Businesses by Age Groups

There are two types of Latino entrepreneurs. The older generation tends to be within the age range of 45 to 70 years old. These business owners are not accustomed to doing business over the Internet, email, fax, or phone. Online lenders may have difficulties in retrieving information from these clients. This group has a high level of distrust in doing business via the Internet. The majority of our clients within this age group are accustomed to doing business face to face. This sales and marketing strategy can be very expensive for lenders, unless you have a team of field agents. The younger generation of this group is made up of Latino entrepreneurs in the age range of 25 to 45. This group is more accustomed to using online banking and online systems. Forbes recently reported that, “With a median age of 28 years old, the timing is ripe for organizations/brands to make a firm commitment to the Hispanic consumer.”

Family Decisions and Delayed Gratification

Despite the age category, many Latino businesses are family-based. Based on my experience, the decision making process is made among family members. You could offer a $50,000 loan at a cost of factor of 1.30 to the husband and he may need to consult with his wife and his children before he signs his John Hancock. This makes the decision-making

process challenging.

Manuel Cosme Jr., the chair of the National Federation of Independent Businesses (NFIB) Leadership Council in California and co-founder of Professional Small Business Services in Vacaville, California has said, “Family plays a big role in Hispanic culture, so naturally it plays a big role in Hispanic-run businesses.”

Trust Factors

Even if you have a Latino staff or bilingual staff, Latino business owners need to trust you in order to gain their business. You will need to build good rapport with these businesses to get them to fill out a loan application and send it via fax, email or online. Latinos are accustomed to traditional banking methods and brick and mortar businesses.

“When we looked at online US Hispanics in 2006, there were four main roadblocks to US Hispanic e-Commerce adoption: 48% of online Hispanics did not want to give out personal financial information; 46% wanted to be able to see things before buying; 26% had heard about bad experiences purchasing online; and 23% did not have access to a credit or debit card,” says Roxana Strohmenger, Director in charge of Data Insights Innovation at Forrester. These are some of the challenges that we face by conducting our business in a digital manner.

According to mediapost.com, only 32% of online Hispanics use the Internet for their banking needs. In order for online lenders to succeed with this marketplace, U.S. banks need to do more to market to Hispanics online. Alternative lenders need to understand that there are barriers to entry in this marketplace.

Social Media

The Pew Research Center conducted a study that clearly indicates the usage of social media by Hispanics. Accordingly, 80 percent of Hispanic adults in the U.S. use social media and the same study revealed that Latino Internet users admitted to using Facebook as the leading social platform. A lot of business owners love to show the storefront, their family working in their businesses, and other images. You should consider Facebook as part of your overall marketing strategy to tap into this marketplace.

Going overseas

Going overseas

Another option to consider is going overseas. CAN Capital set up an operation in Costa Rica mostly for their business processing services. In fact, we at Lendinero decided to do something different that no one else is doing. We set up the majority of our operations in Central America, consisting of outbound agents, digital marketers, programmers and loan analysts. There are great benefits to having a full bilingual staff overseas and the cost of personnel is less expensive. At the same time, there are huge challenges. Since I am of Hispanic descent, it was easier to set up our operation in a Latin American country. However, there are cultural differences and you have to take into account the economic and political conditions of each country. Setting up a corporation can take 1 to 3 months and it is more expensive than the U.S.

The labor pool is huge, but finding the right people can be a challenge. In addition, training agents, processors, and support staff can be time consuming and you may run for a few months before you begin to see a profit. If your staff did not live in the U.S., you need to train them on U.S. culture, the economy, and other topics.

Furthermore, Internet speed and Internet services can be a challenge. Be prepared to pay a high cost for Internet. And labor laws are not like the U.S. If you fire an employee, you will be forced to pay unpaid vacation and a severance. In addition, you have to take other costs into consideration such as travel costs, lodging, auto leasing, and more.

Lastly, if you don’t know people in the country you plan on setting up in, an outsourced business processing service will charge you more money for rent and other services knowing that you are coming from the U.S. It is highly recommended you pair up with a native or someone who has done business in the countries you consider.

In summary, the Latino business community continues to lack financing. This niche market needs to be educated on the revolutionary paradigm shifts in business lending and online lending. If you can obtain these clients, they are clients for life. Once you obtain them as a client, they are loyal. They will not leave you.

Funding Down to a Science

December 21, 2012Account rep: Congratulations, you’ve been approved for $27,000!

