Do Bank Statements Matter in Lending? Business Lenders and Consumer Lenders Disagree

July 16, 2015Bank statements. Those in consumer lending argue they’re all but irrelevant because FICO and credit reports do the job of predicting risk just fine, but over in today’s small business lending environment, there’s an entirely different sentiment; Reveal your recent banking history or be declined.

After having bought nearly $60,000 worth of consumer notes on Lending Club and Prosper combined, there’s something I’ve seen a lot of, bounced ACHs.

Lending Club doesn’t reveal borrower bank data to their investors. Sure, anyone can see the credit report, the income level, zip code, and job title, but the borrower could have negative $10,000 in the bank and be living off overdraft protection on day 1 and an investor would never know it.

Lending Club doesn’t reveal borrower bank data to their investors. Sure, anyone can see the credit report, the income level, zip code, and job title, but the borrower could have negative $10,000 in the bank and be living off overdraft protection on day 1 and an investor would never know it.

For all the fanfare surrounding online marketplace consumer lending, access to borrower banking history is oddly absent.

“Welcome to consumer lending, where the rules are different because the game is too,” replied a user to my comment on a peer-to-peer lending forum.

Veteran consumer lenders assumed I was a lost newbie who knew nothing about lending. “I have a feeling if you ask to crawl someone’s bank account, they’ll just go elsewhere,” one user said. “Seems that’d only work on subprime borrowers who have limited bargaining power.”

“I’m assuming you may be new to lending,” he continued. “Making a loan based on deposit balances is rarely a good idea.”

My initial question to them was that without bank statements, how could they ascertain if a borrower’s finances were actually in order at least at the time the loan was issued? It’s really easy to access someone’s banking history for the last 90 days by using common tools like Yodlee or Microbilt, I argued.

Some people sympathized with my logic but others believed requesting bank data would be suicide in today’s competitive environment. And still more wondered if there might be consumer protection laws that prevented lenders from seeing a loan applicant’s banking records (which sounded ridiculous).

A Credit Card Issuer’s Take

Those questions led me to interview an underwriting manager at one of the nation’s largest credit card issuers who would only speak on the condition of total anonymity, including the bank’s name. There, he oversees a department of people that manually assess credit card applicants. There is no algorithmic approval process. In his department, humans underwrite each application, conduct phone interviews with the prospective borrowers, and request additional documents if they feel it’s warranted.

Requesting bank statements is a regular part of the job, explained the manager. “We require proof of income for any line over 25k,” he added. “It’s the main thing we ask for along with proof of address.”

Requesting these documents keeps them compliant with the Bank Secrecy Act, he explained, but the bank statements in particular are their first choice in verifying somebody’s income, even more than pay stubs. And their underwriters aren’t oblivious zombies, he noted. If an applicant has no money in the bank, they’ll decline it.

Requesting these documents keeps them compliant with the Bank Secrecy Act, he explained, but the bank statements in particular are their first choice in verifying somebody’s income, even more than pay stubs. And their underwriters aren’t oblivious zombies, he noted. If an applicant has no money in the bank, they’ll decline it.

“The Adverse Action reason [for that] would be ‘sufficiently obligated’,” he stated. “That’s when their bank account shows they can not take on any additional financial obligations.”

The manager shared however that he believed there is a very strong correlation between what’s on the credit report and what to expect in the bank statements. Generally speaking, good credit will show a healthy banking situation, he explained. They’re rarely taken by surprise. Overall, the credit reports and phone interviews are enough for them to feel comfortable and the bank statements are really just there to check off a compliance box.

Meanwhile, those that speculated requesting bank data would be a death knell competitively might want to talk to Kabbage’s sister company, Karrot. Karrot already crawls bank accounts as part of their consumer loan application program and competes with Lending Club, Prosper, and Avant. Considering Kabbage has funded more than half a billion dollars worth of business loans using this very methodology, it’s safe to say that applicants aren’t flocking to competitors in droves over the perceived injustice or inconvenience of filling out three additional fields on a web application to share their transaction history.

Bounced Payments

Kabbage CEO Rob Frohwein offered these comments last year about their underwriting, “A critical aspect of consumer lending is determining the appropriate amount of a payment to collect so that an account doesn’t become overdrawn. Our intelligence accurately predicts how much of a payment to request via ACH so consumers avoid the cost and headache associated with non-sufficient funds.”

I thought about those statements when I noticed that thirty-six of my Lending Club notes carried a Grace Period status the other day. These are borrowers whose payments just recently bounced. Some are only three or four months into a five-year loan. Worse, there are those that are saying they have no money whatsoever to make a payment. How can this be when they just practically got approved?

To the consumer crowd it’s business as usual. “If you got their bank account, you still wouldn’t be able to predict who will default. You can’t predict defaults on any individual borrower,” argued one veteran on a forum.

But it’s not all about the lender’s tolerance for risk. ACH rejects can have consequences that affect a lender’s ability to debit accounts in the future.

“Ultimately, regulatory thresholds set by NACHA will continue to become more and more critical of returns,” said Moe Abusaad of ACH Processing Co, an ACH processor based in Plano, TX. “I think it’s safe to say that there is a positive correlation in considering statements as a component of the underwriting process to the rate of returns incurred,” he added.

And while it’s true that bank data can’t make predictions perfectly on its own, nobody in small business lending or merchant cash advance would consider an approval without it.

Bank Statements or Bust

“There is no substitute for banking information when reviewing a client for approval,” said Andrew Hernandez, a co-founder of Central Diligence Group, a risk management firm that allows business lenders and merchant cash advance companies to outsource their underwriting.

“Money moves fast through these businesses and every business is unique, so a lot more variables come into play than just having to account for the timely monthly payments of credit cards, cars, and mortgages as you find in the consumer world,” he added. “A FICO score along with other information presented in a credit report provide a detailed, historical snapshot of a client’s creditworthiness in consumer lending, and while these are great complementary tools for us to use in our underwriting process, I believe that banking data paints us a picture of its own which is absolutely essential in assessing the risk of a B2B transaction in our space.”

Those underwriting business loan deals have reported seeing applicants with open personal loans from Lending Club, which shows that the exact same borrowers are being underwritten in two different ways.

But Julio Izaguirre, another co-founder of Central Diligence Group added that, “banking transactions are essential in gauging the cash flow of the business by looking at recent and up-to-date bank volume, but it is even more important with businesses that lack historical data and cannot provide financials or other documentation to show and prove their track record.”

Translation: A lack of credit history and formal financial statements can be overcome thanks to in-depth analysis of bank account data.

“When our underwriters look at a bank statement you can get a better understanding of the business cash flow, operational cost and how the owner manages his business,” said Heather Francis, CEO of Gainesville, FL-based Elevate Funding. “The credit score is like a person’s blood pressure reading,” she continued. “It indicates there may be an issue but until lab work is pulled and analyzed you don’t know what that issue is. The bank statement is that lab work and it can tell you more about the issues behind the scenes than a credit score can.”

Greg DeMinco, a Managing Partner of Americas Business Capital based in Cherry Hill, NJ would probably agree. “FICO isn’t everything,” he shared. “Bank statements can tell a great story especially if there is upward momentum month after month, and more importantly a high ratio of deposits to requests for the advance.”

Meanwhile, the manager of the credit card issuer was surprised to hear about the high value placed on bank statements in business lending. I offered him the example of an applicant with good credit that was consistently negative in the bank because of a reliance on overdraft protection as a way to make sure all the bills were being paid. “That’s the craziest thing I ever heard,” he commented.

But over in the peer-to-peer lending forum it didn’t sound so crazy at all. “Plenty of Americans are ‘broke’, in the sense that they have negative net worth, yet they’ll continue servicing their debts for… a long time… no matter what it takes,” shared one user.

The argument seems to come full circle, that business lending and consumer lending are just different.

