Good Funding Announces Closing of up to $30 Million Credit Facility

May 19, 2021 Transaction Represents Company’s Inaugural Institutional Financing

Transaction Represents Company’s Inaugural Institutional Financing

TUSTIN, Calif., May 19, 2021 – Good Funding, LLC (“Good Funding”), a recently-launched small business finance company, has closed on a $20.0 million senior revolving credit facility with a U.S.-based, credit focused asset manager. The agreement includes an accordion feature with the option to increase the credit facility to $30.0 million. The transaction represents Good Funding’s inaugural institutional financing. Proceeds will be used to increase the Company’s funding capabilities and execute its strategic growth plan.

“We are thrilled to have closed on this first round of institutional financing,” said Jason Osiecki, Co-Founder and President of Good Funding. “This credit facility will allow us to accelerate the growth of our funding platform, expand our team, and ultimately empower even more small businesses to move forward.”

“With less than a year in business, in the midst of a pandemic that is still negatively impacting America’s small businesses, we view this investment as a strong endorsement of what Good Funding can accomplish,” said Co-Founder and CEO of Good Funding Ben Gold. “Closing on this credit facility validates our mission to transform the way small businesses access the capital they need to grow and thrive. We cannot wait to put this investment into action.”

Brean Capital, LLC served as the Company’s exclusive Advisor and Placement Agent in connection with this transaction.

About Good Funding, LLC

Founded in 2020, Good Funding is a privately-held financial services firm that provides alternative funding resources to America’s small businesses. Our products are designed for business owners who cannot access working capital through traditional methods, or simply need funding with a rapid-fire turnaround. Good Funding allows entrepreneurs, start-ups and established businesses to build self-reliance and a brighter financial future.

Media contact:

Jenny Alonzo

VP, Marketing

714.384.7189

jalonzo@goodfunding.com

Canada’s Top Lending Leaders of 2021

December 16, 2020 The Canadian Lenders Association released its 2021 Leaders in Lending awards. The association is the voice of Canada’s lending ecosystem and represents more than 100 companies in commercial and consumer lending.

The Canadian Lenders Association released its 2021 Leaders in Lending awards. The association is the voice of Canada’s lending ecosystem and represents more than 100 companies in commercial and consumer lending.

All CLA members are vetted and accredited based on their corporate standards

and values. Their role is to support the highest level of lending in Canada,

servicing a wide spectrum of business and consumer borrowers’ growth requirements.

See previous year’s leading lending companies

See previous year’s leading lending executives

2021 Award Winners:

Lending Woman of the Year

|

Tiffany Kaminsky | Co-Founder of Symend

Tiffany Kaminsky is the co-founder of Symend, a fintech that uses analytics and behavioural science to create individualized debt recovery programs. The startup, which has offices in Calgary, Toronto and Denver, received USD $52 million in funding earlier this year and plans to hire up to 200 more roles in 2021. |

|

Nicole Benson | CEO of Valeyo

Nicole Benson is the President & CEO of Valeyo, a business solutions provider to financial institutions in Canada. Nicole drives every facet of business forward, with a focus on growing, evolving, and innovating Valeyo’s suite of solutions to meet the changing needs of its clients and the financial services industry. |

|

Andrea Fiederer | CMO of goeasy

Andrea Fiederer is EVP & CMO of goeasy, a leader in non-prime financial services with over 2000 employees. Andrea is responsible for goeasy’s overall marketing and brand strategy for both the easyhome and easyfinancial business units. |

|

Elena Ionenko | Co-Founder of Turnkey Lender

Elena Ionenko is the Co-Founder of Turnkey Lender, a loan origination platform. Under Elena’s leadership, the company has entered 50+ local markets, raised over $3.5 million in venture capital and launched regional offices all over the globe. |

|

Minal Shankar | CEO of Easly

Minal is the CEO of Easly, a SR&ED financing firm. This year Minal has doubled Easly’s capital under management & customer base. Prior to leading Easly, Minal was an investment manager for the VC firm Northgate Capital and an associate in the Technology Investment Banking group at J.P. Morgan Chase. Minal holds an MBA from the NYU Stern School of Business. |

Fintech Innovator the Year

|

Flinks

Flinks is a data company that empowers businesses to connect their users with the financial services they want. |

|

REPAY

REPAY is a leading provider of vertically-integrated payment solutions. |

|

VoPay

VoPay seamlessly connects you to the banking ecosystem enabling anyone to offer efficient and simple bank account payment processing. |

|

Fundmore

FundMore.ai is an automated underwriting system that uses machine learning to streamline the Pre-Funding process for loans. |

|

Provenir

Provenir offers a suite of risk analytics tools for lenders to make adjudication faster and simpler. |

Executive of the Year

|

Jason Mullins | CEO of goeasy

Jason Mullins is the President & CEO of goeasy, a leader in non-prime financial services with over 2000 employees. Since joining goeasy in 2010, Jason has helped the company scale to $1 billion in market capitalization with compound earnings growth of 28%. Jason is a recipient of Canada’s Top 40 Under 40 Award. |

|

Wayne Pommen | CEO of PayBright

Wayne Pommen is the CEO and Founder of PayBright, a Canadian leader in the BNPL space. His firm has partnered with 7,000 domestic and international retailers, and has approved over $1 billion in consumer credit. This year PayBright was acquired by Affirm in a $340 million transaction. |

|

Lawrence Krimker | CEO of Simply Group

At just 33 years of age, Lawrence Krimker has built Simply Group into a category leader in home equipment financing. This year his firm acquired competitors Dealnet & SNAP Financial in transactions that totalled over $750 million and brought his firm to $1.45 billion in assets under management. |

|

Andrew Graham | CEO of Borrowell

Andrew Graham is the CEO and Co-Founder of Borrowell, Canada’s first fintech to provide free credit monitoring. This year Andrew launched Borrowell Boost to help the 53% of Canadians living paycheck to paycheck meet their bill payments. |

|

Maria Soklis | President of Cox Automotive

In the 6 years that Maria Soklis has led Cox Automotive Canada, the company has become a category leader in software and financing solutions for consumers and dealers across the country. Maria has also left her mark with initiatives that promote diverse and inclusive workplaces, and this year signed the BlackNorth Initiative CEO Pledge. |

