Lending Club Faces Pressure to Redeem An Entire Industry

May 15, 2016

In the wee early morning hours of May 3rd, I finally wrapped up the latest AltFinanceDaily story and hit the publish button. Then as I made my way off to bed, I started to second guess the headline. Titled, Is The Marketplace Lending Apocalypse Upon Us?, I fretted over whether or not it was overly sensational.

Apocalypse. Apocalypse. Apocalypse, I repeated over and over in my head.

As I tossed and turned for an hour, I worried that thousands of readers would think AltFinanceDaily was crossing over into tabloid territory. I decided to leave it up anyway, certain enough at least that the clouds forming over the horizon signaled the arrival of a dark storm.

Less than a week later, Lending Club’s famous CEO would resign in disgrace in a scandal that also brought down several other employees. The company would delay its quarterly earnings report and the stock would drop by more than 50% over the course of just a few days. Closely related companies like OnDeck would be dragged down by the news, Wall Street banks would announce suspensions of securitizations, and community banks would halt the purchases of Lending Club loans. Blackstone Group would end its planned foray into online lending and banks like Wells Fargo, smelling blood in the water, would strike at the heart of some marketplace lenders by announcing a new technology-enabled product.

Reporters from all types of media outlets would contact me to ask what I thought of it all and I spoke from my gut in some of them.

Little details would trickle out, such as a whistle-blower submission to the SEC last July over Lending Club’s disclosure practices and another board member’s stake in a little known company named Cirrix Capital would be called into question. The non-stop fearmongering headlines from the media definitely didn’t help.

Lending Club’s complete silence after Monday morning’s announcement only made it worse. Those who buy notes on their platform never received a single communication about it, a fact that might be entirely related to quiet period rules surrounding the release of quarterly earnings. For some platform users, that continued silence fed into even the most rational investors’ worst fears.

On the LendAcademy forum for example, some users argued that Lending Club could be facing bankruptcy before the end of the year. Many who were more calm but still concerned, indeed said they were refraining from purchasing new notes until they got further guidance just to be safe. Others ventured off into complete paranoia while rational minds tried to reel them back to reality. As someone who has a significant Lending Club portfolio, I found myself shifting back and forth between those roles.

Everything is fine. Or is it?! No, everything should be fine. BUT WHAT IF IT’S NOT?!!

On Monday, In what will be a semi-post-apocalyptic world, Lending Club will have a lotta ‘splainin to do. New CEO Scott Sanborn will be tasked with restoring order to the world of marketplace lending. His predecessor, Renaud Laplanche, was the face of peer-to-peer finance. He was an icon. As the four-time keynote speaker of LendIt, Laplanche’s persona assured a skeptical public that disruption in lending was true Silicon Valley innovation, not Wall Street engineering. This lending marketplace could not possibly be risky, one might have supposed, because it looked so charmingly French. The intellectual in the red vest with a degree from école des Hautes Etudes Commerciales de Paris did not look and sound like Dick Fuld from New York City. And yet Lending Club’s offense that led to Laplanche’s departure, opened it up to comparison to the shoddy mortgage origination market in the early 2000s that led to Lehman Brothers’ collapse and the Great Recession.

This week, Scott Sanborn will have to make a most convincing argument to restore belief in the movement. Regulators, legislators, investors, and borrowers alike, have pegged at least some of their perceptions surrounding fintech to Lending Club. What happens this week may very well decide the future of online lending altogether. For Sanborn, those are some very big shoes to fill, or in Lending Club’s case, it will all depend on how good he looks in his red vest.

Autres temps, autres mœurs

Godspeed.

Loan Originations Slow Industrywide

May 10, 2016

It’s not just one marketplace lender experiencing a slowdown in originations. Some of the largest players across the spectrum cooled their jets in Q1 of this year compared to Q4 of last year.

| Company | Origination Growth |

| Lending Club | +7% |

| Square Capital | +4% |

| OnDeck | +2% |

| Prosper | -12% |

| Avant | -27% |

While Lending Club weathered the storm relatively well, the resignation of their CEO amid a loan manipulation scandal does not bode well for its immediate future prospects.