But to Isaac Stern, the CEO of New York-based Yellowstone Capital, the bank statements are not just about financial health. “We are literally underwriting against fraud,” said Stern, who said his office regularly receives applications with doctored statements. “Logging in [to the banks] and verifying those statements are probably the most important part of the process,” he noted.

His logic goes that a consumer that is paid a salary has a predictable stream of income and so that information along with a credit report might be enough for a consumer lender, but business revenue is less predictable and can vary practically day-to-day.

“You can’t just look at a FICO score and say, ‘this is a good a business’,” Stern explained. “The story is in the bank statements.”

Still Reviewing Paper Bank Statements? Stop

June 26, 2015 Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Technology has made it easier to create authentic looking documents and the rise in online lending seems to be bringing out the worst in people. Somebody in a desperate situation might not have the guts to look a banker in the eye and hand him a stack of fraudulent documents but they might roll the dice with somebody over the Internet they’ll never have to meet.

The fakes aren’t obvious anymore. Anyone can go online and buy doctored documents from professionals. The business is booming on Craigslist for example where fraudulent documents can be made to order in under an hour.

In the Miami area, fraud hucksters are even beginning to offer deals such as buy 2 fake documents, get 1 free.

Industry-wide, funding companies are complaining that attempted fraud is out of control. One broker recently took to the dailyfunder forum to share her frustration. “I can spot them a mile away!!! 2 different deals submitted this week with fraudulent statements!!!,” she vented.

Other brokers chimed in, sharing their stories such as a merchant whose doctored statements were only noticed because ATM withdrawals were listed with odd amounts like $90.83.

Oddly, nobody seems to be reporting this fraud to the authorities. It all seems to get swept under the rug as business as usual. Orchard co-founder David Snitkoff for example, was asked just last month about the rate of marketplace lending fraud and he apparently said, “No worries, none to date.” He seemed to be implying that fraudulent applicants are getting screened out. But that doesn’t mean people aren’t trying.

Seven months ago, merchant cash advance underwriter Pierre Mena wrote in detail about the challenges he faces in detecting fraud. He said:

Some of the more well hidden fraud can usually be found by comparing the summary page and last page of the bank statement to other statements. Typically, most banks and some credit unions offer you a snapshot of the starting balance, which should generally match up with the ending balance of the previous month. If it doesn’t, you should look for any transactions from the previous month that did not settle until the current month. If there is none, this is usually a red flag indicating that the merchant forgot that statements are continual time series financial data whose totals carry on to the following month.

-Pierre Mena, Rapid Capital Funding

A lot of these issues can be easily overcome by simply disregarding paper statements altogether. Microbilt’s instant bank verification tool for example, will allow you to pull the most recent 90 days worth of transaction data directly from the banks themselves. Funders using these automated checks swear by their effectiveness and the capability is essential for any company that wants to scale.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

Cultural differences play a role in this according to Gil Zapata, the founder of Florida-based Lendinero. Zapata recently wrote that latino business owners over the age of 45 are not accustomed to doing business over the Internet, email, fax, or phone. “This group has a high level of distrust in doing business via the Internet,” he said.

So is there a middle ground? On the dailyfunder forum, Chad Otar, a managing partner of Excel Capital Management said that he tells merchants they can change their online banking passwords after a verification. And Andy McDonald of Yellowstone Capital wrote that verifying the bank data is beneficial for the merchants too. “It protects the merchant by allowing us to check their account to make sure our pulls aren’t going to bounce,” he wrote in a thread back in April. He also added that he comes across 2-3 applications PER DAY with altered statements.

Humans can only do so much. Pierre Mena actually wrote, “Some of these statements are doctored so well that you may have to zoom in upwards of 300% to find a comma that should actually be a period to separate dollars from cents.” At this point, an instant bank verification would probably work wonders.

Online business lender Kabbage might have the best model. On their website, applicants are instructed to enter their email address followed by their bank account username and password. Their system will analyze their bank transactions and if eligible, will then ask the applicant for their first and last name. It flies in the face of all the pushback that funders claim merchants give them over data privacy and security.

Four months ago Kabbage announced they were already up to funding $3 million per day. Obviously there is an entire segment of small business owners that are sucking up whatever concerns they had about bank verifications in order to get the capital they need.

The majority of the small business financing industry is still relying on paper statements and probably shouldn’t be. If you have to zoom in upwards of 300% to find a comma that should actually be a period and if con artists are offering discounts for bulk orders of fraudulent statements, it may be time to throw in the towel and join the rest of the world in using the Internet…

The Dumbest Guy in the Room

May 11, 2015 “This is the absolute dumbest thing I’ve ever seen,” she said while raising her voice. She was visibly agitated as if someone had just attempted to pass off a child’s crayon drawing as their doctoral dissertation. I began to laugh, not at her, but at the irony of the truth she was going on about.

“This is the absolute dumbest thing I’ve ever seen,” she said while raising her voice. She was visibly agitated as if someone had just attempted to pass off a child’s crayon drawing as their doctoral dissertation. I began to laugh, not at her, but at the irony of the truth she was going on about.

“So what would need to be different in order for this to be a more viable idea? Like what would I need to change and come back with?” I asked.

“Come back?! COME BACK?! Don’t come back,” she shouted while taking my business plan and literally crumpling it into a ball and throwing it on the ground. She then got up and left. She was shaking from the rage. I was the dumbest person she ever encountered and it took effort for her not to kill me.

This experience happened to me three years ago when a NYC-based Venture Capital group sent out invitations to a free seminar and workshop. I liked the refreshing thought of hearing what VCs had to say, especially those not familiar with the merchant cash advance industry. Besides, I had a few concepts I wanted to get feedback on, and thought this would be a great opportunity to do it.

The seminar was more of a fireside chat, held by a zen-like VC I’ll refer to as Rain. He was in his mid-30s, wore a long flowy purple velvet shirt and sat indian style and barefoot in the front of the room. It was a stark contrast to the attendees in the audience, all of whom were wearing suits. Rain walked the crowd through his experience as a VC, most of which seemed to be an annoyance to him. Startups were full of personal drama of which he often got roped into. There was always a partner who was an idiot, a delusion the founder(s) couldn’t see past, or an insatiable need for additional funds.

And during the Q&A at the end, an attendee asked him if he would ever consider using a VC to raise money if he were not a VC himself. “Put the phones down guys, this stays here,” he said. “I wouldn’t.”

However confusing that might come across as, it didn’t change the energy in the room. Just about everyone who attended had an idea for a startup and desperately wanted VC funding.

Afterwards, you were allowed to schedule a one-on-one with one of their startup experts to develop your ideas further. It sounded cool and it was free, so I signed up.

I drafted up a concise business plan based upon a model that was just starting to take root in the merchant cash advance industry. It had its own little twist and I’m sure flaws too, but I believed this one-on-one would be a helpful conversation where I could get honest feedback without giving anything away to potential competitors.

Three minutes into the meeting, I was being scolded. “What do you mean it would break even for the first 2 years?!”

“Oh, well what I’m try –,” I attempted to respond. She talked over me. “You mean to tell me you would make no money in the first 2 years? Are you starting a charity?!”

“Well I was under the impress–,” I started, but she kept going. “This is the absolute dumbest thing I’ve ever seen.”

It was the hardest no I had ever gone through. I looked around the room to see if the other one-on-ones being conducted were going the same way. They weren’t. Everyone else looked to be cozying up to each other, crunching numbers, sharing laughs, and possibly on their way to even getting funded.

It was the hardest no I had ever gone through. I looked around the room to see if the other one-on-ones being conducted were going the same way. They weren’t. Everyone else looked to be cozying up to each other, crunching numbers, sharing laughs, and possibly on their way to even getting funded.

Not me though. I was the dumbest guy in the room, too dumb to even come back with something better. It was a humiliating moment considering I thought this was supposed to be an instructional meeting where the experts would essentially help you master a business plan.

As I walked out of the office towards the elevator, I noticed that even the cheery receptionist who had excitedly welcomed me in, ignored me with her head down as I walked out.