Merchant: How did you come up with these figures?

Account rep: It was science. Science did this.

Funny? Maybe not, especially since an underwriting super algorithm may be on its way to the United States. In the days after we posted Made for Each other?, friends, acquaintances, and strangers have been telling us to keep an eye on Wonga’s potential acquisition of On Deck Capital. “It’s not just a european company’s gateway to the US. They’re going to change everything,” a few have said. Aside from their background of being a payday lender, having prestigious VC backing, and the resources to throw a quarter billion dollars at a main street lender in a takeover bid a lot of people didn’t see coming, apparently there is much more to be seen.

Just like MCA in years past, Wonga has worked hard to repel a negative image. Not easy stuff, especially considering they embrace their hefty costs wholeheartedly. Sure, it’s easy to calculate an APR equivalent of a very short term loan and spin whatever number you come up with as the symbol of something evil. If I let a stranger borrow $100 today with the stipulation that they pay me the whole thing back tomorrow plus 1 dollar extra to make it worth my while, would I be evil? That’s an APR of 365%. If I did the same thing with 100 strangers, what are the real odds that all 100 would actually pay me back? Somewhere along the line because of a borrower’s circumstances, bad decisions, or even malicious intent, I’m going to lose the entire $100 I lent out. Others might need more time to pay me back. If one person out of those hundred doesn’t pay back, I break even. If two people don’t pay back, I lose money. If one person doesn’t pay back and another can’t come up with the whole thing, I lose money. You can lend money at 365% APR and lose BIG.

So how do banks manage to charge 4, 7, and 10% APR? Is it just because they’re smarter? No. They don’t make money off loans at these rates either. In the US, interest rates are distorted by government guarantees. Politicians have decided that certain interest rates sound “fair,” then push big banks to lend money at these low unsustainable rates. But of course it doesn’t work and so government agencies sweeten the deal by reimbursing banks for up to 90% of the losses on the borrowers that default. Banks make money on the loan closing fees and other services they sell to the businesses. The loan is the doorbuster offer the bank puts in the storefront window. Once you come inside, they try to sell you on other things so that you don’t walk away with just the loan, otherwise they’re losing money.

So when you hear “banks aren’t lending,” don’t be so surprised. Lending money means giving it away to someone that might not pay it back. That’s a really tough business to be in, no matter how qualified the borrowers are or how good the underwriters are supposed to be.

But somewhere in between the opinions of the Merchant Processing Resource staff and government bureaucrats over what is fair, is a special recipe that determines once and for all what works best. It’s science. Wonga’s lending success is rooted in science and propelled by an advanced algorithm that can systematically calculate risk better than any bank in the world, or so they say.

One of Wonga’s major investors, Mark Wellport, is a knighted renowned immunologist and rheumatologist that has defended Wonga’s methods against regulation. He believes their data-based process and strong motivation to make their borrowers satisfied places them in an entirely different category than payday lenders.

One of Wonga’s major investors, Mark Wellport, is a knighted renowned immunologist and rheumatologist that has defended Wonga’s methods against regulation. He believes their data-based process and strong motivation to make their borrowers satisfied places them in an entirely different category than payday lenders.

Wonga takes a human-free approach, something no MCA provider in North America does regardless of how automated their process may seem. In the UK, their business loan application process takes only 12 minutes and the funds are wired 30 minutes later. That’s it. Their max loan is £10,000 but just think about how that compares to MCA in the US. How much time and overhead is being spent on printing documents, underwriters, conference room meetings to discuss deals, setting up the merchant interview, trying to reach the landlord, trying to get page 7 of a bank statement from 6 months ago and the signature page of the lease, etc. etc. Funders might have had the wrong approach all along.

Wonga’s founder, Errol Damelin believes in data. According to some quotes in The Guardian, Damelin believes interacting with the borrower actually impairs a lender’s judgement.

From the Guardian:

Asking for a loan from a financial institution had traditionally involved making a strong first impression – putting on a suit to see the bank manager – then rigorous questioning, checking your documents and references, before the institution made an evaluation of your trustworthiness. In a way, it was exactly the same as an interview, but instead of a job being at stake it was cash.Damelin found this system old-fashioned and flawed. “The idea of doing peer-to-peer lending is insane,” he says. “We are quite poor at judging other people and ourselves – you get to know that in your life, both with personal relationships and in business. You realise that we’re not as good as we think we are at that stuff, and that goes for almost everybody. I certainly thought I was much better at it.