Emerging Lending Platform of the Year

|

Moselle

Moselle is a digital platform that simplifies the importing workflow for small medium business owners. |

|

Moves

Moves is a financial services platform for independent “gig” workers. |

|

Vendor Lender

VendorLender is Canada’s first POS lender for dealers in the equipment finance space. |

|

Lendle

Lendle is Canada’s first interest free credit provider. |

|

goPeer

goPeer helps everyday Canadians to achieve financial freedom through Peer-to-Peer Lending |

Small Business Lending Platform of the Year

|

Merchant Growth

Merchant Growth is a leading Canadian financial technology company that specializes in small business financing. Over the past decade, Merchant Growth has supported Canadian businesses with hundreds of millions of dollars in growth financing. |

|

Loop

Launched this year, Loop builds credit & payment products specifically for online merchants. The company is operated by the LendingLoop team that popularized P2P lending in Canada. |

|

Thinking Capital

Thinking Capital is one of Canada’s best known fintech lenders to the small business sector. This year the firm has forged relationships with multiple Credit Unions and hit $1 billion in loans deployed. |

|

OnDeck

Since its launch in 2015, OnDeck Canada has |

| Clearbanc

Canadian based Clearbanc is the world’s largest e-commerce funder. Their data-driven approach takes the bias out of decision making. Clearbanc has funded 8x more female founders than traditional VC. |

Consumer Lending Platform of the Year

|

Flexiti

Flexiti is a leader in point of sale financing for retailers and has been named one of Canada’s fastest growing companies two years straight. |

|

CHICC

CHICC is one of the country’s leading rental & homeimprovement financing companies. |

|

Marble Financial

Marble uses fintech to empower Canadians to improve their credit score, manage debt, and budget to achieve financial goals. |

|

PayBright

PayBright is one of Canada’s leading buy now, pay later providers. This year the firm was acquired by BNPL giant, Affirm for $340 million. |

|

goeasy

Canada’s leading alternative financial services provider servicing non-prime Canadians through its easyhome and easyfinancial divisions. |

Auto Lending Platform of the Year

|

GoTo Loans

GoTo Loans is a fintech lender focused on helping consumers access the equity from their vehicle and the leading provider in Canada for automotive repair loans. |

|

Auto Capital Canada

AutoCapital Canada is a national auto finance company that works with dealer partners to help clients finance the purchase of new and used vehicles. This year the firm acquired competitor Rifco. |

|

Carfinco

The Western Canada based lender is a leader in non-prime lending to the auto sector. |

|

Canada Drives

Canada Drives is a leader in fintech auto lending. This year the firm hit over 400 employees and 1 million transactions, servicing consumers across Canada, the US, and the UK. |

|

Clutch

Clutch aims to bring speed and convenience to used car sales by taking the experience completely online. The fintech raised a $7 million round this year from Real Ventures. |

Technology Lending Platform of the Year

|

BDC

Launched only five years ago, BDC’s Tech Group has become a leader in lending to Canadian technology entrepreneurs. |

|

TIMIA

TIMIA is a specialty finance company that provides growth capital to technology companies in exchange for payments based on monthly revenue. |

|

Flow Capital

Flow Capital Corp. is a diversified alternative asset investor, specializing in providing minimally dilutive capital to high-growth businesses. |

|

Venbridge

Venbridge is a Canadian finance company offering non-dilutive venture debt, SR&ED financing, and tax credit consulting services. |

|

SVB

SVB has lead the technology lending movement for 35 years. The firm opened their first Canadian office last year. |

IN DEFAULT OR ABOVE WATER: How PPP Saved or Didn’t Save America

July 31, 2020 Kristy Kowal, a silver medalist in the 200-meter breast stroke at the 2000 Olympic games in Australia, had recently relocated to Southern California and embarked on a new career when the pandemic shutdown hit in March.

Kristy Kowal, a silver medalist in the 200-meter breast stroke at the 2000 Olympic games in Australia, had recently relocated to Southern California and embarked on a new career when the pandemic shutdown hit in March.

After nearly two decades as a third-grade teacher in Pennsylvania, Kowal was able to take early retirement in 2019 and pursue her dream job. At last, she was self-employed and living in Long Beach where she could now devote herself to putting on swim clinics, training top athletes, and accepting speaking engagements. “I’ve been building up to this for twenty years,” she says.

But fate had a different idea. The coronavirus not only grounded her from travel but closed down most swimming pools. At first, she tried to collect unemployment compensation. But after two months of calling the unemployment office every day, her claim was denied. “‘Have a great day,’ the lady said, and then she hung up,” Kowal reports. “She wasn’t rude; she just hung up.”

Then, in June, the former Olympian heard from friends about Kabbage and the Paycheck Protection Program. Using an app on her smart phone, Kowal says, she was able to upload documents and complete the initial application in fewer than 20 minutes. A subsequent application with a bank followed and within a week she had her money.

“I was down to ten cents in my checking account,” says Kowal, who declined to disclose the amount of PPP money for which she qualified, “and I’d begun dipping into my savings. This gives me the confidence that I need to go back to my fulltime work.”

Kowal is one of 4.9 million small business owners and sole proprietors who, according to the U.S. Small Business Administration, has received potentially forgivable loans under the Paycheck Protection Program. The PPP, a safety-net program designed to pay the wages of employees for small businesses affected by the coronavirus pandemic, is a key component of the $1.76 trillion Coronavirus Aid, Relief, and Economic Security Act (CARES Act). Since the U.S. Congress enacted the law on March 27, the PPP has been renewed and amended twice. It’s now in its third round of funding and Congress is weighing what to do next.