There goes the dumbest guy that ever existed, I imagined she was thinking.

My world spinning as the elevator descended, I tried to recount how it went wrong so quickly. I had showed her a pro-forma P&L that broke even for the first two years as I would reinvest 100% of the profits back into marketing to scale. I personally didn’t like it that way. I wanted to make money, but everyone around me was bleeding red and raising tens of millions along the way. I had started to believe that sacrificing any shred of profitability in exchange for growth is what got investors excited.

My expert didn’t share that view. A business that wasn’t profitable wasn’t a business. It was dumb, and not just regular dumb, but the dumbest thing that anyone ever thought of. EVER.

A couple of days later when I had shaken off the blow to my self esteem, I was thankful for the experience. She was a New Yorker to the core and so was I. I had no inner desire to start a business that didn’t make money (for the sake of disrupting or whatever), but I was being swept up in the craze of companies that were doing just that. She brought me back to reality, though she left a lasting imprint of a boot on my ass.

Three years later, companies with models similar to the one I had cooked up have raised hundreds of millions of dollars. They don’t break even. They lose money, lots of it. But they are looked upon and celebrated as some of the brightest guys in the room. Many of those guys are smarter than me and are probably executing their concepts way better than I ever could. But the lose-a-lot-of-money and grow model isn’t meant for everyone. It all depends on who you’re talking to.

In HBO’s Silicon Valley, a hit that many view as more of a reality show than a sitcom, they poke fun at a truth purveying the California startup scene. Forget profits, the show explains, just having revenues hurts your chances of raising money.

“If you have no revenue, you can say you are pre-revenue,” says the show’s billionaire Russ Hanneman. “You’re a potential pure play. It’s not about how much you earn; it’s about what you’re worth. And who’s worth the most? Companies that lose money! Pinterest, Snapchat, no revenue. Amazon has lost money for the last 20 years, and that Bezos motherfucker is the king!”

“If you have no revenue, you can say you are pre-revenue,” says the show’s billionaire Russ Hanneman. “You’re a potential pure play. It’s not about how much you earn; it’s about what you’re worth. And who’s worth the most? Companies that lose money! Pinterest, Snapchat, no revenue. Amazon has lost money for the last 20 years, and that Bezos motherfucker is the king!”

Two years ago, Bezos was worth $25 billion and was the 20th richest person in the world. Some experts might say a business model that loses money for 20 years would qualify as the new winner for dumbest thing that ever existed ever. It’s apparently just the opposite.

But once you find an investor that believes in the loss model, do you take the money and then go out and disrupt, hoping that somehow you’ll end up a billionaire?

Loan broker Ami Kassar is faced with that very dilemma. In his recent blog post, he wrote about the offer he has on the table from a VC, “While I could substantially grow my top line – the chances of making any profit are small and the chances of losing money are high.”

Fictional billionaire Russ Hanneman would surely approve, but over in realityville, Kassar is balking. “I can only speculate that they’re more interested in market share – than profits. Their investors want growth. They’re on the venture capital treadmill.”

Admittedly, I poked fun at Kassar, an entrepreneur I’ve often sparred with online. “Should I be worried that in their quest for growth they will build a train and run me over?” He asked in his blog.

Of course I linked to it in the following manner:

Kassar concludes that sustainable long term value is the only logical way forward. Is he wrong?

The current investment atmosphere where anybody with a model and a programmer is raising hundreds of millions of dollars to basically see how fast they can spend it all, is affecting those that have always believed in profits and longevity.

In another post by Kassar just a week earlier, he wrote, “Am I missing the boat and doing something wrong? That’s how I have felt lately as I’ve watched the emergence of the online small-business financing space. It seems every other week I wake up to another announcement about a company in the small-business financing space who has raised a lot of money from venture capitalists at a really high valuation.”

Just last week, consumer lending startup Affirm raised $275 million in a Series B round. Many people in the alternative lending community had never heard of Affirm but they are apparently so good that they can raise a quarter billion dollars.

Investors are scrambling. They don’t want to be left out. On multiple occasions, I have heard of investors skipping basic due diligence in a rush to capture a deal. Some of those deals blew up in a matter of weeks, others in months when they realized they didn’t even know who the owners were or what financial standing they were in.

Lending Club and OnDeck have received billion dollar valuations. That’s what everybody wants, though the market has temporarily cooled on OnDeck, a company that has lost money for almost eight straight years.

Even Shark Tank investor Kevin Harrington has gotten in on it, through his new business loan marketplace, Ventury Capital.

One thing looks certain three years after I met with that expert. The supposed dumbest thing that could ever be conceived of ever has made tons of people millionaires.

A year ago, Kevin Roose of New York Magazine wrote this of profitless startups, “They’re simply taking millions of dollars in venture capital with the hope of keeping prices low, pushing rivals out of the market, and eventually finding a way to turn a profit.” It can be predatory pricing, Roose argues. Basically large venture backed companies can sell below their cost using unlimited funds until the competition is out of business. Then with the entire market all to themselves, they can figure out a model towards profitability.

There seems to be a lot of this happening in the alternative lending space where the lenders backed by hundreds of millions of dollars are not only undercutting the competition at a loss, but they’re running lobbying campaigns that accuse their profitable brethren of being greedy and predatory. The media and general public eat this message up. There is no defense for a lender who has been accused of charging too much by one charging less even if the one charging less will need to declare bankruptcy if it does not raise a fresh round of new capital to sustain operations.

Only the rare observer can read between the lines as Forbes contributor Marc Prosser did. In his own research, he discovered that, “a company which loans money to small businesses at an interest rate of more than 50% was losing money.”

Though I won’t name names, there are a few players out there that believe the answer to their cycle of losses is to push regulatory agencies to attack profitable companies, or at least constrain them through penalties and new laws. Essentially, if it looks like they can’t win the war of attrition, then they might as well stick the government on them.

Speaking of the war of attrition, the race to bring costs to merchants down to zero doesn’t seem to be having the desired effect on the competition. In OnDeck’s Q4 earnings call for example, CEO Noah Breslow said the following:

Overall this market is still characterized by extreme fragmentation. The behavior that we see with our customers is that they might research other competitive options online but then when they actually apply to OnDeck and receive that offer, they kind of have this bird in hand dynamic, and there’s so much search cost associated with going out and looking at other places and so much uncertainty around that, they typically just take that offer that OnDeck has provided to them.

Translation: Once merchants have an offer from somewhere, they go with it. There is no price-competitive marketplace on the macro level.

OnDeck has been undercutting the entire merchant cash advance industry for years. None of their competitors have gone out of business, at least not because of a profit squeeze. Instead, everyone is growing, OnDeck included.

So why lose money?

In the case of OnDeck, they can argue that growth has allowed them to expand into Canada and Australia. They’ve forged partnerships with Prosper and Angie’s List. They’ve acquired more data because they’ve done more deals than most. And who is another billion dollar company likely to partner with in the lending space? Probably the one doing 10x the volume of everyone else, the one whose name is all over the place. They have the advantage to win the partnerships.

Five years from now, when the competition is trying to catch up in volume, all the lucrative partnerships might be snatched up already. Maybe it really is about who can spend the most the fastest. It’s a depressing thought.

Some startup vets will you tell that the most important aspect is actually the team. The CEO of 140 Proof for example has written, “You succeed or fail not on the strength of your idea or your product, but on the strength of your team. Venture capitalists fund teams, not business plans.”

With that in mind, I tried to imagine how that meeting three years ago would’ve turned out had I showed up with OnDeck’s CEO Noah Breslow and Lending Club’s CEO Renaud Laplanche in tow. “We’re going to disrupt lending,” I imagine the three of us tell the fierce startup expert.

The expert knew nothing about me. As far as she knew, I was just some random guy off the street holding a stack of papers with an incredulous plot to dominate the lending industry. I had never worked for a bank. I was young. I had no partner. I didn’t graduate from Harvard or MIT. It probably looked pretty ridiculous. “Duhhh so whaddya think?” I imagined I appeared to her.