Avant CEO Al Goldstein, whose company’s loan volume among the bunch dropped off the most, told Crain’s Chicago last month, “If we can’t find capital, we’re not going to grow fast. If we can, we will.”

In a later comment to the WSJ, an Avant spokesperson explained that Q4 loan volumes are typically elevated because of the holidays and Q1’s volume down because many borrowers are receiving their tax refunds.

Lending Club CEO Resigns After Shady Dealing, Manipulated Loan Application Dates

May 9, 2016

Lending Club CEO Renaud Laplanche has resigned after an internal probe revealed that all was not right with the sale of a $22 million pool of near-prime loans to a single accredited institutional investor. The pool contained loans that the investor specifically did not want. It was not a mistake. “Certain personnel apparently were aware that the sale did not meet this investor’s criteria,” said new executive chairman Hans Morris.

The Board stepped in and conducted its own investigation. During the course of it, they also found that a senior manager had manipulated the application date on $3 million worth of loans. A forensic auditor was then called in but they didn’t find any evidence to indicate that other loan data had been manipulated.

Three senior managers have also resigned or been terminated. None will be getting severance pay. Morris said that they could not disclose their identities.

Company President Scott Sanborn is now the temporary CEO.

Did Peer-to-Peer Lending Sell its Soul to Wall Street?

May 8, 2016

“We have so many fans but we also have some people here that are looking to take advantage of us, that are here for a short term trade and they won’t be part of this industry.” – Ron Suber, President of Prosper Marketplace

Ron Suber may have been talking about specific players in the capital markets when he said those words at LendIt just a few weeks ago but that characterization could just as easily apply to all of Wall Street in general. During his presentation, he offered two real world examples about how their message got hijacked by the same facilitators they originally believed were there to help them. The first was a case of bad buyers.

“When a marketplace lender sells a bunch of loans and the buyer isn’t aligned with the marketplace, if the buyer of those loans is going to buy those loans and leverage them, rate them, and securitize them every single quarter without alignment with the industry and just sell those bonds into the marketplace, […] that won’t be good for you, for the industry,” he said. “And we learned that lesson. When we don’t have alignment with our investors, when groups sell our loans into the market no matter what if the market’s not ready, it’s not good and we learned that at Prosper this year.”

Keynote Presentation by Ron Suber of Prosper at the LendIt USA 2016 conference in San Francisco, California, USA on April 11, 2016. (photo by Gabe Palacio)

What he was saying is that the buyer matters because if they’re repackaging up the product for mass consumption, it is ultimately the original seller (i.e. companies like Prosper) that is being judged for the success or failures of the product’s reception down the line.

A second example stemmed from mismatched projections. You might think it’d be a good thing if a rating agency’s own analysis of your loan portfolio projected even lower loss rates than you projected on your own. Not so, and this actually happened; Moody’s projected loss rates for the loans packaged inside of Citigroup-issued Prosper bonds were lower than what Prosper projected itself for the same vintage. So when default rates were on pace to exceed Moody’s aggressive projections (and fall in line with Prosper’s), news of an impending bond downgrade due to allegedly poor performance roiled the market. The media interpreted Moody’s adjustment to mean that something was wrong with Prosper, not that something was wrong with Moody’s initial assessment.

Suber summed these experiences up by telling the audience, “we must control our story.” That’s a challenge because Wall Street loves to commoditize things, especially loans. The value goes up, the value goes down, and Wall Street will sell it if there is a buyer for it without any regard for the story. What to do then?

CommonBond CEO David Klein said on a panel in late March that marketplace lenders will look to tap back into individual investors, that there will be a return to the industry’s peer-to-peer roots.

Fundera CEO Jared Hecht, a co-panelist, said that “retail investors are more loyal to a specific platform” and that this can create a “network effect.”

The problem of course with retail investors, aside from the steep regulatory hurdles to sell to them, is the comparably slow speed at which they allow a platform to scale. The downside for any company that takes this organic approach is that they could grow so slowly that they get eclipsed by everyone else.