Kowal is one of 4.9 million small business owners and sole proprietors who, according to the U.S. Small Business Administration, has received potentially forgivable loans under the Paycheck Protection Program. The PPP, a safety-net program designed to pay the wages of employees for small businesses affected by the coronavirus pandemic, is a key component of the $1.76 trillion Coronavirus Aid, Relief, and Economic Security Act (CARES Act). Since the U.S. Congress enacted the law on March 27, the PPP has been renewed and amended twice. It’s now in its third round of funding and Congress is weighing what to do next.

Kowal’s experience, meanwhile, is also a wake-up call for the country on the prominent role that both fintechs like Kabbage as well as community and independent banks, credit unions, non-banks and other alternatives to the country’s biggest banks play in supporting small business. Before many in this cohort were deputized by the SBA as full-fledged PPA lenders, a significant chunk of U.S. microbusinesses – especially sole proprietorships — were largely disdained by the brand-name banks.

“After the first round,” notes Karen Mills, former administrator of the U.S. Small Business Administration and a senior fellow at the Harvard Business School, “more institutions were approved that focused on smaller borrowers. These included fintechs and I have to say I’ve been very impressed.”

Among the cadre of fintechs making PPP loans – including Funding Circle, Intuit Quickbooks, OnDeck, PayPal, and Sabre — Kabbage stands out. The Atlanta-based fintech ranked third among all U.S. financial institutions in the number of PPP credits issued, its 209,000 loans trailing only Bank of America’s 335,000 credits and J.P. Morgan Chase’s 260,000, according to the SBA and company data. Kabbage also reports processing more than $5.8 billion in PPP loans to small businesses ranging from restaurants, gyms, and retail stores to zoos, shrimp boats, beekeepers, and toy factories.

To reach businesses in rural communities and small towns, Kabbage collaborated with MountainSeed, an Atlanta-based data-services provider, to process claims for 135 independent banks and credit unions around the U.S. The proof of the pudding: Eighty-nine percent of Kabbage’s PPP loans, says Paul Bernardini, director of communications at Atlanta-based Kabbage, were under $50,000, and half were for less than $13,500.

The figures illustrate not only that Kabbage’s PPP customers were mainly composed of the country’s smaller, “most vulnerable” businesses, Bernardini asserts, but the numbers serve as a reminder that “fintechs play a very important, vital role in small business lending,” he says.

The helpfulness of such financial institutions contrasts sharply with what many small businesses have reported as imperious indifference by the megabanks. Gerri Detweiler, education director at Nav, Inc., a Utah-based online company that aggregates data and acts as a financial matchmaker for small businesses, steered AltFinanceDaily toward critical comments about the big banks made on Nav’s Facebook page. Bank of America, especially, comes in for withering criticism.

“Bank of America wouldn’t even take my application,” one man wrote in a comment edited for brevity. “I have three accounts there. They are always sending me stuff about what an important client I am. But when the going got tough, they wouldn’t even take my application. I’m moving all my business from Bank of America.”

Lamented another Bank of America customer: “I was denied (PPP funding) from Bank of America (where) I have an individual retirement account, personal checking and savings account, two credit cards, a line of credit for $20.000, and a home mortgage. Add in business checking and a business credit card. Yesterday I pulled out my IRA. In the next few days I’m going to change to a credit union.”

Many PPP borrowers who initially got the cold shoulder from multi-billion-dollar conglomerate banks have found refuge with local — often small-town — bankers and financial institutions. Natasha Crosby, a realtor in Richmond, Va., reports that her bank, Capital One, “didn’t have the applications available when the Paycheck Protection Program started” on April 6. And when she finally was able to apply, she notes, “the money ran out.”

Crosby, who is president of Richmond’s LGBTQ Chamber of Commerce, is media savvy and was able to publicize her predicament through television appearances on CNN and CBS, as well as in interviews with such publications as Mother Jones and Huffington Post. A “friendly acquaintance,” she says, referred her to Atlantic Union Bank, a Richmond-based regional bank, where she eventually received a PPP loan “in the high five figures” for her sole proprietorship.

“It took almost two months,” Crosby says. “I was totally frozen out of the program at first.”

Talibah Bayles heads her own firm, TMB Tax and Financial Services, in Birmingham, Ala. where she serves on that city’s Small Business Council and the state’s Black Chamber of Commerce. She told AltFinanceDaily that she’s seen clients who have similarly been decamping to smaller, less impersonal financial institutions. “I have one client who just left Bank of America and another who’s absolutely done with Wells Fargo,” she says. “They’re going to places like America First Credit Union (based in Ogden, Utah) and Hope Credit Union (headquartered in Jackson, Miss.). I myself,” she adds, “shifted my business from Iberia Bank.”

Main Street bankers acknowledge that they are benefiting from the phenomenon. “In speaking to our industry colleagues,” says Tony DiVita, chief operating officer at Bank of Southern California, an $830 million-asset community bank based in San Diego, “we’ve seen that many of the big banks have slowed down or stopped lending small-dollar amounts that were too low for them to expend resources to process.”

Main Street bankers acknowledge that they are benefiting from the phenomenon. “In speaking to our industry colleagues,” says Tony DiVita, chief operating officer at Bank of Southern California, an $830 million-asset community bank based in San Diego, “we’ve seen that many of the big banks have slowed down or stopped lending small-dollar amounts that were too low for them to expend resources to process.”

At the same time, DiVita says, his bank had made 2,634 PPP loans through July 17, roughly 80% of which went to non-clients. Of that number, some 30% have either switched accounts or are in the process of doing so. And, he notes, the bank will get a second crack at conversion when the PPP loan-forgiveness process commences in earnest. “Our guiding spirit is to help these businesses for the continuation of their livelihoods,” he says.

Noah Wilcox, chief executive and chairman of two Minnesota banks, reports that both of his financial institutions have been working with non-customers neglected by bigger banks where many had been longtime customers. At Grand Rapids State Bank, he says, 26% of the 198 PPP applicants who were successfully funded were non-customers. Minnesota Lakes Bank in Delano, handled PPP credits for 274 applicants, of whom 66% were non-customers.