With her guard down, she had no reason to hold back from saying what she really felt, that the plan was the absolute dumbest thing she’s ever seen.

Might the dumbest guy in the room only be that because he believed what she said? Or did she have it right all along?

The Industry’s Bad Paper

February 8, 2015 Sometimes deals go bad. But what happens next?

Sometimes deals go bad. But what happens next?

I just finished reading, Bad Paper: Chasing Debt From Wall Street to the Underworld on a recommendation from a friend. In it, author Jake Halpern walks readers through the shadowy world of consumer debt collection. It was eye-opening to say the least.

Halpern’s research uncovered that consumer debts with seemingly no original paperwork is sold, resold, and resold again to companies that the debtor never heard of and would not recognize. A debt’s record amounted to some fields on a spreadsheet where the information is not always correct and might even have been collected already by someone else.

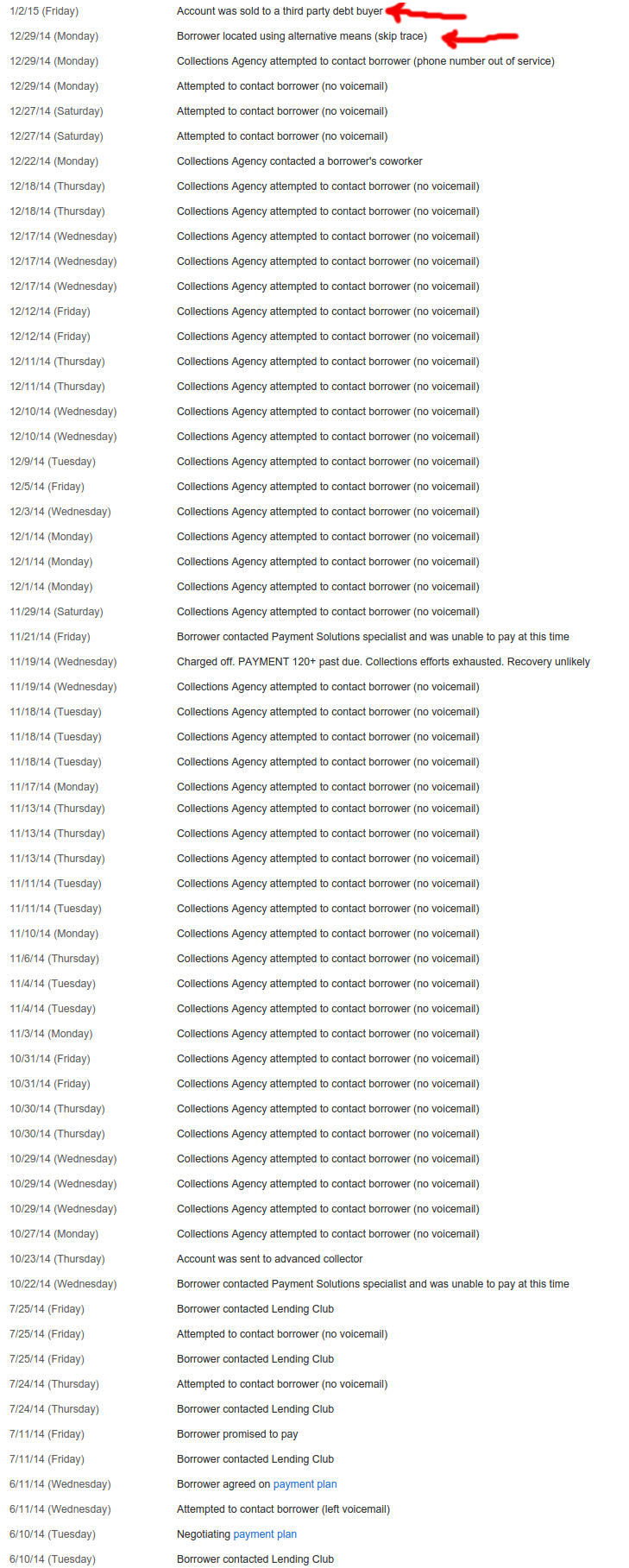

One has to wonder whose hands a Lending Club loan I participated in are in now. It was a $25,000 loan to a nurse. The notes below are from the real collections log provided by Lending Club. After making just 3 full payments on their 3-year loan, this 700 credit borrower went from negotiating a payment plan to off the grid. They called a co-worker, skip traced them, and finally gave up and sold her debt to a third party.

One has to wonder whose hands a Lending Club loan I participated in are in now. It was a $25,000 loan to a nurse. The notes below are from the real collections log provided by Lending Club. After making just 3 full payments on their 3-year loan, this 700 credit borrower went from negotiating a payment plan to off the grid. They called a co-worker, skip traced them, and finally gave up and sold her debt to a third party.

I’ve found that a lot of my defaulted loans thus far have gone bad in the first few months, a pattern that looked more like fraud than borrower hardship. It actually prompted me to call Lending Club and speak to a representative about it, who explained that they’re doing all they can to prevent fraud.

They were pretty relentless on this particular file, a nurse that was making $60,000 a year sounded like a winner. They had virtually no debt but the loan was supposedly used to consolidate outstanding debt into one monthly payment at the rate of 9.67%. The story didn’t exactly add up but since I don’t actually get to talk to the borrowers or look at their paperwork, I’m essentially just playing a numbers game.

That debt has been sold off and I as a note holder do not appear to be entitled to any money on the sale of it, not even pennies on the dollar. Bummer.

Because of platforms like Lending Club, I wasn’t the only one to lose out. 277 other retail investors who I don’t know and have never met participated in it with me. We’re all playing the numbers and we lost on this one.

With 1907 notes acquired on the platform so far, I’m not emotionally invested in any of them. How can I be? I have no idea who the borrowers are. I don’t even know their names! All I can do is diversify and make decisions based off of statistical analysis. If the borrower stops paying, go after them hard whoever they are!

Meanwhile in commercial transaction land

When it comes to merchant cash advance and business lending, the collection rules are different but so are the relationships. Even with strong advancements in automation, phone interviews remain an integral part of the underwriting process. A risk analyst typically calls the business owner, their landlord, and even several of their suppliers. Large dollar amount deals may even be presented to an entire risk committee for approval.

Suffice to say, pesky things like signed contracts do not usually prove elusive when a collector in this world gets their hands on it. Many commercial funding providers even record phone calls with the business owners where they get an additional verbal confirmation to the terms and conditions of the arrangement.

The collections process usually begins with the sales person or sales office that negotiated the terms with the business. Back when was I was an account rep, my commissions were paid in two pieces, upfront and a residual. That meant almost half my pay on a deal was tied to its performance. If a deal started to fall apart or defaulted, I had a personal stake in restoring the business to good standing.

The Fair Debt Collection Practices Act does not cover commercial transactions. And in the case of traditional merchant cash advances, there is likely no debt at all in a default, but rather a possible case of stolen receivables.

In the event where a deal I brokered was suspected of diverting receivables, I’d be the first one to know about it and the first person tasked with fixing it. That meant calls to the business, their home phones, their cell phones, and when necessary their landlord. If none worked, then their suppliers. The first goal was to determine if the business was still operating and in the vast majority of cases where defaults happened, they were.

Hardship was sometimes cited as a reason for breaching the agreement but not always. With a chunk of my paycheck on the line, I had to talk them back into good standing and unlike debt collectors, I didn’t have the ability to renegotiate the terms, lower a payment or cut them slack. It was back to the way it was or nothing.

It escalates

Some returned to good standing and others played hardball. The deal’s original underwriter might then involve themselves and if they failed, then on it went to the internal funder’s portfolio management/collections team.

This is why the situation here on out is different: Imagine a doctor sells you the accounts receivable of all his patients for a discounted price. The doctor gets cash upfront and the buyer will hopefully collect the full value of the accounts receivable to earn a profit.