But perhaps the underlying issue is that some companies that originally set out to be peer-to-peer lenders have succumbed to this identity of being “online lenders.” That’s a problem because traditional financial institutions can use technology to lend online too and the Internet will eventually become the standard medium for all lending. That means that soon being an online lender will just mean being a lender period. And if you are just a lender, well then Wall Street will indeed take advantage, control the story and charge their standard fare just for playing the game.

The price? One soul.

And once you sell yours, it’s hard to get it back.

Square Capital’s Default Rate is 4%

May 5, 2016

Square revealed today that its Square Capital division had extended $153 million through more than 23,000 advances and loans in the first quarter. The company is still transitioning from merchant cash advances to loans to appease institutional investors. This was not only said at LendIt by Jackie Reses but also reiterated in their Q1 earnings report. “We believe that the transition to a loan product further increases our ability to attract new Square Capital investors,” it said.

Their default rate continued to hover at 4%.

That number is shockingly low considering that under a pure merchant cash advance model they did not conduct credit checks, nor did even they review bank statements or tax returns. Rather the company relied almost entirely on a merchant’s sales history with Square.

This process may have made funding easy but was potentially a hard sell to regulators. As part of their transition to a lending model, all applicants are now subject to a credit approval and have to supply identifying documents. Square also bought an analytics startup less than two months ago to help them make more informed underwriting decisions. This can only mean that if their default rate was 4% with no underwriting, their prowess as a lender will likely increase considerably.

Is The Marketplace Lending Apocalypse Upon Us?

May 3, 2016

Days after rumors leaked that Prosper Marketplace had planned to lay off staff, the WSJ is now reporting that the company is indeed eliminating 171 jobs, closing their Utah office and letting go of their chief risk officer. CEO Aaron Vermut’s salary has also been cut to zero.

The timing for the industry they’re a part of couldn’t be worse. OnDeck’s stock closed down 34% today after Q1 losses and revised projections took analysts by surprise. The source of the pain? OnDeck’s “Marketplace.” The institutional investors typically willing to pay a high premium for loans disappeared, according to OnDeck executives on the earnings call.

Unsurprisingly, Prosper’s “Marketplace” has historically relied on institutional buyers for their loans too, as much as 92% of all loans on the platform in fact. Prosper’s roots as a peer-to-peer lender don’t make it an ideal candidate to just shift loans to their balance sheet like OnDeck, which could make the changing capital markets landscape even more painful for them.

Two months ago, Prosper raised the interest rates they charge, citing a “turbulent market environment.” And just weeks ago, Citigroup announced that they would no longer buy loans from Prosper to package into bonds. Now, signs of stress are finally starting to show.

And then there’s Lending Club, a “marketplace” rival to both Prosper and OnDeck, who experienced a 10% decline in its stock price today. The company’s model is under fire through a class action lawsuit that alleges among other things that they along with WebBank are Racketeer Influenced Corrupt Organizations. Lending Club plans to release their Q1 earnings on May 9th.

And it’s not just the capital markets and lawsuits shaking up the landscape. Half a dozen trade associations have been formed over the last few months to quell some of the negative rhetoric surrounding online lending in Washington and to educate policymakers on the positive aspects of these services.

In the Illinois State Senate for example, a pending bill has the potential to outlaw all nonbank business lending altogether.

Some of those that broker business loans have already fallen on hard times due to things like the cost of leads skyrocketing.

“Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify CEO David Goldin in AltFinanceDaily’s most recent magazine. “There’s going to be a shakeout. I can feel it.”

The early signs of that prediction may finally be starting to unfold.

After the Lendit Conference last month, I speculated that marketplace lending euphoria ended because the relationship between investors and platforms was in some ways based on lust, not love. The breakup is now starting to manifest itself in the form of missed earnings and layoffs.

Is the apocalypse upon us? Probably not yet, but these foreshocks are a good sign that we’ll soon be separating the wheat from the chaff.

Make sure to wear your hazmat gear as you enter the marketplace.

BlueVine a Serious Player After Citigroup Investment (And it Could Land Them Citigroup Referrals)

April 27, 2016

When BlueVine announced raising $40 Million from Menlo Ventures three months ago, they raised eyebrows in the marketplace lending community but they didn’t steal the spotlight. That’s because BlueVine’s core focus, invoice factoring, is arguably the least sexy segment of small business finance. Just hearing the phrase invoice factoring is enough to induce one into a coma. That of course is what made the age-old practice ripe for disruption. But even so, BlueVine isn’t limiting themselves to just that.