“People who had been customers forever at big banks told us that they had been applying for weeks and were flabbergasted that we were turning those applications around in an hour,” says Wilcox, who is also the current chairman of the Independent Community Bankers of America, a Washington, D.C.-based trade group representing community banks.

Noting that one of his Gopher State banks had successfully secured funding for an elderly PPP borrower “who said he had been at another bank for 69 years and could not get a telephone call returned,” Wilcox added: “We’ve had quite a number of those individuals moving their relationships to us.”

For Chris Hurn, executive director at Fountainhead Commercial Capital, a non-bank SBA lender in Lake Mary, Fla., the psychic rewards have helped compensate for the sometimes 16-hour days he and his staff endured processing and funding PPP applications. “It’s been relentless,” he says of the regimen required to funnel loans to more than 1,300 PPP applicants, “but we’ve gotten glowing e-mails and cards telling us that we’ve saved people’s livelihoods.”

Yet even as the Paycheck Protection Program – which only provides funding for two-and-a-half months – is proving to be immensely helpful, albeit temporarily, there is much trepidation among small businesses over what happens when the government’s spigots run dry. The hastily contrived design of the program, which has relied heavily on the country’s largest financial institutions, has contributed mightily to the program’s flaws.

“The underbanked and those who don’t have banking relationships were frozen out in the first round,” says Sarah Crozier, director of communications at Main Street Alliance, a Washington D.C.-based advocacy organization comprising some 100,000 small businesses. “The new updates were incredibly necessary and long overdue,” she adds, “but the changes didn’t solve the problem of equity in access to the program and whom money is flowing to in the community.”

Professor David Audretsch, an economist at Indiana University’s O’Neill School of Public and Environmental Affairs and an expert on small business, says of PPP: “It’s a short-term fix to keep businesses afloat, but it missed in a lot of ways. It was not well-thought-out and a lot of money went to the wrong people.”

The U.S. unemployment rate stood at 11.1% in June, according to the most recent figures released by the Bureau of Labor Statistics, about three times the rate of February, just before the pandemic hit. The BLS also reported that 47.2% of the U.S. population – nearly half –was jobless in June. Against this backdrop, SBA data on PPP lending released in early July showed that a stunning array of cosseted elite enterprises and organizations, many with close connections to rich and powerful Washington power brokers, have been feasting on the PPP program.

In a stunning number of cases, the program’s recipients have been tony Washington, D.C. law firms, influential lobbyists and think tanks, and even members of Congress. Many businesses with ties to President Trump and Trump donors have also figured prominently on the SBA list of those receiving largesse from the SBA.

Businesses owned by private equity firms, for which the definition of “small business” strains credulity, were also showered with PPP dollars. Bloomberg News reported that upscale health-care businesses in which leveraged-buyout firms held a controlling interest, were impressively adept at accessing PPP money. Among this group were Abry Partners, Silver Oak Service Partners, Gauge Capital, and Heron Capital. (Small businesses are generally defined as enterprises with fewer than 500 employees. The SBA reports that there are 30.7 million small businesses in the U.S. and that they account for roughly 47% of U.S. employment.)

Businesses owned by private equity firms, for which the definition of “small business” strains credulity, were also showered with PPP dollars. Bloomberg News reported that upscale health-care businesses in which leveraged-buyout firms held a controlling interest, were impressively adept at accessing PPP money. Among this group were Abry Partners, Silver Oak Service Partners, Gauge Capital, and Heron Capital. (Small businesses are generally defined as enterprises with fewer than 500 employees. The SBA reports that there are 30.7 million small businesses in the U.S. and that they account for roughly 47% of U.S. employment.)

Boston-based Abry Partners, which currently manages more than $5 billion in capital across its active funds, merits special mention. Among other properties, Abry holds the largest stake in Oliver Street Dermatology Management, recipient of between $5 million and $10 million in potentially forgivable PPP loans. Based in Dallas, Oliver Street ranks among the largest dermatology management practices in the U.S. and, according to a company statement, boasts the most extensive such network in Texas, Kansas and Missouri.

Meanwhile, the design of the program and the formula for the looming forgiveness process is proving impractical. As it currently stands, loan forgiveness depends on businesses spending 60% of PPP money on employees’ wages and health insurance with the remaining 40% earmarked for rent, mortgage or utilities.

Many businesses such as restaurants and bars, storefront retailers and boutiques – particularly those that have shut down — are preferring to let their employees collect unemployment compensation. “Business owners had a hard time wrapping their heads around the requirement of keeping employees on the payroll while they’re closed,” notes Detweiler, the education director at Nav. “They have other bills that have to be paid.”

Many businesses such as restaurants and bars, storefront retailers and boutiques – particularly those that have shut down — are preferring to let their employees collect unemployment compensation. “Business owners had a hard time wrapping their heads around the requirement of keeping employees on the payroll while they’re closed,” notes Detweiler, the education director at Nav. “They have other bills that have to be paid.”

The forgiveness formula remains vexing for businesses where real estate costs are exorbitant, particularly in high-rent cities such as New York, Boston, Washington, D.C., San Francisco, and Chicago. Tyler Balliet, the founder and owner of Rose Mansion, a midtown Manhattan wine-bar promising an extravagant, theme-park experience for wine enthusiasts, says that it took him a month and a half to receive almost $500,000 from Chase Bank. Unfortunately, though, the money isn’t doing him much good.

“I have 100 employees on staff, most of whom are actors,” he says. “We shut down on March 13. I laid off 95 employees and kept just a few people to keep the lights on.”

At the same time, his annual rent tops $1 million and the forgivable amount in the PPP loans won’t even cover a month’s rent. “I haven’t paid rent since March and I’m in default,” Balliet says. “Now I’m just waiting to see what the landlord wants to do.”

Like many business owners, Balliet financed much of his venture with credit card debt, which creates an additional liability concern, notes Crozier of the Main Street Alliance. “It’s very common for borrowers to have signed personal guarantees in their loans using their credit cards,” she says. “As we get closer to the funding cliff and as rent moratoriums end,” she adds, “creditors are coming after borrowers and putting their personal homes at risk.”