The 42-year-old entrepreneur grew up in apartheid South Africa, and he believes the experience of living in that country in the 80s has had a significant impact on his outlook. He was active in student politics at the University of Cape Town and marched in civil disobedience protests. So, when it came to deciding who should be lent money, Damelin says he wanted to strip away some of the prejudice – decisions would be taken without a face-to-face meeting; you wouldn’t even speak to an adviser on the phone, because people subconsciously judge accents too. The final call on whether to hand out cash would be based on “the belief that data could be more predictive than emotion”.

According to Wired, Damelin and his team created a system to approve or decline applicants all on its own. They tested it on a site called SameDayCash by using Google Adwords and within ten minutes of their ad going live, their system had already approved its first customer. In its early forms, it wasn’t very profitable from a lending standpoint but it did allow them to collect a massive amount of data.

From Wired

its strategy over this period wasn’t just to disburse money — it was to accumulate facts. For every loan, good or bad, SameDayCash gathered data about the borrowers — and about their behaviour. Who were they? What was their online profile? Did they repay the money on time? The site was feeding an algorithm that would form the basis of Wonga, launched a year after the beta experiment that was SameDayCash.

MCA has utilized Adwords for lead generation for years with mixed success, but few have used it for the purpose of accumulating facts. This isn’t to say that the firms collecting information for the purpose of leads aren’t sitting on treasure troves of data, it’s just that none of it to date has led to 100% computerized underwriting. The MCA industry is quite possibly about to undergo a major shift in how they promote their product on Adwords as a result of Google’s ominous warning a couple weeks ago. New disclosure requirements may change the way consumers respond and apply, ultimately impacting the data collected.

So will european science work in the good ‘ol US of A? If Wonga acquires On Deck Capital, you can bet they’ll try to replicate their success. There is a gigantic market of really small businesses that aren’t getting funded, and even the ones that are, they’re waiting 3-7 days to deal with the paperwork, handle the phone calls, fax documents, complete a landlord verification, and in some cases, deal with a credit card processing equipment change. If On Deck Capital becomes a household name as Wonga is in the UK, a lot of smaller funders are going to get squeezed.

Wonga claims to have a net-promoter score above 90%, a customer satisfaction metric that beats most banks and even Apple Computer. It’s a company that seems to be winning on every front.

Critics will say that the American lending market is big enough for everyone, that the loans Wonga has done traditionally are really small and therefore not in the same league as MCA, or that their own company has something similar or better. We believe however, that if this deal goes through that it’s a bad idea to get comfortable. There are Wonga-like companies in the US already, data fortresses that will soon revolutionize how loans are issued and determine what makes a successful business. New York based Biz2Credit is one such example.

We’ve been right about a lot of things in the last couple years and wrong about some. But we believe it is inevitable that any lender ignoring the automation revolution on the horizon is not going to last very long. Go ahead, brush it aside and convince yourself that this whole Automation thing is just hype as BusinessWeek did in 1995 about the Internet. “Automation? Bah!”

As Damelin told Wired in June, 2011, “For me the epiphany was right there. People were online, looking for a solution to a problem.” Ask any funder using Adwords or pouring work into SEO and they’ll tell you the same thing. People are looking online for money. What happens after they fill out the form on the website is what makes the USA MCA/alternative lending industry different from Wonga.

But will a perfected european algorithm work in the US? Americans approach debt and money differently than the rest of the world and small businesses operate in a much more open manner. You never know, the european lab coat wearing scientists could come here and get their butts handed to them. Plenty of smart companies have jumped headfirst into MCA and left after disastrous results. Some veterans that have been in this business a long time will you tell that an impressive resumé, big investors, and a fancy algorithm will help you make it through the first six months. After that, you better know what the hell you’re doing, if you can continue to do it at all.

But will a perfected european algorithm work in the US? Americans approach debt and money differently than the rest of the world and small businesses operate in a much more open manner. You never know, the european lab coat wearing scientists could come here and get their butts handed to them. Plenty of smart companies have jumped headfirst into MCA and left after disastrous results. Some veterans that have been in this business a long time will you tell that an impressive resumé, big investors, and a fancy algorithm will help you make it through the first six months. After that, you better know what the hell you’re doing, if you can continue to do it at all.