Now imagine the doctor accepts your cash upfront and then also collects the accounts receivable from the patients and shuts you out. In traditional merchant cash advances, collectors aren’t going after debt, but rather acquired property that is rightfully theirs. The business has shut them out of receivables they purchased.

If internal collection efforts fail, they can attempt to freeze various receivables the business might have. Merchant processing proceeds are usually the first stop. If the business accepts credit cards, the merchant processor can be instructed to freeze all or a percentage of the revenues without a court order. This is easier said than done but it does work and there are even a few third party collection firms that specialize in this.

And if that doesn’t work? Well, thousands of lawsuits have been filed against businesses for breaching these commercial transactions. The business owners themselves can potentially be culpable and liable depending on the agreement and the nature of the breach.

And if that doesn’t work? Well, thousands of lawsuits have been filed against businesses for breaching these commercial transactions. The business owners themselves can potentially be culpable and liable depending on the agreement and the nature of the breach.

Some business owners are shocked to learn that a deal they made over the phone with people they never met will actually track them down and sue them. Unlike consumer debts which might only be a few hundred dollars, commercial transactions are typically tens of thousands or hundreds of thousands of dollars. They will definitely pursue it.

On the largest default I ever presided over as an underwriter, the business owner said something to the effect of, “I stole your money. Let’s see how good you are at getting it back.” He said this just 24 hours after we had wired him the money. Ouch!

That happened more than six years ago but it was something I’ll never forget. A quick Google search today reveals that guy is still alive and kicking as he was recently interviewed about his success in amassing a restaurant empire in Florida.

Over the next couple years, I would hear variations of that “I stole your money” line from other businesses, typically on deals larger than $75,000. These were strategic defaults designed to strong-arm the funding company into a settlement or an attempt to simply walk off with the funds altogether. In other words, fraud.

All this does is raise the cost for the next business that conducts themselves honestly. It’s a damn shame.

Merchants prey on Wall Street

Critics can say what they want about the sophistication of businesses that enter into merchant cash advance transactions. Running a business requires a great deal of intelligence. And to some savvy businessmen, Wall Street’s money is on the menu as fresh meat.

Critics can say what they want about the sophistication of businesses that enter into merchant cash advance transactions. Running a business requires a great deal of intelligence. And to some savvy businessmen, Wall Street’s money is on the menu as fresh meat.

One experience I had was with the owner of a steakhouse in NYC that flew up from his residence in Brazil to try and close me (as the underwriter) on purchasing roughly $400,000 of his future credit card sales. What he didn’t know is that the night before I checked out the place anonymously by having dinner there with my wife. When the bill came, the server told me they no longer accepted credit cards. The next morning, the owner who spoke only in Portuguese arrived in tow with a translator and a lawyer. They traveled directly from JFK to our office, to which I informed them of the decline. They had stopped accepting credit cards a day too early for their scam on us to work and the restaurant closed two months later.

In another case, a souvenir shop in NYC asked if I would come by to pick up his application and statements in person since we were locally-based. After spending a half hour with the guy at his shop, I returned back to the office only to find out that he gave me doctored bank statements.

And then there’s the owner of a florist that made a career off of robbing merchant cash advance companies. The store, which is close to my hometown, had obtained more than 20 merchant cash advances by late 2008 and defaulted on all of them, netting the business close to $1 million. They hoped to make me victim number 21 but we figured it out in the 11th hour before the funds went out. The business is still there today though I’m unsure if it’s still the same owner.

In 2015, fake documentation is an epidemic. Underwriters in the industry cannot rely on faxed or emailed statements alone. They should be verified through APIs or through direct contact with banks. Many funding providers go a step further and actually request the usernames and passwords to business bank accounts just to be absolutely sure that what they’re seeing is what they’re getting.

But as tech-savvy millenials become the face of American small business, the ante is being upped on fraud. One underwriter told me they saw something even more worrisome, a fake bank website.

The scam is this: Knowing the underwriter is going to request the username and password of the business bank account to verify the statements, the applicant has designed a functional replica of a bank website on a web domain they own, one that looks like the bank name. The unsuspecting underwriter logs in to it and verifies the account data. There’s only one problem, it’s all fake.

While this appears to be an isolated event, it just goes to show that the war on bad paper is entering another phase.

Bad paper

While fraud is a substantial cause of the bad paper in the merchant cash advance and business lending industries, hardship does have its place. It is perhaps fortunate that in the commercial space, the paper isn’t sold off into some convoluted world of debt collection. More than likely the business will be dealing with the actual funding provider the entire way through the collections process, not a debt buyer ten levels down the chain. That’s good and bad for them.

It’s good because the owner will able to discuss matters related to the default with the party directly familiar with the original contract.

It’s bad because any chance that the contract and proof of the agreement will somehow get lost in the shuffle is pretty much nil.

Jake Halpern discovered that debtors can win lawsuits by simply challenging the debt buyer to produce evidence the debt is owed. That might work in the consumer world where debt changes hands ten times. On the commercial side, bad paper is an enduring companion. It may be business-to-business but somehow it’s more personal.

Contrast that with the Lending Club nurse who I know only as Member XXXXXXX. His/her debt is in the wind. I have no idea who they are, nor anything about the 277 other people that invested with me.

Halpern spent 256 pages tracing the path of a debt, the companies that bought it, sold it, stole it, and sued for it. It’s amazing how complex it is.

If he were to do a book on bad paper in merchant cash advance, it would go like this:

The business defaulted, the funding provider tried to collect and then sued. The End.

Alternative Lending: Big Government and Big Data

May 7, 2014– Professor Michael Barr at LendIt 2014

One of the clear themes of the LendIt 2014 conference was that borrowers are willing to pay extra for speed and convenience. Regulators have taken note of this trend but they’re still supportive of the alternative lending phenomenon anyway. Truth be told, the government is acting like a weight has been lifted off its shoulders. Ever since the 2008 financial crisis, the feds have prodded banks to lend more, but they’ve barely budged, especially with small businesses. Non-bank lenders have relieved them of the stress and all they need do now is make sure everybody plays nice.

One of the clear themes of the LendIt 2014 conference was that borrowers are willing to pay extra for speed and convenience. Regulators have taken note of this trend but they’re still supportive of the alternative lending phenomenon anyway. Truth be told, the government is acting like a weight has been lifted off its shoulders. Ever since the 2008 financial crisis, the feds have prodded banks to lend more, but they’ve barely budged, especially with small businesses. Non-bank lenders have relieved them of the stress and all they need do now is make sure everybody plays nice.

Professor Michael Barr, a former US Treasury official, key architect of the Dodd-Frank Act, and Rhodes Scholar, believes the best way forward is to empower consumers. That’s something lenders can accomplish through education and transparency. On transparency, he cited many of the commendable practices that credit card companies and mortgage companies have implemented, but did not fail to note that these were forcibly instituted through regulation (Hint hint…).

When a LendIt attendee asked Barr to name someone in the alternative lending industry that is a great role model for transparency, Barr answered by saying, “I haven’t seen anyone in the industry doing things the way I would do them in regards to education and disclosure.” On the path towards transparency, “the potential is not yet realized,” he added.

While it sounded as if he favored eventual regulation of alternative lending, he offered all in attendance advice to prevent it. “Take the high road to prevent regulatory interest,” he said.

Barr’s sobering presentation also covered the Consumer Financial Protection Bureau (CFPB) and the role they might play in alternative lending, if any. Payday lenders and debt collectors were their primary supervisory targets he said, but added the “the CFPB has the flexibility in the marketplace to address problems before they occur.” That flexibility essentially gives them jurisdiction over whatever they decide they want to be in their jurisdiction.

Sophie Raseman, the Director of Smart Disclosure in the U.S. Treasury Department’s Office of Consumer Policy appealed to the industry in a different manner. “Small businesses are at the heart of the economy. We want to serve you [alternative lenders] better so that we can better serve them,” Raseman pleaded. As part of that, she came bearing gifts, a reminder that the federal government had loads of data available via APIs at http://finance.data.gov. The government wants to make sure we have access to as many tools as possible, most likely to help drive borrowing costs down. If you need to verify someone’s income, Raseman recommended the IRS’s Income Verification Express Service.