Mark Frier is the owner of three restaurants in Vermont ski towns, including The Reservoir — his flagship — in Waterbury. In toto, his eateries chalked up $6.5 million in combined sales in 2019. But 2020 is far different: the restaurants have not been open since mid-March and he’s missed out on the lucrative, end-of-season ski rush.

Consequently, Frier has been reluctant to draw down much of the $750,000 in PPP money he’d secured through local financial institutions. “We could end up with $600,000 in debt even with the new rules,” Frier says, adding: “We live off very thin margins. We need grants not loans.”

As the country recorded 3.7 million confirmed cases of coronavirus and more than 141,000 deaths as of mid-July, PPP money earmarked by businesses for health-related spending was not deemed forgivable. Yet in order to comply with regulations promulgated by the Occupational Safety and Health Administration and mandates and ordinances imposed by state and local governments, many establishments will be unable to avoid such expenditures.

“What we really needed was a grant program for companies to pivot to a business environment in a pandemic,” says Crozier. She cites the necessity businesspeople face of “retrofitting their businesses, buying masks, gloves and sanitizers and cleaning supplies, restaurants’ taking out tables and knocking down walls, installing Plexiglass shields, and improving air filtration systems.”

Meanwhile, as Covid-19 was taking its toll in sickness and death, the economic outlook for small business has been looking dire as well. The recent U.S. Census’s “Pulse Survey” of some 885,000 businesses updated on July 2 found that roughly 83% reported that Covid-19 pandemic had a “negative effect on their business. Fully 38% of all small business respondents, moreover, reported a “large negative effect.”

Meanwhile, as Covid-19 was taking its toll in sickness and death, the economic outlook for small business has been looking dire as well. The recent U.S. Census’s “Pulse Survey” of some 885,000 businesses updated on July 2 found that roughly 83% reported that Covid-19 pandemic had a “negative effect on their business. Fully 38% of all small business respondents, moreover, reported a “large negative effect.”

Amid the unabated spikes in the number of coronavirus cases and the country’s grave economic distress, PPP recipients are faced with the unsettling approach of the PPP forgiveness process. As Congress, the SBA, and the U.S. Treasury Department continue to remake and revise the rules and regulations governing the program, businesses are operating in a climate of uncertainty as well. Currently, the law states that the amount of the PPP loan that fails to be forgiven will convert to a five-year, one-percent loan — a relaxation in terms from the original two-year loan which is not necessarily cheering recipients.

“One of the biggest problems with PPP is that the rule book has been unclear,” frets Vermont restaurateur Frier, glumly adding: “This is not even a good loan program.”

Ashley Harrington, senior counsel at the Center for Responsible Lending, a research and policy group based in Durham, N.C., argued in House committee testimony on June 17, that there ought to be automatic forgiveness for PPP loans under $100,000. Such a policy, she declared, “would likely exempt firms with, on average, 13 or fewer employees and save 71 million hours of small business staff time.”

She also said, “The smallest PPP loans are being provided to microbusinesses and sole proprietors that have the least capacity and resources to engage in a complex (forgiveness) process with their financial institution and the SBA.”

William Phelan, president of Skokie (Ill.)-based PayNet, a credit-data services company for small businesses which recently merged with Equifax, sounded a similar note. Observing that there are some 23 million “non-employer” small businesses in the U.S. with fewer than three employees for whom the forgiveness process will likely be burdensome, he says: “Estimates are that it will cost businesses a few thousand dollars just to get a $100,000 loan forgiven. It’s going to involve mounds of paper work.”

The country’s major challenge now will be to re-boot the economy, Phelan adds, which will require massive financing for small businesses. “The fact is that access to capital for small businesses is still behind the times,” Phelan says. “At the end of the day, it took a massive government program to insure that there’s enough capital available for half of the U.S. economy” during the pandemic.

For his part, Professor Audretsch fervently hopes that the country has learned some profound lessons about the need to prepare for not just a rainy day, but a rainy season. The pandemic, he says, has exposed how decades of political attacks on government spending for disaster-preparedness and safety-net programs have left the U.S. exposed to unforeseen emergencies.

“We’re seeing the consequence of not investing in our infrastructure,” he says. “That’s a vague word but we need a policy apparatus in place so that the calvary can come riding in. This pandemic reminds me a lot of when Hurricane Katrina hit New Orleans,’ he adds. “The city paid a heavy price because we didn’t have the infrastructure to deal with it.”

The Aftermath: What Industry Experts Had to Say About The Future Alignment of People and Data

July 20, 2020

Like never before, the ways in which people and data are employed are overlapping more in a post-covid economy. Nearly three months of slow-down and, in some cases, complete economic shutdown have forced brokers and funders alike to view businesses differently than before. New documents, metrics, and terms are being incorporated into underwriting with the belief that it will provide a much more comprehensive picture of each business applying for funding.

Broker Fair Virtual took the chance to explore these new perspectives in The Aftermath, a panel featuring Moshe Kazimirsky, VP of Strategic Partnerships and Business Development at Become; Heather Francis, CEO of Elevate Funding; and David Snitkof, Head of Analytics at Ocrolus. Here, the industry experts discussed what the future of data and people may look like, what the new things that funders are looking out for are, and how the coronavirus has changed consumer and merchant behavior.

First up was Heather Francis, who gave a run down of how Elevate has adapted to the constantly shifting environment created by covid-19. “There were slim pickings on what we could fund,” Francis noted of the early lockdown period. Explaining that many businesses didn’t fit their criteria in the early days of lockdown, Elevate began the process of including new metrics and lenses through which to ascertain if businesses were financially viable.

National, state, and local restrictions became a daily check-in, rather than monthly; with one person being assigned to cover changes in local and even county regulations. As well as this, Francis explained that the company shifted its focus from underwriting the business owner’s activity to underwriting the consumers’ activity. This meant that foot traffic was constantly reviewed via FourSquare, trends that showed which industries were seeing upticks and downturns were monitored, and what customers in varying geographies were comfortable with was gauged.