If in three years the average small business owner thinks Wonga is the last name of a guy that owns a chocolate factory, we promise to write a jingle that admits we were wrong about them. But On Deck Capital has been around the block and knows the business. They would allow Wonga to skip the learning curve and together could quite possibly nail lending down to a science.

Oompa Loompa do-ba-dee-doo, I’ve got another algorithm for you.

– Merchant Processing Resource

../../

There is great feedback to this article in a LinkedIn Group HERE

Not an Expert in Payment Processing? Then Don’t Fund Merchant Cash Advances

August 23, 2011

If you have no experience in underwriting payment processing accounts, don’t bother becoming a Merchant Cash Advance (MCA) provider.

After a quick underwriting process, a MCA provider  purchases Business ABC’s future card sales. Business ABC receives a lump sum of capital and a percentage of each card sale is now directed back to the MCA provider. Two weeks later, Business ABC loses a $2,000 payment dispute with a customer and suffers a chargeback. Unwilling to bear any additional risk, the payment processor terminates Business ABC’s account. Business ABC can no longer accept card payments. What does the MCA provider do?

purchases Business ABC’s future card sales. Business ABC receives a lump sum of capital and a percentage of each card sale is now directed back to the MCA provider. Two weeks later, Business ABC loses a $2,000 payment dispute with a customer and suffers a chargeback. Unwilling to bear any additional risk, the payment processor terminates Business ABC’s account. Business ABC can no longer accept card payments. What does the MCA provider do?

Why did we hypothesize this scenario? Because this situation happens. The underwriting of a MCA doesn’t start with a credit score and end with a cash flow examination. The focus should be on the merchant’s future card payments. If the merchant’s ability to accept payments is at risk, then all the other factors aren’t worth diddly. You can have a client with 800 credit, processing consistent volume, have $50,000 in the bank at all times, and it just won’t matter. So what can go wrong? Your client’s funds can be frozen or their account closed in any of the following situations:

- The merchant processes a sale that is outside their approved parameters. For example: A restaurant has a $50 average ticket with a maximum allowable sale of $300. During the holidays they book a catering gig and attempt to swipe a $3,500 sale. BAD NEWS.

- The merchant is set up to swipe 95% of all card transactions but lately has been key-entering the card numbers nearly 70% of the time. BAD NEWS.

- The merchant you funded owns a retail store. His brother has a landscaping business. Occassionally the landscaping business will swipe cards through the retail store’s credit card machine and the brother will pay him the proceeds. If a business accepts payments on behalf of another business…. then BAD NEWS.

- The merchant has too many customers disputing charges. BAD NEWS.

- The merchant has insufficient funds in the bank account to cover the month end fees to the payment processor. BAD NEWS.

- The merchant processes payment far in advance of the services being rendered. BAD NEWS.

- The merchant’s average sale size is in excess of $1,000. BAD NEWS.

- The merchant swipes their own credit card through the terminal, effectively giving themselves a cash advance. This is illegal. BAD NEWS.

- The merchant has no refund policy. BAD NEWS.

- The merchant is processing with non-pci compliant equipment. BAD NEWS.

- The merchant changes their business ownership structure or legal entity type. BAD NEWS.

- The merchant takes payment for a prohibited item or service. BAD NEWS.

- The merchant has a security breach. BAD NEWS.

- The merchant violates any policy of their payment processor or payment network. BAD NEWS.

These are just a few situations that MCA providers need to be prepared for. One day everything is perfect and the next day their client’s ability to accept card payments is suspended or terminated. Historical statements can provide clues but anything can happen. A merchant with no chargeback history can have their account jeopardized with just one chargeback.

Alternative methods of collection such as direct debit and lockbox will be futile since they still depend on proceeds of payment processing. Simply speaking, if there are no more card sales, then you cannot recoup what you have purchased. And that’s the end of it.

It’s a risky business. MCA providers place an unbelievable amount of faith in their clients’ continuing ability to accept card payments. Rookies often comment that MCA providers are in a much better position to collect funds than a bank is on outstanding loans. This is outright false. A bank is entitled to payment no matter what happens to the business. Failure to pay a loan results in the reposession of collateral.

We have witnessed hundreds of MCA deals go south due to unforeseen payment processing issues. Being a funding provider may look attractive on paper, but if you think looking at the average sales volume, credit score, and cash flow history will get the job done, you’ll get smoked in this business. There’s a reason our site has two sections, Merchant Processing and Merchant Cash Advance. They go together. Don’t learn the hard way.

– The Merchant Cash Advance Resource