The Income Verification Express Service program is used by mortgage lenders and others within the financial community to confirm the income of a borrower during the processing of a loan application. The IRS provides return transcript, W-2 transcript and 1099 transcript information generally within 2 business days (business day equals 6 a.m. to 2 p.m. local IVES site time) to a third party with the consent of the taxpayer.

The irony with this service is the two business day timeline, though I haven’t confirmed if that’s still the case. Delays and archaic data aggregation methods are the exact things alternative lenders are trying to overcome. Kabbage comes to mind as the length of time it takes for them to go from application to funding can be as quick as 7 minutes, a time frame I found to be reality after watching the demonstration by Kabbage’s COO, Kathryn Petralia.

Kababge’s blazing speed is made possible by access to big data, which made Petralia an excellent choice to have on the Big Data Credit Decisioning Panel. She was joined by Noah Breslow of OnDeck Capital, Jeff Stewart of Lenddo, and Paul Gu of Upstart.

Stewart, whose company lends internationally presented the idea of mining not just data on social networks, but the photographs on them. One possibility was measuring whether or not borrowers appeared in photographs with other borrowers known to be bad, or whether or not they hung out with undesirables such as ex-convicts. He was a big believer in association risk, speculating that friends of bad borrowers also made them more likely to be bad borrowers themselves.

Breslow of course said you have to be careful with the noise of social media as there can be a lot of false signals. Does that mean there are big data problems then? Upstart’s Paul Gu said, “we have small data problems” in reference to why there seems to be so much trouble evaluating applicants that have little to no credit history. Gu believes that basic information such as where a borrower went to college, their major, and their grades can be used as an accurate predictor of payment performance and his company has acquired the data to back that up.

Breslow of course said you have to be careful with the noise of social media as there can be a lot of false signals. Does that mean there are big data problems then? Upstart’s Paul Gu said, “we have small data problems” in reference to why there seems to be so much trouble evaluating applicants that have little to no credit history. Gu believes that basic information such as where a borrower went to college, their major, and their grades can be used as an accurate predictor of payment performance and his company has acquired the data to back that up.

Somewhere along in the discussion though the meaning of automation got twisted. OnDeck for instance has an automated process, yet humans play a role in 30% of the loan decision making. Does that mean they are not actually automated? Breslow clarified that aggregating data from many different sources using APIs and computers was automation and that there was still a role for humans. The goal is to make sure that humans aren’t doing the same things that the computers are doing.

“The world’s greatest chess human can beat the world’s greatest chess algorithm,” said Lenddo’s Stewart. “Humans should be pulling what the algorithms can’t think of,” added Breslow. He presented an example of an applicant satisfying all of an algorithm’s criteria but sending up a red flag at the human level. “Why would the owner of a New York restaurant live in California?” Breslow asked. That’s something an algorithm might get confused about. It might mean nothing or it might mean something.

“The world’s greatest chess human can beat the world’s greatest chess algorithm,” said Lenddo’s Stewart. “Humans should be pulling what the algorithms can’t think of,” added Breslow. He presented an example of an applicant satisfying all of an algorithm’s criteria but sending up a red flag at the human level. “Why would the owner of a New York restaurant live in California?” Breslow asked. That’s something an algorithm might get confused about. It might mean nothing or it might mean something.

“Algorithms are probabilistic,” Stewart reminded the audience. They spell out the likelihood of repayment, they don’t guarantee it.

For Kabbage, algorithms and automation have been instrumental in allowing them to scale. “I don’t need to hire a lot more people to serve a lot more customers,” Petralia explained.

“Let the data speak for itself,” Breslow proclaimed. And there is a lot of statistically interesting data. “People with middle names perform better than people without them,” added Breslow.

For Gu, borrowers with degrees in Science, Technology, Engineering, and Mathematics fare better than their academic peers, though he wouldn’t reveal which major is #1. That information, while probably available to OnDeck, likely plays little or no role. “There is a lot more data to analyze on the business side than the consumer side which is why [things like] the social graph is a little less relevant,” Breslow said.

In the end, lenders don’t need to go on a wild data goose chase to learn all about their prospective clients. Kabbage applicants for instance are asked to provide their online banking credentials in the very first step of the applications. “A lot of people would be surprised as to the amount of data borrowers are willing to share,” Petralia proclaimed. Indeed, many alternative business lenders and merchant cash advance companies are analyzing historical cash flow activity using third party aggregating services like Yodlee, something that requires the client’s credentials.

During Kabbage’s earlier demonstration, some members in the audience worried that factors such as deposit activity could be gamed. Petralia assured them that their algorithm was sophisticated enough to detect manipulation and at the same time explained that they analyzed far more than just deposit and balance history.

Perhaps all this technology though has gone overboard. Is it possible to predict performance just based on what the applicant says? Believe it or not, “the language someone uses is an indicator of default probability,” Stewart said. But even that kind of detection has become automated. “Lenddo uses semantic analysis. People tend to use different words when they’re desperate.”

Who knows, a year from now getting a loan might be as easy as picking up your phone and saying, “Siri, send money.” Just make sure to delete all the photos of you hanging out with criminals off your phone first. A lender might use them against you.

Would You Fund This Business?

April 12, 2014 Is the site inspection dead?

Is the site inspection dead?

One of the strangest byproducts of the automation age is that underwriting tools once deemed absolutely essential are being replaced with APIs, digital verifications, and algorithmic scoring. Speed is everything, but why?

Faster speed through automation allows for scaleability. The promise of speed to a potential customer also encourages them to apply. Working capital can be an impulse decision now. You don’t even need to leave your chair to get $80,000 for your small business. But who’s making sure these businesses are sound… or more importantly, that they even exist?

I learned through conversations at Transact 14 that there is a growing dependency on Google Earth for site verification, more specifically Street View. Really??? Street View?!

While tech heavy funding companies laud real-time data through hundreds of APIs, it’s amusing to think that something like Street View, which might not be updated for months or years at a time, suffices as a site verification. Indeed, Street View still shows Christmas decorations in my home town.

Google Earth can pinpoint the obvious things like showing you something is located in the middle of nowhere:

But can it show you this sign located inside?

And how would you know if the writing was literally on the wall if it just went up yesterday?

Or that everything is completely on the up and up except that the business will be:

If you had the chance to speak with Jason Fullen or Joe Volk at NVMS during Transact 14, you’d know that site inspections performed by real live humans can be done in the same day they’re ordered. Or if you were getting wild at the Quiktrak party, you’d know that many of the older merchant cash advance companies still rely on site inspections, particularly on large deals.

How dumb would you feel if the $150,000 deal you funded looked like this on the inside?

Investigate a little

Who better to know the scoop on the business than the locals? I am reminded of the time a $100,000 deal I worked on where the site inspector commented that a restaurant was actually a front for a brothel that was likely going to get shut down.

I also recall almost funding a $100,000+ supermarket until the site inspection revealed that all of the shelves in the store were empty. I guess that merchant wasn’t lying when they said they needed the money to buy inventory!

And there was my own personal trip to a Brazilian Steakhouse for the final approval on an MCA deal based on credit card transactions. The server politely informed me at the end of my meal that the establishment no longer accepted credit cards as of a few days ago. How convenient…

Can social media be our eyes?

In the social media era, it’s almost as if a million site inspections are being conducted every minute. Can reviewer data be our eyes?

If there are too few reviews or they’re aged, can you rely on all your other data points? Can you trust that the available reviews are from real customers?

Speed is king these days, but ignorance is never in style. One has to consider if they can trust external data versus what they see with their own two eyes. We’ve all seen deals that looked great on paper, but turned out to be complete

After further review of the deal:

Should we fund businesses we never see? It’s your call.