“There are some areas in our country that were not heavily impacted,” Francis explained, commenting on the discrepancies between locations, particularly for bars and restaurants. “I know some of us have our optics on what’s going on in our daily lives, and a lot of people in our space are located in New York or California, and these were the very heavily regulated areas where everything was shut down and there was not much to do. Here in Florida, it was easier, with open-seating dining.”

David Snitkof echoed Francis’s points, saying that “the old way of businesses underwriting credit is no longer sufficient … If you were to only look at people’s repayment histories, their credit profiles, and things like that, you wouldn’t get all the data you need to make the right decision. Generally there’s this idea that the past is prologue and the greatest predictor of future results is past behavior, and this type of pandemic makes that no longer the case … we need to think beyond the traditional data sets that people have used to underwrite credit.”

According to Snitkof, the old models for underwriting and funding have been overturned, with funders adhering to three principals going forward as they chart new methods: more data, more time, more detail. This means incorporating more data and analytics than before, pushing for more data-driven strategies; requesting information and data from merchants that cover longer periods of time, with the hope of gaining further insight into the pattern of the business; and upping the thoroughness with which each merchant is scrutinized, recording more information that is unique to their industry, location, and business management.

“Lenders will realize that in order to make a credit decision, we need to have access to very deep, detailed, and wide time-framed data of our customers; and we need to be able to process it in an automated and efficient way,” Snitkof asserted.

Still, while it looks like data is due to play a larger role in the future, Heather Francis took care to mention that important data is currently missing from their metrics. Credit and delinquency reporting are on hold, just as rent is paused for many tenants; meaning that in two or three months, many funders could be in for a surprise when they realize their merchant is having trouble.

Speaking on the Paycheck Protection Program as well as the Economic Injury Disaster Loan, both Snitkof and Francis expressed that while it is good to see deposits for the government programs, questions must be asked regarding them. They can’t be viewed as revenue, since they do not reflect a business’s ability to generate revenue, said Snitkof, but rather they offer a chance to view how a company manages its cash-flow, with how they spread out PPP and EIDL funds being a key insight.

Speaking on the Paycheck Protection Program as well as the Economic Injury Disaster Loan, both Snitkof and Francis expressed that while it is good to see deposits for the government programs, questions must be asked regarding them. They can’t be viewed as revenue, since they do not reflect a business’s ability to generate revenue, said Snitkof, but rather they offer a chance to view how a company manages its cash-flow, with how they spread out PPP and EIDL funds being a key insight.

Looking forward, the panelists noted that the experiences of economic shutdown; PPP; EIDL; and how many business owners’ banks supported, or did not support, them could lead to a shift in how non-banks are viewed.

“It’s definitely a time and place for us to really highlight how our industry is placed to assist small businesses,” Francis stated. “We should really take this opportunity to expand on what we can do and how we can help. I think it’s our moment to shine because a lot of banks have pulled back on what they’re able to do in this time.”

This pulling back by banks became clear during the peak of the PPP application period, when many business owners complained of a lack of or poor communication between themselves and the bank they applied to. Highlighting the importance of the customer experience, Snitkof pointed out that this aspect of alternative finance may only become more important as time goes on.

“We have this golden age of customer service. Customers are going to demand good funding, on the right terms, with full transparency, with good speed of decisioning, with a good relationship, and if they can get that from someone who is not a bank, but is an alternative finance provider, then that’s a great funding scenario for them.”

More generally though, the panel ended on a note of ambiguity over the future, with the speakers agreeing that what comes next will be uncertain and challenging, as Francis reminded the audience of what 2020 has in store: a presidential election and a possible second wave of the novel coronavirus.

But there may also be opportunity for those who are there to take it, according to Snitkof, who finished off by saying that “the silver lining of what we’ve just been through as a country, as a world, as an industry, is that all those things that were good enough, they were on pause. So it’s given people the time and space to reimagine what they could do and actually look at the capabilities that we’ve available to us and say ‘maybe we can provide a great personalized customer experience to every small business and customer out there. Maybe we can be more automated and data-driven in our decisions. Maybe we can actually extend better terms on financing to people because we’re able to determine risk better, and optimize our market spend and cost of capital better.’ One of the good things about a disruption is it takes away a lot of the stuff that was good enough; a lot of those sacred cows are now ready to be disrupted and maybe in a few years we’ll see rapid innovation along those lines.”

CFG Merchant Solutions Enhances Partnership with Arena Investors and its Affiliates to Serve SMEs

May 29, 2020NEW YORK, New York., May 29, 2020 — CFG Merchant Solutions (“CFGMS”), a leading financier of small and medium-sized enterprises (“SMEs”), announced today that the company is building upon its partnership with Arena Investors, LP (“Arena”), in conjunction with Ceteris Portfolio Services (“Ceteris), an Arena servicing affiliate, in servicing and providing liquidity to Platinum Rapid Funding’s (“PRF”) merchant portfolio. CFGMS has been a leading capital provider to SMEs and an originator of advances to growing merchants, providing in excess of $400 million merchant cash advances since 2015. Arena has been CFGMS’s primary capital partner since 2016.

CFGMS and Arena are determined to prioritize the needs of PRF’s existing customers in the wake of the COVID-19 crises and its resulting impact on small businesses across the country.

“Arena is pleased to continue its partnership with CFGMS and its senior management team consisting of CEO, Andrew Coon, Chief Legal Officer and General Counsel, Robert Martini, and President, William Gallagher. Together, we remain deeply committed to serving the needs of PRF’s existing customers, particularly for ongoing financing and liquidity needs in an environment when even much larger businesses struggle to attract capital,” said Victor Dupont, who leads Arena’s investments in the financing of the SME sector. “We welcome further involvement with PRF’s customers and their affiliated ISOs and are committed to working collaboratively with all throughout the COVID-19 crises and beyond”.

“Arena and its affiliates have built a reputation as a group that combines uniquely flexible capital with broad-based expertise in servicing, resolutions, and SME finance,” said Coon. “So, while we excel at sourcing, originations, and underwriting, we felt that they brought a critical level of IP and know-how that is uniquely suited to benefit all parties in today’s environment. Combining forces to offer a broader set of servicing solutions to the MCA market segment made complete sense.”