The company now offers business lines of credit with interest as low as 6.9%, according to their website. That makes them a competitor of OnDeck, Lending Club, Funding Circle and many others in a crowded field.

A new investment from Citigroup however could change everything for them. While the terms from Citi Ventures (the banks’s investing arm) were not disclosed, Arvind Purushotham, told CNBC that it’s possible that Citigroup forms a referral arrangement with BlueVine to help small business customers of the bank find attractive credit. That’s significant because Purushotham is a managing director at Citi Ventures.

Two weeks ago, OnDeck CEO Noah Breslow, told the crowd at the LendIt conference that partnering is a company’s only chance now to gain a real foothold in the industry. Breslow could speak from experience since OnDeck currently has a unique arrangement with JPMorgan Chase.

While the sources interviewed by CNBC stressed that the BlueVine-Citigroup investment did not constitute a commercial partnership, the stage seems to have been set for that to be possible in the future.

Even though BlueVine just started making loans 3 months ago (they have been factoring since 2013), loans already make up 15% of their overall business. This is one invoice factoring company that rival small business lenders won’t want to sleep on.

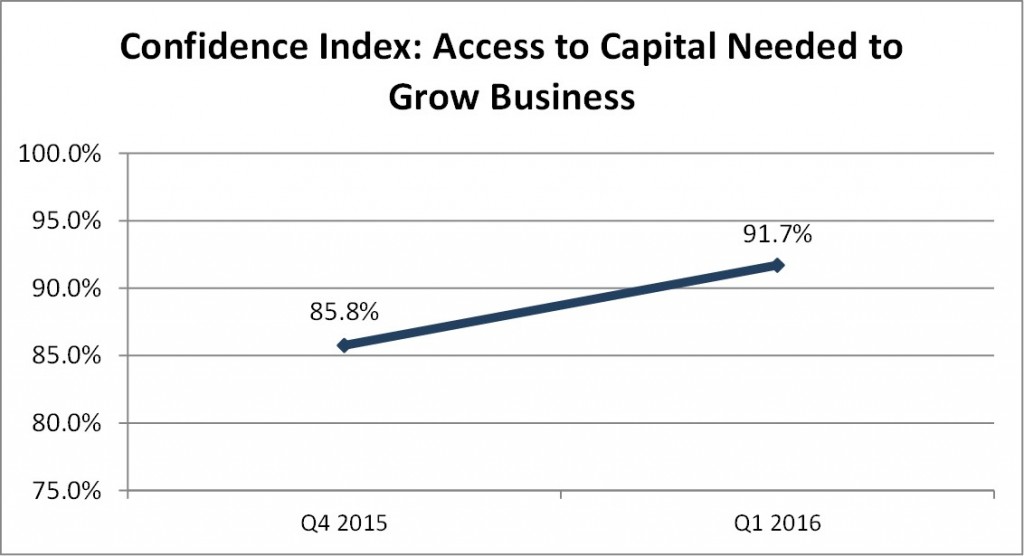

Small Business Lending and Merchant Cash Advance Industry Confidence On The Rise

April 25, 2016A fresh survey of industry captains revealed that their confidence is actually increasing.

Late last year, AltFinanceDaily and Bryant Park Capital teamed up to produce the first ever comprehensive industry report on merchant cash advance and small business lending. More recently, eligible participants took a narrower survey to gauge their confidence in Q1 2016 and that was compared to results measured in Q4 2015.

The results were striking. Despite the apparent end of a euphoric love affair between investors and marketplace lenders earlier this month at LendIt, those on the small business side are still feeling very optimistic.

Confidence among industry captains increased from 84.4% in Q4 2015 to 91.7% in Q1 2016.

Confidence among industry captains in their ability to access capital needed to grow their business increased from 85.8% to 91.7%.

The 2015 comprehensive report is available for $495. Please contact sean@debanked.com for more information.