Alternative Lending: People are Finally Getting it

September 12, 2013 Alternative lending is all the rage these days and so much so that BusinessWeek asked the question: What Do Small Businesses Need Banks for Anyway?. They go on to name many companies with ties to the merchant cash advance industry, which is no surprise to us of course. It is interesting however to notice that the mainstream media is not only giving us the time of the day, but starting to treat us like royalty.

Alternative lending is all the rage these days and so much so that BusinessWeek asked the question: What Do Small Businesses Need Banks for Anyway?. They go on to name many companies with ties to the merchant cash advance industry, which is no surprise to us of course. It is interesting however to notice that the mainstream media is not only giving us the time of the day, but starting to treat us like royalty.

Five and a half years ago this very same collective of lenders were referred to as bottom feeding vampires¹. Over the next couple years they upgraded us to a very expensive alternative, then to an acceptable alternative, and now finally to who the hell needs banks when you have these great companies?!. You have to laugh just a little bit at the shift.

It’s easy to call a lender that charges high rates a bad seed when you have no sense of the context. The reality in lending is that a material amount of borrowers don’t make their payments on time or they don’t pay back the loan at all. That causes rates to go up to compensate for the losses. Critics argue that borrowers can’t make the payments or default because the rates were too high to begin with. Some lenders cave to that assumption and position themselves as a fair lender by undercutting the market rates. They eventually learn that defaults are less related to the cost of the loan and more so tied to a borrower’s willingness to repay or ability to repay. Meaning, loans with no interest tacked on to the principle will still be rocked by late payers and defaults. Wait, seriously?

Yes, welcome to America where sometimes borrowers face circumstances beyond their control or they maliciously decide they don’t want to pay. The overwhelming majority are in the former camp, the ones where sudden or gradual hardship is interfering with their ability to make good on their commitment. I admit, even I feel uncomfortable mentioning this. Nobody wants to be seen as picking on borrowers. We’d all rather pretend that lenders are inherently bad and borrowers are inherently innocent. The truth is that most lenders and borrowers are good but some lenders and borrowers are bad. Lending is a two way street and what’s fair for all is somewhere in the middle.

My friends in the commercial banking sector tell me their tolerance for bad debt is less than 1%. Even 1 single loan default over the course of a year could cause their entire portfolio performance to come crumbling down. They do make loans, but they’re often in the tens of millions or hundreds of millions of dollars and only to large established businesses that quite often, don’t even need the capital but would rather not jeopardize their liquidity by spending their own cash. Some of these loans end up getting classified as small business loans even though there’s nothing small business about them.

Mom and pop shops see the statistics and the corresponding rates of say 4% to 10% APR and set that as the bar to shoot for. Then they head down to their local bank and hit a roadblock. The average small retail/food service business is going to have a greater than 1% chance of default no matter how good it looks on paper. I mean think about it, what are the odds that things will go 99% as planned for a restaurant over the next 12 months? Do you think it’s reasonable to assume there is at least a 5% chance that any of the following could happen in the next year even without knowing anything specific? A failed health inspection, bad reviews published online, a revoked liquor license, construction outside impeding pedestrian traffic, internal damage caused by a flood or disaster, extreme weather hurting sales, major job losses in the area leading to people having lower disposable income, key employees quitting, theft, landlord not renewing the lease, competitor opening up in the neighborhood, or declining sales for no single identifiable reason? Lending money to retail businesses is risky, really risky. Suppose the above business owner had a history of late payments and defaults to begin with. At what cost does it begin to make sense to do this deal? And those are just the risks of what could happen to the business itself, so what about the other risks involved?

To a bank, the stereotypical entrepreneur is damaged goods. The hard knock humble beginnings of turning a vision into a successful business usually comes with personal financial sacrifice and in turn a lower credit score. And just as the successful entrepreneur is getting ready to explain his/her high debt to income ratio and story of triumph, they’re already being declined. Banks don’t care about the story. They care about the aggregate mathematics. If there’s just a 5% chance that the business isn’t going to be where it thinks it will be in a year from now, then the deal’s probably a non-starter. Leveraged? Declined. Poor credit? Declined. Business is running smoothly? Who cares, it’s declined already!

Extension on your taxes? Declined. Showing modest profit or a loss for tax purposes ::wink wink:: ? Declined. Didn’t file a tax return? Declined. Co-mingling funds with your personal finances? Declined. Overdrafts or NSFs? Declined. Unaudited financials? Declined. No collateral? Declined. Doing the books with paper and pen? Declined. Have less than 5 employees? Declined. Can’t find a document the bank wants? Declined. Need the money really badly? Declined. Experiencing a downturn? Declined. Have a tax lien? Declined. Have a criminal record? Declined.

Extension on your taxes? Declined. Showing modest profit or a loss for tax purposes ::wink wink:: ? Declined. Didn’t file a tax return? Declined. Co-mingling funds with your personal finances? Declined. Overdrafts or NSFs? Declined. Unaudited financials? Declined. No collateral? Declined. Doing the books with paper and pen? Declined. Have less than 5 employees? Declined. Can’t find a document the bank wants? Declined. Need the money really badly? Declined. Experiencing a downturn? Declined. Have a tax lien? Declined. Have a criminal record? Declined.

Get the picture? If you take a look at Lending Club, an alternative lender, they’re widely known to have a 90% decline rate. Their maximum interest rate is 29.99% APR. Think about that for a second. Some people would say, “WOW, 30% are you kidding me?” but statistically, Lending Club would be losing money on the deal 9 times out of 10 if they approved every single person that applied. Lending Club actually used to be more liberal with their approvals when they first started and what happened is that too many borrowers just didn’t pay. If you believe that Lending Club should approve even more loan applications than they already do, then they would have to compensate for the increased risk and we’d quickly see APRs reach well into the 40s,50s,and 60s.

A critic might argue that once an applicant exceeds the risk of a 30% APR loan, they probably shouldn’t be getting a loan from anyone. That’s not a bad suggestion and what happened is that when the lending world concurred with that 5 years ago, Americans and politicians went up in arms because “Banks weren’t lending.” No loans? Businesses can’t hire. No loans? Businesses can’t grow. No loans? Economy gets stuck in neutral. The nation demanded that capital flow despite the risks presented to the lenders. And so the finance world heeded the call to provide solutions and came up with a smorgasbord of financial products. Merchant Cash Advance financing was already established but had an especially unique characteristic that allowed it to take off. It structured financing as a sale, not a loan. A big problem was that traditional lenders and alternative lenders were at the mercy of state regulated interest rate caps. Once an applicant reached a certain risk threshold, they just couldn’t do the deal anymore. But when financial companies came in to buy future revenues in exchange for a large chunk of cash upfront, the system started to gain some traction.

The effective cost of the money got high, very high, yet they weren’t predatory. I say that because despite how expensive it seemed, most of them were getting eaten alive by defaults. From 2008 – 2010, many merchant cash advance companies filed for bankruptcy. One of the main attributes of a predatory lender is for the lender to actually be getting filthy rich. That means layering on interest way in excess of a healthy profit. Losing a lot of money to help borrowers and small businesses when no one else will can hardly describe a predatory lender.

One has to wonder that perhaps there is a better way. If unsecured financing breeds high defaults, then surely things would be different if a risky applicant secures the loan with collateral. Have the borrower put skin in the game and we’d have a different outcome right? Lenders such as Borro publicly describe their default rate as falling between 8-10%. They offer collateralized personal loans and are described as a “pawn shop for the posh” in the below video, though most of their clients are small business owners. This tells me that even in the instance where borrowers have something very valuable to lose, a significant percentage of them will not repay the loan in full regardless.