Jonathan Pike, CEO of Ceteris, added: “Ceteris is excited to work with CFGMS and Arena by offering best-in-class servicing strategies and assisting merchants in a difficult economic environment.”

The Small Business Association (“SBA”) estimates that traditional banks still reject approximately 90 percent of SME loan applications. Since 2015, CFGMS has emerged as a proven platform that leverages sales partner relationships, analytics, and proprietary underwriting to provide SMEs with a straightforward and streamlined access to critical funding. The company addresses the fundamental capital needs of SME owners across a broad credit spectrum and through every stage of a business’s life cycle.

SMEs across a wide variety of industries that include restaurants, retail stores, salons, spas, dry cleaners, auto body shops, and professional offices. All of these businesses, and more, rely on CFGMS to secure the necessary capital they need to grow.

For questions or funding solutions, please contact:

– William Gallagher

– (646) 880-3817

– WGallagher@CFGMS.com

– Ryan Banda

– (856) 545-8322

– rbanda@ceterisassetsolutions.com

About CFGMS

Headquartered in New York, NY, CFGMS specializes in providing financing to support the growth and development of underserved small-to-medium sized businesses that lack access to traditional bank funding. Founded in 2010, CFGMS’s affiliated company, CapFlow Funding Group, provides factoring, purchase order finance, and asset-based lending solutions. CFGMS and CapFlow have together provided over $1 billion in liquidity solutions to their SME clients. For more information please visit www.cfgmerchantsolutions.com

About Arena Investors, LP

Arena Investors is a privately held, SEC-registered, global alternative investment firm which combines mandate flexibility, proprietary sourcing and systems-plus-servicing to enable solutions for those seeking capital. The firm was founded in 2015 and is headquartered in NewYork with additional offices in Jacksonville, London, and San Francisco. For more information, please visit www.arenaco.com.

About Ceteris Portfolio Services

Ceteris is a nationally licensed servicing company providing debt recovery solutions and other related services for consumers and commercial businesses across a broad range of financial assets. Ceteris provides first- and third-party revenue cycle management, business process outsourcing and portfolio backup servicing to heavily regulated, high volume industries including banking, automotive finance, credit card, equipment leasing, medical, telecommunications, utilities, retail and other industries. For more information please visit www.ceterisholdco.com.

Income Share Agreements – Operating Under Current Regulations and Preparing for the Future

February 28, 2020The Income Share Agreement (“ISA”) market is rapidly developing with more providers offering ISA programs to students and outside money moving into the space. However, the legal environment remains uncertain, and providers entering the ISA market must prepare themselves both to operate in the current environment and for potential changes.

Background – What is an Income Share Agreement?

ISA providers have set a modest goal: disrupt the $1.6 trillion-dollar student loan market that has wreaked havoc on a generation’s finances by aligning the interests of students and providers. In an ISA transaction, the student does not owe a specific amount of money and no interest is charged on a balance. Instead, the student agrees to pay a proportion of their future income above a specified threshold for a certain number of years. The provider of an ISA has an interest in the student consistently earning a high income for the duration of the contract—because the ISA provider generally does not get paid if the student fails to earn sufficient income.

Evolving Legal Environment

The current legal environment has not yet adapted to ISAs entering the market for funding education and associated expenses. No federal statute directly addresses ISAs and only one state—Illinois—has passed legislation contemplating ISAs. Even that legislation (the Student Loan Investment Act) merely permits a state investment fund to enter into ISAs and does not impact the private ISA market.

California and Washington have both considered legislation related to ISAs, but neither passed anything into law. Indiana’s legislature exempted certain “State educational institutions” from its Uniform Consumer Credit Code, including leading ISA provider Purdue University. However, Indiana did not expressly address ISAs under the UCCC.

No federal or state courts have published cases analyzing the treatment of ISAs under state or federal credit laws. But federal regulators appear to be aware of this issue. In a December 2019 discussion paper on ISAs released by the Federal Reserve Bank of Philadelphia, the authors acknowledged the uncertainty created by the lack of authoritative statements from courts and regulators, but did not weigh in on the legal issues.

Careful Consideration Required

When considering compliance with state and federal laws in this uncertain environment, participants must first assess which laws may apply. For state laws, if an educational institution is entering an ISA with a student, the institution must consider licensing, disclosures, and other restrictions applicable under state installment sales acts. Third-party providers must consider the application of lender licenses and associated disclosures and restrictions.

In either case, providers must consider the application of the Truth in Lending Act (“TILA”), the Equal Credit Opportunity Act (“ECOA”), the Credit Practices Rule, state laws governing the assignment of wages, and generally applicable state and federal laws, such as laws governing unfair and deceptive acts and practices and certain anti-discrimination laws.

Careful analysis of each statute, implementing regulation, and associated commentary provides some initial guidance. For example, TILA’s Regulation Z commentary excludes an “investment plan” where the party extending capital to the consumer risks the loss of capital advanced from the definition of “credit” under the Truth in Lending Act. 12 CFR 1026.2(14) cmt. 1(viii). However, participants must carefully consider with their counsel whether the Regulation Z exclusion is intended to only apply to traditional equity investments because they are not debt, or if it more broadly excludes investments that do not create an absolute obligation to pay.

Additionally, the definition of “credit” under ECOA in Regulation B not only lacks a similar comment, but also includes a comment stating that Regulation B “covers a wider range of credit transactions than Regulation Z.” 12 CFR 1002.2(j) cmt. 1. Although the Regulation B comment arguably only refers to ECOA’s coverage of commercial credit and credit regardless of the number of installments or inclusion of a finance charge, this is one example of how providers must carefully consider each potentially applicable law.

Merely assuming that laws applicable to credit do not apply to an ostensibly non-credit product without conducting an appropriate analysis creates serious regulatory risks.

Potential Federal Changes

In 2017, Senators Rubio and Young introduced the Student Success Act, and in 2019, Senators Warner and Coons joined them with a more robust ISA Student Protection Act of 2019 (the “Act”). The Act proposes a number of important steps. First, it proposes substantive consumer protection rules on ISAs and defines a “qualified ISA” to include only ISAs meeting those substantive requirements. Second, the Act would expressly preempt state laws affecting the validity of a qualified ISA, in addition to state usury, ability to pay, and licensing laws for qualified ISAs. Third, the Act would clarify the treatment of ISAs under federal credit, security, and tax laws, and empower the CFPB to promulgate certain guidance and regulations.

However, that Act has not become law and it is unclear if, or how, lawmakers will address the issue in the future. For example, in response to reports that the U.S. Department of Education was exploring offering ISAs, Senator Warren questioned whether ISAs were “in the best interest of students,” stating they could be “predatory and dangerous.”

Conclusion

The market for ISAs continues to grow, and it’s easy to see why. Given the growing student lending crisis, the presence of an alternative has significant potential. However, due to the current regulatory uncertainty, market participants must carefully weigh the legal risks.

Caleb Rosenberg is an associate in the Maryland office of Hudson Cook, LLP. Caleb can be reached at 410-782-2323 or by email at crosenberg@hudco.com.

The End Of An Era – AltFinanceDaily Through The Decade

December 30, 2019

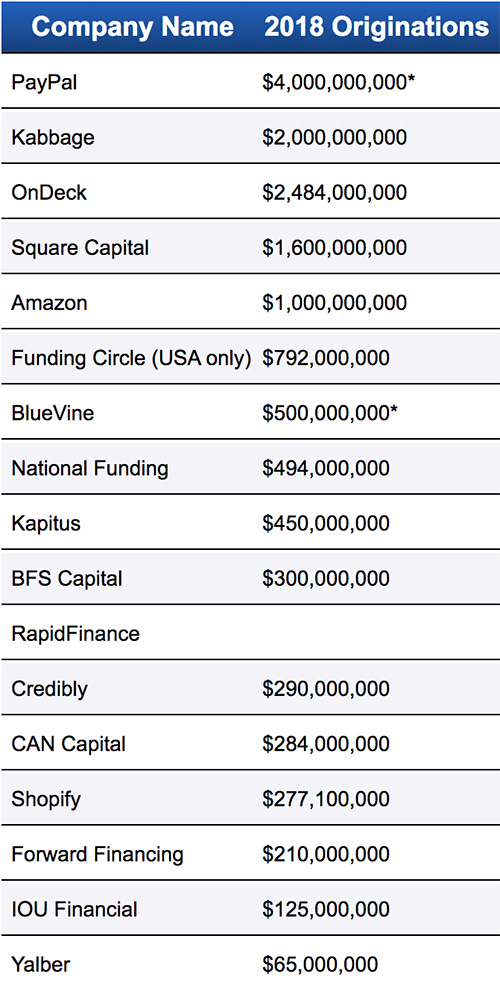

AltFinanceDaily estimated that approximately $524 million worth of merchant cash advances had been funded in 2010.

In 2019, merchant cash advances and daily payment small business loan products exceed more than $20 billion a year in originations.

First Funds

Merchant Cash and Capital

Business Financial Services

AmeriMerchant

Greystone Business Resources

Strategic Funding Source

Fast Capital

Sterling Funding

iFunds

Kabbage

OnDeck

Square Capital

Amazon Lending

Funding Circle USA

Yellowstone Capital

Entrust Cash Advance

Merchants Capital Access

Merchant Resources International

American Finance Solutions

Nations Advance

Bankcard Funding

Rapid Capital Funding

Paramount Merchant Funding

CAN Capital Announces New CCO

October 15, 2019We are proud to announce that we have hired David Lafferty as CAN Capital’s new Chief Credit Officer (CCO.) Lafferty brings his expertise in commercial lending, business development, operational planning and profit & loss management to the CAN Capital team.

Lafferty has over twenty years of proven experience providing financial services to small businesses. He is the former Vice President of Capital Markets and Credit and Risk Management at Marlin Business Bank. In that role, he has assisted small businesses in obtaining the capital they need to operate and grow, with a special focus on helping businesses finance the lease or purchase of equipment. Lafferty is a graduate of Pennsylvania State University, and a member of the Equipment Leasing and Financing Association (ELFA) Small Ticket Advisory Council.

“I have focused my entire career on serving the small business owner as they are the backbone of the United States economy. Being given the opportunity to join this team in a time when the company is experiencing rapid growth and gaining significant market share is extremely exciting. I am really looking forward to joining an already very talented workforce as we take CAN Capital to the next level,” said Lafferty.

Ed Siciliano, CAN’s CEO, had this to say about the new hire: “I’m very excited to welcome Dave to CAN Capital. He will be joining a strong group of talented people focused on Risk and Credit Underwriting and applying his deep experience in small business lending to calibrate CAN’s 20-year proven credit models. We all welcome Dave and feel fortunate to have him join.”

A Philadelphia native who now resides in New Jersey, Lafferty is the proud father of twin sons. When he isn’t helping small businesses succeed, you’ll find Lafferty golfing or riding motorcycles, or on the water boating and fishing in Punta Gorda Isles, Florida.

Please join us in welcoming new CCO David Lafferty, who, along with our dedicated group of CAN Capital team members, is ready to support our mission of helping every small business succeed.

About CAN Capital

CAN Capital, Inc., established in 1998, is the pioneer in alternative small business finance, having provided access to over $7 billion in capital for over 81,000 small businesses in a wide range of locations and different business types. As a technology powered financial services provider, CAN Capital uses innovative and proprietary risk models combined with daily performance data to evaluate business performance and facilitate access to capital for entrepreneurs in a fast and efficient way.

CAN Capital, Inc. makes capital available to businesses through business loans made by WebBank, member FDIC, and through Merchant Cash Advances made by CAN Capital’s subsidiary CAN Capital Merchant Services, Inc. ©2019 CAN Capital. All rights reserved

Media Contact: Carey Kirk, 678-858-6911, ckirk@cancapital.com