A look around at what merchant cash advance companies have been willing to admit has put their average bad debt between 2-5%. In my experience in this industry however, 8% – 15% is a lot more realistic. But are these funding companies getting filthy rich or treading water? Anyone can look at the financial statements of IOU Central², a lender that’s part of the broader merchant cash advance industry. Since they’re owned by a publicly traded company in Canada, we get to see firsthand that they’re suffering tremendous losses quarter after quarter. I find that to be perfectly in line with what I suggested about undercutting the market earlier. IOU Central’s allure is that their loans cost less than a traditional merchant cash advance. The end result is that after paying commissions to sales agents, paying interest on their capital, and factoring in bad debt, they’re hurting pretty badly.

On Deck Capital too, a company mentioned in the BusinessWeek article above acknowledges that they are not profitable, though they do not make their financials public to verify how unprofitable they are or if that’s really even the case.

An SBA loan through a bank may cost approximately 5.5% APR, but if the loan goes bad, the SBA covers almost all of the bank’s losses. There is no such security blanket in the real private sector. The market determines the rates based on the risk. Each funder measures risk differently and in 2013, there is no longer a one-size-fits-all cost of unsecured funding much like there was in 2007 with merchant cash advances. Compared to a bank loan, almost all of these alternative options will be perceived as expensive, but if banks don’t approve anyone, then they’re a terrible standard for a comparison.

It’s taken a long time for the public and the media to come to terms with that. Banks are still technically in the game but by proxy. They are financing numerous alternative lenders and merchant cash advance companies. Banks shouldn’t be lending out their client’s deposits to really risky businesses anyway. A bank is supposed to be safe. If they’re lending money to 100 businesses and 15 of them aren’t paying it back, then that’s the opposite of safe.

So what do small businesses need banks for anyway? Checking, payroll, overdraft coverage, debit cards, wires, record keeping, CDs etc. There is a place for banks in 2013 and beyond. Alternative lenders charge more and that’s okay. Ultimately it’s up to the borrowers to decide what they can sustain. It is better to have expensive options than no options at all. There’s endless proof of that when credit dried up five years ago. Small businesses cried foul so the market reacted. And here we are now with Kabbage, On Deck Capital, Business Financial Services, and Capital Access Network being portrayed as the norm, the new standard. Almost everything that would cause a bank to say “no” can be resolved in some way. That’s incredible and how it should be.

So what do small businesses need banks for anyway? Checking, payroll, overdraft coverage, debit cards, wires, record keeping, CDs etc. There is a place for banks in 2013 and beyond. Alternative lenders charge more and that’s okay. Ultimately it’s up to the borrowers to decide what they can sustain. It is better to have expensive options than no options at all. There’s endless proof of that when credit dried up five years ago. Small businesses cried foul so the market reacted. And here we are now with Kabbage, On Deck Capital, Business Financial Services, and Capital Access Network being portrayed as the norm, the new standard. Almost everything that would cause a bank to say “no” can be resolved in some way. That’s incredible and how it should be.

People are finally getting it.

– Merchant Processing Resource

../../

MPR.mobi on your iPhone, Android, or iPad

¹ It took 5 years but Forbes has Finally deleted the March 13, 2008 article that haunted the merchant cash advance industry forever. In Look Who’s Making Coin off the Credit Crisis, Maureen Farrell referred to merchant cash advance companies as vampires that were feasting on small businesses and singled out some of the biggest names in the business at the time. It was Global Swift Funding* (GSF), one of the major funders cited by Farrell that exposed this assertion to be blatantly false. Not too long after the article was published, GSF closed their doors and filed for bankruptcy. It would seem that small businesses actually feasted on them by defaulting in record numbers. Back in April of this year, Forbes essentially rebuked that article when Cheryl Conner revisited the industry to note how much good it was doing in ‘Money, Money’ — How Alternative Lending Could Increase Your Company’s Revenue in 2013

*Disclosure: Raharney Capital, LLC the owner of this website currently owns the former domain of Global Swift Funding (GlobalSwiftFunding.com) though the companies did not have and do not have any ties to each other.

² IOU Central is a subsidiary of IOU Financial Inc. Management’s Discussion and Analysis of Financial Condition and Results of Operations as of August 22, 2013 are available at: http://cnsxmarkets.com/Storage/1563/144040_MDA_%282Q2013%29_-_FINAL.pdf

8 Advances Are Better Than 1

September 11, 2012Things just got interesting. Your merchant processing $20,000 a month got approved for $26,000 and it was hard fought. Bad credit and some other issues would normally have forced this deal to go the starter route, but not this time. This time you can reflect back on the past few weeks of sweet talking the underwriter and know that it’s starting to pay off. Maybe it was the fact that you obnoxiously concluded every e-mail to him or her with a <3 or 🙂 just to make them feel extra special even if it was in response to a deal of yours they moronically declined.

I understand why you had to decline my client with 720 credit. We’ll get the next one! <3 :-)

And now this time you’re chalking up a tally on the closer board for a deal that shouldn’t have gotten done…that is until your client claims to have received a contract for $50,000 from another source. “There’s no way that can be true,” you tell them while rolling your eyes in frustration. This always happens at the finish line. Someone comes in and shouts out wild figures just to steal their attention away for a minute. But what if there really was a company offering 250% of processing volume to merchants who teeter on the subprime/starter threshold?

Sure there are ACH funders out there who will step in and say “based on their gross sales we might be able to give this merchant 500% of their processing volume!” and the like, but very few people are doing this from a split processing perspective.

We’ve been speaking with Heather Francis at Merchant Cash Group (MCG) and they plan to formally announce the details of their Fast Funding Equity program in the next couple of weeks. Without going into all qualifying parameters merchants must meet to be eligible, we’ve learned that these advances will be disbursed in 8 fixed monthly installments rather than the entire lump sum upfront. And that’s the catch. Under this program the merchant might be contracted for $50,000 but only receive a deposit for $6,000 today. However, there would be no future “renewal agreements” to negotiate or sign. Additional funds would be sprinkled into the merchant’s bank account on a near constant basis of every 6 weeks.

MCG might not win the deal every time with this program but they’re going to give a lot of account reps a run for their money. We all know the pitch of verbally promising additional funds in 3-6 months from the date of the initial advance, which is based mainly on hope that the account will perform and that the funder won’t play games. Put that up against 7 renewals in writing and it’s fair to say we’ve got a good match on our hands. There are some other special incentives for MCG account reps on the Fast Funding Equity program that are being leaked on the DailyFunder Forum.

———————————

G-Day

Today was G-Day in the Merchant Cash Advance arena. GoDaddy.com’s servers were taken down singlehandedly by a jerk (let’s be real here) in the hacker group known as Anonymous. But this time we couldn’t all point and laugh like when it happened to Sony, Yahoo, or LinkedIn. No, this time thousands of MCA agents, underwriters, and staffers wondered why they stopped receiving e-mails after 2pm EST. This time Internet leads stopped coming in, internal databases stopped responding, and websites stopped loading. This time we learned that almost everyone uses GoDaddy for something no matter how much they brag about their systems and technology.

Today was G-Day in the Merchant Cash Advance arena. GoDaddy.com’s servers were taken down singlehandedly by a jerk (let’s be real here) in the hacker group known as Anonymous. But this time we couldn’t all point and laugh like when it happened to Sony, Yahoo, or LinkedIn. No, this time thousands of MCA agents, underwriters, and staffers wondered why they stopped receiving e-mails after 2pm EST. This time Internet leads stopped coming in, internal databases stopped responding, and websites stopped loading. This time we learned that almost everyone uses GoDaddy for something no matter how much they brag about their systems and technology.

We didn’t take a poll of which companies were affected (we couldn’t because our e-mail was down!), but we did participate in the mass hysteria with several other people that were affected. As this very website went down around 2pm today, we lost contact with our database and e-mail servers. One ISO reported that their website, e-mail, and even their VOIP phones were down (You can have GoDaddy phones?). Another reported that their system was so connected to their GoDaddy servers that they couldn’t even print, scan, or fax! If you’re not a fan of Mondays, today was certainly a good day to make up an excuse to leave early. With systems crashing nationwide, chances are your stapler may not have been stapling right and your boss would have had no choice but to send you home.